- Beverages

- Tea Market

Tea Market Size, Share, Growth, and Regional Forecast, 2025 to 2032

Tea Market By Type (Black Tea, Green Tea, Oolong Tea, Herbal Tea, Others), Distribution Channel (Hypermarkets & Supermarkets, Convenience Stores, Retail Stores, Online Stores), and Regional Analysis from 2025 to 2032

Tea Market Size and Trends Analysis

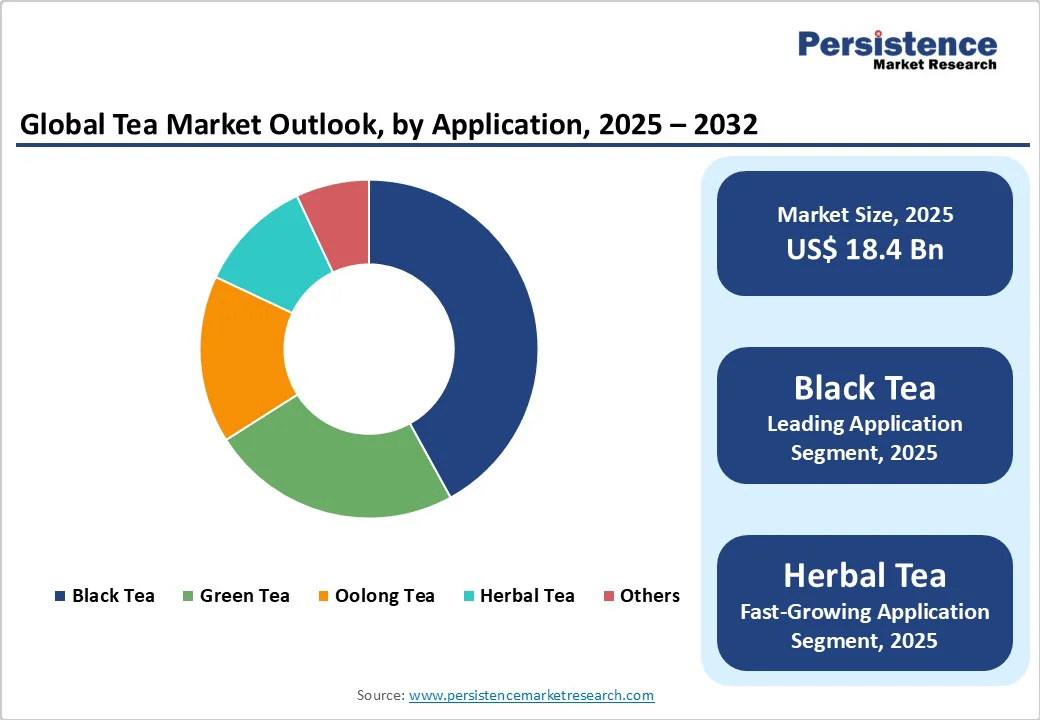

The global tea market size is likely to be valued at US$18.4 billion in 2025. It is expected to reach US$28.0 billion by 2032, growing at a CAGR of 6.2% during the forecast period from 2025 to 2032, driven by evolving consumer preferences and technological innovations in the processing, flavoring, and packaging of tea.

Key Industry Highlights

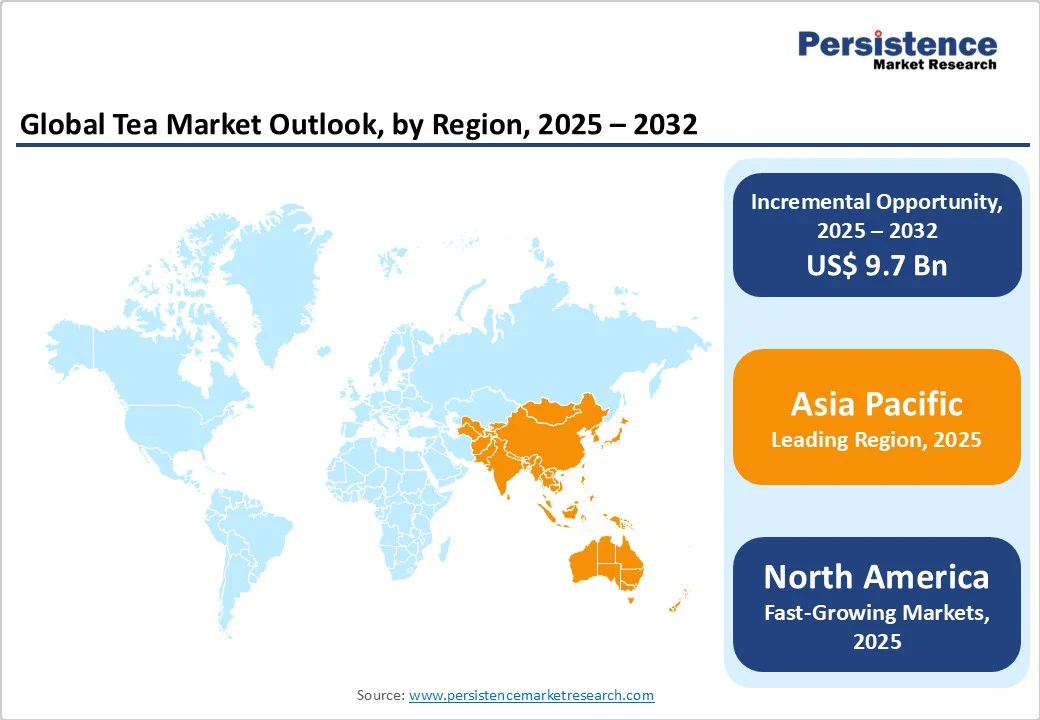

- Leading Region: The Asia Pacific dominates the market, driven by high domestic consumption, a well-established tea culture, and large-scale production.

- Fastest-Growing Type: Herbal and functional teas, due to increasing health awareness and demand for wellness-oriented beverages.

- Market Drivers: Rising health consciousness, expanding ready-to-drink (RTD) tea formats, and growing preference for premium and flavored teas.

- Investments: Expansion of organized retail and e-commerce platforms, sustainability initiatives by tea producers, and innovations in packaging, flavors, and experiential retail channels.

| Key Insights | Details |

|---|---|

| Tea Market Size (2025E) | US$18.4 Bn |

| Market Value Forecast (2032F) | US$28.0 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Health Trends, Premium & RTD Teas, and Urbanization

The tea market is driven by rising health awareness among consumers, which has significantly boosted demand for teas with functional benefits, such as green, herbal, and antioxidant-rich varieties, which are associated with improved immunity, digestion, and overall wellness.

Increasing disposable incomes, particularly in emerging economies, have encouraged consumers to explore premium, specialty, and flavored teas, creating opportunities for brand differentiation and value-added offerings. Urbanization and fast-paced lifestyles are also fueling demand for convenient tea formats, including ready-to-drink (RTD) teas, tea bags, and instant brews, which allow consumers to enjoy tea without the need for lengthy preparation.

The expansion of organized retail and e-commerce platforms has enhanced accessibility and availability, making tea products more accessible across diverse regions. Additionally, cultural and traditional consumption patterns, especially in countries such as China, India, and Japan, continue to sustain long-term demand. Promotional campaigns, seasonal launches, and innovations in flavors and packaging further encourage trial and repeat purchases, thereby reinforcing the overall growth momentum of the global tea market.

Competition from Alternative Beverages and Climate Change

Tea faces increasing competition from alternative beverages and challenges from climate change, which affects production. In several major markets, coffee remains the leading beverage, accounting for nearly 60% of hot beverage consumption in North America and parts of Europe.

Younger consumers are also turning to energy drinks and functional beverages, which has limited tea’s appeal among the 15-35 age group. Ready-to-drink (RTD) teas and other convenient beverage formats are gaining traction, offering ease of consumption that traditional loose-leaf and bagged teas cannot always provide.

Tea cultivation is being impacted by climate variability. Key producing regions are experiencing unpredictable monsoons, temperature fluctuations, and other adverse weather conditions. These supply constraints have caused price volatility. Such increases may slow demand growth in markets where consumers are price-sensitive, posing challenges to the overall expansion of the global tea industry.

Premium, Artisanal, and Sustainable Products Drive Growth Opportunities

Single-origin teas and craft-blended varieties are increasingly attracting consumers willing to pay higher prices for unique flavors and superior quality, creating potential for higher profit margins. There is also a growing demand for eco-friendly and sustainably sourced products, as environmentally conscious consumers prefer teas that are certified and sourced ethically.

E-commerce and experiential retail channels are expanding rapidly, providing brands with direct access to consumers and the ability to create engaging experiences through tea lounges, tasting rooms, and interactive events.

Asia Pacific, Africa, and Latin America offer untapped potential, driven by rising disposable incomes, urbanization, and growing awareness of tea’s health benefits. Innovations in flavors, blends, and packaging, coupled with the demand for convenient, ready-to-drink formats that combine wellness and taste, enable brands to differentiate themselves and expand their market presence globally.

Category-wise Analysis

Type Insights

Black tea continues to hold the largest share of the tea market, accounting for nearly 42% of total consumption. Its dominance stems from deep-rooted cultural traditions and widespread popularity across Asia, the U.K., and African nations, where tea drinking remains an integral part of daily life.

Classic blends such as Earl Grey, Darjeeling, Assam, and English Breakfast continue to command strong consumer loyalty in mature markets, while innovative spiced versions such as masala chai are driving fresh growth in emerging economies.

The adaptability of black tea, whether served hot, iced, or infused with milk and flavors, adds to its global appeal. Its rich aroma, strong taste, and relatively higher caffeine content make it a preferred alternative to coffee. Despite rising interest in green, herbal, and specialty teas, black tea maintains its market leadership through tradition, versatility, and consistent demand across both household and foodservice sectors worldwide.

The herbal tea segment is projected to grow fastest, driven by rising health awareness and demand for natural, caffeine-free beverages. Popular varieties such as chamomile, peppermint, and ginger are valued for their therapeutic benefits. Expanding specialty tea outlets and wellness trends further boost herbal tea’s global market growth and consumer preference.

Distribution Channel Insights

Hypermarkets and supermarkets are the leading channels for tea sales worldwide, holding around 44% of the total market share in 2025. Their popularity comes from offering a wide range of tea products from regular black tea to premium, organic, and flavored varieties, at affordable prices

These large retail stores give consumers convenient access to different brands in one place, making shopping easier and more enjoyable. The rapid growth of organized retail, especially in emerging economies such as India, with thousands of supermarket outlets, continues to strengthen this channel.

Supermarkets also work closely with tea producers to maintain steady product availability and quality, supported by efficient supply chains. Attractive shelf displays, eye-catching packaging, and seasonal promotions such as discounts or combo deals help boost sales and brand visibility.

With their strong presence, variety, and promotional activities, supermarkets and hypermarkets remain the most influential and trusted platforms for tea distribution, shaping global buying patterns and consumer preferences.

Regional Insights

Asia Pacific Tea Market Trends

The Asia Pacific tea market continues to dominate global production and consumption, supported by deep-rooted cultural preferences and the growing modernization of tea consumption.

China remains the largest tea producer and consumer, with demand shifting toward premium segments such as high-quality green tea and oolong, reflecting rising health awareness and a preference for authenticity. India ranks second in consumption, driven by its traditional chai culture and the expansion of modern tea cafés catering to younger urban consumers.

Across ASEAN countries, rising incomes, rapid urbanization, and lifestyle changes are fueling demand for both traditional and specialty teas. Thailand and Vietnam are emerging as major tea processing and export hubs, benefiting from competitive manufacturing costs and enhanced quality standards. The region’s overall trend shows a shift toward premiumization, convenience formats, and export-oriented growth, positioning Asia-Pacific as the most dynamic and influential region in the global tea industry.

North America Tea Market Trends

The North American tea market is witnessing steady expansion, driven by a growing preference for premium and health-oriented tea varieties. Consumers in the U.S. are increasingly shifting toward green and herbal teas as healthier alternatives to coffee, supported by the FDA’s regulatory support for antioxidant-related health claims.

Innovation centers in states such as California and New York are leading advancements in cold-brew tea formulations, ready-to-drink options, and eco-friendly packaging, fueling product diversification and premiumization. E-commerce has become a major growth channel, with subscription-based and direct-to-consumer models gaining popularity.

Retail giants are expanding organic and sustainably sourced tea flavors to align with consumer demand for clean-label products. The market also benefits from the growing consumer interest in specialty blends and craft teas, positioning North America as an evolving landscape where wellness, convenience, and sustainability drive future growth.

Competitive Landscape

The global tea market exhibits moderate fragmentation, with leading players holding approximately 35% combined market share. Companies pursue diversification strategies through organic tea acquisitions, premium brand development, and geographic expansion into emerging markets.

Key differentiators include sustainable sourcing programs, innovative packaging solutions, and direct-to-consumer digital platforms. Emerging business models focus on subscription services, experiential retail concepts, and blockchain-enabled supply chain transparency to build consumer trust and loyalty.

Key Industry Developments

- In September 2025, Bigelow Tea, a leading family-owned tea company in the United States, introduced two new limited-edition seasonal flavors, Simply Cinnamon Apple Herbal Tea and Sweet Cinnamon Dolce Black Tea, expanding its range of festive, aromatic blends for the upcoming season.

- In February 2025, Tata Tea Premium introduced ‘Premium Care’, a new tea blend crafted with natural ingredients for enhanced wellness and flavor.

- In September 2024, Tata Tea Gold introduced a special limited-edition Kumartuli-themed packaging in honor of the Durga Puja festival. The packs highlight five traditional cultural symbols: Dhunuchi dance, Shankho Dhwani, Dhaki, Ashtami Pujarin, and Sindoor Khela.

Companies Covered in Tea Market

- Starbucks Corporation

- Wissotzky Tea

- Nestle S.A.

- Associated British Foods

- Tata Global Beverages

- R. Twining and Company Limited

- Dilmah Ceylon Tea Company PLC.

- Bigelow Tea

- PepsiCo

- YORKSHIRE TEA

- Caraway Tea

- The Republic of Tea

Frequently Asked Questions

The market is projected to be valued at US$18.4 Billion in 2025.

Rising health consciousness, increasing demand for specialty teas, and expanding global consumption drive growth.

The tea market is poised to witness a CAGR of 6.2% between 2025 and 2032.

Innovation in flavored teas, ready-to-drink variants, organic products, and emerging markets offer significant expansion opportunities.

Top companies operating in the tea market include Associated British Foods, Wissotzky Tea, Unilever, Starbucks Corporation, Nestlé S.A., and Tata Global Beverages (Tata Tea Ltd.).