- Plastics, Polymers & Resins

- Packaging Films Market

Packaging Films Market: Size, Share, Trends, Growth, and Forecast (2025 - 2032)

Packaging Films Market by Material Type (Polyethylene, Polypropylene, Polyester, PVC), Application (Food & Beverages Packaging, Medical & Pharmaceutical Packaging, Consumer Products Packaging, Industrial Packaging), and Regional Analysis for 2025 - 2032

Packaging Films Market Size and Trends Analysis

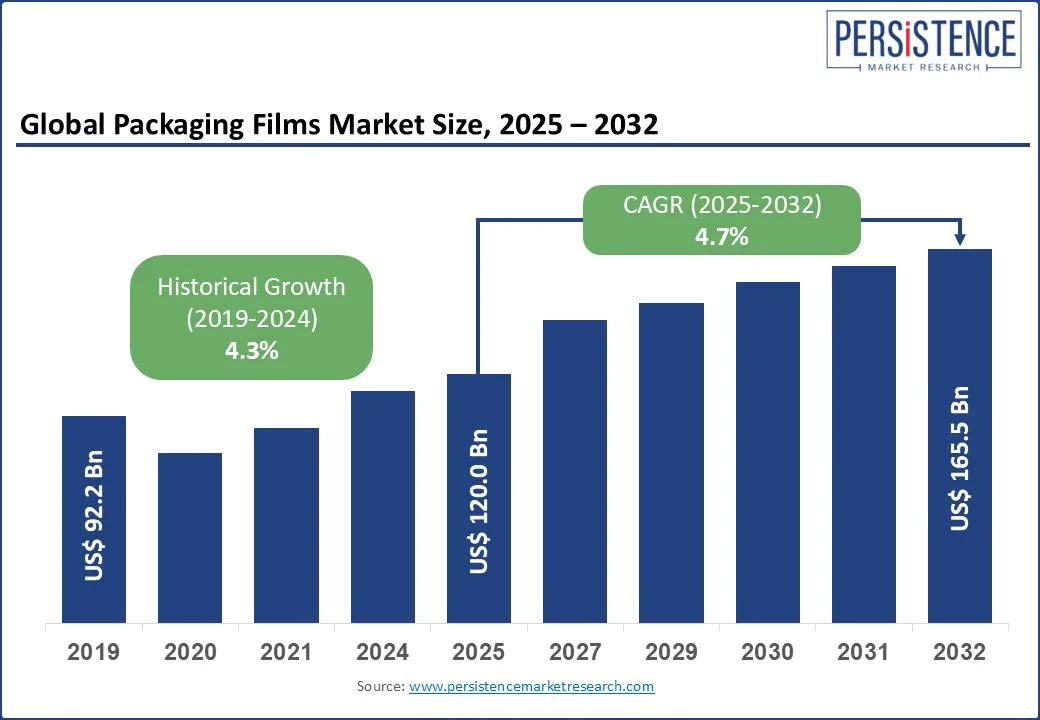

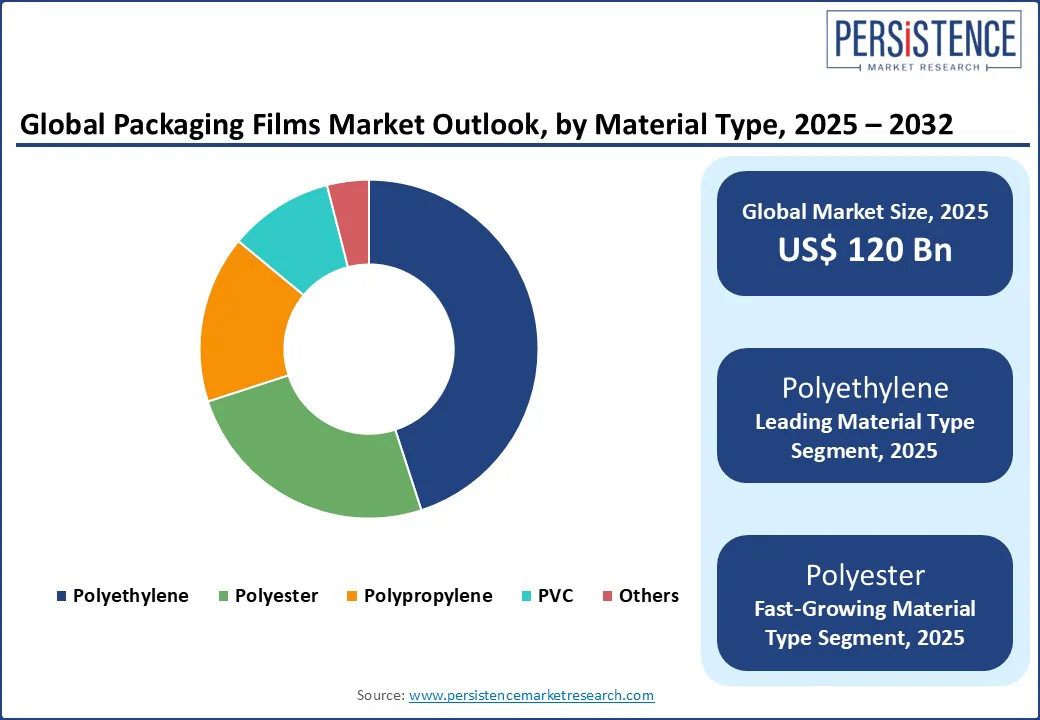

The global packaging films market size is likely to be valued at US$ 120.0 Bn in 2025, and is expected to reach US$ 165.5 Bn by 2032, growing at a CAGR of 4.7% during the forecast period from 2025 to 2032.

Primarily, the growth is driven by the rising demand for flexible, lightweight, and durable packaging solutions across the food, pharmaceutical, and consumer goods industries. Growing consumer preference for convenient and sustainable packaging, coupled with advancements in film materials and manufacturing technologies, is propelling market growth. Additionally, e-commerce expansion and increasing focus on extended shelf life further boost the demand for packaging films globally.

Key Industry Highlights:

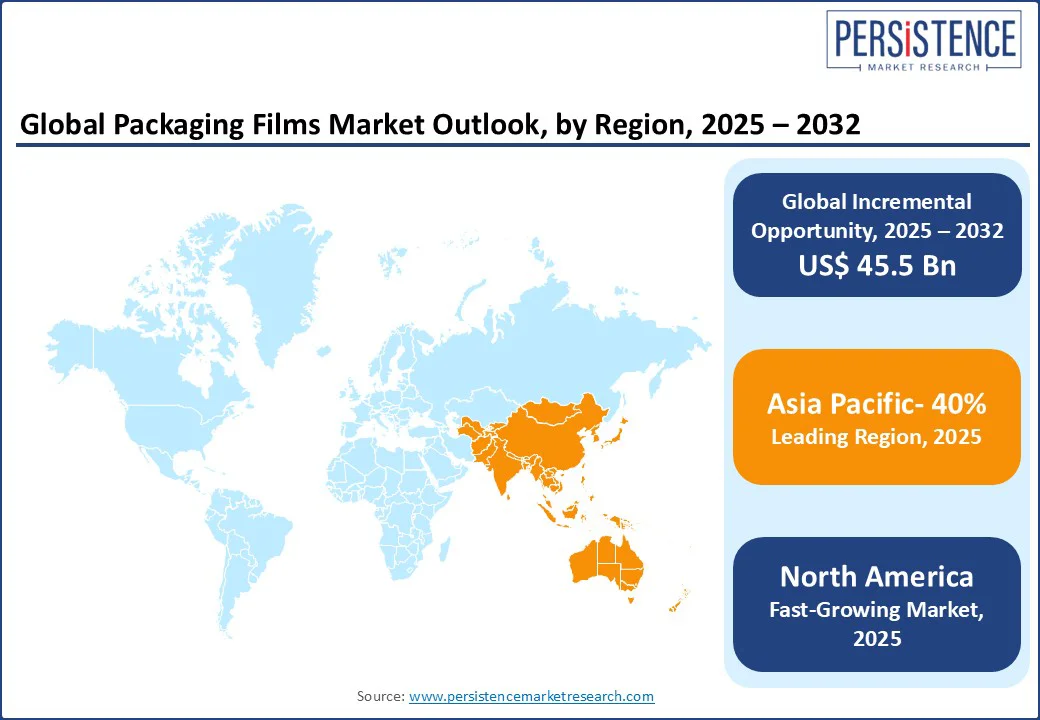

- Leading Region: Asia Pacific holds a 40% market share of the global packaging films market, driven by strong growth in the food industries of China and India, fueled by urbanization and rising incomes.

- Fastest-Growing Region: North America grows at 5.2%, led by U.S. demand for sustainable packaging materials, stricter environmental regulations, and innovations in eco-friendly film technologies.

- Leading Material Type: Polyethylene commands 45% market share in 2025, favored for its affordability, flexibility, moisture barrier properties, and extensive use in food and consumer packaging.

- Leading Application: Food & Beverages Packaging captures 40% market share, supported by rising convenience food consumption, extended shelf life needs, and growing urban lifestyles globally.

- Innovation Trends: Biodegradable and recyclable films increase by 25% in 2025, reflecting global sustainability efforts, consumer awareness, and regulatory mandates encouraging eco-friendly packaging solutions.

|

Global Market Attribute |

Key Insights |

|

Packaging Films Market Size (2019) |

US$ 92.2 Bn |

|

Packaging Films Market Size (2025E) |

US$ 120.0 Bn |

|

Market Value Forecast (2032F) |

US$ 165.5 Bn |

|

Projected Growth (CAGR 2025-2032) |

4.7% |

|

Historical Market Growth (CAGR 2019-2024) |

4.3% |

Market Dynamics

Driver - Surging Demand Across Major End-use Industries

Surging demand across major end-use industries is a key driver. Industries such as food and beverages, pharmaceuticals, FMCG, and electronics are increasingly adopting flexible packaging films due to their durability, cost-efficiency, and ability to extend shelf life.

For instance, in India, packaging consumption per capita nearly doubled in recent years as urbanization, rising disposable incomes, and lifestyle changes increased demand for processed and packaged products. Government initiatives supporting food safety, reducing wastage, and offering investment incentives in the packaging sector are also fueling market growth.

In addition, growing environmental concerns are encouraging the development and adoption of sustainable packaging films. Government research institutions have introduced biodegradable film technologies that match the performance of traditional plastic films, particularly for food and medical applications. This shift towards eco-friendly and high-performance materials supports the evolving needs of key end-use industries, further strengthening the outlook.

Restraint - Raw Material Price Volatility and Environmental Concerns

This industry faces challenges from raw material price volatility and environmental concerns. In 2025, polymer prices, such as polyethylene and polypropylene, fluctuated by 15% due to supply chain disruptions, increasing production costs, and impacting profitability, particularly in price-sensitive regions. Compliance with stringent plastic waste regulations, such as those in the EU and U.S., has raised production costs by 12%, limiting adoption for small-scale manufacturers.

Competition from alternative packaging materials, such as paper and glass, used in 30% of food packaging applications, restricts market penetration in eco-conscious markets. High energy costs in film production, up by 10% due to volatile energy markets, pose operational challenges. Supply chain constraints, including a 12% shortage in raw materials such as ethylene, further hinder production capacity, particularly for polyester and PVC films, limiting growth in developing regions.

Opportunity - Sustainable and Biodegradable Packaging

The shift toward sustainable and biodegradable packaging presents significant opportunities. Drives demand for eco-friendly films, with biodegradable options gaining 25% market share. Innovations in bio-based films, supported by US$ 8 Bn in R&D investments, target food and pharmaceutical applications, growing by 20% in 2025.

The rise of e-commerce, with global sales growing at 15%, increases demand for lightweight films in consumer product packaging by 18%. Emerging markets, with 2.5 billion urban consumers by 2030, offer untapped potential, particularly for polyester films in medical packaging. Smart packaging technologies, incorporating antimicrobial films, enhance food safety, positioning packaging films as critical components in sustainable and innovative solutions.

Segmental Insights

Material Type Insights

In 2025, polyethylene dominates, holding approximately 45% market share. Known for its cost-effectiveness, flexibility, and excellent barrier properties, polyethylene is the material of choice for a wide range of flexible packaging applications. It is especially favored in the food and beverage packaging sector, where it represents 65% of material usage due to its ability to protect product freshness and reduce packaging costs.

Polyester films are experiencing the fastest growth, driven by rising demand in pharmaceutical packaging. Their high clarity, strength, and chemical resistance have led to an 18% increase in adoption in 2025, particularly for packaging that requires visibility and hygiene.

Polypropylene holds a 30% share, valued for its heat resistance and durability across various consumer and industrial uses. PVC films continue expanding in industrial applications, while the remaining 10% consists of specialty materials designed for unique or high-performance packaging needs.

Application Type Insights

In 2025, food and beverage packaging leads the segment, accounting for approximately 50% of the total market share. This dominance is driven by the rising demand for convenience and ready-to-eat foods, along with a 70% adoption rate of flexible packaging materials. Increasing focus on food safety and extended shelf life further supports its growth, with steady expansion across both developed and emerging markets.

Medical and pharmaceutical packaging is the fastest-growing application, driven by the global rise in healthcare demand and stringent regulatory standards. In 2025, the sector has seen a 20% increase in packaging film adoption, particularly for high-barrier and sterile packaging formats.

Meanwhile, consumer products packaging holds a 25% share, benefiting from lightweight and customizable film solutions ideal for personal care and household goods. Industrial packaging accounts for 15%, where durable, puncture-resistant films are essential for protecting machinery, components, and bulk products during transit.

Regional Insights

North America Packaging Films Market Trends

North America is the fastest-growing region in the packaging films market, driven by strong demand from the food and beverage, pharmaceutical, and consumer goods industries. The region benefits from rising consumer preference for convenient, sustainable packaging solutions and stringent regulatory requirements for food safety and medical packaging.

Innovations in biodegradable and recyclable packaging films are accelerating growth, supported by government initiatives promoting environmental sustainability. The rapid expansion of e-commerce further boosts demand for lightweight and protective packaging materials.

Additionally, increasing awareness about plastic waste reduction encourages manufacturers to adopt eco-friendly packaging films. These factors collectively fuel robust growth in the North America packaging films market, positioning it as a key driver in the global industry with strong prospects for continued expansion.

Europe Packaging Films Market Trends

Europe holds a significant share of the packaging films market, driven by well-established food, pharmaceutical, and consumer goods industries. The region’s strict regulations on food safety and environmental standards boost demand for high-quality, sustainable packaging films.

Europe is a leader in adopting biodegradable and recyclable packaging materials, supported by government policies aimed at reducing plastic waste and promoting a circular economy. Additionally, the rise of convenience foods and growth in the pharmaceutical sector contribute to steady demand for flexible packaging solutions.

Innovations in advanced barrier films and growing consumer awareness around sustainability further strengthen Europe’s position as a key player with a robust market share in the packaging films industry.

Asia Pacific Packaging Films Market Trends

The Asia Pacific region dominates, commanding a substantial 40% market share in 2025. This leadership is driven by rapid industrialization, urbanization, and rising disposable incomes across countries such as China, India, and Southeast Asia.

Growing demand from key sectors such as food and beverage, pharmaceuticals, and consumer goods fuels the need for flexible and sustainable packaging solutions. Additionally, expanding e-commerce and the modernization of supply chains further boost packaging films adoption.

Government initiatives promoting environmentally friendly packaging and investments in advanced manufacturing technologies support the region’s robust growth. Asia Pacific’s strong market presence and evolving consumer preferences position it as a critical driver in the packaging films industry.

Competitive Landscape

The global packaging films market is marked by intense innovation and technological advancements, focusing on developing sustainable and high-performance materials. Companies are investing heavily in research to improve film durability, barrier properties, and biodegradability to meet evolving regulatory and consumer demands.

Strategic collaborations and expansions into emerging markets are common as firms aim to capture growing opportunities in food, pharmaceutical, and industrial packaging sectors. This dynamic environment drives continuous product enhancements and competitive pricing strategies across the industry.

Key Developments

- March 2024: Sealed Air Corporation reported a 14% revenue increase in its Cryovac® active packaging line, driven by antimicrobial films, maintaining ~12% share of the antimicrobial packaging market.

- 2023: Amcor PLC partnered with ExxonMobil and NOVA Chemicals to expand recycled polyethylene use in food and healthcare packaging, advancing its plastic waste reduction goals.

- 2023: Cosmo Films Ltd. introduced sustainable packaging innovations, including PCR-based BOPP and PVC-free films, enhancing applications in pharmaceutical and food sectors.

Companies Covered in Packaging Films Market

- AEP Industries Inc.

- Novolex

- Amcor PLC (Bemis Company Inc.)

- RKW SE

- Dupont Teijin Films

- Jindal Poly Films Ltd

- Innovia Films

- ProAmpac

- Cosmo Films Ltd

- SRF Limited

- Graphic Packaging International LLC

- Sigma Plastics Group

- Sealed Air Corporation

- Others

Frequently Asked Questions

The packaging films market is projected to reach US$ 120.0 Bn in 2025, driven by demand in food and beverage packaging.

Key drivers include flexible packaging demand, food industry growth, and sustainability trends.

The packaging films market is expected to grow at a CAGR of 4.7% from 2025 to 2032, reaching US$ 165.5 Bn.

Opportunities include biodegradable films, e-commerce growth, and smart packaging technologies.

Leading players include Amcor PLC, Sealed Air Corporation, Jindal Poly Films Ltd, and Cosmo Films Ltd.