- Pharmaceuticals

- Therapeutic Albumin Market

Therapeutic Albumin Market Size, Share, and Growth Forecast 2026 - 2033

Therapeutic Albumin Market by Source (Human-derived, Recombinant), by Indication (Hypovolemia and Shock Management, Burn Treatment, Hypoalbuminemia, Acute Liver Failure, and Nephrotic Syndrome), by Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), by Regional Analysis, 2026 - 2033

Therapeutic Albumin Market Size and Trend Analysis

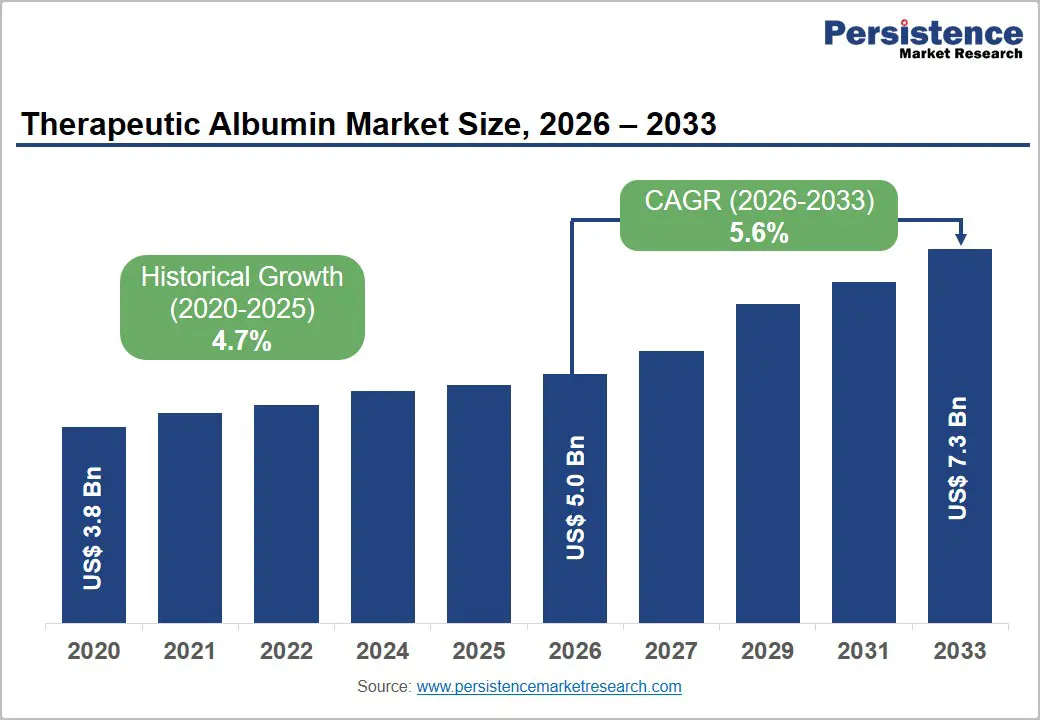

The global therapeutic albumin market size is expected to be valued at US$ 5.0 billion in 2026 and projected to reach US$ 7.3 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033. This sustained growth is driven by the irreplaceable clinical role of albumin infusion in critical care medicine, the expanding global burden of liver disease and critical illness requiring volume replacement, and the accelerating development of recombinant albumin technology that is diversifying the supply base beyond human plasma donation.

According to the World Health Organization (WHO), liver diseases affect over 1.5 billion people worldwide, with cirrhosis and acute liver failure representing the primary high-volume therapeutic albumin indications. Simultaneously, the International Society for Blood Transfusion (ISBT) highlights chronic global plasma supply constraints, accelerating investment in recombinant and plant-derived albumin production platforms as structurally important long-term supply chain diversification strategies.

Key Industry Highlights:

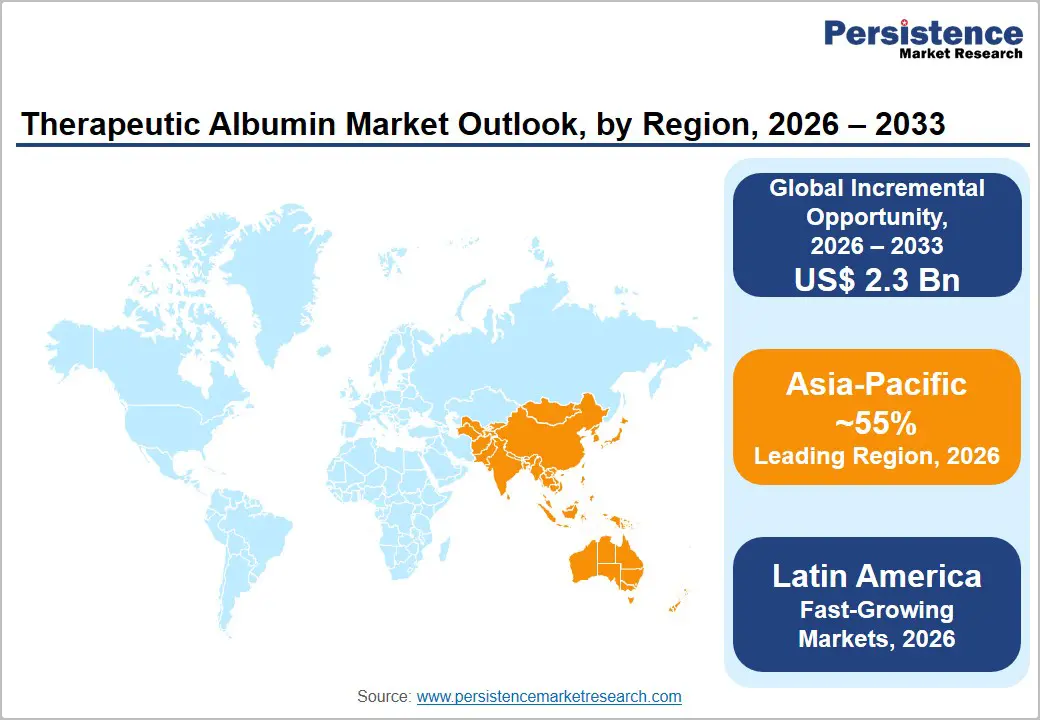

- Leading Region: Asia Pacific leads the global market with 55% share in 2026, anchored by China’s massive liver disease patient population, 30+ NMPA-licensed domestic fractionators, historically high albumin infusion rates, and Japan’s premium therapeutic albumin consumption in elderly hepatic disease management.

- Fastest Growing Region: Latin America is projected to register the highest CAGR during 2026 - 2033, driven by Brazil’s SUS reimbursement of albumin in ICU and liver disease protocols, Mexico’s and Colombia’s expanding hospital critical care capacity, and high viral hepatitis and alcohol-related liver disease burdens across the region.

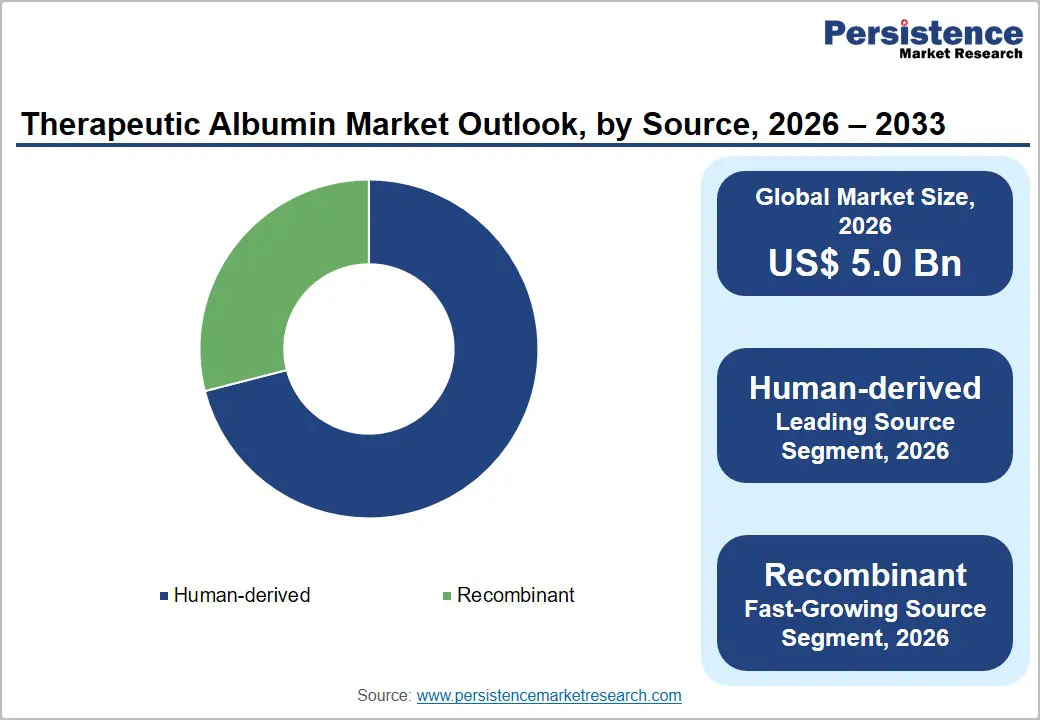

- Dominant Segment: Human-derived albumin commands approximately 71% share in 2026, underpinned by multi-decade clinical validation, established FDA/EMA/NMPA regulatory approvals, and the commercial dominance of Grifols, CSL Behring, Octapharma, and Baxter International through integrated plasma collection-to-fractionation supply chains.

- Fastest-Growing Segment: Recombinant albumin is the fastest-growing source segment over 2026- 2033, driven by Merck KGaA’s Recombumin® Elite expansion, EMA guideline maturation for recombinant plasma proteins, and the strategic imperative to reduce plasma donation dependency as liver disease patient populations grow.

- Key Market Opportunity: The development of therapeutic-grade recombinant human albumin platforms addressing plasma supply constraints documented by PPTA and eliminating pathogen transmission risks,s combined with Latin America’s critical care expansion, creates the highest incremental growth opportunity for innovator companies.

Market Dynamics

Drivers - Rise in Global Burden of Liver Disease and Critical Care Admissions

The escalating global prevalence of chronic liver disease, cirrhosis, and hepatic failure is the primary clinical driver sustaining therapeutic albumin demand across all major geographies. The WHO estimates that liver diseases cause approximately 2 million deaths annually worldwide, with cirrhosis complications including spontaneous bacterial peritonitis (SBP), hepatorenal syndrome (HRS), and hepatic encephalopathy requiring high-dose intravenous albumin as standard of care per European Association for the Study of the Liver (EASL) clinical guidelines.

The EASL recommends albumin infusion at 1.5 g/kg on day 1 and 1.0 g/kg on day 3 as the evidence-based gold standard for SBP management. Additionally, growing intensive care unit (ICU) admissions globally, with the Society of Critical Care Medicine (SCCM) documenting approximately 5.7 million ICU admissions annually in the U.S., generate consistent critical care volume replacement demand for albumin solutions.

Restraints - Chronic Global Plasma Supply Constraints and Donor Availability Limitations

Human-derived albumin production is fundamentally constrained by the availability of eligible plasma donations, which cannot be rapidly scaled to meet demand surges. The Plasma Protein Therapeutics Association (PPTA) has documented persistent global plasma supply imbalances, with demand for all plasma-derived therapies, including albumin, immunoglobulins, and clotting factors, growing faster than the expansion of collection infrastructure in many regions. EU and U.S. regulatory requirements for plasma donor qualification, viral inactivation validation, and lot release testing add a minimum 9-12 month production cycle time, limiting supply responsiveness to demand fluctuations and creating procurement vulnerability for hospital formularies dependent on albumin.

Market Opportunities

Recombinant Albumin Technology: Fastest Growing Segment Transforming Supply Landscape

Recombinant human albumin (rHA) is the fastest-growing source segment in the therapeutic albumin market, driven by its potential to eliminate dependence on plasma donation, eliminate the pathogen-transmission risk inherent in plasma-derived products, and enable scalable industrial production through yeast, rice, or tobacco plant expression systems. Merck KGaA and Thermo Fisher Scientific Inc. are among the global leaders commercializing recombinant albumin for biopharmaceutical manufacturing and research applications, with therapeutic-grade rHA development programs advancing at multiple organizations.

Albumedix’s Recombumin® platform represents the most clinically advanced rHA system, produced via fermentation in Pichia pastoris yeast. As regulatory frameworks for therapeutic rHA mature, the European Medicines Agency (EMA) has published guidelines. Companies investing in rHA production scale-up are positioned to capture above-average revenue growth through 2033 as the technology transitions from niche to mainstream clinical supply.

Category-wise Analysis

Source Insights

Human-derived albumin dominates the therapeutic albumin market by source, accounting for approximately 71% of market share in 2025. This substantial leadership reflects human-derived albumin’s multi-decade clinical validation record, established regulatory approval in all major markets, and the absence of commercial-scale therapeutic recombinant albumin alternatives for intravenous administration. Human serum albumin (HSA) produced via plasma fractionation by CSL Behring, Grifols, S.A., Octapharma AG, and Baxter International Inc. underpins the vast majority of global hospital formulary procurement.

The FDA and EMA have well-established regulatory pathways for plasma-derived albumin under their respective biologics licensing frameworks, providing procurement confidence for hospital pharmacy buyers. Human-derived albumin’s commercial dominance is expected to persist through the forecast period, though its market share will gradually erode as recombinant platforms achieve therapeutic-grade regulatory approvals.

Indication Insights

Hypoalbuminemia is the leading indication segment in the therapeutic albumin market in 2025, reflecting the broad clinical applicability of albumin infusion to correct serum albumin deficits across multiple underlying disease conditions. Hypoalbuminemia, defined as serum albumin below 3.5 g/dL, is a marker of nutritional depletion, hepatic dysfunction, sepsis, and critical illness that is highly prevalent across hospitalized patients globally.

According to studies published in Critical Care Medicine, approximately 40-50% of hospitalized patients in intensive care settings present with serum albumin levels below the normal range, creating a large patient population across which albumin infusion is clinically considered. EASL and AASLD (American Association for the Study of Liver Diseases) guidelines specifically mandate albumin for large-volume paracentesis, SBP prophylaxis, and HRS prevention in cirrhotic patients, the highest-volume hypoalbuminemia patient group sustaining the indication’s leading revenue position.

Regional Insights

Asia-Pacific Therapeutic Albumin Market Trends and Insights

Asia Pacific dominates the Therapeutic Albumin Market due to its large patient population, rising burden of liver diseases, increasing ICU admissions, and expanding plasma collection infrastructure. The region records a high prevalence of hepatitis-related liver disorders and chronic kidney diseases, which significantly increases albumin usage in hospitals. According to the World Health Organization, China and India together account for a major share of global hepatitis cases, while Japan has one of the world’s oldest populations requiring critical care therapies.

Governments across the region are expanding biologics manufacturing and hospital infrastructure, increasing accessibility to plasma-derived therapies. Rapid healthcare modernization and rising surgical procedures are further strengthening albumin demand across the Asia Pacific, making it the largest regional market globally.

China Therapeutic Albumin Market Trends and Insights

China is the leading country in the Asia Pacific Therapeutic Albumin Market and is expected to reach nearly US$ 1.9 Bn by 2026, driven by strong demand from hospitals and advanced plasma fractionation capabilities. According to the Chinese Center for Disease Control and Prevention, China reports millions of chronic hepatitis B cases annually, increasing the need for albumin therapy in liver disease treatment. The country has also significantly expanded its intensive care infrastructure after the pandemic.

China’s National Health Commission has supported domestic biologics and plasma-product manufacturing under healthcare modernization initiatives. Rising numbers of surgical procedures, trauma cases, and critical care admissions are further driving albumin utilization, while local manufacturers continue to expand plasma collection and recombinant protein production capacity.

India Therapeutic Albumin Market Trends and Insights

India is the fastest-growing market for the therapeutic albumin market and is expected to reach nearly 8% CAGR during the forecast period. According to the National Health Mission and Indian Council of Medical Research, India is witnessing an increasing prevalence of chronic kidney disease, liver cirrhosis, and malnutrition-related hypoalbuminemia. The country collects over 12 million blood units annually, improving plasma availability for therapeutic applications.

Government programs such as Ayushman Bharat are expanding access to tertiary healthcare and ICU capacity across urban and semi-urban regions. India is also strengthening domestic biologics manufacturing under the “Make in India” initiative, thereby supporting greater adoption of plasma-derived and recombinant albumin products in hospitals and in pharmaceutical manufacturing.

Europe Therapeutic Albumin Market Trends and Insights

Europe constitutes as a significant region for its advanced healthcare systems, high plasma donation standards, and strong adoption of albumin therapies in critical care and surgery. The region has well-established plasma collection networks regulated by the European Medicines Agency and national health authorities.

The increasing prevalence of chronic liver disease and aging populations is supporting albumin demand in hospitals and specialty clinics. Europe also maintains strong biotechnology and pharmaceutical manufacturing capabilities, which are driving recombinant albumin development. Countries across the region continue investing in emergency medicine, transplantation procedures, and biologics production. In addition, supportive reimbursement systems and strong clinical guidelines for plasma therapies help maintain stable therapeutic albumin consumption across Europe.

Germany Therapeutic Albumin Market Trends and Insights

Germany is the leading country in the European Therapeutic Albumin Market and is expected to reach approximately US$ 40 Mn in 2026. According to the German Federal Statistical Office, the country performs millions of inpatient surgical procedures annually, creating significant demand for plasma-derived therapies and volume expanders such as albumin. Germany also has one of Europe’s strongest plasma collection and biopharmaceutical manufacturing infrastructures.

Rising elderly population levels are increasing chronic disease burden and ICU admissions, supporting albumin utilization in critical care settings. In addition, Germany invests heavily in biologics and recombinant protein technologies, helping expand the country’s therapeutic protein production capabilities and strengthening its leadership position within the European albumin market.

France Therapeutic Albumin Market Trends and Insights

France is among the fastest-growing countries in Europe and is expected to achieve a CAGR of around 5.5% during the forecast period. According to Santé Publique France, chronic liver disease and hospital admissions related to severe infections and surgical interventions continue to rise, increasing albumin demand in critical care. France has strengthened investments in biologics manufacturing and plasma-derived medicinal products through national healthcare modernization programs.

The country also supports extensive healthcare reimbursement for advanced therapies, improving patient access to albumin treatment. An aging population and growing demand for transplantation and intensive care procedures are further contributing to the expansion of therapeutic albumin use across France.

Latin America Therapeutic Albumin Market Trends and Insights

Latin America is emerging as a fast-growing market owing to the expanding healthcare infrastructure, rising ICU capacity, and increasing adoption of plasma-derived therapies. According to the Pan American Health Organization, countries across the region are investing in strengthening blood systems and improving access to biologic medicines. The increasing incidence of trauma injuries, liver disorders, and chronic diseases is supporting higher demand for albumin treatment in hospitals.

Governments are also expanding public healthcare coverage and upgrading emergency care facilities. Improvements in biologics distribution networks and rising healthcare expenditure are further contributing to market expansion, while rising awareness of plasma therapies continues to drive therapeutic albumin adoption across Latin America.

Brazil Therapeutic Albumin Market Trends and Insights

Brazil is the leading country in the Latin American Therapeutic Albumin Market and is expected to reach nearly US$ 0.18 Bn by 2026. According to Brazil’s Ministry of Health, the country has expanded investments in intensive care units, trauma care, and public healthcare infrastructure in recent years. Brazil also reports high hospitalization rates associated with liver disease and chronic illnesses, increasing the need for albumin-based therapies. The country’s healthcare system supports broad adoption of plasma-derived products in tertiary hospitals.

In addition, Brazil continues to strengthen domestic biologics and blood-product manufacturing capabilities to reduce import dependence, while rising surgical volumes and emergency care procedures are further driving nationwide demand for therapeutic albumin.

Mexico Therapeutic Albumin Market Trends and Insights

Mexico is likely to witness fast growth in the Latin American therapeutic albumin market and is expected to capture 6.5% CAGR during the forecast period. According to the Mexican Ministry of Health, healthcare investments in critical care and emergency medicine have increased significantly over the past few years. The growing prevalence of liver disease, trauma-related hospitalization, and chronic kidney disorders is increasing demand for plasma-derived therapies, including albumin.

Mexico is also expanding healthcare access through public insurance and hospital modernization programs. Increasing partnerships with biologics manufacturers and growth in plasma product imports are supporting broader albumin availability. These factors, combined with improvements in hospital infrastructure, are accelerating growth in the therapeutic albumin market across the country.

Competitive Landscape

The global therapeutic albumin market is moderately consolidated, with a small number of integrated plasma fractionation companies commanding the majority of production capacity and revenue. Grifols, S.A., CSL Behring, Octapharma AG, Baxter International Inc., and Takeda Pharmaceutical collectively control a dominant share of global human albumin supply through ownership of extensive plasma collection networks, fractionation facilities, and regulatory approvals in over 100 countries.

Chinese domestic manufacturers including Hualan Biological Engineering, Shanghai RAAS, and China Biologic Products Holdings dominate the Asia Pacific volume tier. Key competitive differentiators include plasma supply chain security, manufacturing capacity scale, and recombinant albumin R&D investment.

Key Developments:

- August 2025: The Plasma Protein Therapeutics Association (PPTA) responded to China’s recent approval of recombinant albumin and stated that the development represented a significant advancement in albumin innovation and supply diversification. The approval followed the authorization of a rice-derived recombinant human albumin injection by China’s National Medical Products Administration (NMPA), aimed at treating hypoalbuminemia associated with liver disease.

- May 2025: Orion Corporation announced that it had agreed with Shilpa Medicare Limited for the development and commercialization of Recombinant Human Albumin in the European market. Under the agreement, Shilpa Medicare supplied and developed the recombinant albumin product, while Orion received commercialization rights across Europe.

Companies Covered in Therapeutic Albumin Market

- Grifols, S.A.

- Kedrion S.p.A.

- Octapharma AG

- CSL Behring

- Baxter International Inc.

- Takeda Pharmaceutical Company Limited

- Biotest AG

- China Biologic Products Holdings, Inc.

- Shire (now part of Takeda)

- Hualan Biological Engineering Inc.

- Shanghai RAAS Blood Products Co., Ltd.

- Green Cross Corporation

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Others

Frequently Asked Questions

The global therapeutic albumin market is projected to be valued at US$ 5.0 billion in 2026.

Rising liver diseases, ICU admissions, surgeries, trauma cases, plasma therapies, and expanding biologics manufacturing demand globally.

Asia Pacific leads with approximately 55% market share in 2025.

Growing recombinant albumin adoption in biologics, cell therapies, drug formulation, and emerging healthcare infrastructure expansion.

Grifols S.A., CSL Behring, Octapharma AG, Baxter International Inc., Takeda Pharmaceutical.