- Food Packaging

- Nutraceutical Rigid Packaging Market

Nutraceutical Rigid Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Nutraceutical Rigid Packaging Market By Product Type (Bottles & Jars, Blisters & Strips, Others), Material (Plastics, Glass, Others), Application and Regional Analysis for 2026 - 2033

Nutraceutical Rigid Packaging Market Size and Trends Analysis

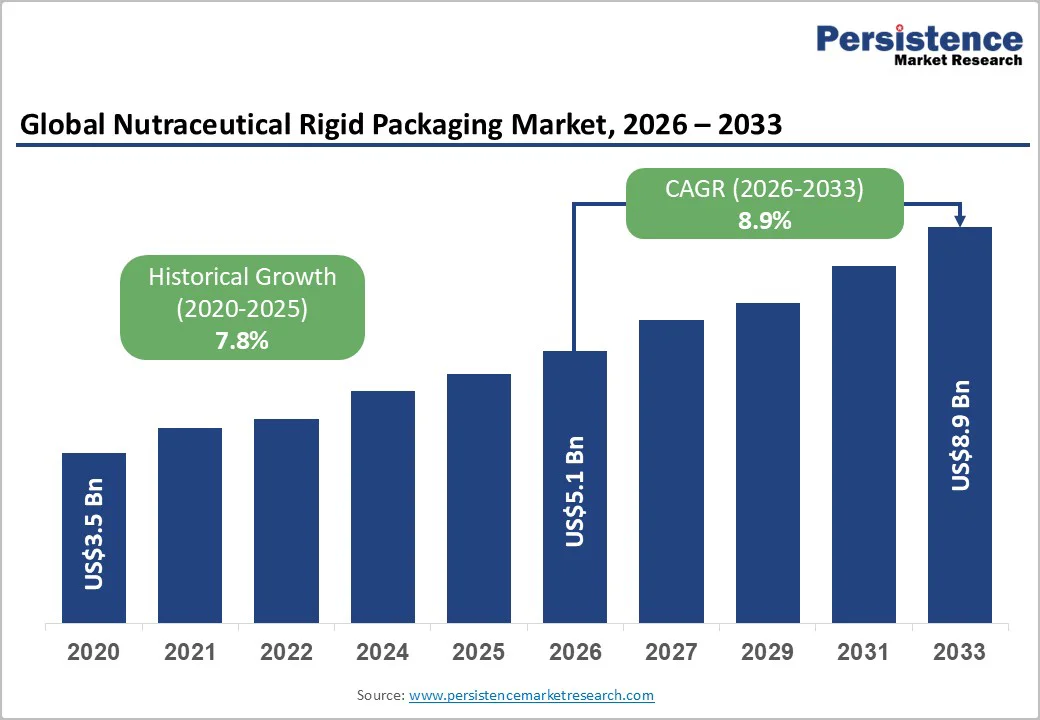

The global nutraceutical rigid packaging market is likely to be valued at US$5.1 billion in 2026 and is expected to reach US$8.9 billion by 2033, indicating an approximate CAGR of 8.3% between 2026 and 2033.

Growth is supported by rising global demand for dietary supplements and functional foods, premiumization trends, and accelerating adoption of sustainable, high-barrier rigid materials. Regulatory pressures, child-safety requirements, and elevated raw material costs continue to influence strategic decisions across the packaging value chain.

Key Industry Highlights

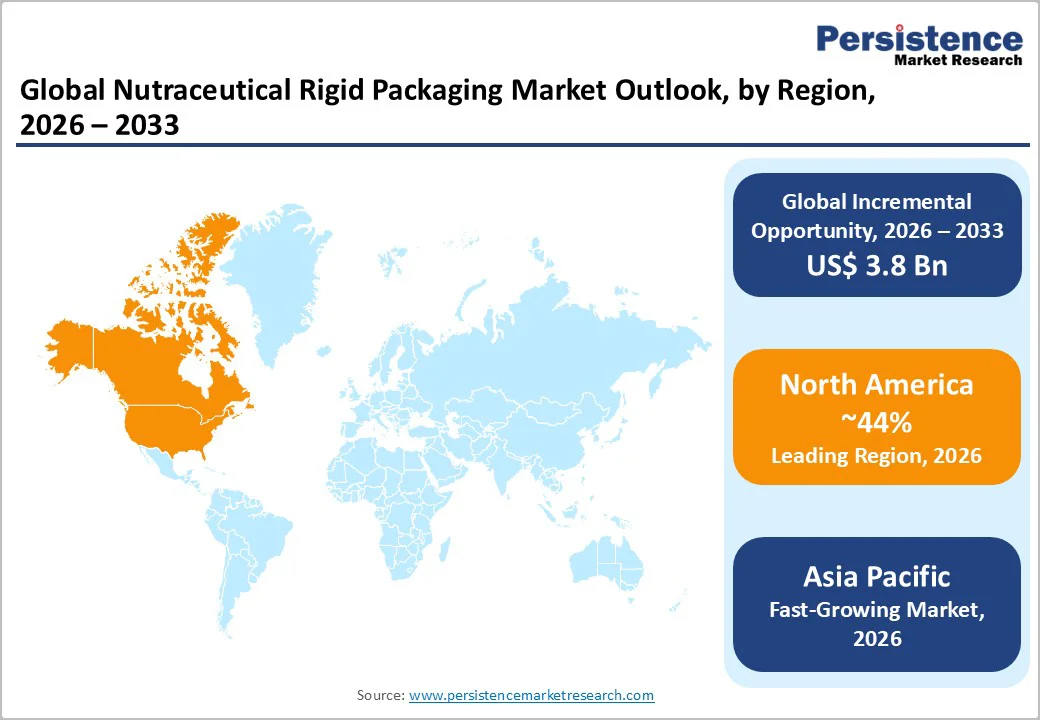

- Leading Region: North America, holding approximately 44% of the global nutraceutical rigid packaging market, driven by stringent FDA standards, widespread supplement adoption, and advanced packaging infrastructure.

- Fastest-growing Region: Asia Pacific, projected to record the highest CAGR due to large-scale nutraceutical consumption in China and India, expanding manufacturing capacity, and rapid e-commerce penetration.

- Investment Plans: Strong industry-wide investment momentum toward mono-material PET, lightweight glass, PCR-enriched HDPE, and high-barrier composite structures, supported by capacity expansions from suppliers including Amcor, Stoelzle, UFlex, and Shandong Pharmaceutical Glass.

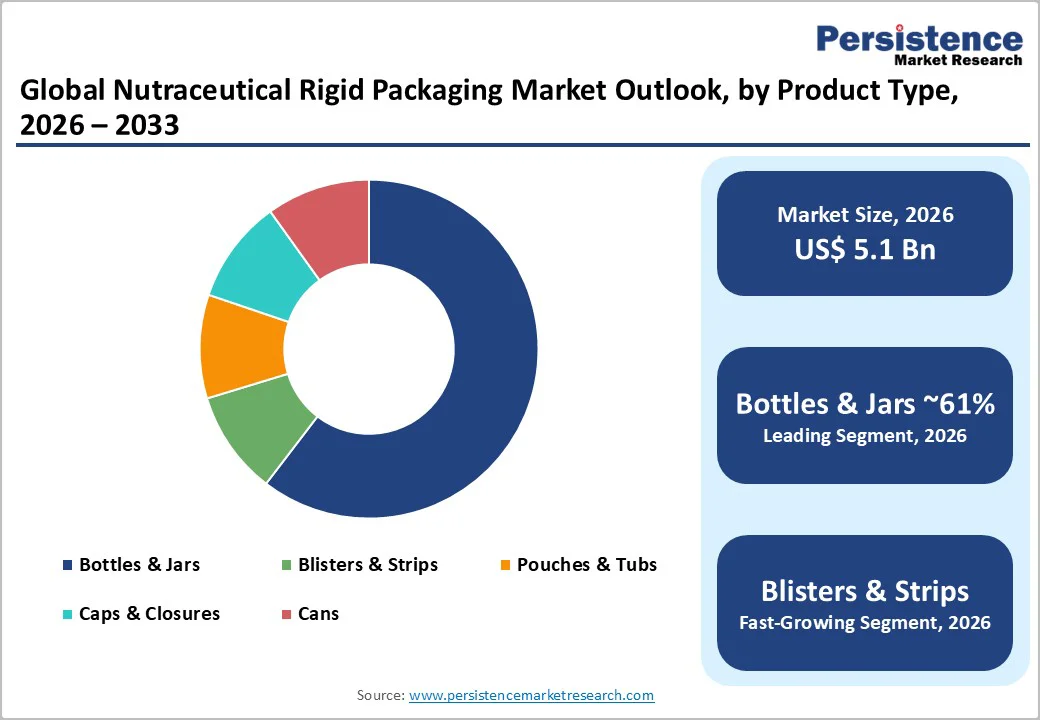

- Dominant Material Type: Plastics, contributing nearly 50% of total market value, led by PET, HDPE, and PP formats widely used for capsules, tablets, gummies, and powdered supplements.

- Leading Product Type: Bottles and Jars, accounting for 61% of global nutraceutical rigid packaging value, supported by high-volume usage in vitamins, gummies, and sports-nutrition powders.

| Key Insights | Details |

|---|---|

| Nutraceutical Rigid Packaging Market Size (2026E) | US$5.1 Bn |

| Market Value Forecast (2033F) | US$8.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growing Global Nutraceutical Demand and Premiumization

Demand for supplements, vitamins, and functional foods continues to rise as aging demographics and preventive healthcare trends strengthen worldwide. Reported CAGRs for the broader nutraceutical packaging sector fall within the mid-single-digit range, supporting expanded usage of rigid packaging formats such as bottles, jars, and blister systems.

Rigid packaging is favored for capsules and tablets because it offers strong moisture and oxygen barriers, enhanced dosing accuracy, and tamper evidence. This dynamic increases unit consumption for rigid formats and accelerates innovation in high-barrier plastics and advanced closure systems.

Regulatory and Quality Requirements Favoring Rigid Packaging

Nutraceuticals must adhere to stringent safety, labeling, and contamination-control standards, especially in markets that treat these products as quasi-pharmaceutical. Rigid packaging formats are selected to meet child-resistant closure rules, validated barrier requirements, and traceability expectations.

Updated safety regulations in major markets continue to increase demand for certified high-barrier rigid containers and validated tamper-evident closures. This results in higher specification requirements and premium positioning for established, compliant rigid-packaging suppliers.

Sustainability and Recyclability Mandates Accelerating Rigid-Format Innovation

Governments and retailers now emphasize recyclable or recycle-ready packaging, driving investments in mono-material bottle systems, reclaimable PET, recyclable HDPE solutions, and glass formats. Sustainable packaging categories exhibit CAGRs notably higher than the general packaging average, encouraging rapid R&D across rigid packaging lines.

The effect is a dual-track market where high-performance barrier formats continue to grow while recyclable rigid alternatives capture increasing share.

Raw Material and Logistics Cost Volatility

Fluctuating prices for polymers, metals, and specialty barrier laminates place pressure on profit margins. Bio-based or sustainable alternatives often carry a cost premium and may require equipment adjustments, raising capital expenditure for packaging manufacturers. This slows the adoption pace of eco-friendly materials for cost-sensitive brands, leading to uneven regional uptake.

The variability in feedstock pricing also complicates long-term planning for both suppliers and nutraceutical producers.

Complex Certification and Compliance Requirements

Nutraceutical rigid packaging frequently requires simultaneous compliance with food-grade, pharmaceutical-adjacent, and environmental safety standards. Child-resistant closures, migration testing, barrier verification, and labeling compliance extend development timelines and raise pre-production costs. Smaller nutraceutical brands face barriers to market entry due to the expense of validated custom rigid formats and extended product-testing cycles.

Retrofitting For Recyclable Mono-Material Rigid Systems

Extended Producer Responsibility (EPR) rules and retailer sustainability requirements are accelerating the conversion of multi-layer rigid formats to mono-material or mechanically recyclable systems. Recycle-ready PET bottles, HDPE mono-materials, and lightweight glass represent major opportunities for suppliers capable of offering scalable, compliant solutions.

Based on industry projections, sustainable rigid formats could represent a significant share of total rigid-packaging spending by 2030, creating strong long-term growth potential.

E-Commerce-Optimized Rigid Packaging

The rise of direct-to-consumer subscription models and online retail increases demand for rigid formats that withstand handling, stacking, and shipping stresses. Lightweight, impact-resistant rigid containers with reclosable closures reduce return rates and product damage during transport.

Brands increasingly invest in upgraded rigid packaging to improve unit economics and shelf-presentation in digital storefronts, creating opportunities for suppliers that specialize in durable, e-commerce-ready rigid formats.

Category-wise Analysis

Product Type Insights

Bottles and jars are anticipated to account for 61% of the total market share, making them the most widely adopted formats for dietary supplements and functional nutrition. Their structural strength, familiar dosing experience, and compatibility with safety features such as tamper-evident bands and CRC systems solidify their dominant position.

Plastic bottles remain essential for capsules, tablets, gummies, and powdered supplements, especially across high-volume retail and e-commerce channels where durability during transport is crucial. HDPE bottles are standard for multivitamins and mineral tablets marketed by Centrum, One A Day, and Kirkland Signature.

PET jars are preferred for gummy supplements due to their clarity and shelf impact, commonly used by brands such as Olly and Vitafusion. Rigid PP jars serve sports-nutrition powders across global brands, including Optimum Nutrition, MuscleTech, and MyProtein, where structural stiffness and wide-mouth openings support efficient scooping and dispensing.

The integration of digital features like QR-coded labels and near-field communication (NFC) tags for authentication is also growing in premium product lines.

Blister and strips packaging formats are expanding rapidly due to their strong stability performance and consumer-friendly portability. Blisters provide precise dose protection by isolating each tablet or capsule from ambient air and humidity until consumption. This makes them ideal for probiotics, herbal tablets, enzyme formulations, and dissolvable strips that deteriorate quickly when exposed to moisture.

The rise of on-the-go nutrition trends is accelerating the use of single-dose formats, especially in North America and Asia. PVC-aluminum blister packs remain common for herbal tablets and botanical blends, while high-barrier aluminum-aluminum (alu-alu) blisters are increasingly used for probiotics and high-potency capsules requiring extended shelf life.

Brands such as Himalaya, Nature’s Bounty, Amway’s Nutrilite, and Swiss premium supplement makers frequently use blisters for botanical and condition-specific nutraceuticals. Strips and melt-in-mouth nutrition films are also growing within energy, immunity, and sleep-aid categories, supported by improvements in push-through film technology and recyclable blister materials introduced by global suppliers like Huhtamaki and UFlex.

Material Type Insights

Plastics such as PET, HDPE, and PP continue to dominate nutraceutical rigid packaging, expected to contribute over 50% of the total market share. Their leadership is reinforced by a combination of high cost-efficiency, excellent impact resistance, lightweight handling, and reliable moisture-oxygen barrier performance that matches stability requirements for capsules, tablets, and powdered supplements.

These materials also support advanced packaging features, including child-resistant closures, tamper-evident bands, and shrink-sleeve labels that enhance safety and on-shelf differentiation. Rapid moldability enables brands to create unique silhouettes and premium aesthetics without significant tooling complexity.

In practice, PET bottles are extensively used for vitamin C and immunity-boosting tablet formats, while HDPE canisters dominate protein powders, collagen blends, and mass-market multivitamins due to their rigidity and compatibility with induction sealing.

PP is widely adopted for closures and specialty CRC caps used by brands such as Nature Made for its vitamin bottle range, GNC for its sports-nutrition packaging, and Herbalife for high-volume powder tubs. Large packaging suppliers such as Berry Global, Amcor, and ALPLA continue to expand portfolios of PCR (post-consumer recycled) PET and HDPE formats, supporting sustainability requirements in the United States and Europe.

Glass and advanced composite materials represent the fastest-growing category, driven by a shift toward premium, clean-label, and sensitive formulations. Glass packaging appeals to brands emphasizing purity and chemical inertness, and its inherent UV protection makes it suitable for light-sensitive antioxidant blends, essential oil-based nutraceuticals, liposomal formulations, and high-potency herbal extracts.

Growth is reinforced by rising adoption of glass bottles for probiotics in both cold-chain and ambient-stable formats, especially in Europe and Japan. High-barrier composite structures are also gaining momentum for niche applications that require elevated moisture control or oxygen impermeability.

These include multilayer cans for effervescent tablets, desiccant-integrated composite containers for adaptogenic blends, and heavily laminated structures used for hygroscopic herbal formulations. Amber glass bottles used for omega-3 oils, tinted glass for turmeric curcumin drops, and multilayer composite tubes for vitamin B12 sprays are increasingly visible in product lines from NOW Foods, Solgar, Garden of Life, and premium Japanese functional-food brands.

Regional Insights

North America Nutraceutical Rigid Packaging Market Trends- Advanced Infrastructure, Premium Formats, and Material Innovation

North America remains one of the largest and most commercially influential markets, anticipated to hold 44% of market share, supported by high supplement intake across adult and active-lifestyle groups and well-developed retail and e-commerce channels.

The U.S. continues to lead the region due to its advanced packaging infrastructure, strong adoption of child-resistant closures, and strict FDA requirements addressing product identity, strength, purity, and packaging integrity. Premium rigid formats are gaining market traction as brands increasingly seek enhanced shelf stability and improved aesthetics that align with consumer expectations for professional-grade nutraceutical products.

Investment momentum is shifting toward mono-material PET containers, lightweight glass bottles, RFID-enabled closures, and recyclable HDPE formats. Collaboration between packaging suppliers and nutraceutical brands remains strong, with contract manufacturers providing automated filling capabilities, CRC-cap integration, and high-speed induction sealing systems that support consistent quality and scalability.

Recent developments illustrate this trend, including Amcor’s introduction of a PCR-enriched PET bottle line for U.S. supplement manufacturers in February 2025, Gerresheimer’s expansion of glass-bottle production capacity at its Indiana facility in July 2024, and Berry Global’s March 2025 partnership with a California-based supplement company to launch lightweight HDPE bottles designed for e-commerce durability and reduced material consumption.

Europe Nutraceutical Rigid Packaging Market Trends- Sustainability-Driven Regulations and High-Purity Premium Packaging

Europe functions as a high-value, regulation-driven market shaped by stringent sustainability mandates, advanced recycling targets, and strong consumer demand for premium-quality packaging. Core markets such as Germany, France, the U.K., Italy, and Spain maintain robust nutraceutical consumption levels while supporting highly developed rigid-packaging manufacturing ecosystems.

Sustainability-oriented regulatory frameworks, including the EU Packaging and Packaging Waste Regulation (PPWR), encourage the adoption of mono-material formats, lightweight glass, high-clarity PET, and high-barrier composite structures suitable for botanical extracts and sensitive nutraceutical ingredients.

Consumer preference for clean-label, responsibly sourced, and environmentally aligned packaging materials continues to influence product development strategies among nutraceutical brands. European packaging suppliers are also investing heavily in circular-economy infrastructure and digital traceability technologies to support recyclability and supply-chain transparency.

Recent advancements in this region include Stoelzle Glass Group’s May 2025 expansion of its Czech facility to increase amber and flint bottle production for premium herbal-extract brands, Huhtamaki’s October 2024 launch of recyclable paper-aluminum hybrid blisters for vitamin and probiotic formulations, and Alpla’s January 2025 increase in rPET conversion capacity in Germany to address growing demand for higher recycled content in rigid bottles.

Asia Pacific Nutraceutical Rigid Packaging Market Trends- Rapid Growth, High-Capacity Production, and E-Commerce-Ready Formats

Asia Pacific continues to be the fastest-growing region in the nutraceutical rigid packaging market, supported by rising consumer health awareness, growing supplement adoption among middle-class populations, and the rapid expansion of regional nutraceutical manufacturing hubs.

China and India underpin much of the region’s volume due to extensive production capabilities, competitive packaging supply chains, and strong export-oriented contract manufacturing ecosystems. Japan remains a premium market with high demand for precision-designed glass containers, child-resistant systems, and specialized rigid formats suitable for functional beverages, probiotic drops, herbal concentrates, and high-potency extracts.

The quick expansion of e-commerce and cross-border nutraceutical sales strengthens the need for lightweight, durable rigid packaging that withstands extended logistics chains. Manufacturers in the region are investing in high-capacity PET and HDPE bottling lines, advanced composite structures for effervescent tablets, and fully recyclable rigid formats aligned with evolving sustainability mandates in nations such as Japan, South Korea, Australia, and India.

Recent developments highlight continued capacity building, including Shandong Pharmaceutical Glass’s April 2025 expansion of amber-glass bottle production to meet rising domestic and export demand for probiotics and herbal extracts, UFlex’s August 2024 introduction of high-barrier composite canisters for moisture-sensitive Ayurvedic formulations in India, and Nipro Pharma Packaging’s June 2025 upgrades to its Japanese facilities to support growing demand for premium nutraceutical oils and liquid supplements.

Competitive Landscape

The global nutraceutical rigid packaging sector is moderately consolidated at the top, dominated by global suppliers offering integrated solutions across materials, preforms, closures, and compliance testing.

Below this tier, the market remains fragmented, with mid-sized regional manufacturers supplying glass containers, closures, and specialized rigid solutions. Plastics command the largest volume share, while glass and specialty closures represent higher-value segments.

Key industry strategies include innovation in recyclable rigid formats, vertical integration across materials and closures, adoption of circular-economy models, and the development of e-commerce-optimized rigid packaging.

Key Industry Developments

- In January 2025, West Pharmaceutical Services introduced its new Daikyo PLASCAP® Ready-to-Use Validated (RUV) closures in a nested format (6×8 tub configuration) compatible with standard 13 mm and 20 mm vial crowns, aiming to streamline fill-finish operations for advanced therapeutics and biologics.

- In March 2025, West Pharmaceutical Services reported strong growth in its stopper and plunger-seal segment, reflecting elevated demand for premium containment systems and validating its strategic focus on high-performance elastomeric materials and assembly efficiency.

Companies Covered in Nutraceutical Rigid Packaging Market

- Amcor plc

- Berry Global Inc.

- Gerresheimer AG

- Alpla Group

- Stoelzle Glass Group

- AptarGroup Inc.

- WestRock Company

- Silgan Holdings Inc.

- Ardagh Group

- TricorBraun

- Winpak Ltd.

- Comar LLC

- O-I Glass Inc.

- Huhtamaki Oyj

- Nipro Pharma Packaging

- UFlex Limited

- Shandong Pharmaceutical Glass Co. Ltd.

- Plastic Ingenuity Inc.

- Pretium Packaging

- Weener Plastics Group

Frequently Asked Questions

The market size is estimated to reach US$5.1 billion in 2026.

By 2033, the market value is projected to reach US$8.9 billion.

Major industry trends include growing demand for sustainable rigid formats (PCR PET, lightweight glass, mono-material HDPE), increasing use of child-resistant and tamper-evident systems, rapid growth in premium bottles and blisters for probiotics and botanical extracts, and rising integration of e-commerce-friendly packaging designs.

Plastics remain the leading material segment, contributing the highest market share due to cost efficiency, barrier performance, and suitability for capsules, tablets, gummies, and powders. In product types, bottles and jars represent the dominant format across global supplement categories.

The market is projected to grow at a CAGR of 8.9% between 2026 and 2033.

Leading companies with strong manufacturing portfolios and global presence include Amcor plc, Berry Global Inc., Gerresheimer AG, Alpla Group, and Stoelzle Glass Group.