- Baby Care & Accessories

- Baby Nipples/Teats Market

Baby Nipples/Teats Market Size, Share, and Growth Forecast 2026 - 2033

Baby Nipples/Teats Market by Product Type (Standard Nipples, Naturally Shaped Nipples, Anti-vacuum or Vented Nipples, Orthodontic Nipples), Material Type (Plastic, Silicone, Latex, Others), Age Group (0 to 3 Months, 3 to 6 Months, 6 to 9 Months, 9+ Months), Flow Type (Cross-cut, Standard, Slow-flow), and Regional Analysis for 2026 - 2033

Baby Nipples/Teats Market Size and Trends Analysis

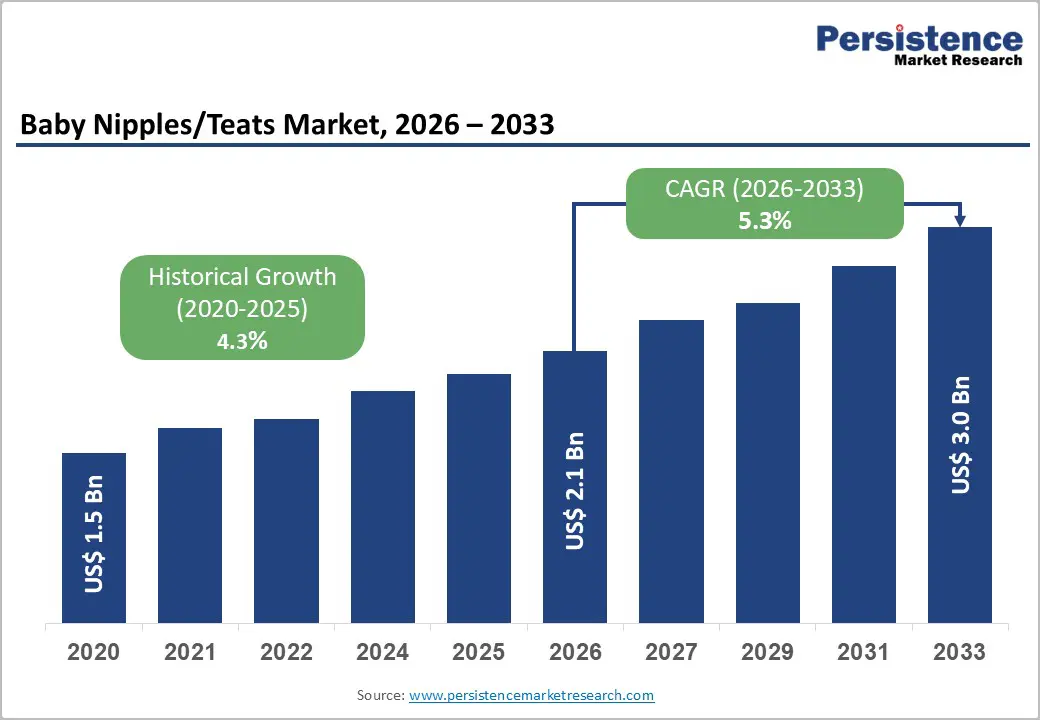

The global baby nipples/teats market size is supposed to be valued at US$ 2.1 billion in 2026 and is projected to reach US$ 3.0 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033.

This steady growth is anchored by a global live birth volume of approximately 132 million babies in 2025, per Our World in Data, citing United Nations projections, creating a structurally large and recurring annual consumer base for feeding accessories. Heightened parental awareness of infant feeding safety, driven by US FDA, EU LFGB, and CPSC regulatory mandates that eliminate BPA, phthalates, and latex from baby feeding products, is accelerating the trade-up from commodity plastic nipples to premium silicone and naturally shaped alternatives, thereby increasing average revenue per unit.

Key Industry Highlights:

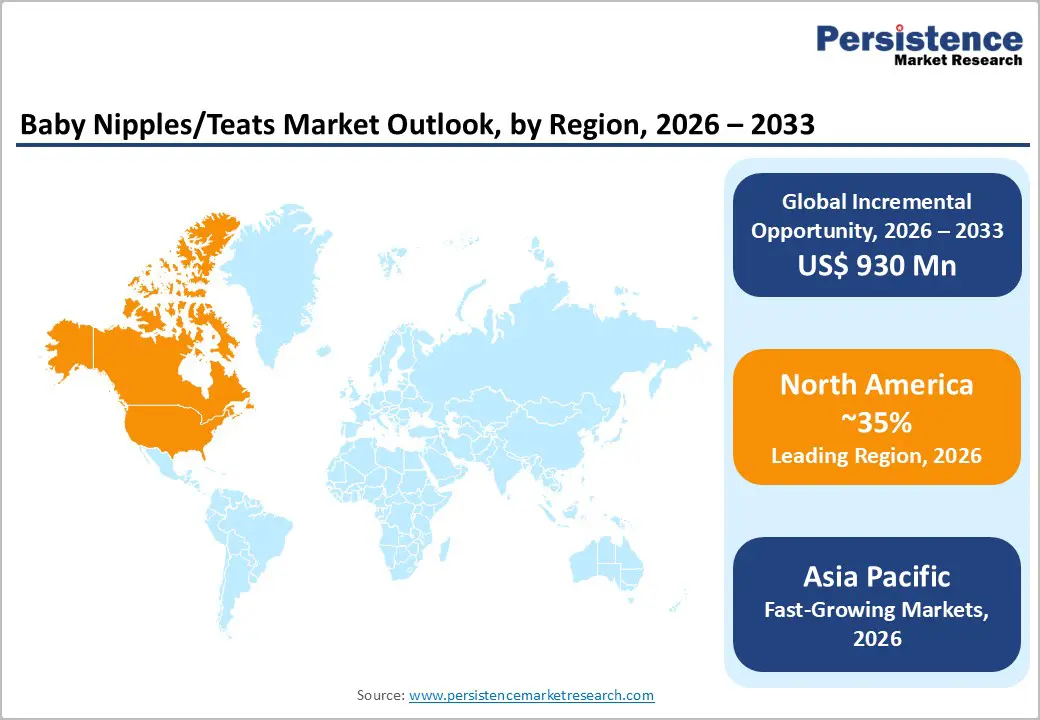

- Leading Region: North America leads in per-capita revenue and premium brand penetration, supported by the US FDA and CPSC safety compliance frameworks, approximately 3.6 million annual US births, and a highly engaged millennial parent demographic, guided by the American Academy of Pediatrics (AAP) and La Leche League International recommendations for clinically validated feeding products.

- Fastest Growing Region: Asia Pacific leads as the fastest-growing region, with India registering approximately 23 to 25 million births annually, the world's largest national birth cohort, while premium brand penetration and e-commerce expansion across Vietnam, Indonesia, and the Philippines are accelerating per-unit revenue growth.

- Leading Product: Naturally Shaped Nipples dominate the product type segment with approximately 35% market share, driven by clinical endorsements from lactation consultants and WHO breastfeeding recommendations that favor breast-mimicking designs for supplementary bottle feeding.

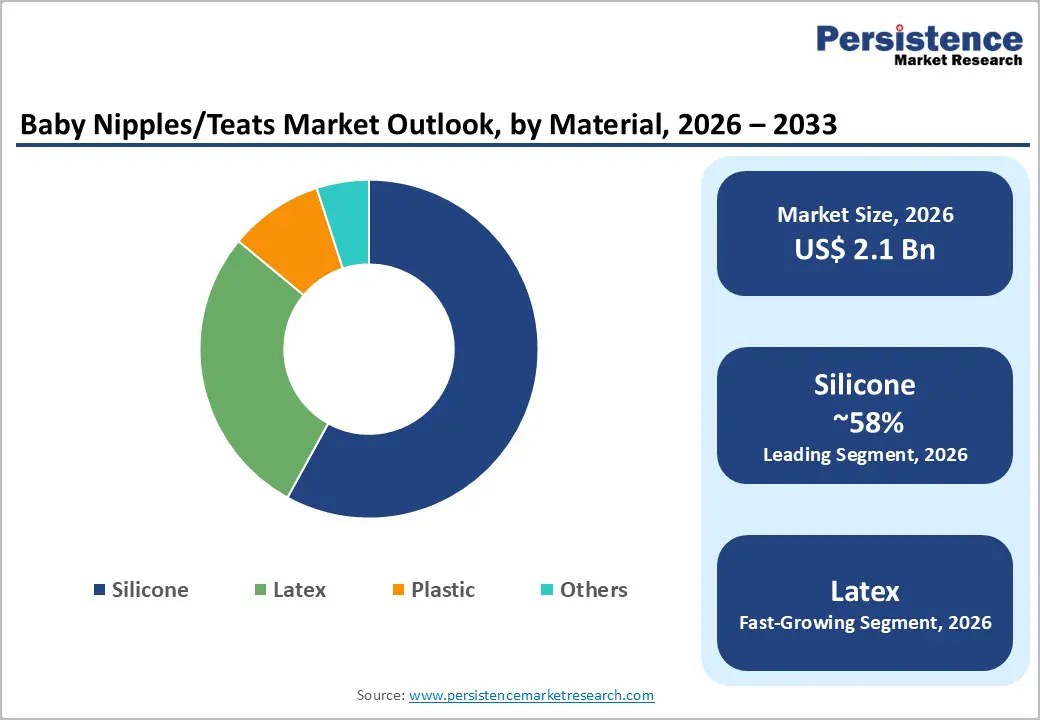

- Fastest Growing Product: Silicone leads the material type segment with approximately 58% market share, supported by FDA, LFGB, and EN 14350 compliance requirements that structurally advantage BPA-free, phthalate-free silicone over plastic and latex in certified markets.

- Opportunity: Medela AG's strategic exit from teat and bottle sales in July 2025, and Philips Avent and Pigeon's continued investment in clinical validation, create a high-value, competitive rebalancing opportunity for brands positioned to capture hospital-channel and premium clinical-segment market share.

| Key Insights | Details |

|---|---|

| Baby Nipples/Teats Market Size (2026E) | US$ 2.1 Bn |

| Market Value Forecast (2033F) | US$ 3.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Dynamics

Drivers - High Global Annual Birth Volume and Rising Working Mothers' Dependency on Bottle Feeding Sustain Recurring Demand

The Baby Nipples/Teats Market benefits from a structurally recurring consumer base driven by the global birth volume of approximately 132 million babies in 2025, per United Nations population data. Every newborn represents an immediate and time-sensitive purchase occasion for feeding accessories, creating non-discretionary demand that is largely insensitive to economic cycles. In parallel, female labor force participation rates have consistently risen globally, with the International Labour Organization (ILO) reporting that women's labor force participation in OECD economies exceeded 65% in 2024, thereby directly increasing demand for bottle-feeding accessories as primary or supplementary infant feeding solutions. Working mothers who combine breastfeeding with bottle feeding require high-quality nipples that minimize nipple confusion and maintain infant latch integrity. This behavioral driver structurally elevates repeat purchase rates and average selling price across the Baby Nipples/Teats Market, as parents opt for clinically validated, naturally shaped, and anti-colic designs over basic commodity alternatives.

Heightened Material Safety Regulations Accelerate Premiumization and Replacement Cycles in Developed Markets

Regulatory pressure on baby feeding product materials has become a powerful demand driver in the Baby Nipples/Teats Market, accelerating both product replacement and trade-up to safer, certified alternatives. The US Consumer Product Safety Improvement Act (CPSIA) restricts phthalates in children's products, while the US FDA regulates food-contact silicone under 21 CFR 177.2600, requiring compliance for all materials that contact infant food. The European LFGB standard and the EN 14350 safety specification for child-use and care articles apply to nipples sold in the EU. Consumer Reports' 2025 testing of major baby bottle brands confirmed that silicone and glass products showed no detectable BPA, lead, or phthalates, validating the material safety case for premium silicone nipples. Philips Avent's Natural Response teat system, Hegen's PPSU-based feeding system, and Pigeon's SofTouch teat series all carry comprehensive certification documentation, and parents in developed markets are actively consulting safety certifications before purchase, driving a structural shift to certified, premium-tier products.

Market Restraints

Declining Birth Rates in High-Income Markets Structurally Cap Addressable Consumer Base

The United Nations World Population Prospects 2024 confirmed that the global total fertility rate stands at 2.25 live births per woman, declining from 3.31 in 1990, with more than half of all countries, including China, Italy, the Republic of Korea, and Spain, now recording fertility below the replacement level of 2.1. In high-income markets that drive premium Baby Nipples/Teats Market revenue, specifically North America, Western Europe, and East Asia, fertility rates are structurally below replacement, constraining the addressable birth volume that generates nipple demand. While premiumization partially offsets this constraint, the demographic ceiling on annual birth cohort size limits the long-run volume growth potential in the world's highest-spending consumer markets.

WHO Breastfeeding Promotion Policies Moderate Supplementary Bottle Feeding Adoption

The World Health Organization (WHO) recommends exclusive breastfeeding for the first six months of an infant's life, with continued breastfeeding alongside complementary foods up to two years or longer. National health authorities in Europe, Asia, and Latin America have institutionalized this guidance through maternity leave policies, baby-friendly hospital initiatives, and restrictions on infant formula marketing under the WHO International Code of Marketing of Breast-milk Substitutes. These policies moderate the rate at which caregivers adopt bottle-feeding as the primary feeding method, particularly in Scandinavia, the UK, and Japan, where public health infrastructure actively supports compliance with exclusive breastfeeding. This directly constrains the absolute volume of nipple and teat procurement in policy-aligned markets.

Opportunity - Asia Pacific's Large and Young Birth Cohort Combined with Premiumization Represents the Market's Highest Growth Opportunity

Asia Pacific is the most commercially significant growth opportunity for the Baby Nipples/Teats Market, combining the world's largest absolute birth volumes with an accelerating willingness to pay for premium, certified feeding accessories as disposable incomes rise. India alone registers approximately 23 to 25 million births annually, the largest birth cohort of any country globally, while Indonesia, Vietnam, the Philippines, and Bangladesh collectively add tens of millions more. Premium nipple penetration in these markets remains low relative to the demonstrated consumer intent.

Pigeon Corporation's strategic expansion across Southeast Asian retail channels, combined with the proliferation of e-commerce platforms including Shopee, Lazada, and Amazon India, has dramatically lowered the distribution barrier for premium brands. Trends in the Baby Apparel Market across Asia Pacific similarly confirm that parents are actively increasing per-child expenditure across all infant product categories, including feeding accessories.

Innovation in Anti-Colic, Naturally Shaped, and Clinically Validated Nipple Designs Commands Premium Pricing in Western Markets

Product innovation around infant health outcomes, specifically the reduction of colic, gas, and nipple confusion, is generating a structurally superior premium product tier in the Baby Nipples/Teats Market that commands price points two to four times above commodity standard nipples. Philips Avent's Natural Response teat is clinically proven to mimic the breast's sensory feedback, enabling comfortable transition between breast and bottle feeding. Dr. Brown's anti-colic internal vent system, distributed by Handi-Craft Company, has demonstrated, in multiple peer-reviewed clinical studies, a 28% reduction in infant colic symptoms.

In July 2025, Medela AG announced the discontinuation of feeding bottle and teat sales effective July 1, 2025, reflecting a strategic refocus on breast pump and lactation solutions. This exit from a leading clinical brand creates a measurable white space for competitors to capture existing Medela customer relationships in the premium hospital-grade and clinically endorsed nipple segment, representing a direct portfolio expansion opportunity for players such as Hegen, Pigeon, and Mayborn Group.

Category-wise Analysis

Product Type Insights

Naturally Shaped Nipples lead the product type segment of the Baby Nipples/Teats Market, accounting for approximately 35% of global revenue. These nipples are engineered to replicate the shape, feel, and flexibility of the maternal breast, enabling infants to maintain consistent oral motor patterns during bottle feeding and facilitating latch-on for breastfed infants who require supplementary bottle feeding. Philips Avent's Natural Response teat, Pigeon SofTouch, and Hegen's PPSU system are leading commercial embodiments of this category. The segment's dominance reflects the broad trend toward breastfeeding support and the growing clinical guidance from lactation consultants recommending breast-mimicking nipples to prevent nipple confusion in neonates. As the WHO's exclusive breastfeeding recommendations create a category of parents who supplement rather than replace breastfeeding, naturally shaped nipples occupy the most clinically endorsed product tier in the Baby Nipples/Teats Market.

Material Type Insights

Silicone leads the material type segment, accounting for approximately 58% of global Baby Nipples/Teats Market revenue. Silicone dominates because it is inherently free of BPA, phthalates, and latex allergens, the three primary material safety concerns identified by the US FDA, EU LFGB, EN 14350, and CPSC, while offering superior thermal stability, durability, and optical clarity that enable parents to visually verify cleanliness. Food-grade silicone meeting FDA 21 CFR 177.2600 can withstand temperatures from -40°C to +250°C, making it suitable for steam sterilization, dishwasher cleaning, and microwave warming without chemical degradation. Consumer Reports' 2025 testing confirmed that silicone products showed no detectable BPA or phthalates, validating the material's safety profile compared with alternatives. Latex remains commercially active in cost-sensitive markets but is declining due to documented allergy risk with latex allergy prevalence estimated at 1 to 6% among the general pediatric population per MedlinePlus and progressively restrictive European regulatory review.

Age Group Insights

The 0 to 3 Months age group leads the Baby Nipples/Teats Market by segment, accounting for approximately 38% of global revenue. This leadership reflects the critical nature of the newborn feeding period, in which parents make their initial and most considered purchasing decisions for feeding accessories, typically under the guidance of healthcare professionals, lactation consultants, and pediatricians. During the first three months of life, infants transition between breast and bottle feeding most frequently, consuming the most nipple units per infant and driving the highest replacement rates. Philips Avent, Pigeon, and Chicco all maintain dedicated newborn-specific nipple lines with the lowest flow rates and breast-mimicking designs optimized for this age group.

Flow Type Insights

Slow-flow nipples lead the flow type segment, accounting for approximately 42% of the global Baby Nipples/Teats Market revenue. Slow-flow designs are universally recommended for newborns and young infants under three months, as they replicate the natural flow pace of breastfeeding and prevent the overfeeding, reflux, and gas accumulation that result from excessive milk flow velocity. Philips Avent's product guidance explicitly recommends starting with slow-flow teats and allowing the infant's drinking style, rather than age alone, to determine flow progression. Dr. Brown's slow-flow anti-colic nipple, endorsed across multiple clinical feeding studies, further reinforces the segment's dominance in the medically recommended feeding product tier.

Regional Insights

North America Baby Nipples/Teats Market Trends

The United States leads North American demand for baby nipples and teats, supported by a combination of strong birth cohort volume, high per-capita parental spending, and the most comprehensive regulatory oversight of baby product material safety of any major market. The US Consumer Product Safety Commission (CPSC) enforces phthalate restrictions under the CPSIA, while the FDA regulates food-contact silicone formulations, creating a well-defined compliance framework that effectively excludes low-quality imports and drives premiumization. Annual US births averaged approximately 3.6 million between 2020 and 2024, creating a consistent annual demand pool.

The US also benefits from a highly engaged millennial parent demographic, the largest generational cohort currently in peak parenting years, who research feeding products through certified pediatric and lactation resources before purchase. The American Academy of Pediatrics (AAP) and La Leche League International are influential sources of guidance that shape nipple product selection, particularly regarding anti-colic valve systems and breast-mimicking designs.

Europe Baby Nipples/Teats Market Trends

Europe's Baby Nipples/Teats Market operates within the world's strictest baby product safety regulatory environment, governed by the EN 14350 standard for child-use and care articles, the EU Directive 2011/65/EU (RoHS) restricting hazardous substances, and the European LFGB food-contact material standard. These frameworks have effectively eliminated non-silicone and non-certified materials from mainstream European retail shelves, creating a structurally premiumized market.

Spain's relatively higher fertility rate of approximately 1.2 births per woman in 2023, the lowest in Europe alongside Italy, creates specific demographic pressure on market volume in Southern Europe, while Nordic markets and the UK sustain premium unit economics. The EU's General Product Safety Regulation (GPSR), which entered into force in December 2024, further harmonizes product recall and online marketplace compliance requirements across all EU member states, reducing regulatory fragmentation for cross-border e-commerce in baby products.

Asia Pacific Baby Nipples/Teats Market Trends

Asia Pacific is both the largest-volume and fastest-growing region in the global Baby Nipples/Teats Market. India generates approximately 23 to 25 million births annually, while the South and Southeast Asian region broadly contributes over 60 million births per year, creating an enormous annual demand pool for infant feeding accessories. China, despite its declining fertility rate of approximately 1.09 per woman in 2022, maintains a substantial absolute birth volume of approximately 9 to 10 million annually, with a highly premium-oriented parenting culture concentrated in Tier 1 and Tier 2 cities investing heavily in certified, internationally branded feeding products.

Pigeon Corporation (Tokyo, Japan) is the dominant brand across Asia Pacific, with deep retail penetration from Japan and South Korea to India and Malaysia, offering age-specific teat systems and clinically validated, naturally shaped nipple designs. Japan's sophisticated baby product safety standard the Japan Food Sanitation Act and ST Mark (Safety Toy Standard) creates a high-quality domestic baseline that sets regional product expectations.

Competitive Landscape

The global Baby Nipples/Teats Market is moderately consolidated, with a small number of globally recognized infant care brands, including Koninklijke Philips N.V. (Philips Avent), Pigeon Corporation, Newell Brands (NUK and Graco), Mayborn Group (Tommee Tippee), and Chicco controlling the dominant share of premium-tier revenue in developed markets. The mid-tier is more fragmented, particularly in the Asia Pacific, where regional manufacturers compete on price.

Competitive differentiation centers on clinical validation, regulatory certification depth, pediatric endorsements, and digital direct-to-consumer engagement. Emerging business model trends include subscription-based nipple replacement services, personalized nipple flow selection tools integrated into brand apps, and hospital gifting programs that establish brand preference at the point of birth.

Key Developments:

- In July 2025, Medela AG announced the discontinuation of feeding bottle and teat sales effective July 1, 2025, reflecting a strategic refocus on breastfeeding and lactation support products, creating competitive white space in the clinically endorsed hospital-grade nipple segment for rivals including Pigeon, Hegen, and Mayborn Group.

- In 2024, Philips Avent (a brand of Koninklijke Philips N.V.) advanced its Natural Response teat system, featuring a patented valve that only releases milk when the baby actively sucks and swallows, clinically differentiating the product from competing naturally shaped nipple designs across North American and European retail channels.

Companies Covered in Baby Nipples/Teats Market

- NVIDIA Corporation

- Intel Corporation

- Advanced Micro Devices, Inc.

- Micron Technology, Inc.

- Broadcom Inc.

- Samsung Electronics Co., Ltd.

- SK Hynix Inc.

- Arm Limited

- AWS

- Alibaba Group

- Texas Instruments Incorporated

- Other Key Players

Frequently Asked Questions

The global Baby Nipples/Teats Market is projected to reach US$ 3.0 Bn by 2033, growing at a CAGR of 5.4% from an estimated US$ 2.1 Bn in 2026. The market recorded a historical CAGR of 4.5% between 2020 and 2025 from a base of US$ 1.6 Bn in 2020, driven by global birth volumes and premiumization trends.

The leading drivers are approximately 132 million global births in 2025 per United Nations data, creating a structurally recurring annual consumer base and heightened material safety regulations including the US CPSIA, FDA 21 CFR 177.2600, and European EN 14350 standard, which are accelerating trade-up from commodity plastic to premium certified silicone nipples across developed markets.

Silicone leads the material type segment with approximately 58% of global market revenue, driven by its compliance with FDA, LFGB, and EN 14350 food safety standards and its inherent freedom from BPA, phthalates, and latex allergens.

North America leads in per-capita revenue and premium brand penetration, supported by US FDA and CPSC safety compliance frameworks, approximately 3.6 million annual US births, and a highly engaged millennial parent demographic guided by American Academy of Pediatrics (AAP) and La Leche League International recommendations for clinically validated feeding products.

Leading players include Koninklijke Philips N.V. (Philips Avent), Pigeon Corporation, Mayborn Group (Tommee Tippee), Newell Brands (NUK), Hegen, Chicco (Artsana S.p.A.), Abbott Laboratories, Medela AG, Suavinex, Mee Mee, Ninio Baby, and Vital Innovations Ltd., competing across premium silicone, naturally shaped, anti-colic, and orthodontic nipple product tiers globally.