- Medical Devices

- Tissue Processing System Market

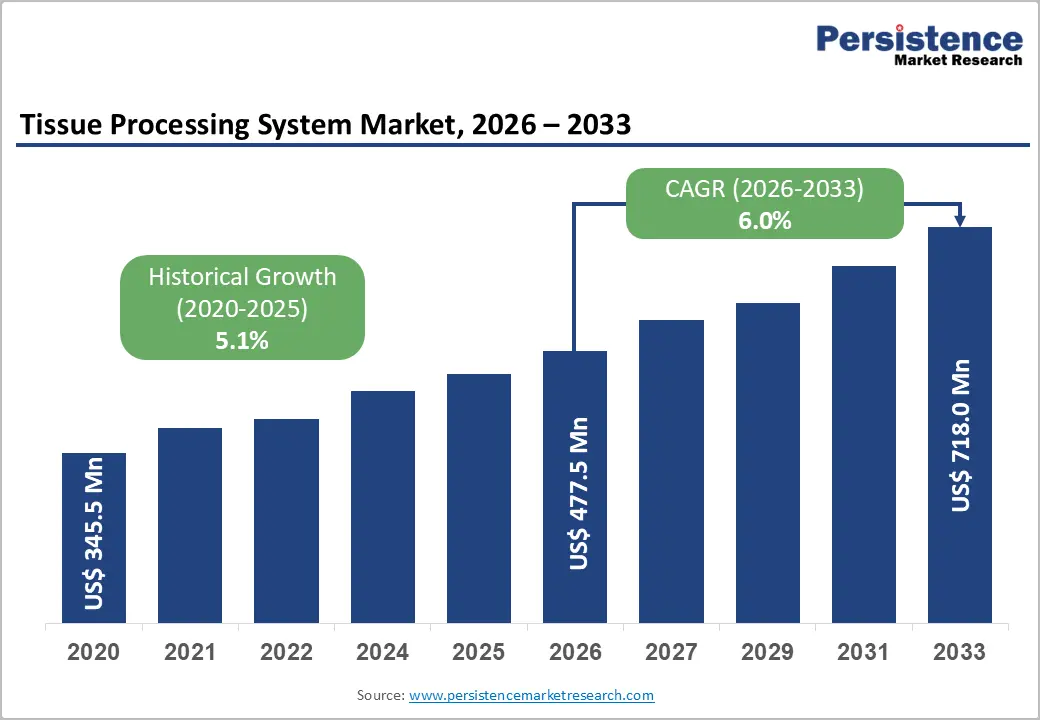

Tissue Processing System Market Size, Trends, Share, Growth, and Regional Forecast, 2026 - 2033

Tissue Processing System Market by Product Type (Small Volume Tissue Processors, Medium Volume Tissue Processors, Rapid High Volume Tissue Processors), Modality (Stand-Alone, Bench-Top), Technology (Microwave Tissue Processors, Vacuum Tissue Processors), End-user (Hospitals, Diagnostic Laboratories, Others), and Regional Analysis from 2026 - 2033

Tissue Processing System Market Share and Trends Analysis

The global tissue processing system market size is likely to be valued at US$ 477.5 million in 2026 to US$ 718.0 million by 2033, growing at a CAGR of 6.0% during the forecast period from 2026 to 2033.

The global market is expanding steadily, fueled by rising biopsy volumes, growing demand for automated histology, and hospital infrastructure upgrades. North America leads due to advanced healthcare systems and high adoption of automated tissue processors. Asia Pacific is the fastest-growing region, driven by expanding laboratory capacity, rising diagnostic demand, and significant healthcare investments.

Key Industry Highlights:

- Dominant Segment: Rapid high-volume tissue processors lead with 41.6% share in 2025, driven by high throughput, automation, and efficiency. Small and medium volume processors grow steadily.

- Dominant Region: North America holds the largest share 40.2% due to advanced labs, high biopsy volumes, and strong adoption of automated tissue processors. Asia Pacific is the fastest-growing region, supported by expanding diagnostic facilities and healthcare investments.

- Growth Indicators: Growth is driven by rising biopsy volumes, increasing demand for automated and integrated tissue processing, lab modernization, and the need for faster turnaround times.

- Market Opportunity: Key opportunities include the adoption of fully automated and high-throughput processors, integration with digital pathology workflows, expansion in emerging markets, and demand for multi-modality compatible systems.

| Key Insights | Details |

|---|---|

|

Tissue Processing System Market Size (2026E) |

US$ 477.5 Mn |

|

Market Value Forecast (2033F) |

US$ 718.0 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

6.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.1% |

Market Dynamics

Driver - Rising Prevalence of Chronic Diseases and Cancer

The rising prevalence of chronic diseases, particularly cancer, is a fundamental driver of the tissue processing system market because diagnostic workflows increasingly rely on histopathological examination of biopsy tissue. According to the World Health Organization, chronic non-communicable diseases account for about 74% of global deaths, with cancer a major contributor. Globally, new cancer cases were nearly 20 million in 2022, and projections indicate continued growth in incidence through 2030 as populations age. Early and accurate tissue diagnosis is essential for staging and treatment planning, directly increasing demand for advanced tissue processors in hospitals and labs worldwide

Cancer represents a significant and expanding public health burden that drives pathology workloads. For example, India saw over 1.46 million new cancer cases in 2022, with incidence projected to rise further, emphasizing the need for robust diagnostic infrastructure. Pathology and cancer registries in the United States collect extensive tissue pathology data, underscoring the role of biopsy and histological analysis in clinical care. As chronic diseases like cancer increase, so do procedures requiring tissue processing for diagnosis, personalized treatment decisions, and monitoring. This escalating diagnostic demand directly stimulates investment in automated and high-throughput tissue processing systems.

Restraints - Stringent Regulatory Requirements

Stringent regulatory requirements for medical devices, including tissue processing systems, significantly constrain market growth by increasing complexity, approval time, and cost for manufacturers. In major jurisdictions such as the United States and European Union, regulatory pathways demand extensive premarket evaluation, quality system audits, clinical evidence, and ongoing postmarket surveillance, which lengthen time-to-market. For example, the U.S. FDA’s 510(k) clearance process averages 140–175 days and frequently exceeds its 90-day target, while EU conformity under MDR can take up to 18 months or more due to rigorous clinical and documentation demands

These regulatory burdens translate into higher development costs and delayed product launches, directly impacting innovation and competitive dynamics within the Tissue Processing System Market. Surveys indicate that over 70% of medical device manufacturers allocate increased resources to meet regulatory compliance, exacerbating financial and administrative strain. In the EU, the transition to MDR has left millions of legacy devices awaiting new certification, underscoring bottlenecks and approval backlogs. This environment particularly hampers small and medium enterprises, which face disproportionate barriers in navigating complex requirements, often resulting in deferred market entry or withdrawal of devices, a key restraint on market expansion.

Opportunity - Adoption of Compact and High?Throughput Systems

The adoption of compact and high-throughput tissue processing systems is a key opportunity for the Tissue Processing System Market because laboratories face increasing sample volumes that traditional manual methods cannot efficiently handle. In histology and cytology workflows, over 62% of tissue samples are already processed using automated systems, reflecting a broad industry movement toward automation to improve consistency and reduce errors. Automated processors enable labs to process multiple samples simultaneously with standardized protocols, improving throughput and turnaround time, an essential advantage as pathology workloads grow with rising biopsy volumes. Compact and benchtop automated solutions allow smaller facilities to adopt these efficiencies without large capital investments.

Rising pathology workloads underscore the value of high-throughput adoption. In the United States alone, millions of biopsies and over 350 million anatomic pathology tests are performed annually, reflecting substantial demand for tissue analysis. Histology labs handling large caseloads increasingly integrate automation to manage these volumes while maintaining quality and turnaround time. Digital pathology adoption is already present in many major labs, further driving the need for systems that can deliver high-volume, reliable processing. The growth of compact, automated processors presents an opportunity for broader market penetration, especially among smaller labs and regional centers that previously lacked capacity for high-throughput workflows.

Category-wise Analysis

By Product Type, Small Volume Tissue Processors Dominate the Tissue Processing System Market

The hydraulic power source occupied 41.6% share in 2025. They are ideally suited for smaller laboratories, hospital-based labs, and research facilities that handle moderate biopsy and diagnostic specimen volumes. In the U.S., for example, over 200,000 clinical laboratories operate, many of which are small-scale facilities requiring compact, cost-effective tissue processors that fit limited space and budgets while ensuring reliable and consistent results.

Globally, histology workflows process hundreds of millions of tissue samples annually, and small-volume systems allow efficient handling of these batches with automation, reducing manual errors and improving turnaround times. Their adaptability, affordability, and suitability for routine diagnostics across decentralized labs make them the leading product segment in the market.

By Modality, Stand-Alone is gaining traction due to high throughput, automation, and compliance with large lab requirements

Stand-alone tissue processing systems dominate the market because they serve the needs of large hospitals, centralized pathology labs, and high-throughput diagnostic centers that handle the majority of surgical and biopsy workflows. In the United States, for example, there are over 6,000 hospitals that perform inpatient and outpatient procedures requiring histopathology, and centralized labs often process thousands of specimens per day, necessitating robust, standalone systems with greater capacity and automation.

Stand-alone units typically offer higher throughput, more program flexibility, and better integration with other laboratory instruments, which supports compliance with quality standards such as CLIA (Clinical Laboratory Improvement Amendments) and CAP (College of American Pathologists) accreditation requirements. These factors make stand-alone processors the preferred choice in environments with heavy specimen volumes, contributing to their leading market share.

Regional Insights

North America Tissue Processing System Market Trends

North America dominates the tissue processing system market with 40.2% share in 2025, due to its advanced healthcare infrastructure, high biopsy and diagnostic testing volumes, and early adoption of automated technologies. In the U.S. alone, over 620 million laboratory tests are performed annually, representing roughly 34% of global testing volumes, creating significant demand for efficient tissue-processing workflows. Large hospital networks, centralized pathology laboratories, and reference centers increasingly rely on automated and high-throughput processors to manage workloads with accuracy and speed.

Regulatory compliance, including CLIA (Clinical Laboratory Improvement Amendments) and CAP (College of American Pathologists) accreditation, further drives adoption of reliable, stand-alone systems. Strong healthcare spending, digital pathology integration, and emphasis on high-quality diagnostics sustain North America’s leading market share in tissue processing systems.

Europe Tissue Processing System Market Trends

Europe is a key region in the Tissue Processing System Market due to its high diagnostic demand, robust healthcare infrastructure, and widespread adoption of advanced laboratory technologies. European laboratories process over 310 million histology and cytology specimens annually, representing roughly 25–29% of global volumes, with around 58% of labs employing automated systems to improve efficiency and accuracy. National cancer screening programs in countries such as Germany, France, and the United Kingdom establish consistent specimen workflows, driving demand for reliable tissue processors.

Established healthcare systems, stringent regulatory standards, and tertiary hospitals offering advanced testing such as immunohistochemistry and molecular diagnostics further reinforce market importance. Public health initiatives and broad insurance coverage sustain high diagnostic volumes, making Europe a critical market for tissue processing systems.

Asia Pacific Tissue Processing System Market Trends

Asia Pacific is the fastest-growing region in the tissue processing system market due to rapidly expanding healthcare infrastructure, rising population, and increasing prevalence of chronic diseases and cancer. Countries like China and India have witnessed a significant growth in hospital and diagnostic laboratory capacities over the past decade, with thousands of new pathology and clinical labs established to meet rising diagnostic demand.

According to the World Health Organization, Asia accounts for nearly half of global cancer cases, driving the need for efficient biopsy and tissue analysis workflows. Investments in modern laboratory technologies, government initiatives to improve healthcare access, and a growing emphasis on early disease detection further accelerate the adoption of automated and high-throughput tissue processing systems across the region.

Market Competitive Landscape

Leading companies in the tissue processing system market focus on innovative, automated, and high-throughput solutions. They invest in compact designs, digital integration, and workflow automation, enhancing efficiency, reliability, and consistency. R&D emphasizes accuracy, ease of use, and scalability, while collaborations with hospitals and diagnostic labs drive the adoption of advanced tissue processors worldwide.

Key Industry Developments:

- In February 2025, Thermo Fisher Scientific introduced the Invitrogen™ EVOS™ S1000, a cutting-edge system designed for advanced spatial tissue imaging. The platform enabled researchers and clinical laboratories to capture high-resolution, multi-dimensional images of tissue samples with improved accuracy and workflow efficiency.

- In May 2024, Sakura Finetek Europe B.V. advanced its laboratory automation by introducing the Tissue-Tek xPrint® LP Laser Cassette Printer. The system enabled laboratories to automate tissue cassette labeling with high precision, improving workflow efficiency and reducing errors in histology and pathology processes.

Companies Covered in Tissue Processing System Market

- Leica Biosystems Nussloch GmbH

- Thermo Fisher Scientific Inc.

- Sakura Finetek Europe B.V.

- Slee medical GmbH

- Milestone Srl

- General Data Company Inc.

- Agar Scientific Ltd.

- MEDITE GmbH

- Bio-Optica Milano SpA

- Jokoh Co. Ltd.

- Others

Frequently Asked Questions

The global tissue processing system market is projected to be valued at US$ 477.5 Mn in 2026.

Rising biopsy volumes, increasing automation, expanding pathology labs, chronic disease prevalence, and demand for faster, accurate tissue diagnostics drive growth.

The global tissue processing system market is poised to witness a CAGR of 6.0% between 2026 and 2033.

Adoption of high-throughput, compact, and automated systems, integration with digital pathology, emerging market expansion, and personalized medicine drive opportunities.

Leica Biosystems Nussloch GmbH, Thermo Fisher Scientific Inc., Sakura Finetek Europe B.V., Slee medical GmbH, Milestone Srl, General Data Company Inc.