- Specialty & Fine Chemicals

- Stearate Market

Stearate Market Size, Share, and Growth Forecast 2026 - 2033

Stearate Market by Product Type (Zinc Stearate, Calcium Stearate, Magnesium Stearate, Other), Grade (Food, Pharmaceutical, Industrial), Application (Stabilizers, Lubricants, Anti-caking Agents, Emulsifiers & Thickeners, Other), Industry (Plastic and Rubber Industry, Pharmaceutical Industry, Personal Care & Cosmetics Industry, Food & Beverage Industry, Other), and Regional Analysis for 2026 - 2033

Stearate Market Size and Trend Analysis

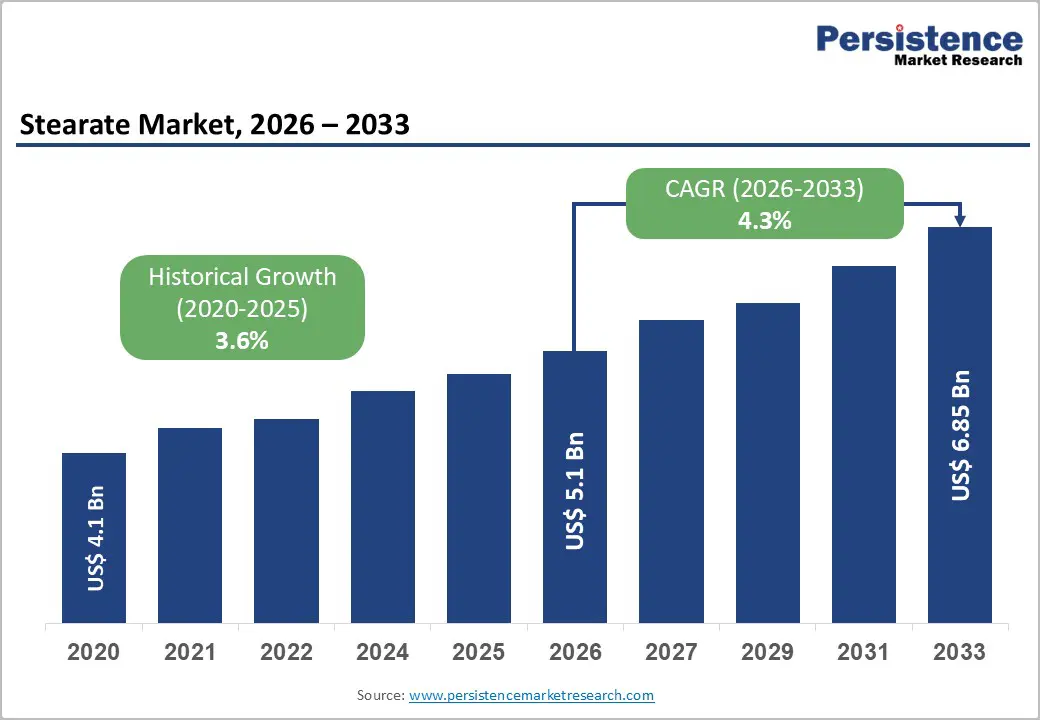

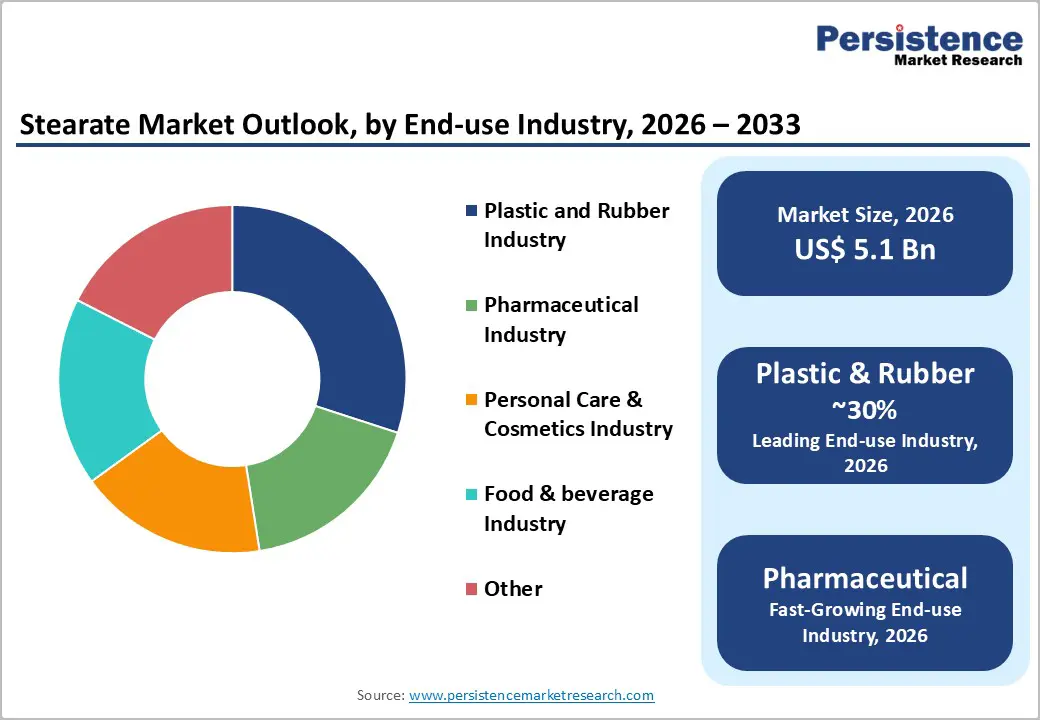

The global stearate market is valued at US$ 5.1 billion in 2026 and is projected to reach US$ 6.85 billion by 2033, growing at a CAGR of 4.3% between 2026 and 2033.

The stearate market is experiencing sustained growth, driven by rising demand from the plastics, rubber, pharmaceutical, and personal care industries, where stearates serve as essential lubricants, stabilizers, and processing aids. Expanding industrial activity in the Asia-Pacific, increasing PVC production, greater utilization of pharmaceutical excipients, and the rapid development of cosmetic formulations collectively support this upward trajectory. Additionally, the transition toward bio-based and environmentally compliant stearate grades, reinforced by stringent regulatory frameworks in North America and Europe, continues to strengthen long-term market fundamentals.

Key Industry Highlights:

- Regional Leader: Asia Pacific is the leading regional market, holding over 40% of global stearate demand, driven by China's massive PVC and plastics manufacturing sector and India's expanding pharmaceutical and construction industries.

- Fastest Growing Region: Europe emerges as the fastest growing region, with Germany, the United Kingdom, France, and the Netherlands serving as major centers for production and consumption.

- Leading Product: Zinc Stearate is the dominant product segment, commanding approximately 32% of global market share in 2026 due to its multifunctional role as a lubricant, release agent, and stabilizer across plastics, rubber, coatings, and cosmetics industries.

- Fastest Growing Product: The Pharmaceutical grade segment is the fastest-growing grade category, driven by surging global generic drug production and nutraceutical manufacturing, with India's pharma excipients market alone forecast to reach US$ 1.2 Bn by 2026.

- Kay Opportunity: Key market opportunity lies in bio-based and sustainable stearate formulations, aligned with tightening EU Green Deal regulations and global corporate ESG commitments, with manufacturers investing in RSPO-certified and plant-derived grades targeting premium pharmaceutical and personal care markets.

| Key Insights | Details |

|---|---|

| Stearate Market Size (2026E) | US$ 5.1 Bn |

| Market Value Forecast (2033F) | US$ 6.85 Bn |

| Projected Growth CAGR (2026 - 2033) | 4.3% |

| Historical Market Growth (2020 - 2025) | 3.6% |

Market Dynamics

Drivers - Expanding Plastics and Rubber Industry Demand

The plastics and rubber industries are the largest end-use sectors for these compounds. Stearates function as essential heat stabilizers, mold-release agents, and processing lubricants, ensuring dimensional accuracy and superior surface quality in polymer manufacturing. The increasing use of lightweight materials in automotive applications has further strengthened demand, as reduced vehicle weight directly improves fuel efficiency, thereby elevating the importance of stearate additives.

With global plastic production surpassing 400 million metric tons in 2023, the need for functional additives remains robust. Similarly, global rubber consumption reached 15 million tons, driven by rising tire production. Stearates’ thermal stability supports high-speed extrusion processes, reinforcing their critical role in enhancing product durability and overall industrial output.

Rising Pharmaceutical Excipient Applications

The pharmaceutical industry remains one of the most resilient growth drivers for the stearate market, supported by rising global medicine consumption and the rapid expansion of generic drug manufacturing. Magnesium stearate is the most widely utilized tablet lubricant in solid oral dosage forms, ensuring smooth tablet compression, preventing adhesion to equipment, and maintaining consistent weight and dosage.

Regulatory data indicate that over 50 novel drugs were approved annually by the U.S. FDA between 2020 and 2024, most of which incorporated magnesium stearate as a standard excipient. India’s excipient market is projected to reach US$ 1.2 billion by 2026, reflecting strong generic and nutraceutical output. Additionally, global tablet production exceeded 2.8 trillion units in 2024, reinforcing demand for reliable lubricants. In the food sector, calcium stearate provides essential anti-caking functionality, supporting product stability and shelf life.

Restraints - Volatility in Stearic Acid Raw Material Prices

Stearates are predominantly produced from stearic acid, which is derived from animal fats and vegetable oils such as palm oil and tallow. However, fluctuations in raw material prices present a persistent structural challenge for manufacturers. For instance, palm oil prices increased by 35-40% between 2021 and 2022 due to supply chain disruptions, adverse weather conditions, and export restrictions imposed by major producing countries such as Indonesia.

Such volatility compresses manufacturer margins and introduces uncertainty in downstream pricing, often delaying procurement decisions and discouraging capital investment. The industry’s dependence on agricultural commodities further heightens exposure to climate-related risks and geopolitical disturbances, thereby limiting profitability and reducing the predictability of product pricing.

Regulatory Pressure on Zinc-Containing Compounds

Increasing regulatory scrutiny of heavy metal-containing chemical additives has emerged as a significant constraint for certain stearate categories. Zinc stearate, although widely used across plastics, rubber, and coatings, is subject to heightened environmental and health-related oversight in the European Union and other jurisdictions. Under the EU’s REACH framework, stricter limits on zinc compounds, due to their aquatic ecotoxicity, are compelling manufacturers to undertake reformulation efforts, resulting in short-term demand disruptions and higher compliance costs.

Smaller producers without adequate R&D capabilities risk displacement by competitors, while larger firms must absorb additional operational expenses. REACH and EPA guidelines impose impurity caps as low as 0.1%, and non-compliance led to the rejection of 15% of EU chemical imports in 2024, increasing production costs and restraining growth in personal care and cosmetics markets.

Opportunity - Bio-based and Sustainable Stearate Formulations

The growing emphasis on bio-based and sustainable specialty chemicals presents a significant long-term opportunity for participants in the stearate market. As global sustainability commitments strengthen and regulatory bodies in the European Union and North America advance green-chemistry policies, demand for plant-derived and RSPO-certified stearates is expanding rapidly. Manufacturers capable of verifying sustainable sourcing and demonstrating reduced environmental impact are increasingly accessing premium segments in pharmaceutical, food-grade, and personal care applications.

Companies such as Peter Greven GmbH & Co. KG are expanding bio-based production capacities and entering new markets, underscoring the commercial viability of sustainable stearate technologies. The clean-label movement further accelerates this trend, while rising global demand for bio-chemicals and investments in oleochemical advancements enable firms to capture higher-value opportunities among environmentally conscious consumers.

Rapid Industrialization and Demand Surge in Southeast Asia and India

Southeast Asia and India constitute significant high-growth regions for stearate market participants, with demand expanding at 7-9% annually, and notably higher growth observed in mature markets. Vietnam’s plastics manufacturing capacity has increased by approximately 15% per year since 2021, while India’s rapid construction activity and rising PVC pipe installations continue to generate strong and sustained demand for calcium stearate, particularly for use as a cement additive and PVC heat stabilizer.

Furthermore, import tariffs ranging from 8% to 15% on finished stearate products in these markets encourage the establishment of localized production facilities and strategic joint ventures, which enhance cost efficiency and market accessibility. Companies developing manufacturing bases in Indonesia, Thailand, Vietnam, or India will be well-positioned to capture superior volume growth throughout the 2026-2033 period.

Category-wise Analysis

Product Type Insights

Zinc stearate holds the dominant position in the global stearate market, accounting for nearly 32% of the total market share in 2026. This leadership is driven by its exceptional versatility across a wide range of industrial applications. The compound functions simultaneously as a lubricant, release agent, stabilizer, and flattening agent, making it a preferred additive in the plastics, rubber, paints and coatings, and cosmetics industries.

In plastics processing, zinc stearate enhances operational efficiency by reducing equipment downtime and improving the surface finish of PVC pipes, profiles, and cable insulation. Its role as a texture-enhancing and smoothing agent in pressed powders and creams further broadens its utility in cosmetics. The compound’s extensive adoption across both advanced and emerging markets solidifies its continued dominance over the forecast period.

Grade Insights

The industrial-grade segment remains the leading category in the stearate market, accounting for 54.3% of overall consumption due to its extensive use across the plastics, rubber, coatings, and construction industries. Industrial-grade variants, including zinc and calcium stearates, are consumed in significantly higher volumes than pharmaceutical or food-grade alternatives, primarily because of the large-scale output associated with polymer processing and surface coating applications worldwide.

The plastics sector alone, which accounts for nearly 30% of total stearate usage, relies heavily on industrial-grade materials for essential heat-stabilization and lubrication. Although pharmaceutical and food grades command premium pricing, their contribution to total volume remains relatively modest. Demand for industrial-grade stearates is particularly strong in Asia-Pacific manufacturing hubs, where rapid urbanization, expanding PVC production, and intensified rubber processing continue to accelerate consumption.

Application Insights

Stabilizers constitute the leading application segment in the stearate market, with 32% market share, supported by their essential function in PVC processing and the broader polymer manufacturing chain. Calcium stearate and zinc stearate form the core of modern lead-free thermal stabilizer systems, widely adopted across the PVC industry following the global discontinuation of lead-based stabilizers. These metallic stabilizers protect polymer integrity by preventing chain degradation during high-temperature processing of PVC pipes, window profiles, flooring materials, and electrical cable insulation.

Continued investment in PVC infrastructure, particularly in rapidly expanding markets across South and Southeast Asia, further reinforces this segment’s prominence. Moreover, regulatory initiatives in the EU and other regions aimed at phasing out heavy metal stabilizers have shifted formulation preferences toward metallic stearate co-stabilizer systems, sustaining strong demand for stabilizer-grade stearates throughout the forecast period.

Industry Insights

The plastic and rubber industry represents the largest end-use sector for stearates, with 30% market share, driven by consistent and high-volume consumption across global manufacturing activities. Within this segment, stearates serve as essential heat stabilizers, internal and external lubricants, mold-release agents, and processing aids, all of which are critical for efficient large-scale polymer production. The global plastics industry’s sustained growth, driven by packaging, automotive, construction, and electrical applications, continues to expand demand for stearates.

With annual plastic production surpassing 400 million metric tonnes, even minor increases in stearate usage per unit output generate significant incremental demand. Emerging applications in biodegradable polymer processing, where stearates enhance melt flow and surface quality, further broaden their relevance. China and India remain key demand centers, benefiting from extensive polymer manufacturing ecosystems.

Regional Insights

North America Stearate Market Trends

North America constitutes a mature yet innovation-oriented market for stearates, with the United States retaining market leadership due to its well-established pharmaceutical, personal care, and specialty polymer industries. The U.S. pharmaceutical sector, regulated by stringent FDA requirements, necessitates high-purity stearate excipients for oral solid dosage forms, thereby sustaining strong demand for premium-grade products.

The region’s growing emphasis on sustainable chemistry, supported by EPA guidelines and expanding corporate ESG commitments, is further accelerating the shift toward bio-derived stearates in personal care and food processing applications. Key industry participants, including Dover Chemical Corporation and PMC Biogenix, Inc., play a central role in supplying metallic and polymer-grade stearates. Increasing regulatory scrutiny and preference for clean-label, traceable, and sustainably sourced materials continue to shape formulation choices across North American markets.

Europe Stearate Market Trends

Europe remains a prominent and highly regulated market for stearates, with Germany, the United Kingdom, France, and the Netherlands serving as major centers for production and consumption. Under the REACH framework, the European Chemicals Agency (ECHA) continues to enforce stringent formulation and compliance standards, particularly for zinc-containing stearates, where concerns over aquatic ecotoxicity have driven significant reformulation efforts in the coatings and plastics sectors.

Manufacturers across the region are increasingly transitioning to vegetable-derived and RSPO-certified stearate grades, aligning with European Green Deal objectives and rising sustainability expectations. Baerlocher GmbH and Peter Greven GmbH & Co. KG anchor the regional supply landscape, with Peter Greven recognized globally for its high-purity pharmaceutical-grade LIGAMED® stearates. Europe’s emphasis on product quality, traceability, and regulatory harmonization continues to strengthen the global competitiveness of its producers.

Asia Pacific Stearate Market Trends

Asia Pacific represents the largest regional market for stearates, accounting for more than 40% of global demand and supported primarily by strong industrial activity in China and India. China leads regional production due to its expansive oleochemical manufacturing base, competitive cost structure, and substantial demand from the plastics, rubber, and construction sectors. Key producers such as CHNV Technology Co., Ltd. and Hangzhou Oleochemicals continue to scale capacity to serve both domestic and export markets, although challenges persist regarding quality perceptions in high-specification pharmaceutical and personal care applications.

India is emerging as a major growth hub, driven by its expanding generic pharmaceutical manufacturing, rising construction activity, and increasing consumption of personal care products. Additionally, Indonesia, Thailand, and Vietnam are registering stearate demand growth rates of 6-9% annually, reinforcing the Asia Pacific’s strategic importance through 2033.

Competitive Landscape

The global stearate market is moderately fragmented, with Baerlocher GmbH holding about 10% market share, while the top three companies account for roughly 23% of total revenue. The landscape includes major multinational chemical producers alongside competitive regional players focusing on pricing, product purity, and specialized applications. Leading companies differentiate through vertical integration with stearic acid sourcing, proprietary formulation capabilities, and stringent regulatory-grade manufacturing standards. Key emerging trends include increased investment in bio-based stearate R&D, adoption of sustainability-linked certifications such as RSPO and ISO 14001, regional capacity expansion, and targeted acquisitions aimed at strengthening technology portfolios and end-use coverage.

Key Developments:

- April 2025: Peter Greven has unveiled a new range of bio-based magnesium stearate grades. These products, derived from RSPO-certified palm oil, are tailored to meet the stringent requirements of pharmaceutical tablet formulations, emphasizing sustainability and quality.

- May 2025: Baerlocher plans to construct a metallic stearate manufacturing plant in Malaysia. The MYR 220 million facility is projected to produce 30 kta of calcium-zinc (Ca-Zn) stearates, catering to growing regional demand. Operations are expected to begin in 2027.

- January 2025: Univar Solutions LLC formed an exclusive North American distribution agreement with Syensqo for beauty care ingredients, expanding its specialty chemicals portfolio. The partnership strengthens its position in personal care markets by enabling integrated solutions that combine calcium stearate with other cosmetic ingredients.

Top Companies in Stearate Market

- Baerlocher GmbH (Munich, Germany): Founded in 1823, Baerlocher is among the world's leading suppliers of metallic stearates and PVC additives, with revenues of approximately US$ 541.7 million and operations spanning Europe, Asia, and the Americas. Its extensive portfolio, deep R&D expertise in heat stabilizer systems, and commitment to sustainable sourcing via RSPO-certified palm derivatives make it the benchmark competitor in the global stearate market.

- Peter Greven GmbH & Co. KG (Bad Münstereifel, Germany): Peter Greven is the recognized global market leader for pharmaceutical-grade stearates, operating dedicated GMP-certified manufacturing facilities in the Netherlands under its flagship LIGAMED® product line. The company serves pharmaceutical, food, and industrial clients globally and is actively expanding its sustainable oleochemical portfolio, including bio-based stearates and lubricant esters, with new U.S. market entry plans announced in 2024.

- FACI SPA (Italy): FACI is one of Europe's oldest and most established producers of metallic stearates, with a diversified product range spanning zinc, calcium, magnesium, and other metallic stearates for plastics, rubber, pharmaceutical, and personal care applications. The company operates integrated manufacturing facilities and has been strategically expanding its commercial footprint in Latin American and Asian markets to capture emerging economy demand growth.

Companies Covered in Stearate Market

- Dover Chemical Corporation

- Baerlocher GmbH

- FACI SPA

- Global Calcium PVT LTD

- ICC Industries, Inc.

- CHNV Technology Co., Ltd.

- Seoul Fine Chemical

- Hangzhou Oleochemicals

- James M. Brown Ltd.

- Peter Greven GmbH & Co. KG

- PMC Group (PMC Biogenix, Inc.)

- Valtris Specialty Chemicals

Frequently Asked Questions

The global Stearate market is valued at US$ 5.1 Bn in 2026 and is projected to reach US$ 6.8 Bn by 2033, growing at a CAGR of 4.3% over the forecast period. Historically, the market grew at a CAGR of 3.6% between 2020 and 2025, reflecting steady demand from the plastics, pharmaceutical, and personal care industries.

The primary demand drivers for the stearate market include the expanding plastics and rubber processing industries, which account for nearly 30% of global stearate consumption, and rising pharmaceutical excipient demand, particularly magnesium stearate usage in tablet manufacturing. Rapid urbanization and industrial growth in Asia Pacific economies, alongside the transition to bio-based stearate formulations driven by sustainability mandates, are further accelerating market growth.

Zinc Stearate is the leading product type segment, accounting for approximately 32% of global market share in 2024. Its dominance is attributed to its multifunctional utility as a lubricant, mold release agent, thermal stabilizer, and flattening agent across the plastics, rubber, paints, pharmaceutical, and cosmetics industries, making it the most widely deployed stearate type globally.

Asia Pacific is the dominant regional market, accounting for over 40% of global stearate demand, driven by robust plastics manufacturing in China, expanding pharmaceutical production in India, and surging PVC and construction activity across Southeast Asian economies, including Vietnam, Indonesia, and Thailand.

The most significant emerging opportunity lies in bio-based and sustainable stearate formulations, driven by the EU Green Deal, RSPO certification programs, and corporate ESG commitments. Manufacturers offering vegetable-derived, clean-label stearates with auditable, sustainable supply chains are gaining preferential access to premium-priced pharmaceutical, food-grade, and personal care market segments globally.

The global Stearate market features prominent players including Baerlocher GmbH, Peter Greven GmbH & Co. KG, FACI SPA, Dover Chemical Corporation, PMC Biogenix, Inc., Valtris Specialty Chemicals, CHNV Technology Co., Ltd., Hangzhou Oleochemicals, Seoul Fine Chemical, and James M. Brown Ltd., among others. The top three players collectively control approximately 23% of global revenue.