- Beverages

- Ready-to-Drink (RTD) Tea Market

Ready-to-Drink (RTD) Tea Market Size, Share, and Growth Forecast, 2026 - 2033

Ready-to-Drink (RTD) Tea Market by Product Type (Black Tea, Herbal Tea, Green Tea, Oolong Tea), Nature (Conventional, Organic), Flavor (Fruit, Lemon, Spice), and Regional Analysis for 2026 - 2033

Ready-to-Drink (RTD) Tea Market Share and Trends Analysis

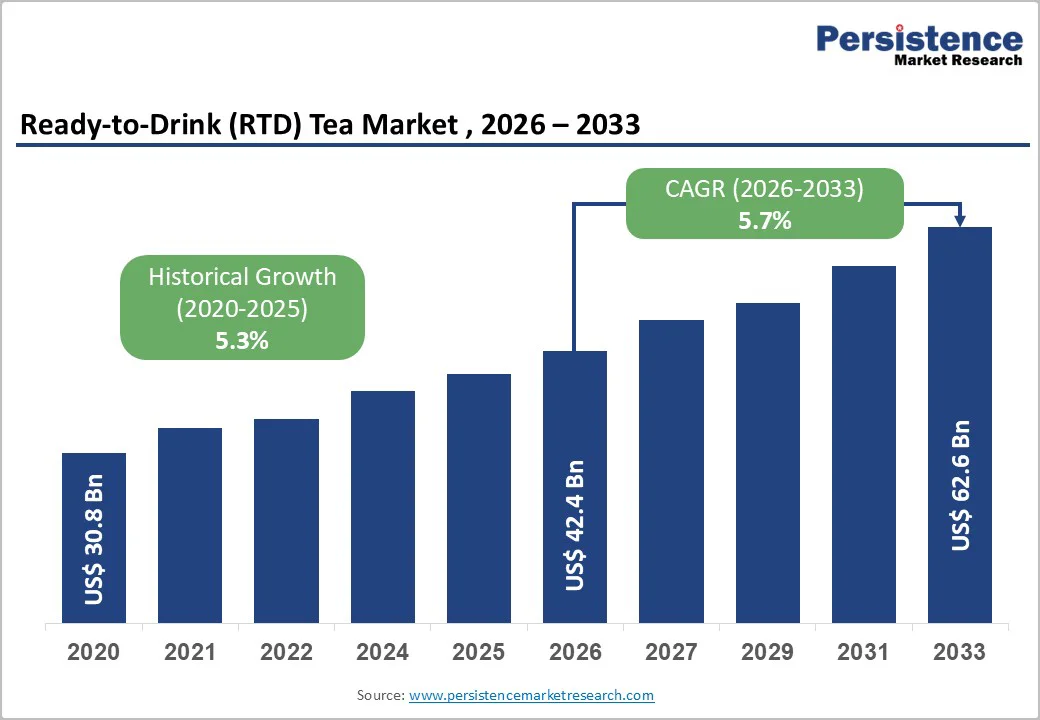

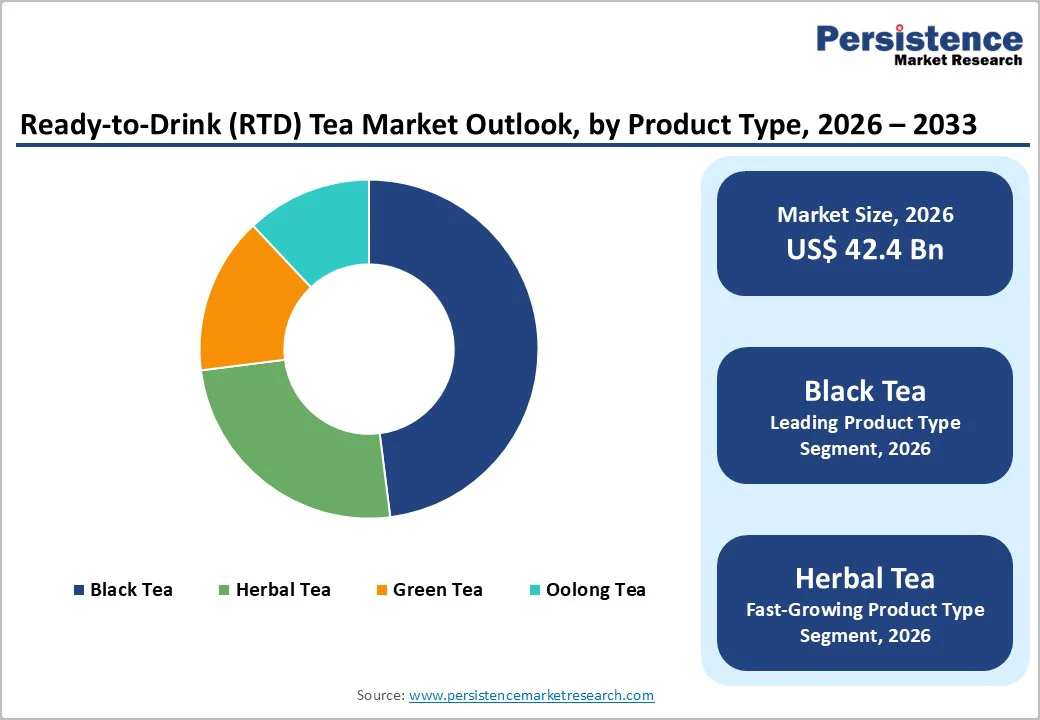

The global ready-to-drink (RTD) tea market size is likely to be valued at US$ 42.4 billion in 2026, and is projected to reach US$ 62.6 billion by 2033, growing at a CAGR of 5.7% during the forecast period 2026−2033. This market expansion reflects the convergence of health-conscious consumer behavior, demand for convenient on-the-go beverages, and continuous product innovation in flavors and functional ingredients.

The market's growth trajectory is underpinned by demographic shifts favoring urban populations, increasing disposable incomes in emerging markets, and the premiumization trend across developed economies. RTD tea's positioning as a healthier alternative to carbonated beverages, combined with its natural antioxidant properties and diverse flavor profiles, continues to attract health-aware consumers globally.

Key Industry Highlights

- Product Leadership: Black tea is set to lead with an approximate 46% revenue share in 2026, while herbal tea is likely to grow the fastest during the 2026-2033 forecast period.

- Leading & Fastest-growing Nature: Conventional is slated to be the dominant segment with an estimated 75.8% share in 2026, whereas organic is anticipated to be the fastest-growing segment through 2033.

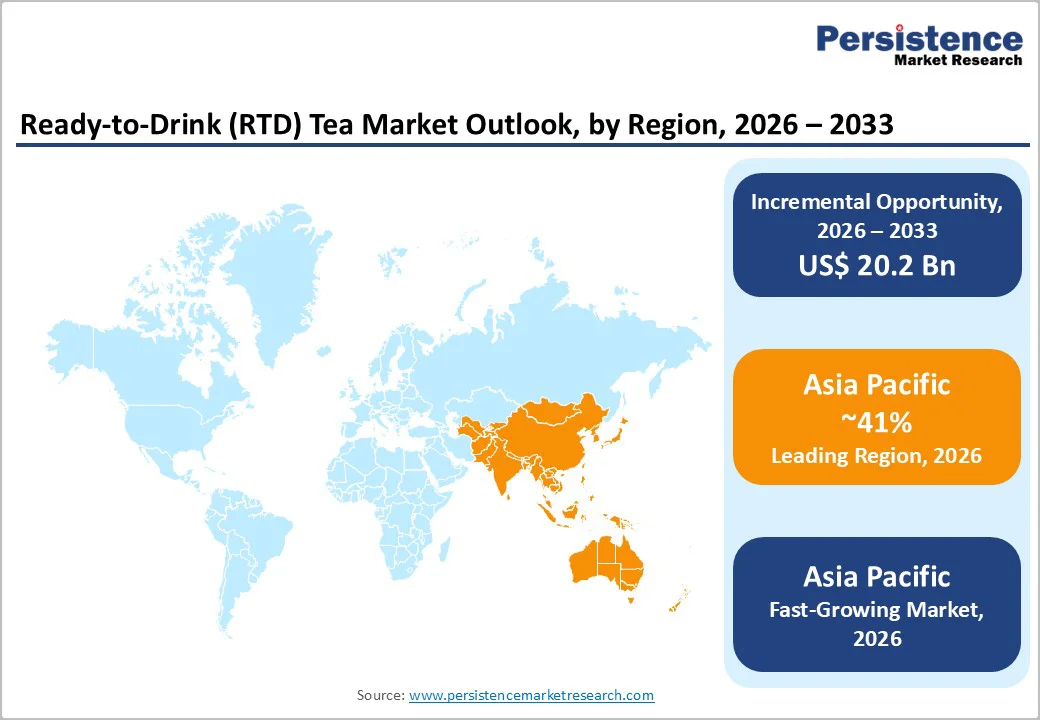

- Dominant Region: Asia Pacific is expected to command about a 41% market share in 2026, and the regional market is also slated to grow the fastest through 2033, owing to the deep-rooted tea-drinking traditions.

- May 2025: Starbucks launched a new RTD “Coffee Tea” line in China, supported by a distinctive bottle structure and visual identity to emphasize quality and authenticity.

| Key Insights | Details |

|---|---|

|

Ready-to-Drink (RTD) Tea Market Size (2026E) |

US$ 42.4 Bn |

|

Market Value Forecast (2033F) |

US$ 62.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Health and Wellness Consciousness Driving Consumer Preference

The global shift toward healthier beverage consumption patterns is a primary catalyst for RTD tea market expansion. Rising concerns about lifestyle-related diseases are prompting consumers to reduce their intake of traditional sugary drinks and seek more balanced, low-calorie options. RTD tea has emerged as a compelling alternative, offering both refreshment and perceived wellness benefits. Products enriched with antioxidants, particularly polyphenols and catechins, strongly resonate with health-conscious consumers who prioritize cardiovascular support, weight management, and immune system enhancement in their daily beverage choices.

Manufacturers are adapting their product portfolios to align with these evolving expectations. They are reformulating ready-to-drink tea offerings with natural sweeteners such as stevia and organic honey, while phasing out artificial additives that are increasingly viewed with consumer skepticism. Sugar-free and low-sugar variants are being developed to preserve familiar taste profiles while reducing health risks associated with excessive sugar intake. At the same time, cleaner labels, simpler ingredient lists, and positioning around natural, functional benefits are helping to build stronger consumer trust and brand loyalty. This coordinated focus on wellness, taste, and transparency is reinforcing RTD tea’s position as a preferred option in the modern beverage landscape.

Sugar Content Concerns and Regulatory Pressures to Subdue Market Prospects

Rising awareness of the health risks tied to high added-sugar intake is putting pressure on classic ready-to-drink tea recipes that depend on heavy sweetening. As consumers connect frequent sugar consumption with conditions such as obesity and type 2 diabetes, demand is shifting toward options positioned as better-for-you, with lower sugar and simpler ingredient statements. This change also shows up at shelf level, where shoppers compare nutrition panels and choose beverages that fit daily wellness routines rather than occasional indulgence.

For RTD tea brands, the practical response is to treat sugar reduction as both a formulation task and a trust-building strategy. In the United States, low, no, or reduced sugar claims appear on about one-third of RTD tea launches, which signals that mainstream players already see sugar management as a competitive requirement, not a niche feature. To keep products appealing while lowering sweetness, teams can pair gradual reformulation with taste-forward innovation such as cold-brew profiles, botanical blends, and clearly communicated clean-label positioning that supports premium pricing without relying on sugar for flavor impact.

Premiumization and Organic Product Segment Expansion

The growing consumer willingness to pay higher prices for organic, sustainably sourced, and functionally enhanced RTD tea products is creating substantial revenue growth opportunities for manufacturers. Health-conscious and environmentally aware shoppers increasingly seek offerings that combine perceived wellness benefits with ethical and responsible sourcing. This shift in preferences is especially evident among younger, urban, and higher-income consumer groups, who often treat product origin, ingredient quality, and sustainability credentials as key decision-making criteria. As a result, RTD tea brands positioned around superior quality, natural ingredients, and strong ethical values are able to command a clear price premium in the marketplace.

Manufacturers can effectively leverage this trend by developing certified organic tea lines, adopting transparent and traceable supply chain practices, and investing in eco-friendly packaging formats such as recyclable bottles and biodegradable cartons. These initiatives not only support environmental goals but also enhance brand differentiation in increasingly crowded retail environments. Premium RTD tea products that emphasize authenticity, clean labels, and functional benefits such as relaxation, immunity, or digestion support tend to foster stronger brand loyalty. This premium segment enables higher margin realization while reinforcing long-term brand equity among consumers who prioritize quality, integrity, and environmental responsibility in their beverage choices.

Category-wise Analysis

Product Type Insights

Black tea is anticipated to be the leading product type in 2026, holding an approximate 46% of the ready-to-drink tea market revenue share. The compatibility of black tea with a wide range of sweeteners and milk additions enhances its versatility and allows it to cater to diverse consumer taste preferences. Its strong presence in Western markets, particularly in North America and Europe, combined with deeply rooted consumption traditions in South Asian and Middle Eastern regions, underpins steady and resilient demand. This broad geographic acceptance reinforces black tea’s role as a core RTD tea base across multiple demographics. The segment also benefits from extensive distribution networks, high brand recognition, and long-standing consumer familiarity, which collectively strengthen its commercial appeal. As a result, black tea remains the foundational product type for many major beverage manufacturers, serving as a reliable volume driver and a platform for flavor extensions and premium line innovations.

Herbal tea is likely to be the fastest-growing segment during the 2026-2033 forecast period. This strong growth is being driven by rising consumer awareness of the health benefits associated with herbal tea consumption, especially among health-conscious individuals looking for caffeine-free alternatives. Manufacturers are responding by launching innovative herbal blends that incorporate functional ingredients such as chamomile for stress relief, peppermint for digestive comfort, and hibiscus for cardiovascular support, each designed to address specific wellness needs.

Nature Insights

The conventional segment is slated to be dominant with an estimated 75.8% of the RTD tea market revenue share in 2026. Conventional ready-to-drink tea maintains a dominant market share due to its cost-effectiveness, wider availability, and established consumer acceptance. The segment benefits from economies of scale in production, extensive distribution networks, and competitive pricing structures that appeal to price-sensitive consumer segments. Conventional products utilize standardized ingredients and manufacturing processes, enabling consistent quality delivery across high-volume production runs while maintaining accessible price points for mass market consumption.

Organic is anticipated to be the fastest-growing segment between 2026 and 2033, propelled by heightened consumer awareness regarding pesticide residues, environmental sustainability, and perceived health advantages of organically grown tea leaves. Organic certification requirements, including U.S. Food and Drug Administration (FDA) and European Union (EU) regulatory compliance, ensure ingredient transparency and production integrity, building consumer trust. This segment commands premium pricing, attracting affluent, health-conscious consumers willing to invest in perceived quality and environmental responsibility. Market growth is supported by expanding organic tea cultivation, improved supply chain logistics, and retailer commitments to expanding organic product selections.

Flavor Insights

Fruit flavor is expected to capture about 48% of the RTD tea market share in 2026. Fruit-flavored RTD teas benefit from broad consumer appeal, a naturally refreshing taste profile, and compatibility with multiple base teas, which makes them widely accepted across age groups. They are often viewed as a healthier alternative to traditional soft drinks, particularly when positioned with natural fruit infusions and reduced sugar content, helping to sustain their leadership in both volume and value terms within flavored RTD tea portfolios. In addition, fruit variants provide strong visual and sensory cues, support seasonal and limited-edition launches, and enable brands to tailor products to local taste preferences, further reinforcing their role as the anchor flavor category in the RTD tea segment.

Lemon flavor is predicted to be the fastest-growing segment during the 2026-2033 forecast period. The growth is reflecting its association with refreshment, detoxification, and immune support, as well as its strong presence in new product launches and iced tea formats. Lemon RTD teas align well with low-sugar, clean-label positioning and are frequently combined with herbs or spices such as ginger or mint, which further enhances their appeal among health-conscious consumers seeking functional benefits and bolder taste profiles. Market with strong traditions of spiced hot tea, where brands translate those profiles into RTD formats to capture consumers looking for warming, comforting, and culturally familiar beverages.

Regional Insights

Asia Pacific Ready-to-Drink (RTD) Tea Market Trends

Asia Pacific is likely to account for a commanding 41% of the ready-to-drink tea market share in 2026. The Asia Pacific market is also anticipated to grow the fastest from 2026 to 2033, since it combines rich tea-drinking traditions with rapid modernization and a growing demand for convenient packaged formats. China leads regional production and consumption, supported by extensive tea cultivation, strong domestic brands, and continuous innovation in flavor, packaging, and functional formulations targeted at urban, health-conscious consumers. The market in Japan is characterized by a strong focus on quality, authenticity, and variety, with consumers showing a clear preference for unsweetened green tea, barley tea, and, increasingly, functional RTD teas enriched with ingredients such as collagen, catechins, and probiotics.

India is evolving into a high-growth ready-to-drink tea market as rampant urbanization, rising disposable incomes, and shifting lifestyles among younger consumers drive a gradual transition from traditional hot tea to chilled, flavored RTD formats. Across ASEAN countries, including Indonesia, Thailand, Malaysia, and the Philippines, the expansion of modern retail infrastructure and the rapid emergence of a sizeable middle class are supporting broader RTD tea adoption. The region’s strengths in tea cultivation, cost-efficient manufacturing, and established export-oriented supply chains further reinforce Asia Pacific’s role as the global production hub for RTD tea.

Europe Ready-to-Drink (RTD) Tea Market Trends

The Europe RTD tea market is characterized by steady, structurally driven growth, supported by a mature yet increasingly health-focused consumer base. Germany, the United Kingdom, France, and Spain are the primary consumption centers, with Germany and the U.K. acting as anchor markets where demand is increasingly shaped by organic, herbal, and functional RTD teas rather than purely traditional offerings. Consumers across the region show a strong preference for premium, sustainably sourced products with clean-label credentials, reflecting heightened awareness of environmental impact, ingredient transparency, and overall product quality. This has positioned ready-to-drink tea as a credible alternative to both conventional soft drinks and traditional hot tea formats, particularly among younger and urban populations.

Within Europe, Germany stands out due to strong health and wellness trends, with consumers gravitating toward green and herbal RTD teas that clearly communicate their functional benefits. The U.K. maintains a deep-rooted tea culture while rapidly adopting innovative RTD formats such as cold brew and sparkling teas, particularly in premium segments. France is experiencing growing interest in organic and artisanal RTD tea, with a distinct emphasis on authentic ingredient sourcing and sophisticated flavor profiles. EU food safety regulations and environmental directives impose stringent standards on ingredients, packaging, and sustainability, which in turn encourage innovation in eco-friendly materials, ethical sourcing practices, and carbon-conscious production. Competitive dynamics combine large multinational beverage companies with specialized European tea brands, while investment increasingly focuses on sustainable production facilities and digital commerce capabilities that enable direct consumer engagement.

North America Ready-to-Drink Tea (RTD) Market Trends

North America is a major market for ready-to-drink tea, supported by a well-established iced tea culture, particularly in the United States, where RTD formats are deeply integrated into everyday consumption habits. Demand is increasingly shaped by interest in functional beverages that deliver benefits beyond basic hydration, with consumers gravitating toward green and herbal teas associated with antioxidant, digestive, and relaxation benefits. As a result, RTD tea has secured a strong position as an attractive substitute for carbonated soft drinks and other sugary beverages, especially among health-conscious and younger demographics seeking convenient yet superior options.

Growth across the region is further supported by premiumization, as consumers show a clear willingness to pay more for organic certification, natural ingredients, and distinctive flavor profiles. Leading brands are capitalizing on this by expanding their portfolios with zero-sugar offerings, plant-based or naturally sweetened formulations, and limited-edition flavors tailored to evolving tastes. At the same time, a stronger regulatory focus on transparent labeling and ingredient safety is accelerating clean-label product development, while the innovation ecosystem in major metropolitan areas continues to foster experimentation in both packaging and formulation. This includes a growing emphasis on recyclable or reduced-plastic packaging, aligning RTD tea products with rising environmental awareness among North American consumers.

Competitive Landscape

The global ready-to-drink tea market structure is moderately consolidated, with top players such as The Coca-Cola Company, PepsiCo Inc., Nestlé S.A., and Tata Consumer Products Limited controlling approximately 50-55% of the market share. While these giants dominate mainstream channels, the moderate concentration leaves room for specialty brands to thrive by targeting niches such as organic, premium, or functional teas. Regional competitors defend their positions by leveraging local market expertise, cultural relevance, and the agility to quickly adapt to shifting consumer preferences.

To stand out in this crowded landscape, companies must lay strong emphasis on brand heritage, ingredient quality, health benefits, sustainability, and superior taste. Differentiation increasingly relies on functional enhancements, organic certifications, and transparent sourcing stories that resonate with values-driven shoppers. For challenger brands, success often comes from articulating a clear, authentic narrative that connects product attributes directly to the lifestyle and ethical priorities of their target audience.

Key Industry Developments

- In April 2025, Lipton unveiled two new ready-to-drink Fusion flavors, Strawberry Lemonade with Iced Tea and Pineapple Mango Lemonade with Iced Tea, sold in 16-ounce cans for around US$ 1 at major retailers.

- In April 2025, AriZona introduced AriZona Hard with Vodka, blending cold-brewed tea with vodka in four tea flavors, while other alcohol brands such as NÜTRL and Captain Morgan roll out new strawberry seltzers and sweet-vs-spicy RTD packs to tap flavor trends.

- In March 2025, Luxmi Tea Estates launched “Makaibari Zero Proof,” a premium line of organic, tea-based concentrates made from high-altitude Darjeeling tea and whole herbs/spices such as ginger, turmeric, Tulsi, and mint, designed to be mixed with soda, wine, or spirits as sophisticated non-alcoholic or cocktail bases.

Companies Covered in Ready-to-Drink (RTD) Tea Market

- The Coca-Cola Company

- PepsiCo Inc.

- Unilever

- Nestlé S.A.

- Suntory Holdings Limited

- Arizona Beverage Company

- ITO EN Ltd.

- Tata Consumer Products Limited

- Asahi Group Holdings Ltd.

- Keurig Dr Pepper Inc.

- Tingyi (Cayman Islands) Holding Corporation

- Danone S.A.

- Uni-President Enterprises Corp.

- Starbucks Corporation

- Pokka Corporation

Frequently Asked Questions

The global ready-to-drink tea (RTD) market is projected to reach US$ 42.4 billion in 2026.

The market is driven by rising health consciousness, demand for convenient on-the-go beverages, and continuous flavor and functional product innovation.

The market is poised to witness a CAGR of 5.7% from 2026 to 2033.

Key market opportunities lie in functional and organic RTD teas and sustainability-focused packaging and clean-label product development.

The Coca-Cola Company, PepsiCo Inc., Nestlé S.A., and Tata Consumer Products Limited are some of the key players in the market.