- Processed Food

- Sugar Free Candy Market

Sugar Free Candy Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Sugar Free Candy Market is segmented by Product Type (Hard Candies, Soft Candies/Gummies, Lollipops, Caramels & Toffees, and Others), by Flavor (Fruit, Coffee, Caramel, Butterscotch, and Others), by Sales Channel (Supermarkets/Hypermarkets, Convenience stores, Drug Stores & Pharmacies, Specialty Stores, Online retail, and Others), and by Regional Analysis, 2026 - 2033

Sugar Free Candy Market Share and Trends Analysis

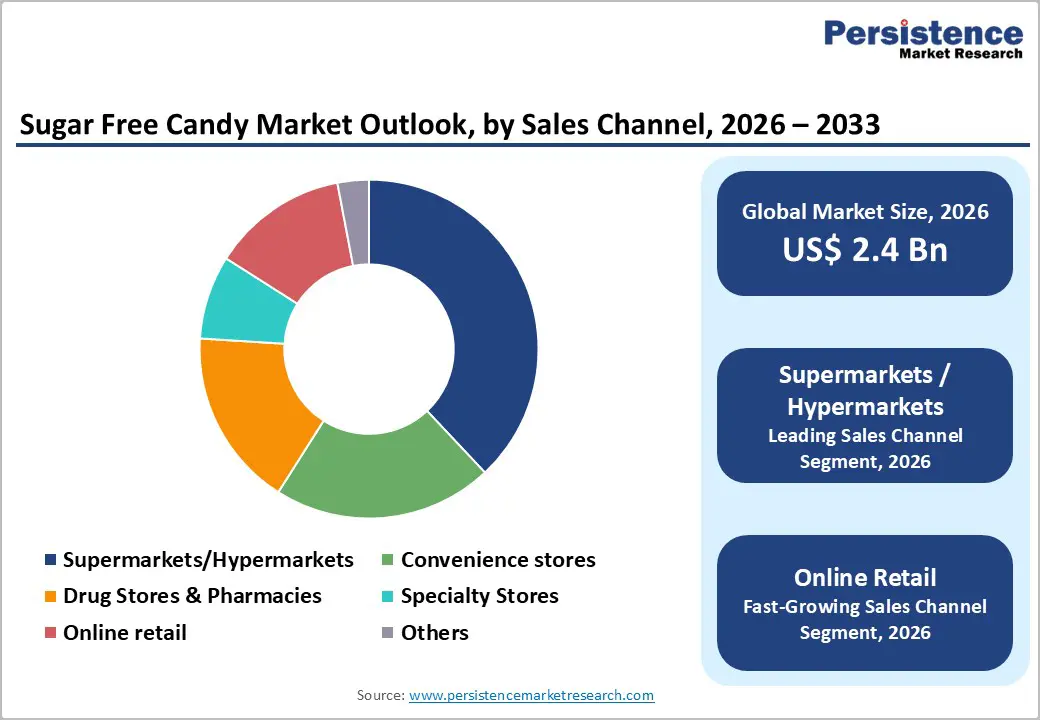

The global sugar-free candy market size is expected to be valued at US$ 2.4 billion in 2026 and projected to reach US$ 3.7 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

The market is predominantly driven by a structural shift in consumer behavior toward preventive healthcare and the escalating global prevalence of lifestyle-related disorders such as diabetes and obesity. The integration of advanced natural sweeteners like Stevia and Monk Fruit has bridged the sensory gap, allowing brands to offer indulgent experiences without the associated glycemic impact, thereby fostering robust market growth through the forecast period.

Key Industry Highlights:

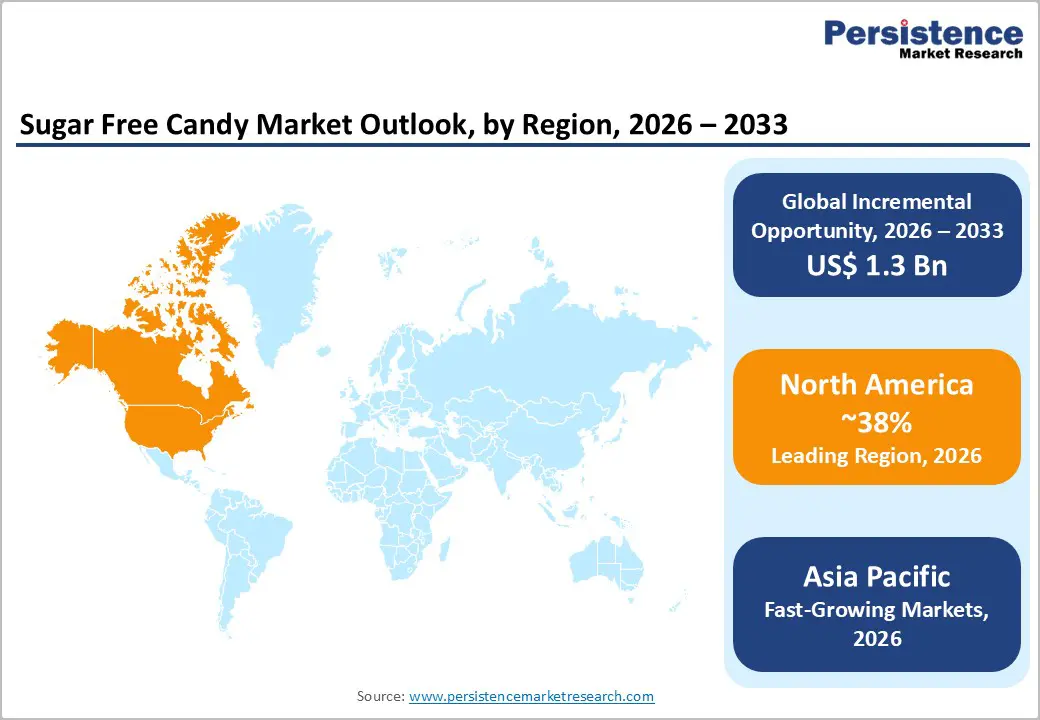

- Leading Region: North America dominated the market in 2025 with a 38% share, supported by a mature health-wellness ecosystem and a high prevalence of metabolic disorders.

- Fastest Growing Region: Asia Pacific is the fastest-growing region through 2033, fueled by rapid urbanization and the world's highest diabetes growth rates in China and India.

- Dominant Segment: Supermarkets / Hypermarkets held a 39% distribution share in 2025, as dedicated better-for-you aisles drive mass-market product visibility.

- Fastest Growing Segment: Online Retail is the fastest growing distribution channel, as e-commerce allows consumers to access a wider variety of niche and functional sugar-free products.

- Key Market Opportunity: The Functional Fortification of sugar-free candies with vitamins and adaptogens represents a significant growth pocket for targeting wellness-focused consumers.

| Key Insights | Details |

|---|---|

|

Sugar Free Candy Market Size (2026E) |

US$ 2.4 Bn |

|

Market Value Forecast (2033F) |

US$ 3.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.6% |

Market Dynamics

Driver - Rising Health Consciousness and Lifestyle Disease Management

The primary catalyst for the sugar-free candy market is the heightened global awareness of the metabolic consequences of excessive sucrose intake. Consumer sentiment has shifted toward better-for-you snacks, driven by public health campaigns from organizations such as the World Health Organization (WHO), which recommends keeping added sugar below 10% of total energy intake. In 2025, the American Heart Association emphasized the link between high-sugar diets and cardiovascular risks, prompting a massive transition toward non-nutritive sweeteners. This health-centric demand is particularly strong among Millennials and Gen Z, who actively seek low-calorie indulgences that align with weight-management goals and fitness-oriented lifestyles.

Restraints - High Production Costs and Supply Chain Volatility

A significant barrier to the widespread adoption of sugar-free confectionery is the premium cost associated with alternative sweeteners and specialized manufacturing processes. Natural sweeteners such as Monk Fruit and high-purity Xylitol are considerably more expensive than traditional beet or cane sugar, often increasing raw material costs by 20% to 35%. Furthermore, sugar-free formulations often require separate production lines to prevent cross-contamination and manage the varying melting points of sugar alcohols. This complexity results in a retail price premium that can alienate price-sensitive consumers in emerging markets. Furthermore, supply chain disruptions for rare plant-based sweeteners can lead to significant price spikes, creating financial pressure for smaller artisanal brands.

Opportunity - Exponential Growth in Online Retail and D2C Channels

The digital transformation of the retail sector offers a significant avenue for brand expansion, particularly for niche and premium sugar-free offerings. Online retail is projected to be the fastest-growing distribution channel through 2032, driven by the high penetration of e-commerce and the ease of comparing nutritional profiles. Direct-to-consumer (DTC) models enable brands to collect first-party data, supporting personalized marketing and subscription services that drive consumer retention. In 2025, social media platforms such as Instagram and TikTok became central to the discovery of viral sugar-free products, with influencer-led campaigns significantly lowering customer acquisition costs. This channel is particularly vital for artisanal brands such as Zolli Candy and Russell Stover to reach a global audience without the traditional barriers of physical shelf-space competition.

Category-wise Analysis

Product Type Insights

Soft candies/gummies segment emerged as a dominant force, favored for its versatility and the ability to incorporate complex flavor profiles. This segment is bolstered by the rise of Keto-friendly gummies that use Pectin instead of gelatin to appeal to vegan demographics. Hard Candies also maintain a significant share, particularly in the throat-soothing and breath-freshening sub-categories, where sugar-free status is often a prerequisite. However, the Caramels & Toffees segment is witnessing rapid innovation as manufacturers overcome the technical hurdles of replicating the creamy texture of dairy and sugar without traditional caramelization processes, appealing to older demographics seeking nostalgic treats.

Sales Channel Insights

Supermarkets/hypermarkets currently lead the distribution landscape, holding a 39% market share in 2025. These retailers provide the high-visibility shelf space and dedicated health aisles necessary for mass-market product discovery. Large-scale chains like Walmart and Kroger have significantly expanded their private-label sugar-free offerings to compete with major brands. Conversely, Online Retail is the fastest-growing channel. The convenience of bulk purchasing and the availability of specialized niche products such as THC/CBD-infused sugar-free candies have made e-commerce the preferred route for health-aware consumers who require specific dietary certifications like Non-GMO, Organic, or Gluten-Free.

Region-wise Insights

North America Sugar Free Candy Market Trends and Insights

North America is the dominant regional market, accounting for 38% of the market in 2025. The United States leads this demand, driven by a mature retail infrastructure and the high prevalence of obesity and Type 2 diabetes. According to the Centers for Disease Control and Prevention (CDC), over 38 million adult Americans have diabetes, creating a massive inherent demand for sugar-controlled treats. The regional market is also characterized by a high level of product innovation; in October 2024, Mars Wrigley unveiled new format innovations at the NACS Show, focusing on variety and novel textures for the convenience channel.

Regulatory frameworks in the U.S., particularly the FDA's mandatory nutrition labeling, have required a high degree of transparency that benefits the sugar-free sector. The Better-For-You (BFY) movement is a structural pivot in the region, where consumers seek permission to indulge without compromising their health goals. Additionally, the presence of major players like The Hershey Company and Mondelez International, who are aggressively reformulating their core product lines, ensures that North America remains at the forefront of global sugar-free confectionery trends.

Asia Pacific Sugar-Free Candy Market Trends and Insights

The Asia-Pacific region is the fastest-growing market globally, projected to grow at a significant CAGR through 2032. This growth is driven by rapid urbanization, rising middle-class disposable incomes, and growing health awareness in China and India. According to the International Diabetes Federation, Southeast Asia has some of the highest diabetes rates in the world, making sugar-free options a medical necessity for millions. The region is seeing a surge in localization strategies, with brands launching traditional flavors such as Matcha or Spiced Mango in sugar-free formats.

Manufacturing advantages in the region, particularly in China, enable cost-effective production of natural sweeteners such as Stevia and Monk Fruit at scale. In India, the expansion of organized retail and the rise of wellness-focused e-commerce platforms are making sugar-free candies accessible beyond tier-1 cities. The Asia Pacific market is also a hub for functional innovation, with many local brands incorporating traditional Ayurvedic or herbal ingredients into sugar-free gummies to appeal to the holistic health preferences of the regional consumer base.

Competitive Landscape

The sugar free candy market is a moderately consolidated landscape, with top-tier multinational conglomerates such as The Hershey Company, Mars Wrigley, and Mondelez International holding a significant portion of the global share. These giants utilize their extensive R&D budgets to continuously improve the taste and texture of their zero-sugar offerings, often acquiring successful niche startups to diversify their portfolios. However, the market remains dynamic with the presence of specialized players like Zolli Candy and Russell Stover, who have built deep brand loyalty through targeted wellness-focused branding.

Key differentiators in the current market include the use of proprietary sweetener blends, functional fortification, and eco-friendly packaging. Emerging business models are increasingly focused on the omnichannel experience, ensuring that premium sugar-free products are available in high-end specialty stores and via direct-to-consumer digital platforms. Research and development are focused on using Artificial Intelligence (AI) to predict consumer flavor preferences and optimize the molecular structures of natural sweeteners to improve sensory performance.

Key Developments:

- In May 2025, Ferrero’s Tic Tac introduced Tic Tac Two, a sugar-free, dual-flavour format that combines two complementary tastes in one mint, targeting younger consumers seeking playful sensory experiences and on-the-go novelty.

- In May 2025, Perfetti Van Melle USA expanded its flavor-led gum strategy with the launch of Trident Vibes Cotton Candy, shipping nationwide to U.S. retailers and tapping into nostalgia-driven, bold flavor experimentation in the sugar-free gum segment.

Companies Covered in Sugar Free Candy Market

- The Hershey Company

- Mondelez International

- Mars Wrigley

- Ferrero

- Lindt & Sprüngli AG

- Perfetti Van Melle

- Cloetta AB

- Zolli Candy

- Russell Stover

- Laymon Candy Company

- See's Candies

- Others

Frequently Asked Questions

The global sugar free candy market is projected to be valued at US$ 2.4 Bn in 2026.

Rising Health Consciousness and Lifestyle Disease Management is driving demand for Sugar Free Candy market.

The Global Sugar Free Candy market is poised to witness a CAGR of 6.2% between 2026 and 2033.

Exponential Growth in Online Retail and D2C Channels is key opportunity for key players in the market.

The sugar free candy market is led by global players such as The Hershey Company, Mondelez International, Mars Wrigley, Ferrero, Lindt & Sprüngli AG, Perfetti Van Melle and Others.