- Food Packaging

- Tea Packaging Machine Market

Tea Packaging Machine Market Size, Share, and Growth Forecast, 2026 - 2033

Tea Packaging Machine Market by Machine Type (Tea Bag Packaging Machines, Pyramid Tea Bag Machines, Others), Packaging Format (Pouches & Sachets, Pyramid Bags, Others), Tea Type, Automation Level, and Regional Analysis for 2026 - 2033

Tea Packaging Machine Market Size and Trends Analysis

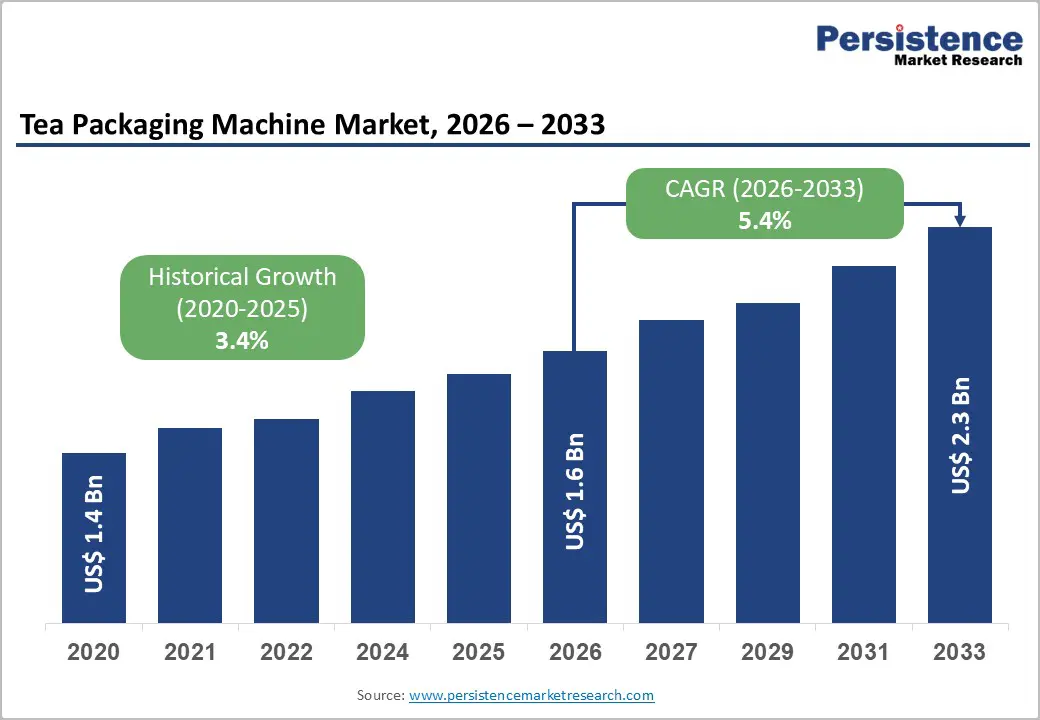

The global tea packaging machine market size is likely to be valued at US$1.6 billion in 2026 and is expected to reach US$2.3 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033, driven by structurally rising tea consumption in Asia Pacific, accelerated adoption of automated packaging lines, and growing demand for convenience-oriented formats such as pouches, pyramid bags, and single-serve packs.

Sustainability mandates and material innovation are reshaping machine specifications toward recyclable-material compatibility and reduced film usage. The premiumization of tea, particularly specialty and herbal blends, is increasing demand for flexible, small-batch, and high-precision packaging solutions across developed and emerging markets.

Key Industry Highlights

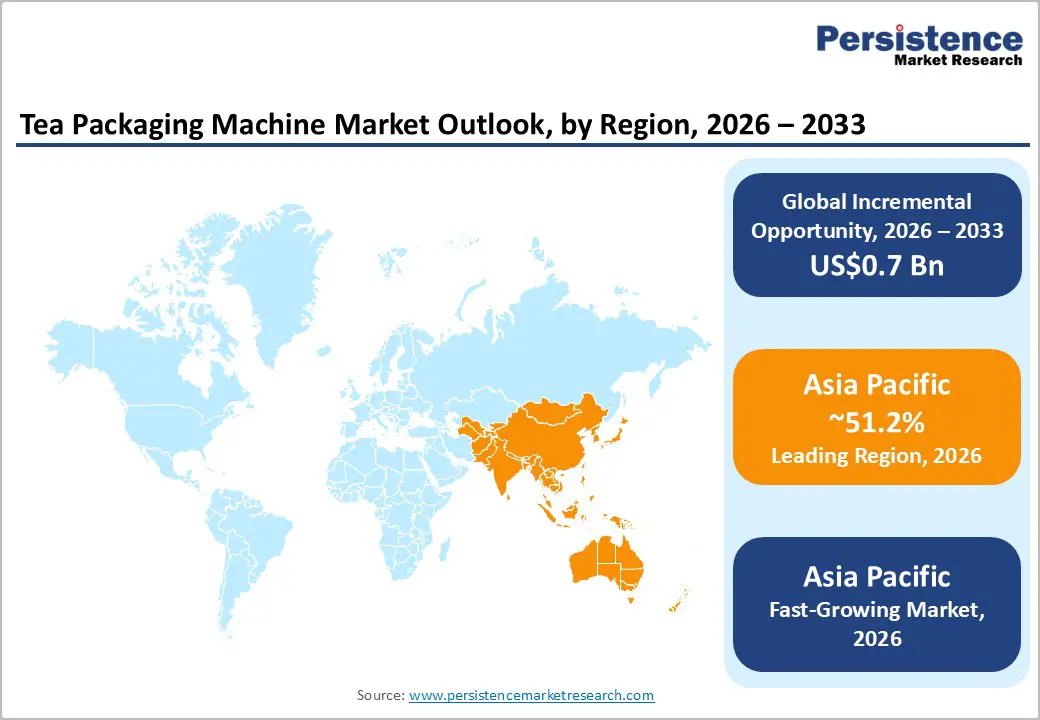

- Leading Region: Asia Pacific is projected to account for 51.2% of the market, driven by large-scale tea production, rising domestic consumption, and export-oriented packaging demand.

- Fastest-growing Region: Asia Pacific, led by China, India, and ASEAN markets, benefiting from automation adoption, premiumization, and government modernization initiatives.

- Investment Plans: Significant investments in automation, pilot testing, and sustainable-material validation; companies such as Tata Tea (India), Syntegon, and Tetra Pak are expanding production and service facilities in APAC to support new lines and retrofits.

- Dominant Machine Type: Tea bag packaging machines are expected to account for a 37.8% share, favored for mass-retail penetration, standardized operations, and integration with cartoning lines.

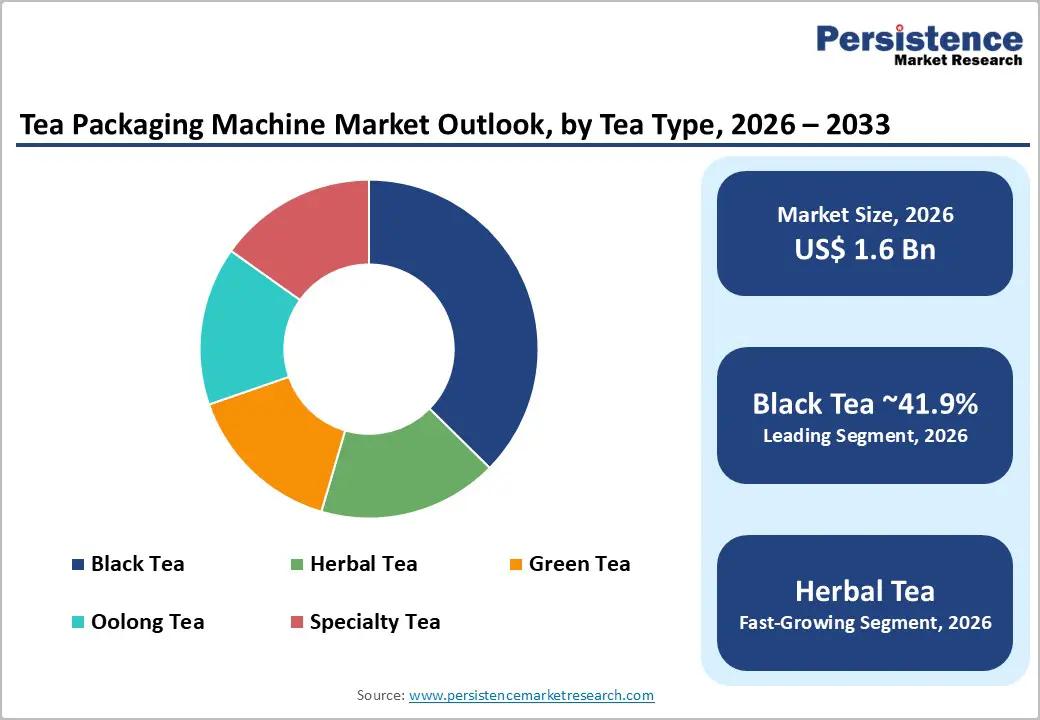

- Leading Tea Type: Black tea is estimated to account for 41.9% of the market, reflecting high production volumes and entrenched consumption.

| Key Insights | Details |

|---|---|

| Tea Packaging Machine Market Size (2026E) | US$1.6 Bn |

| Market Value Forecast (2033F) | US$2.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis -Rising Tea Production and Consumption Concentrated In Asia Pacific

Global tea production and consumption remain heavily concentrated in Asia Pacific, with China and India accounting for the majority of output and domestic demand. Large-scale production volumes, combined with the expansion of packaged tea penetration, directly support sustained demand for tea packaging machines in the region. High domestic consumption reduces reliance on bulk exports and increases localized packaging activity, especially for tea bags and pouches. As a result, Asia Pacific accounts for a disproportionate share of new machine installations and aftermarket service demand. This structural concentration strengthens long-term volume visibility for equipment suppliers and underpins stable multi-year order pipelines for mid- and high-speed tea packaging lines.

Automation and Productivity Upgrades across Tea Processing Lines

Tea processors are increasingly investing in automation to reduce labor dependency, improve throughput consistency, and enhance yield control. Fully automatic tea baggers, integrated weighing systems, and end-of-line cartoning solutions allow manufacturers to improve uptime while lowering per-unit operating costs. Automation adoption is particularly strong among branded tea producers expanding premium and specialty portfolios, where precision dosing and packaging consistency are critical. Integrated solutions that combine weighing, filling, sealing, and cartoning raise average selling prices per line and increase demand for service contracts, software upgrades, and retrofits. This shift toward automation acts as a structural multiplier for market value growth.

Barrier Analysis - Capital Intensity and Long Equipment Replacement Cycles

Tea packaging machines, particularly fully automatic systems, require substantial upfront capital investment and typically operate for long lifecycles of 7-12 years. This limits replacement frequency and encourages operators to prioritize retrofits over full equipment replacement. Small and mid-sized packers face financing constraints and extended payback periods, which can delay purchasing decisions. Even a one- to two-year deferral in replacement cycles can materially slow short-term market growth, making demand more sensitive to macroeconomic conditions and capital availability.

Material and Supply-Chain Volatility

Price volatility in packaging films, specialty papers, and metals, combined with intermittent shortages of electronic components, creates margin pressure for equipment manufacturers and delays project execution. Regulatory restrictions on certain plastic films necessitate redesigns of machines to accommodate alternative substrates, thereby increasing engineering complexity and development costs. Extended procurement lead times for key components disrupt delivery schedules and can delay the commissioning of new lines, introducing execution risk for both OEMs and end users.

Opportunity Analysis - Retrofit and Service-Led Growth Model

The growing installed base of tea packaging equipment presents a sizable opportunity for retrofits, upgrades, and aftermarket services. Operators increasingly favor material-change kits, automation enhancements, and digital monitoring modules over full machine replacement. Retrofit and service activities could account for a meaningful share of incremental industry revenues through 2030, supported by higher margins and recurring revenue streams. For OEMs, expanding service offerings increases customer lifetime value while reducing revenue cyclicality associated with capital expenditure cycles.

Sustainable Packaging Conversions and New Materials

Brand owners are accelerating transitions toward recyclable and material-efficient packaging, driving demand for machines compatible with paper-based barriers and mono-material films. These substrates often require modified sealing temperatures, pressure profiles, and handling systems. Equipment suppliers that certify compatibility with next-generation sustainable materials gain access to premium procurement budgets and early-mover advantages. Even partial conversion of new production lines to sustainability-ready configurations increases machine complexity, raises average selling prices, and expands aftermarket service demand.

Category-wise Analysis

Machine Type Insights

Tea bag packaging machines are expected to account for 37.8% of the market, driven by broad consumer acceptance of bagged tea and deep penetration across both retail and institutional channels. High-speed rotary tea baggers, envelope sealing systems, and automated counting units are standard in large-scale facilities, supporting high-throughput operations and consistent quality control. Multi-pack retail formats (20-50 bag cartons for black tea or herbal blends) drive strong demand for combined bagging and cartoning solutions, particularly in regions such as India, China, and Europe. Well-known brands such as Twinings, Lipton, and Bigelow rely heavily on these machines for standard bagged tea SKUs, further cementing their leadership. Standardizing processes simplifies regulatory compliance (FDA, EU food contact standards), reduces training complexity, and enables equipment vendors to offer scalable service contracts and spare parts revenue, reinforcing the segment’s dominance.

Pyramid tea bag machines are expected to grow at the fastest rate, reflecting the premiumization trend in specialty and single-origin teas. Pyramid or mesh sachets allow whole-leaf tea to expand fully during infusion, enhancing flavor and perceived quality. These machines employ more sophisticated forming, sealing, and gentle leaf-handling mechanisms, which increase equipment value and justify higher investment. Growth is driven by premium brand launches, gifting applications, and direct-to-consumer (DTC) subscription services. For instance, brands such as Teapigs and DAVIDsTEA utilize pyramid sachets to differentiate in e-commerce channels. OEMs providing flexible machines that switch between flat bags, pyramid bags, and enclosed envelopes are capturing outsized growth among both established and emerging specialty producers, particularly in North America and Europe.

Tea Type Insights

Black tea is estimated to dominate the market with a 41.9% share in 2026, due to high global production volumes and entrenched consumption patterns in key markets such as China, India, and the U.K. Packaging lines for black tea are typically configured for high-speed processing, including automated tea bagging, volumetric pouch filling, and end-of-line cartoning. Large-scale operations, especially for export-oriented blends and private-label retail products, rely on standardized equipment for consistent quality and operational efficiency. Prominent brands, including Lipton, Tetley, and Brooke Bond, reinforce demand for high-speed tea bag and pouch machines. The dominance of black tea also drives regular aftermarket demand for retrofits, spare parts, and preventive maintenance, ensuring a stable equipment ecosystem.

Herbal tea is likely to be the fastest-growing segment of the tea category, reflecting rising health, wellness, and functional beverage trends. Products such as chamomile, rooibos, and adaptogenic blends require delicate handling due to fragile ingredients, aroma sensitivity, and variable leaf sizes, necessitating specialized dosing, gentle filling, and precise pouching mechanisms. Higher retail prices for functional and organic herbal teas justify investment in automated, flexible packaging systems capable of maintaining quality while handling small batch production. Brands such as Yogi Tea, Pukka, and traditional Ayurvedic herbal blends increasingly adopt pyramid and sachet formats, accelerating equipment demand relative to bulk black tea packaging. This segment also benefits from growth in e-commerce and gift packaging, where premium presentation drives upgrades to machines.

Regional Insights

North America Tea Packaging Machine Market Trends - Automation-Intensive Machines for Premium and Smart Tea Packaging

North America represents a significant value-driven market in the global tea packaging machine landscape, anchored by high automation levels and strong demand for premium and specialty tea products. The U.S. is the largest contributor within the region, with a rapidly expanding consumer base for herbal, functional, and ready-to-drink tea formats that increasingly require sophisticated packaging solutions. Consumer preferences for convenience, sustainability, and visually appealing packaging, from digitally printed sachets to recyclable pouches, are driving investments in flexible, modular systems that support multiple formats and frequent changeovers.

Industry adoption of high-speed, fully automated tea packaging lines with integrated inspection, traceability, and hygiene features is common among established processors and contract packers aiming to meet stringent regulatory and quality assurance standards. The rise of premium U.S. tea brands and direct-to-consumer channels has prompted manufacturers to adopt smart packaging technologies to enhance product differentiation and brand positioning. North American operators are increasingly incorporating predictive maintenance, OEE dashboards, and digital integration tools to improve uptime and operational visibility.

To manage the high upfront cost of state-of-the-art equipment, many mid-sized packers leverage leasing options or vendor financing programs, allowing them to adopt automation without prohibitive capital burdens. This combination of premium product demand, regulatory compliance, and technology adoption helps sustain North America’s robust growth in advanced tea packaging machinery.

Europe Tea Packaging Machine Market Trends - Sustainability-Compliant, Energy-Efficient Tea Packaging Machinery

Europe is a major market for high-end tea packaging machines, driven by a potent mix of sustainability mandates, a premium tea consumption culture, and engineering leadership. Germany, the U.K., France, and Spain play central roles in shaping regional demand, each contributing unique market dynamics. European customers prioritize energy-efficient machines capable of handling recyclable and compostable materials, given stringent packaging directives aimed at reducing plastic waste. This has led to high demand for packaging lines that support mono-material barrier films, paper-based laminates, and low-temperature heat seals, enabling brands to meet both regulatory requirements and eco-conscious consumer preferences. German and Italian engineering firms are often at the forefront of this transformation, offering machines with advanced control systems and energy optimization features. The U.K.’s deep tea-drinking tradition and high consumption of specialty blends further stimulate demand for versatile machinery capable of producing premium sachets and pyramid bags with intricate graphics and enhanced barrier properties.

France’s sophisticated consumer base drives demand for artisanal and luxury tea packaging formats, prompting buyers to seek flexible, multi-format machines that deliver both performance and aesthetic quality. European producers are also investing in pilot testing and material validation to streamline transitions to recyclable materials and to reduce defect rates through advanced heat-seal and anti-static technologies. In response to regulatory harmonization across the EU, buyers increasingly expect full documentation and validation support from equipment suppliers to ensure compliance with food-contact and energy-efficiency standards. These trends underscore Europe’s strategic emphasis on sustainability, technical excellence, and premium packaging innovation within the tea packaging machine market.

Asia Pacific Tea Packaging Machine Market Trends - High-Volume Automation Driven by Tea Production and Export Growth

Asia-Pacific is expected to be the leading and fastest-growing region in the market, accounting for approximately 51.2% of the market. The dominance stems from the region’s large base of tea production, extensive domestic consumption, and expanding export markets. China and India are the most influential markets. China’s vast tea processing infrastructure has driven high adoption of automated pouch, sachet, and tea bag lines, particularly for products destined for both domestic retail and export. India’s tea industry, supported by the Tea Board of India and government initiatives to modernize processing and packaging facilities, has seen substantial investments in automation to improve throughput and meet rising quality standards.

Large producers such as Tata Tea have announced new facilities with state-of-the-art packaging capabilities, exemplifying how automation upgrades are reshaping capacity in Assam and other tea regions. In ASEAN countries such as Vietnam, Indonesia, and Thailand, export-oriented tea packers are increasingly adopting medium- to high-speed automated systems to serve global requirements for consistent quality and traceability. Across the region, small and mid-sized producers are retrofitting existing lines with digital monitoring tools and flexible feeder systems to handle a growing SKU mix that includes premium and flavored teas.

Government policies that support value addition and technical assistance for food and beverage manufacturing have accelerated the transition from manual or hybrid machines to fully automated, smart packaging systems. This structural modernization, combined with rising disposable incomes and expanding middle-class consumption patterns, ensures robust long-term demand for new installations and aftermarket services throughout the Asia Pacific.

Competitive Landscape

The global tea packaging machine market shows moderate concentration at the top, with global OEMs supplying high-end automated systems and numerous regional players serving cost-sensitive segments. Large players dominate value share through integrated solutions and service capabilities, while smaller manufacturers compete on price and localization.

Leading strategies include modular machine design, sustainability readiness, and expansion of service and retrofit offerings, and regional localization of manufacturing and support.

Key Industry Developments

- In May 2025, Tecno Pack showcased its FP 100 Flow Wrapper with ultrasonic sealing and paper-based capabilities at a major packaging exhibition, highlighting advances in high-speed, sustainable tea packaging solutions that enhance seal integrity and material efficiency.

Companies Covered in Tea Packaging Machine Market

- Syntegon Technology

- Tetra Pak

- IMA Group

- Ishida

- Rovema

- ULMA Packaging

- Mespack

- Coesia Group

- GEA Group

- Krones

- KHS Group

- Heat and Control

- ProMach

- Barry-Wehmiller

- Nichrome Packaging Solutions

- Bossar Packaging

- MULTIVAC

- Omori Machinery

Frequently Asked Questions

The global tea packaging machine market size is likely to be valued at US$1.6 billion in 2026.

By 2033, the tea packaging machine market is expected to reach US$2.3 billion.

Key trends shaping the market include rapid adoption of fully automatic packaging systems to improve throughput and reduce labor dependency, and rising demand for pyramid tea bags and flexible pouch formats linked to premium and specialty teas.

The tea bag packaging machine segment is the leading category, accounting for approximately 37.8% market share, supported by standardized mass-market packaging, strong retail penetration, and high-speed automated line installations.

The tea packaging machine market is projected to grow at a CAGR of 5.4% between 2026 and 2033.

Major players include Syntegon Technology, Tetra Pak, IMA Group, Ishida, and ULMA Packaging.