- Beauty & Personal Care

- Tea Tree Oil Market

Tea Tree Oil Market Size, Share, and Growth Forecast, 2025 - 2032

Tea Tree Oil Market By Product Grade (Bulk Commodity-Grade Oil, Pharmaceutical-Grade Oil) Application, (Cosmetics & Toiletries, Household Cleaning & Hygiene), and Regional Analysis for 2025 - 2032

Tea Tree Oil Market Size and Trends Analysis

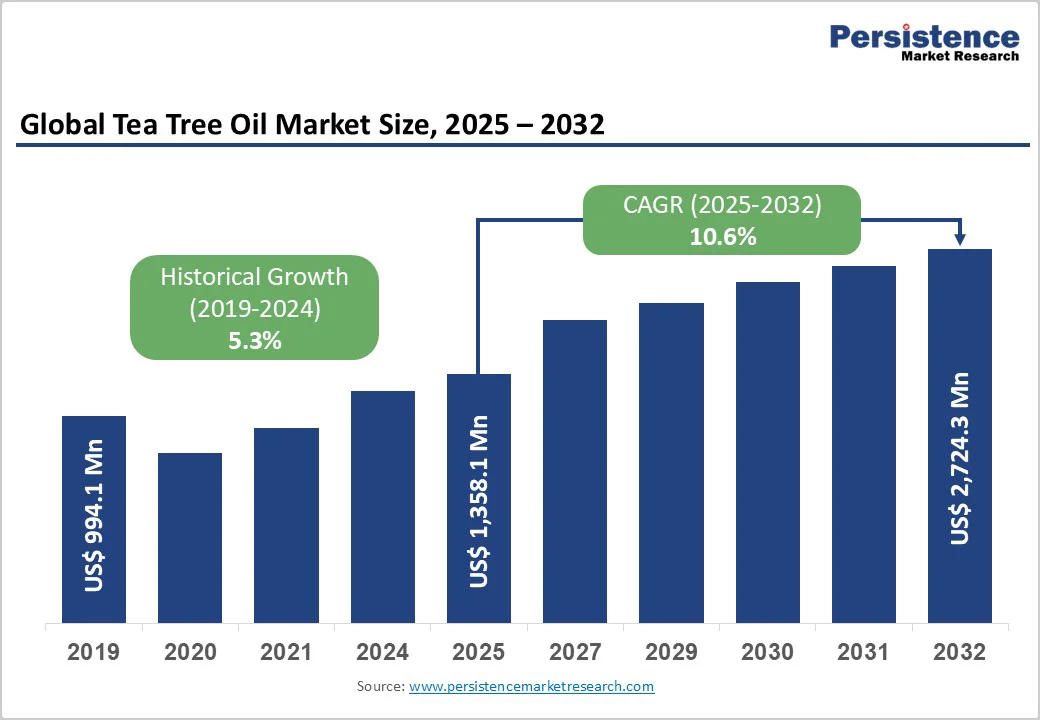

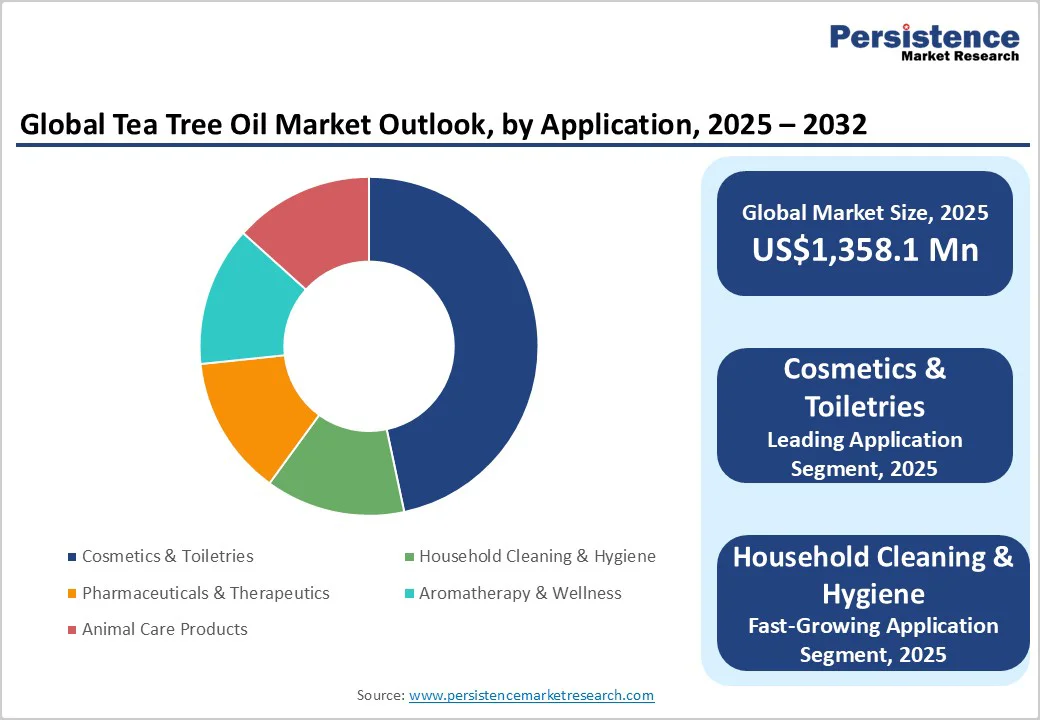

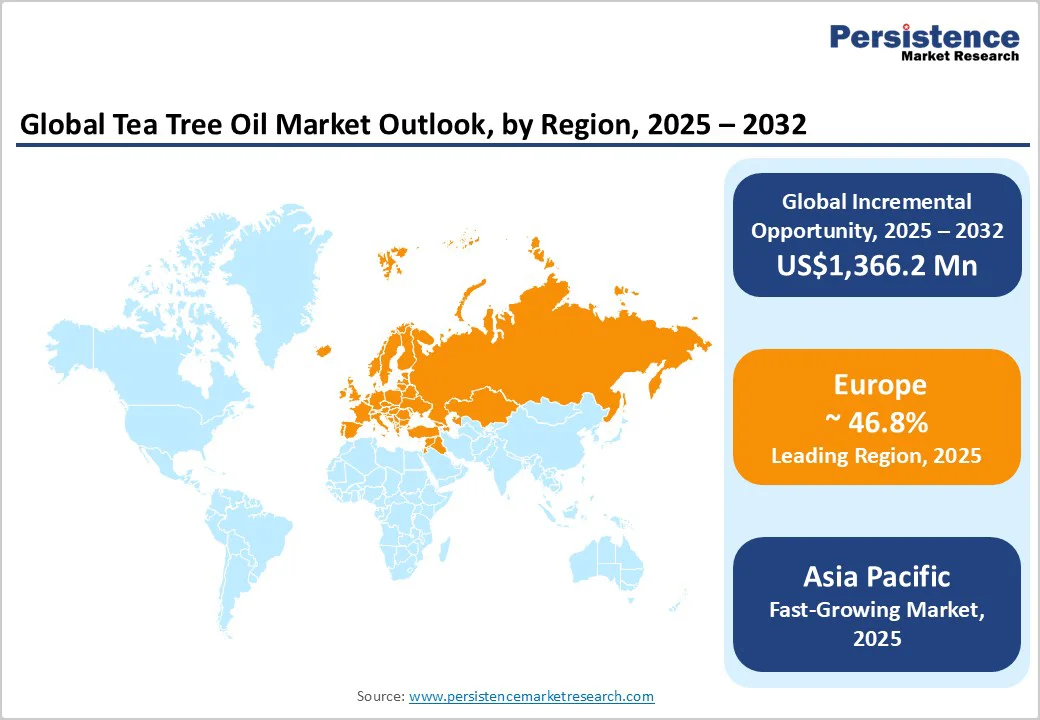

The global tea tree oil market is expected to reach US$1,358.1 million in 2025. It is expected to reach US$2,724.3 million by 2032, growing at a CAGR of 10.6% from 2025 to 2032, driven by rising demand for natural antimicrobial ingredients in cosmetics, personal care, and household cleaning products.

The rising use of cosmeceuticals and the growth of direct-to-consumer essential oil sales are driving long-term momentum. At the same time, tighter regulations raise short-term compliance costs but boost consumer trust and support premium pricing.

Key Industry Highlights

- Leading Region: Europe accounted for 46.8% of the tea tree oil market share, supported by premium cosmetics demand and strict EU regulatory frameworks ensuring consumer trust.

- Fastest-growing Region: Asia Pacific is driven by rising middle-class spending in China and India, and strong production in Australia.

- Investment Plans: Major producers in Australia and Asia are expanding plantations and distillation capacity, with several projects initiated in 2024 - 2025 to support pharmaceutical-grade and organic-certified supply.

- Dominant Product Grade: Bulk commodity-grade tea tree oil holds the largest share, representing over 54% of the global market 24, primarily used in cosmetics, toiletries, and household cleaning products.

- Leading Application: Cosmetics & Toiletries account for around 48.7% of total demand, led by acne-treatment products, haircare, and deodorants.

| Key Insights | Details |

|---|---|

| Tea Tree Oil Market Size (2025E) | US$1,358.1 Mn |

| Market Value Forecast (2032F) | US$2,724.3 Mn |

| Projected Growth (CAGR 2025 to 2032) | 10.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Shift toward Natural Ingredients in Personal Care and Therapeutic Applications

Cosmetics and toiletries account for the largest share of tea tree oil use, with nearly half of the global demand linked to acne treatments, anti-dandruff shampoos, deodorants, and haircare products.

Growing consumer preference for plant-based active ingredients has encouraged brands to reformulate by replacing synthetic antimicrobials with botanicals. The presence of terpinen-4-ol, tea tree oil’s primary antimicrobial compound, is a key differentiator. This trend has increased procurement of certified and traceable oils, reinforcing the market for premium-grade products.

Expanding Household and Hygiene Use

Following heightened hygiene awareness after the COVID-19 pandemic, household cleaning products and surface disinfectants with natural antimicrobial claims have witnessed strong uptake.

Tea tree oil has been incorporated into surface cleaners, wipes, and air fresheners, as well as aromatherapy blends. The growing demand in this segment is prompting suppliers to expand plantations, especially in Asia and Africa, while retailers and private-label manufacturers scale up product launches under “natural-clean” positioning.

Clinical Validation and Safety Research

Recent clinical studies and systematic reviews have strengthened the evidence base for tea tree oil’s antimicrobial and anti-inflammatory efficacy. Regulatory panels in the U.S. and Europe have also issued safety guidelines that reassure large manufacturers.

This growing body of scientific legitimacy is accelerating adoption in regulated cosmeceuticals and OTC topical products, allowing pharmaceutical-grade oil producers to capture higher margins. Suppliers offering quality guarantees, batch-level testing, and pharmaceutical compliance documentation are best positioned to benefit.

Barrier Analysis - Raw-Material Supply Variability and Adulteration Risk

The global supply of tea tree oil is concentrated in a few countries, primarily Australia, China, South Africa, and Kenya. Production is sensitive to climatic conditions, which leads to annual yield fluctuations and price volatility. Reports of adulteration, through dilution or substitution, also pose significant risks to product integrity. Buyers are increasingly demanding stricter supplier audits and certifications, which adds cost and complexity to the supply chain.

Regulatory and Safety Constraints

Global regulatory bodies, including the International Fragrance Association (IFRA) and the European Union’s Scientific Committee on Consumer Safety (SCCS), impose strict concentration limits on tea tree oil in cosmetics and personal-care formulations. These restrictions, while enhancing safety, reduce formulation flexibility and sometimes necessitate costly reformulations. For small and mid-sized companies, compliance costs can reduce profit margins by up to 3%.

Opportunity Analysis - Growth in OTC Therapeutic Formulations

With increasing clinical validation, tea tree oil has strong potential for expansion into regulated topical products such as antifungal creams and antiseptic solutions. Even capturing a small share of the global topical OTC market could generate millions in additional annual demand. Companies with the capacity to deliver pharmaceutical-grade oil and regulatory support services are well-positioned to benefit.

Premium Pricing Through Certification and Traceability

Rising consumer awareness has created a willingness to pay for certified organic and traceable tea tree oil. Certified lots can command a 15-40% price premium over commodity batches. This opportunity encourages producers to invest in advanced testing methods, cooperative farming contracts, and sustainability certifications to secure access to premium markets, particularly in Europe and North America.

Category-wise Analysis

Product Grade Insights

Bulk commodity-grade tea tree oil continues to dominate the market with a share of 54%, supplying large-scale cosmetic, toiletry, and cleaning product manufacturers. Demand in Europe and North America is anchored by multinational FMCG firms that use bulk oil in shampoos, creams, deodorants, and household cleaning solutions.

For instance, multinational personal-care companies have expanded their natural-ingredient portfolios, with tea tree oil-based shampoos and acne-treatment gels being introduced across mainstream retail channels. Commodity-grade producers in Australia and China remain the principal suppliers, with South Africa also increasing its export contribution.

These origins maintain a competitive advantage through economies of scale, although price volatility due to climatic variations remains a challenge.

Pharmaceutical-grade tea tree oil is recording the fastest expansion, primarily due to its integration into cosmeceutical formulations and OTC therapeutic applications. The growing evidence supporting antimicrobial and antifungal efficacy has led to its adoption in topical creams, antiseptic solutions, and medicated shampoos.

For example, in 2024, several dermatology brands in Europe introduced acne serums containing standardized pharmaceutical-grade tea tree oil, positioned as an alternative to synthetic antibacterials. Manufacturers offering batch-level purity certifications and safety documentation are capturing higher margins in regulated markets such as the U.S. and the EU, where compliance with stringent pharmacopoeial standards is a prerequisite.

Application Insights

Cosmetics and toiletries account for nearly 48.7% of the market. Skincare products addressing acne, inflammation, and sensitivity remain the strongest contributors, with tea tree oil replacing synthetic antimicrobials such as triclosan. Major retailers have expanded their “clean beauty” categories, with notable launches in 2023 - 2024 by both premium and mass-market brands incorporating tea tree formulations.

In haircare, anti-dandruff shampoos and scalp treatments are key drivers, supported by increasing consumer preference for botanical actives. Regulatory frameworks in developed economies have supported this segment by limiting the use of synthetic preservatives, further incentivizing the integration of natural oils.

Household cleaning and hygiene products represent the fastest-growing application area. The perception of tea tree oil as a safe, natural disinfectant has made it a favored ingredient in multipurpose cleaners, surface sprays, and even laundry solutions. A surge in demand was observed during the pandemic period and has since stabilized at elevated levels.

Recent product innovations include U.S.-based eco-friendly household brands launching plant-based cleaning sprays with tea tree oil as the primary antimicrobial agent. Private-label brands in Europe are also leveraging consumer trust in natural disinfectants to expand their household portfolios, creating consistent upward demand.

End-user Insights

Retail sales, including specialty outlets and e-commerce platforms, remain the dominant channel in value terms. Premium brands such as doTERRA, Young Living, and NOW Foods capture significant consumer attention with direct-to-consumer business models that emphasize product purity and traceability.

This channel benefits from consumer willingness to pay premium prices, particularly in markets with established aromatherapy and wellness cultures. E-commerce platforms have also played a critical role, with Amazon and regional online retailers expanding their “natural wellness” product lines, often highlighting tea tree oil for skincare, aromatherapy, and household use.

Industrial procurement by cosmetic giants, personal-care formulators, and OTC pharmaceutical firms is expanding at a rapid pace. These buyers prioritize consistency, quality certification, and long-term supply agreements.

In 2024, several multinational cosmetic manufacturers entered into multi-year procurement contracts with Australian plantations to secure pharmaceutical-grade oil. Such contracts reflect growing institutional reliance on standardized, traceable supply chains.

Partnerships between essential oil cooperatives in Africa and European pharmaceutical companies are emerging, designed to meet traceability demands while diversifying sourcing away from a few concentrated regions.

Regional Market Insights

North America Tea Tree Oil Market Trends - Strong Demand for Natural OTC and Personal Care Products

North America continues to be one of the largest consumer markets for tea tree oil, led by strong demand in the U.S. Consumer preference for natural personal-care and over-the-counter (OTC) dermatological products remains a key driver.

The U.S. Food and Drug Administration’s oversight of OTC labeling and safety standards has encouraged brands to source high-quality, well-documented ingredients. In Canada, a thriving organic product sector further supports regional demand, particularly in health and wellness categories.

Recent developments highlight continued market momentum. In 2024, doTERRA expanded its U.S. product line with new tea tree-based skin sprays targeted at younger consumers. NOW Foods also broadened its market reach by entering Canadian retail channels, reinforcing cross-border availability of essential oils. A new testing facility established in Utah in 2025 has enhanced local supply-chain verification efforts, supporting claims of authenticity and purity for retail oils.

Investment in North America is largely directed toward e-commerce infrastructure, traceability audits, and clinical testing partnerships. These initiatives are aimed at increasing consumer trust and ensuring regulatory compliance across distribution channels.

Europe Tea Tree Oil Market Trends - Premium Adoption Supported by Strict Safety Regulations

Europe remains the largest regional market for tea tree oil, accounting for nearly 46.8% of the global market share. Countries such as Germany, the U.K., France, and Spain demonstrate high levels of adoption across premium cosmetics, therapeutic formulations, and the essential oil retail sector.

The European Union's regulatory framework, including reviews by the Scientific Committee on Consumer Safety (SCCS), enforces strict concentration limits. While compliance requirements add to operational costs, they also create competitive opportunities for suppliers with robust safety certifications.

The market has seen several key developments. In 2023, The Body Shop relaunched its “Tea Tree Skincare” line in the U.K. and subsequently expanded across Europe. In 2024, a German pharmaceutical firm introduced a new acne-treatment gel formulated with pharmaceutical-grade tea tree oil, indicating increased acceptance in therapeutic applications. France-based natural beauty brand Yves Rocher launched a limited-edition hygiene range in 2025 that incorporated sustainably sourced tea tree oil.

Investment trends in Europe focus on sustainability certifications, enhanced laboratory testing capabilities, and strategic sourcing partnerships. The fragmented retail environment continues to offer growth opportunities for niche natural brands aiming to scale regionally.

Asia Pacific Tea Tree Oil Market Trends - Rapid Growth Fueled by Local Brands and Certified Supply

The Asia Pacific region is the fastest-growing market for tea tree oil, driven by increasing consumer awareness of natural cosmetic ingredients and the rapid expansion of local wellness brands. China and India serve as key consumption centers, while Australia maintains its position as the world’s largest producer and exporter of premium-grade tea tree oil. Countries in Southeast Asia are also emerging as important secondary manufacturing hubs, supplying both domestic and export-oriented markets.

Recent industry activity reflects strong regional growth. In 2024, Indian wellness company Himalaya launched a new herbal facewash line featuring tea tree oil, targeting younger consumers. In 2025, a Chinese contract manufacturer signed long-term supply agreements with Australian plantations to support the rising demand for herbal OTC creams. Australian producers, including Main Camp Natural Extracts, have responded by investing in plantation expansion and advanced distillation technologies during 2024 and 2025 to scale up production capacity.

Regulatory frameworks vary widely across the Asia Pacific region. However, premium buyers in markets such as Japan and South Korea often prefer certified Australian tea tree oil due to its proven quality and traceability. Investment priorities in the region include sustainable plantation practices, agronomy research, and integration with rapidly growing e-commerce distribution networks.

Competitive Landscape

The global tea tree oil market is moderately fragmented. Origin supply is concentrated in Australia, China, and South Africa, but branded retail is controlled by a mix of global wellness companies and specialty essential-oil brands. Market leaders differentiate through certification, terpinen-4-ol content guarantees, and sustainability credentials.

Regional distributors are consolidating to gain economies of scale. The leading strategies include investment in traceability and certification, expansion into pharmaceutical-grade oil, and direct-to-consumer retail growth. Partnerships with testing labs and contract farming agreements are key competitive differentiators.

Key Industry Developments

- In January 2025, a German dermatology company introduced a prescription-grade acne gel formulated with pharmaceutical-grade tea tree oil, marking one of the first EU-approved clinical OTC products containing the oil.

- In February 2024, Main Camp Natural Extracts (Australia) expanded its tea tree oil plantations and installed new distillation systems to increase pharmaceutical-grade oil output, ensuring traceability and compliance with European Pharmacopeia standards.

Companies Covered in Tea Tree Oil Market

- doTERRA

- Young Living Essential Oils

- NOW Foods

- Melaleuca Inc.

- Main Camp Natural Extracts Pty Ltd

- Naturally Australian Tea Tree Oil (NATTO)

- Jenbrook Pty Ltd

- Australian Botanical Products (ABP)

- G.R. Davis Pty Ltd

- Integria Healthcare

- Arista Industries

- The Body Shop International Limited

- Lebermuth, Inc.

- Ungerer & Company

- HealthAid Limited

- Biolandes

- NHR Organic Oils

- Plant Therapy Essential Oils

- Organic Harvest

- Eden Botanicals

Frequently Asked Questions

The tea tree oil market size is estimated at US$1,358.1 Million in 2025.

The tea tree oil market is projected to reach US$2,724.3 Million by 2032.

Key trends include rising demand for natural and plant-based personal-care products, growth in household cleaning applications, increased adoption of pharmaceutical-grade oil in OTC dermatology, and expansion of e-commerce and DTC retail channels.

The cosmetics & toiletries segment holds the largest share, accounting for nearly 48.7% of the tea tree oil market.

The tea tree oil market is expected to grow at a CAGR of 10.6% between 2025 and 2032.

The key players include doTERRA, Young Living Essential Oils, NOW Foods, Melaleuca Inc., and The Body Shop International Limited.