- Processed Food

- Industrial Brown Sugar Market

Industrial Brown Sugar Market Size, Share, and Growth Forecast, 2025 - 2032

Industrial Brown Sugar Market By Product Type (Light Brown Sugar, Dark Brown Sugar), Form (Granulated / Crystal, Liquid Syrup), Application, and Regional Analysis for 2025 - 2032

Industrial Brown Sugar Market Size and Trends Analysis

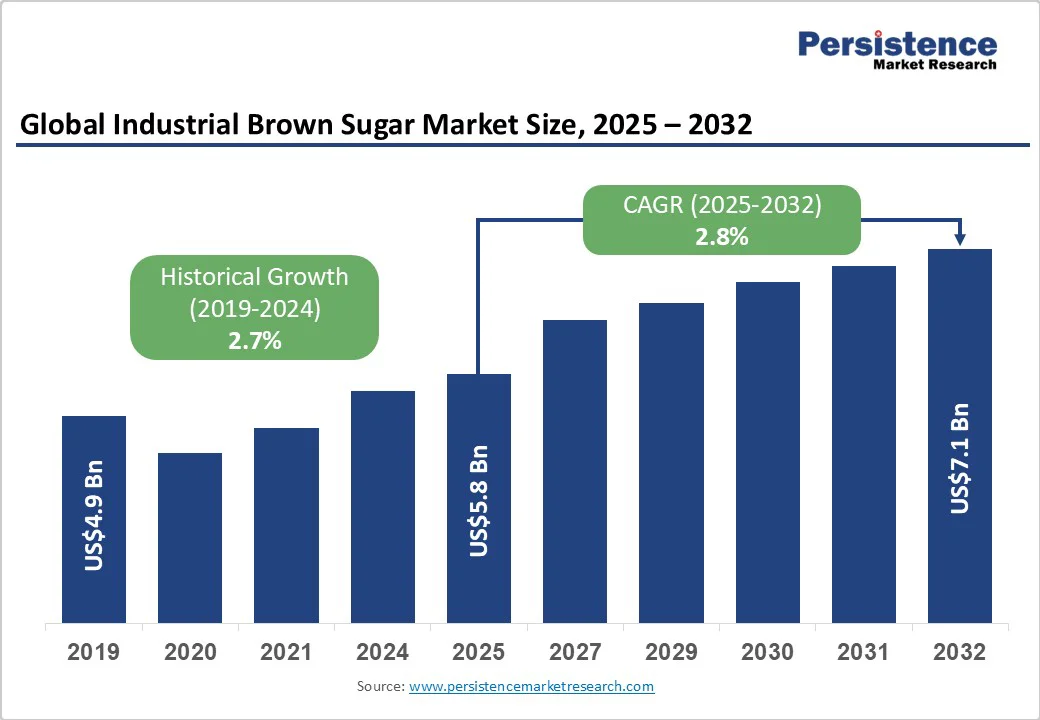

The global industrial brown sugar market is expected to reach US$5.8 billion in 2025. It is expected to reach US$7.1 billion by 2032, growing at a CAGR of 2.8% during the forecast period from 2025 to 2032, driven by rising consumption in the bakery, confectionery, and beverage manufacturing sectors.

Growth in the processed food industry, the increasing use of molasses-rich sugar for natural flavor enhancement, and the broader adoption of clean-label sweeteners are propelling the market forward.

Key Industry Highlights

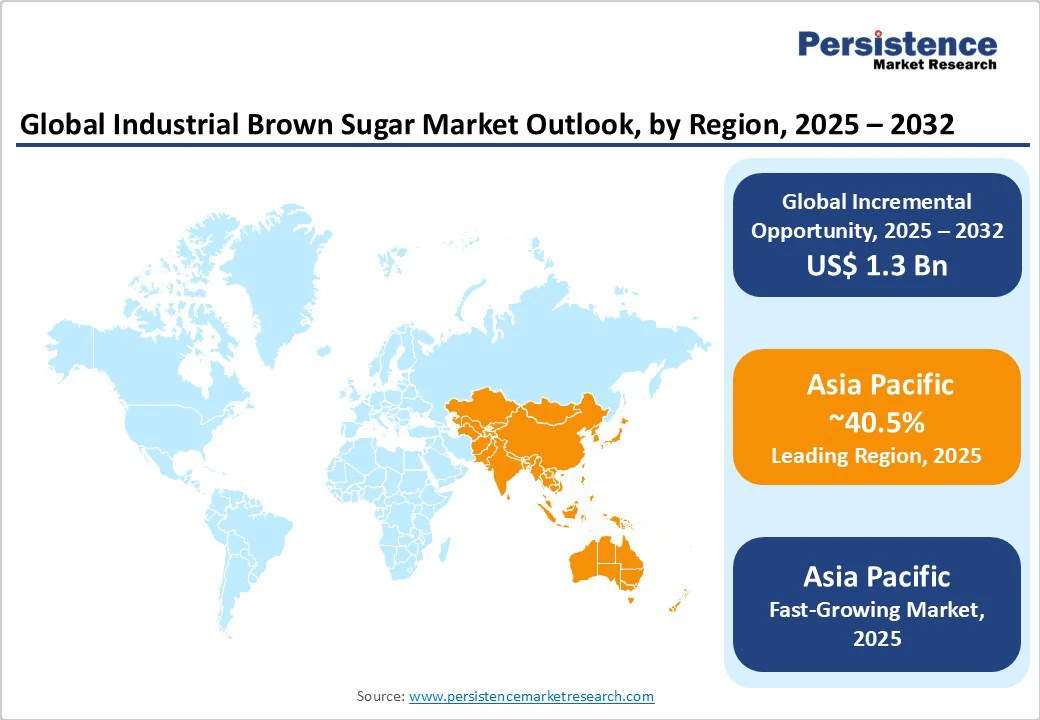

- Leading Region: Asia Pacific, accounting for approximately 40.5% of the global industrial brown sugar demand in 2025, driven by extensive sugarcane cultivation, low production costs, and large-scale food processing.

- Fastest-growing Region: Asia Pacific, fueled by expanding bakery, beverage, and industrial fermentation applications.

- Investment Plans: Major refiners in Asia Pacific and North America are investing in modernization and sustainability, including automation, energy-efficient refining, and traceable packaging, with capital outlays exceeding US$150 million collectively (Mitr Phol, ASR Group).

- Dominant Product Type: Light brown sugar, accounting for 59% of industrial sales by value, preferred for bakery, confectionery, and beverage applications due to balanced sweetness and stable molasses content.

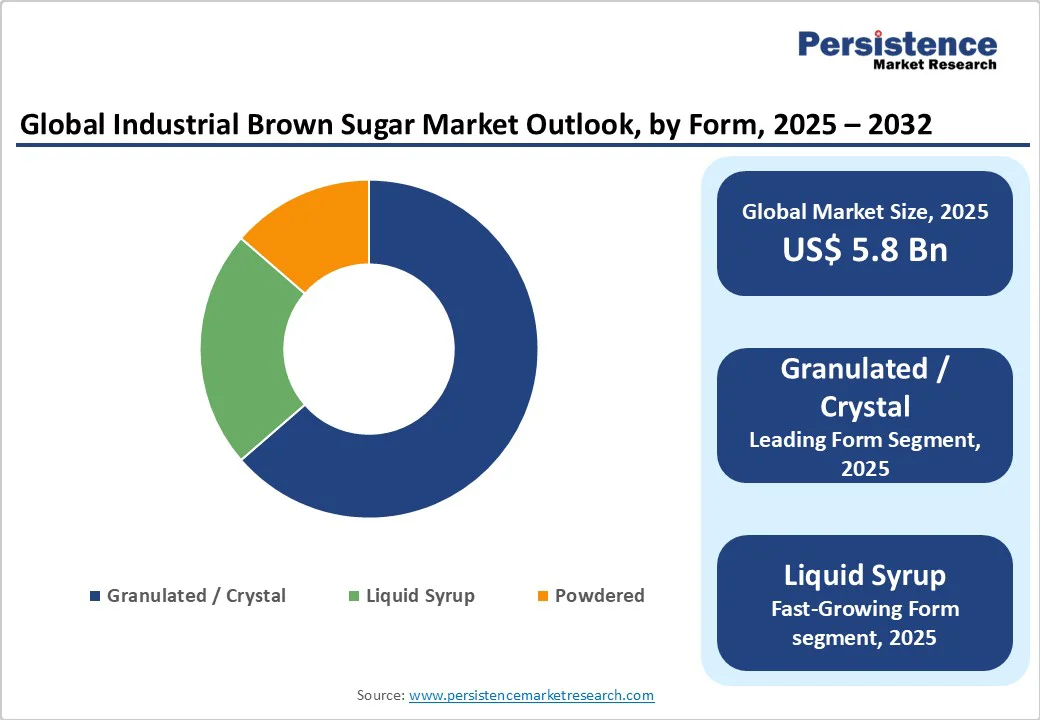

- Leading Form: Granulated/crystal brown sugar, comprising 68% of industrial consumption, favored for automated processing, uniform solubility, and bulk handling efficiency.

| Key Insights | Details |

|---|---|

|

Industrial Brown Sugar Market Size (2025E) |

US$5.8 Bn |

|

Market Value Forecast (2032F) |

US$7.1 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

2.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

2.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Growing Industrial Food Processing and Bakery Demand

The expansion of industrial bakeries, confectionery plants, and beverage manufacturers has significantly increased the consumption of brown sugar as a natural colorant and flavoring agent. The bakery segment alone accounts for a substantial share of industrial usage, with consistent demand for granulated brown sugar in biscuits, cakes, and desserts. Rising consumption of convenience foods and packaged bakery products across the Asia Pacific and Latin America has further stimulated industrial procurement. Large food companies are now entering multi-year supply contracts with refiners to ensure quality consistency and price stability, ensuring sustained market growth.

Rising Preference for Clean-Label and Natural Ingredients

Food manufacturers are increasingly reformulating products using less-processed sweeteners to align with consumer preferences for natural and authentic ingredients. Industrial brown sugar, which retains some of its molasses content, offers a richer flavor and a natural profile attractive to bakery and dairy processors. This trend has encouraged refiners to invest in traceable, certified, and sustainably produced brown sugar grades. Premium organic and fair-trade variants have started gaining share, enabling producers to achieve price premiums of up to 30% over conventional refined sugar and boosting profitability in mature markets.

Growing Use of Brown Sugar as a Feedstock for Industrial Fermentation

Brown sugar serves as a cost-effective carbohydrate source for fermentation-based production of ethanol, organic acids, and enzymes. Countries such as India and Brazil, where ethanol-blending mandates are expanding, have seen rising diversion of sugar toward industrial uses. This trend links sugar markets with biofuel policies, influencing global supply and pricing. As fermentation industries scale up, refiners that establish long-term supply contracts with bio-chemical manufacturers stand to benefit from stable, high-volume demand even during periods of soft consumer consumption.

Barrier Analysis - Stringent Sugar-Reduction Policies and Taxation

Regulatory initiatives to curb sugar intake, such as sugar-sweetened beverage taxes and mandatory labeling rules, have moderated consumption growth in key markets. Countries including the U.K., Mexico, and the Philippines have recorded reduced sales of sugary products following the introduction of these measures. Industrial beverage manufacturers are reformulating recipes to lower sugar content, which indirectly reduces demand for brown sugar. Although reformulation creates opportunities for alternative sweeteners, it remains a limiting factor for traditional brown sugar volumes.

Supply Volatility Driven By Weather and Policy Fluctuations

The sugar industry is highly exposed to climatic variations that affect cane and beet yields, as well as policy changes that influence export availability. Drought conditions, excessive rainfall, or pest outbreaks can reduce output and trigger price spikes. In parallel, government policies promoting ethanol blending often divert sugarcane toward fuel production, creating shortages in industrial sugar supply. These structural uncertainties raise procurement risks for manufacturers and may lead to higher input costs or temporary supply constraints.

Opportunity Analysis - Expansion of Premium, Certified, and Traceable Brown Sugar

Demand for certified organic, fair-trade, and sustainably sourced brown sugar is increasing across developed markets. Manufacturers seeking differentiation are adopting traceability programs and investing in cleaner production lines that minimize environmental impact. If premium-grade brown sugar captures even 10% of total industrial volume by 2030, the incremental revenue potential could exceed several hundred million dollars globally. This opportunity favors refiners that modernize operations and align with environmental, social, and governance (ESG) standards demanded by multinational food brands.

Rising Industrial Applications in Bio-Based Chemicals

The global transition toward renewable raw materials has spurred demand for sugar-derived feedstocks in biochemical and bioplastic production. Industrial brown sugar provides an accessible carbohydrate source for producing lactic acid, citric acid, and other intermediates used in sustainable materials. As industrial biotechnology continues to expand, partnerships between sugar refiners and fermentation companies can ensure predictable supply chains. Capturing even a small share of this market can deliver long-term growth and diversify revenue streams beyond traditional food manufacturing.

Category-wise Analysis

Product Type Insights

Light brown sugar continues to dominate the industrial landscape with a market share of 59% due to its balanced flavor, moderate molasses content (typically 3–4%), and wide applicability in bakery and confectionery formulations. Its ability to provide color, texture, and caramelized flavor without overwhelming sweetness makes it ideal for mass-produced items such as cookies, muffins, breakfast cereals, and ready-to-eat desserts. Major food manufacturers such as Mondel?z International, Kellogg’s, and Nestlé incorporate light brown sugar in biscuits and breakfast bars to maintain product consistency and natural taste. The grade’s granular structure also ensures smooth blending with fats and flours in large-scale automated lines.

Raw or partially refined brown sugar is the fastest-growing segment, driven by demand in the ethanol, biochemical, and fermentation industries. Retaining 8–10% molasses, it offers superior fermentability for producing bioethanol, citric acid, and lactic acid, key to renewable energy and bioplastics. Expanding ethanol programs in India, Brazil, and Thailand, such as India’s E20 initiative, boost industrial use. The cosmetics and pharmaceutical sectors are adopting raw brown sugar for its natural humectant and exfoliating properties.

Form Insights

Granulated brown sugar represents the most widely used industrial form with a market share of 69%, characterized by free-flowing crystals that simplify handling, storage, and dosing in automated production lines. The format’s low moisture and uniform grain size make it suitable for bakery mixes, sauces, spice blends, and confectionery coatings. Large bakery chains such as Grupo Bimbo, Hostess Brands, and Britannia Industries favor granulated sugar for its consistent solubility and ease of incorporation into doughs and batters. It also ensures homogeneous color distribution in caramelized products and reduces the risk of clumping during long-term storage. Industrial suppliers often offer granulated brown sugar in bulk 25- to 50-kilogram bags or intermediate bulk containers (IBCs), facilitating efficient supply to food processors worldwide.

Liquid brown sugar syrup is the fastest-growing form in industrial use, driven by demand from beverage, dairy, and RTD manufacturers. Its easy dissolution and consistency enhance production efficiency and hygiene. Companies such as Coca-Cola, PepsiCo, and Danone favor syrups for automated dosing and reduced waste. Customizable viscosity, color, and molasses content make them ideal for caramel sauces, flavored yogurts, and coffee concentrates.

Regional Insights

Asia Pacific Industrial Brown Sugar Market Trends- Dominance Driven by Sugarcane Cultivation and F&B Growth

Asia Pacific commands the largest share of the market, accounting for roughly 40.5% of global demand in 2025, and is projected to be the fastest-growing regional market through 2032. The region’s leadership is rooted in vast sugarcane cultivation, abundant labor, and low refining costs, supported by a rapidly expanding food and beverage manufacturing base. China and India are both major producers and consumers, together accounting for over 55% of regional production, while Thailand, Indonesia, and Vietnam are leading exporters of industrial-grade brown sugar.

Industrial demand is rising with urbanization, the growth of packaged foods, and the expansion of bakery and beverage chains such as Haidilao, BreadTalk, and Britannia. India’s ethanol blending target of 20% by 2025 has shifted sugar use toward fuel, but strong bakery and dairy growth continues to sustain domestic consumption.

In 2024, Mitr Phol Group (Thailand) announced a US$150 million investment to modernize its Khon Kaen refinery and to integrate solar-powered crystallization systems, aiming to reduce operational emissions by 30%. Wilmar International in China has expanded its refining capacity in Guangdong, enhancing production of liquid brown sugar syrups for beverage applications. EID Parry (India) launched a premium-grade industrial brown sugar line in 2025, targeting confectionery manufacturers, and incorporated eco-friendly packaging and traceable sourcing.

North America Industrial Brown Sugar Market Trends - Mature Market Backed by Policy and Refining Infrastructure

North America remains one of the most mature and structurally stable industrial brown sugar markets, underpinned by extensive refining capacity and a highly diversified downstream food-processing ecosystem. The United States leads regional demand, accounting for nearly 75% of total consumption, followed by Canada and Mexico. Industrial brown sugar is primarily used in bakery, confectionery, beverage, and dairy sectors, where product consistency, purity, and traceability are critical.

The U.S. Department of Agriculture’s (USDA) tariff-rate quotas (TRQs) and the U.S.-Mexico Suspension Agreements regulate imports and stabilize domestic prices. These frameworks protect U.S. beet growers while maintaining access to affordable sugar inputs for industrial users. Market concentration is moderate, dominated by key players such as American Sugar Refining (ASR Group), Domino Foods Inc., Cargill Inc., and Imperial Sugar, which together hold over 55% of regional refining capacity.

Recent investments reflect a shift toward operational efficiency and sustainability. In March 2024, ASR Group announced a US$120 million modernization program across its Louisiana and Florida refineries to upgrade energy-efficient boilers and automated packaging systems. Similarly, Cargill expanded its Minnesota facility in September 2023 to increase brown sugar output for industrial applications, integrating AI-enabled quality control systems.

Europe Industrial Brown Sugar Market Trends - Sustainability and Specialty Sugars Reshape Industrial Use

Europe’s industrial brown sugar market is driven by advanced refining, strong cooperative ownership, and robust export channels. Germany, France, and the U.K. contribute over 65% of regional production, mainly from beet sugar. Leading cooperatives such as Südzucker AG, Nordzucker AG, and Tereos Group operate vertically integrated networks across the EU. Industrial brown sugar is widely used in bakery, chocolate, beverages, and alcoholic fermentation, with exports to the Middle East & Africa.

Growing demand for clean-label and organic bakery products has boosted niche markets for unrefined and fair-trade brown sugar. EU regulations, including the Farm to Fork Strategy and national reformulation efforts, encourage manufacturers to innovate with blended or reduced-calorie brown sugar rather than eliminate sugar.

Sustainability efforts are key: in May 2024, Tereos launched a carbon-neutral refining pilot in Lille using biomass and water recycling. Nordzucker invested €70 million (US$76 million) in 2025 to electrify processes and expand specialty brown sugar production in Denmark. Südzucker partnered with Ingredion in 2023 to develop beet molasses-based sugar alternatives, reinforcing decarbonization and product diversification goals.

Competitive Landscape

The global industrial brown sugar market is moderately concentrated, with a mix of global refining groups and regional mills serving diverse end-use industries. Leading companies, such as Cargill, American Sugar Refining, Tate & Lyle, Südzucker, Tereos, Wilmar, Louis Dreyfus Company, and Raízen collectively account for a substantial portion of international trade and refining capacity. While Europe and North America display higher concentration levels, Asia Pacific region remains more fragmented with numerous national producers. Long-term supply contracts between refiners and major food manufacturers are common to mitigate pricing volatility.

Market leaders are focusing on vertical integration, expanding from cane cultivation to refining and packaging to ensure supply security. Product premiumization, through organic certification, sustainable sourcing, and specialized grades, is a defining theme. Companies are also investing in automation, logistics efficiency, and partnerships with bio-based industries to diversify revenue and reduce exposure to commodity price cycles.

Key Industry Developments

- In July 2025, Tate & Lyle expanded its ingredient portfolio by introducing enhanced sweetener and mouthfeel systems designed to complement sugar-reduction efforts in processed foods. This development highlights the company’s strategy of integrating natural sweeteners with industrial brown sugar applications for reformulated products.

- In April 2025, Wilmar International and partner companies reported increased ethanol output in India, resulting in tighter sugar export availability. The development emphasizes the growing linkage between sugar and energy markets, influencing industrial supply planning.

Companies Covered in Industrial Brown Sugar Market

- Cargill, Inc.

- American Sugar Refining (ASR Group)

- Tate & Lyle Plc

- Südzucker AG

- Tereos S.A.

- Raízen/Cosan

- Wilmar International Ltd.

- Louis Dreyfus Company

- Nordzucker AG

- Mitr Phol Group

- American Crystal Sugar Company

- China National Sugar and Alcohol Group

- Shree Renuka Sugars Ltd.

- Dalmia Bharat Sugar and Industries Ltd.

- Associated British Foods (ABF Sugar)

- Imperial Sugar Company

- EID Parry Ltd.

- Shandong Sugar Group

- COFCO Sugar

- Florida Crystals Corporation

Frequently Asked Questions

The industrial brown sugar market size was US$5.8 Billion in 2025.

By 2032, the market is projected to reach US$7.1 Billion, reflecting steady demand across bakery, beverage, and industrial fermentation applications.

Key trends include rising demand for clean-label and natural ingredients, growth in industrial fermentation and bio-based chemical applications, premiumization through organic and traceable sugar, and increased adoption of liquid brown sugar syrups in beverages and dairy.

By product type, light brown sugar is the leading segment, accounting for approximately 59% of industrial sales by value, widely used in bakery, confectionery, and beverage manufacturing.

The industrial brown sugar market is projected to grow at a CAGR of 2.8% from 2025 to 2032.

Major players include Cargill, Inc., American Sugar Refining (ASR Group), Tate & Lyle Plc, Südzucker AG, and Mitr Phol Group.