- Food Packaging

- Food and Beverage Packaging Market

Food and Beverage Packaging Market Size, Share, and Growth Forecast, 2025 - 2032

Food and Beverage Packaging Market by Product Type (Rigid, Semi-rigid, Flexible), Packaging Type (Bottles and Jars, Caps and Closures, Cans, Cartons, Pouches and Sachets), Application (Beverages, Dairy Products, Processed Food, Poultry and Seafood, Confectionery and Bakery Products), and Regional Analysis for 2025 - 2032

Food and Beverage Packaging Market Size and Trends Analysis

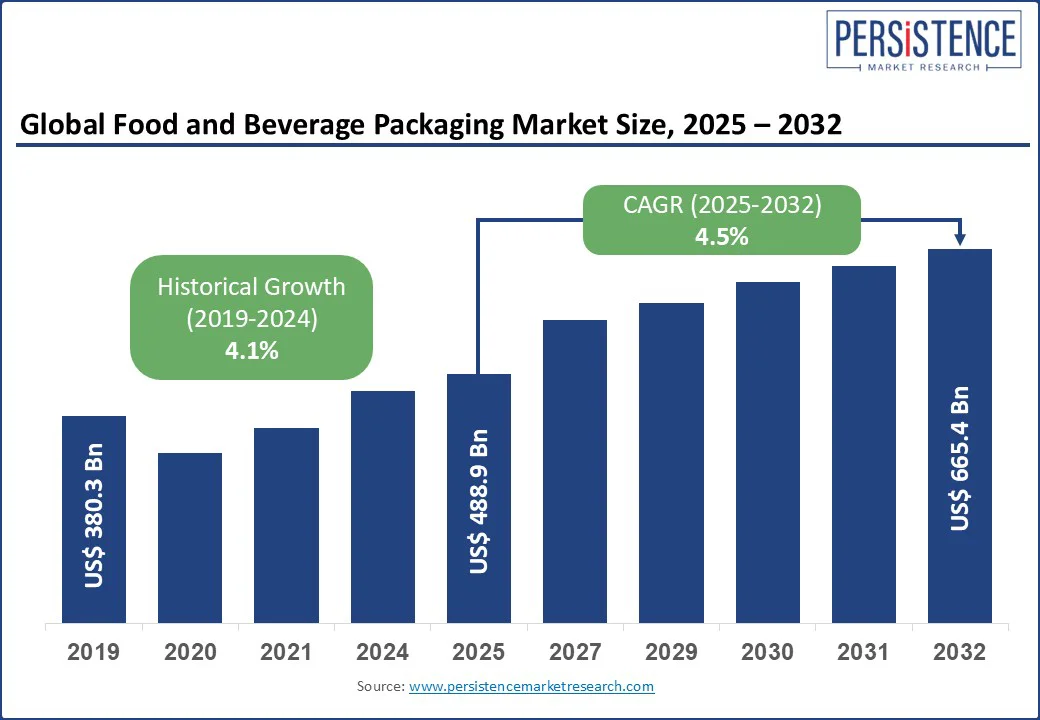

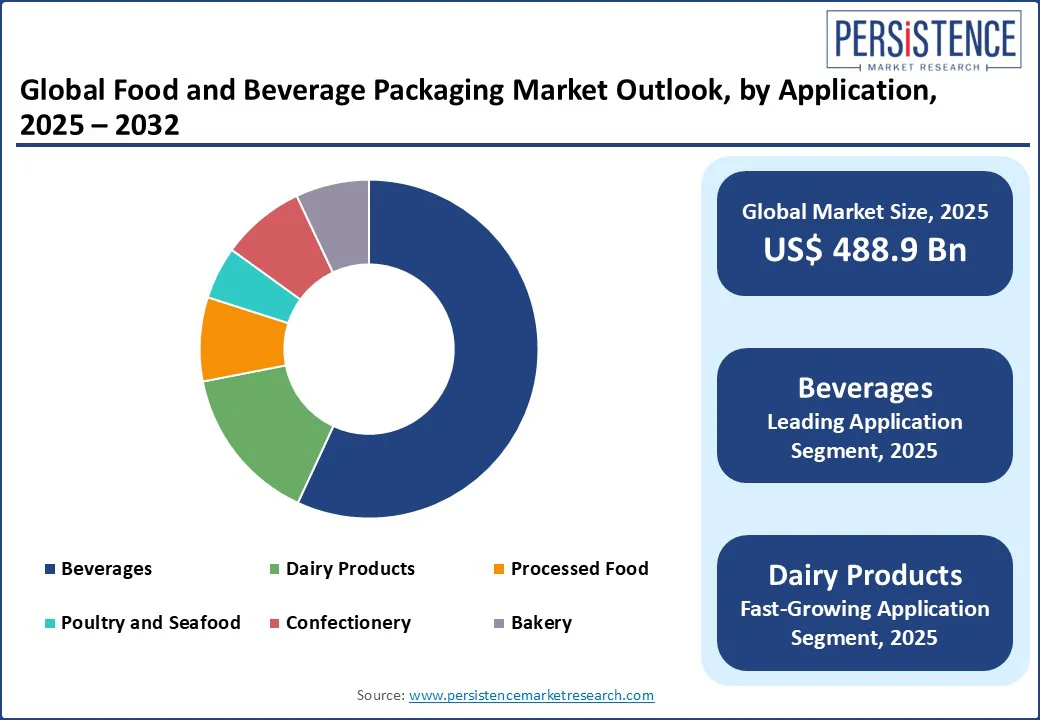

The global Food and Beverage Packaging Market is projected to grow from US$ 488.95 Bn in 2025 to US$ 665.4 Bn by 2032, achieving a robust CAGR of 4.5% during the forecast period. This market has seen substantial growth, fueled by the rising demand for convenient, sustainable, and innovative packaging solutions that cater to evolving consumer preferences and global supply chain requirements. The sector is driven by increasing consumption of packaged food and beverages, advancements in packaging technologies, and a growing emphasis on sustainability to meet stringent environmental regulations.

Key Industry Highlights:

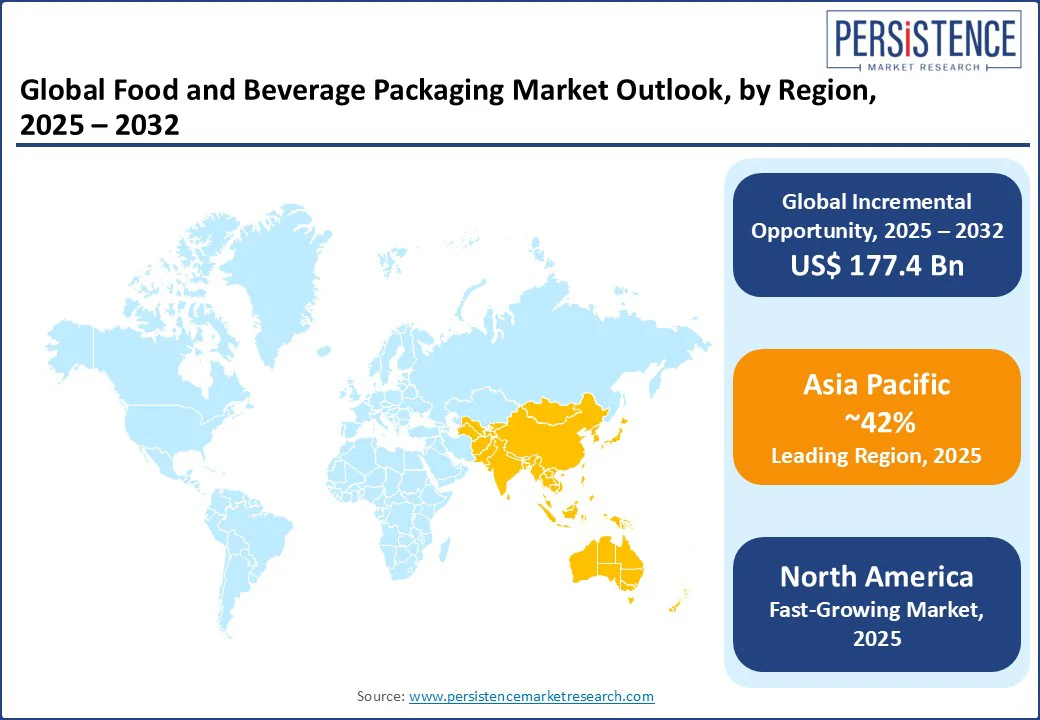

- Leading Region: Asia Pacific, commanding a 42% market share in 2025, driven by rapid urbanization, a booming food and beverage industry, and increasing disposable incomes fueling packaged goods consumption.

- Fastest-growing Region: North America, propelled by e-commerce growth, consumer demand for sustainable packaging, and advancements in food safety regulations. Europe is advancing through initiatives such as the EU’s Circular Economy Action Plan, with significant investments in sustainable packaging technologies.

- Dominant Product Type: Flexible packaging, holding a 55.60% market share, due to its lightweight nature, cost-effectiveness, and suitability for diverse food applications.

- Leading Application: Beverages, accounting for over 56.78% of market revenue, driven by the global demand for bottled water, soft drinks, and alcoholic beverages.

- Historical Growth: The sector registered a CAGR of 4.1% from 2019 to 2024, driven by rising demand for convenient and eco-friendly packaging solutions.

|

Key Insights |

Details |

|

Food and Beverage Packaging Market Size (2025E) |

US$ 488.95 Bn |

|

Market Value Forecast (2032F) |

US$ 665.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.1% |

Market Dynamics

Driver- Surge in Quick-Service Restaurants and Food Delivery Demand

The exponential growth of quick-service restaurants (QSRs) and food delivery services is a pivotal driver of the food and beverage packaging market. The rise in on-the-go consumption and online food ordering has significantly increased the demand for reliable, convenient, and sustainable packaging solutions to ensure product safety and quality during transit. Flexible packaging, such as bags and pouches, is particularly favored for its lightweight, durable, and customizable properties, making it ideal for delivering a wide range of food products, from snacks to ready-to-eat meals. Leading food delivery platforms are increasingly using flexible packaging to meet logistical demands.

For instance, companies such as Zomato and Swiggy in India have partnered with sustainable packaging providers to introduce compostable and recyclable containers for restaurant partners, aiming to reduce single-use plastic consumption. Additionally, government policies promoting sustainable packaging, such as the EU’s single-use plastic ban and India’s Extended Producer Responsibility (EPR) framework, have encouraged QSRs and food delivery platforms to adopt recyclable and biodegradable packaging solutions. The affordability and scalability of these packaging types further support their widespread adoption, making them a preferred choice in the fast-paced food and beverage industry.

Restraint: Volatility in Raw Material Costs

Fluctuating raw material prices, particularly for plastics, paper, and aluminum, pose a significant restraint on the food and beverage packaging market. Raw materials represent a substantial portion of production costs, making the industry highly susceptible to price volatility. Factors such as global demand for raw materials, supply chain disruptions due to geopolitical tensions, and environmental regulations limiting resource extraction contribute to these fluctuations.

For instance, a recent surge in the price of recycled plastic resins, driven by shortages and logistical bottlenecks in Asia, has impacted manufacturers’ profit margins. The food and beverage packaging industry is also energy-intensive, relying heavily on electricity for processes such as extrusion, molding, and printing. Rising energy costs, particularly in Europe and parts of Asia, further increase operational expenses, limiting scalability for small and mid-sized producers and affecting their competitiveness in the industry. For instance, several packaging firms in Germany and Italy have reported temporary production slowdowns due to high energy tariffs, forcing them to reassess pricing strategies and reduce output volumes.

Opportunity: Advancements in Sustainable Packaging Technologies

The growing emphasis on sustainability presents a significant opportunity for the food and beverage packaging market. Innovations in eco-friendly materials, such as biodegradable films, plant-based plastics, and recyclable paper-based packaging, enable manufacturers to meet stringent environmental regulations while maintaining product integrity.

For instance, in 2024, Amcor plc introduced a fully recyclable, high-barrier flexible packaging solution for dairy products, reducing reliance on non-recyclable laminates. This aligns with the global push for circular economies, encouraging the use of sustainable packaging materials. Advancements in digital printing technologies also allow high-resolution, customizable designs on packaging surfaces, enhancing brand visibility for food and beverage companies. For instance, Nestlé adopted digitally printed flexible packaging for its snack products, improving both aesthetics and recyclability. These developments position sustainable packaging as a key driver for market expansion across developed and emerging economies.

Category-wise Analysis

Product Type Insights

Flexible packaging dominates the sector, expected to hold a 55.60% share in 2025. Its dominance is attributed to its lightweight design, cost-effectiveness, and versatility across applications such as snacks, dairy, and beverages. Flexible packaging, including pouches and sachets, reduces material usage and transportation costs, making it ideal for e-commerce and retail.

Rigid packaging is the fastest-growing segment from 2025 to 2032, driven by increasing demand for durable containers such as bottles, jars, and cans in beverages and processed foods. Rigid packaging offers superior protection for high-value products and aligns with consumer preferences for premium, reusable packaging, particularly in developed markets.

Packaging Type insights

Bottles and Jars lead the domain, accounting for 30.15% of revenue in 2025. Their widespread use in beverages, such as bottled water, soft drinks, and alcoholic beverages, drives their dominance. The durability and recyclability of glass and PET bottles make them a preferred choice for manufacturers and consumers.

Pouches and Sachets are the fastest-growing segment, fueled by their convenience, portability, and sustainability. The rise of single-serve and resealable pouches for snacks, sauces, and baby food is accelerating their adoption, particularly in urban markets and e-commerce.

Application Insights

Beverages led the food and beverage packaging market, accounting for over 56.78% of market revenue in 2025. The segment’s dominance is driven by the global surge in demand for bottled water, soft drinks, alcoholic beverages, and functional drinks. The rise in health-conscious consumers and the popularity of premium beverages, such as craft beers and organic juices, further fuel the need for innovative and sustainable packaging solutions.

Dairy Products are the fastest-growing application segment, driven by increasing global consumption of milk, yogurt, and cheese, particularly in emerging markets. The demand for sterile, tamper-proof, and eco-friendly packaging to ensure product safety and extend shelf life is accelerating the adoption of advanced packaging solutions in this segment. Regulatory requirements for food safety and sustainability further drive growth in dairy packaging.

Regional Insights

North America Food and Beverage Packaging Market Trends

North America is the fastest-growing region in the global food and beverage packaging market, with the United States and Canada leading the charge. The U.S. market is driven by the rapid expansion of e-commerce, increasing demand for convenient and sustainable packaging, and stringent food safety regulations.

The rise of online grocery shopping and meal delivery services has boosted the need for durable and protective packaging to ensure product integrity during transit. Additionally, consumer awareness of environmental issues has led to a shift toward recyclable and biodegradable packaging materials, supported by regulations such as the U.S. FDA’s food safety guidelines. The U.S. holds a dominant position in the region, with ongoing investments in smart packaging technologies and circular economy initiatives driving sustained growth through 2032.

Europe Food and Beverage Packaging Market Trends

Europe holds the second-largest share in the global food and beverage packaging market, driven by strong sustainability initiatives, advanced manufacturing capabilities, and the growing adoption of food delivery services. Leading countries include Germany, the UK, and France. Germany benefits from its advanced industrial base and leadership in sustainable packaging, with companies investing heavily in recyclable solutions.

The UK’s market is bolstered by the rapid growth of food delivery and initiatives promoting alternatives to single-use plastics. France’s market is supported by significant investments in sustainable packaging innovation. The EU’s stringent regulations, such as the Packaging and Packaging Waste Directive, drive the adoption of eco-friendly packaging solutions, though compliance with complex environmental laws poses challenges. Europe’s food and beverage packaging market is projected to grow steadily from 2025 to 2032.

Asia Pacific Food and Beverage Packaging Market Trends

Asia Pacific dominates the global food and beverage packaging market, accounting for over 42% of total revenue in 2025. This leadership is driven by high industrial activity in countries such as China, India, and Japan, which fuels demand for packaging solutions for both domestic and export markets.

The rapid growth of e-commerce, particularly in China and India, has increased the need for durable and sustainable packaging for last-mile delivery. Rising urbanization, growing middle-class populations, and increasing disposable incomes are boosting the consumption of packaged food and beverages, further driving demand. China leads the market, supported by its vast manufacturing ecosystem and significant export volumes, while India’s market is fueled by government initiatives promoting sustainable packaging and a growing food processing industry. The region’s commitment to sustainability aligns with global circular economy objectives.

Competitive Landscape

The food and beverage packaging market is characterized by intense competition, regional dynamics, and a blend of global and local manufacturers. In mature markets such as North America and Europe, major players such as Amcor plc, Tetra Pak International S.A., and Sealed Air Corporation lead the industry through large-scale operations, advanced packaging technologies, and longstanding partnerships with leading food and beverage brands. In the Asia Pacific, rapid urbanization, rising consumption, and expanding food delivery networks are attracting substantial investments from both domestic and international firms. Companies across regions are prioritizing sustainability, cost-efficiency, and product customization to strengthen their market positions. Automation and digital printing technologies have become key enablers, supporting mass personalization and improved production efficiency. Strategic alliances and increased R&D efforts in eco-friendly and recyclable materials are further intensifying competition and shaping future innovations in the sector.

Key Developments

- In September 2022, Amcor plc acquired a European flexible packaging facility, enhancing its production capabilities for food and beverage Packaging Types.

- In May 2022, Tetra Pak committed USD 250 million toward expanding its carton manufacturing operations in Asia, aiming to meet the rising demand for sustainable beverage packaging.

- June 2024: Crocco partnered with Versalis to develop food packaging film made from recycled post-consumer plastics. Utilizing Versalis’ Balance material, the packaging maintains essential food safety and performance standards. This collaboration highlights the importance of diversified raw materials and strategic partnerships in advancing circular economy goals.

Companies Covered in Food and Beverage Packaging Market

- WestRock

- Bemis Company

- Silgan Holdings

- Ardagh Group

- Crown Holding

- Smurfit Kappa

- Amcor

- Sonoco Products

- Mondi Group

- Greif

- Ball Corporation

- Owens-Illinois

- Huhtamaki

- Jindal Aluminium

- Tetra Pak

- Others

Frequently Asked Questions

The Food and Beverage Packaging market is projected to reach US$ 488.95 Bn in 2025.

The surge in demand for sustainable packaging solutions and the growth of e-commerce are key drivers.

The Food and Beverage Packaging market is poised to witness a CAGR of 4.5% from 2025 to 2032.

Advancements in smart packaging technologies offer significant growth opportunities.

WestRock, Amcor, Smurfit Kappa, Tetra Pak, and Crown Holdings are among the key players.