- Beverages

- Zero Sugar Syrups Market

Zero Sugar Syrups Market Size, Share, and Growth Forecast 2026 - 2033

Zero Sugar Syrups Market by Product Type (Liquid syrups, Powdered syrups), by Sweetener Type (Natural sweeteners, Artificial sweeteners, Blended sweeteners), by Application (Beverages, Desserts & toppings, Bakery & cooking, Health & fitness foods), by End-user (Household, Foodservice, Food & beverage manufacturers), by Regional Analysis, 2026 - 2033

Zero Sugar Syrups Market Share and Trends Analysis

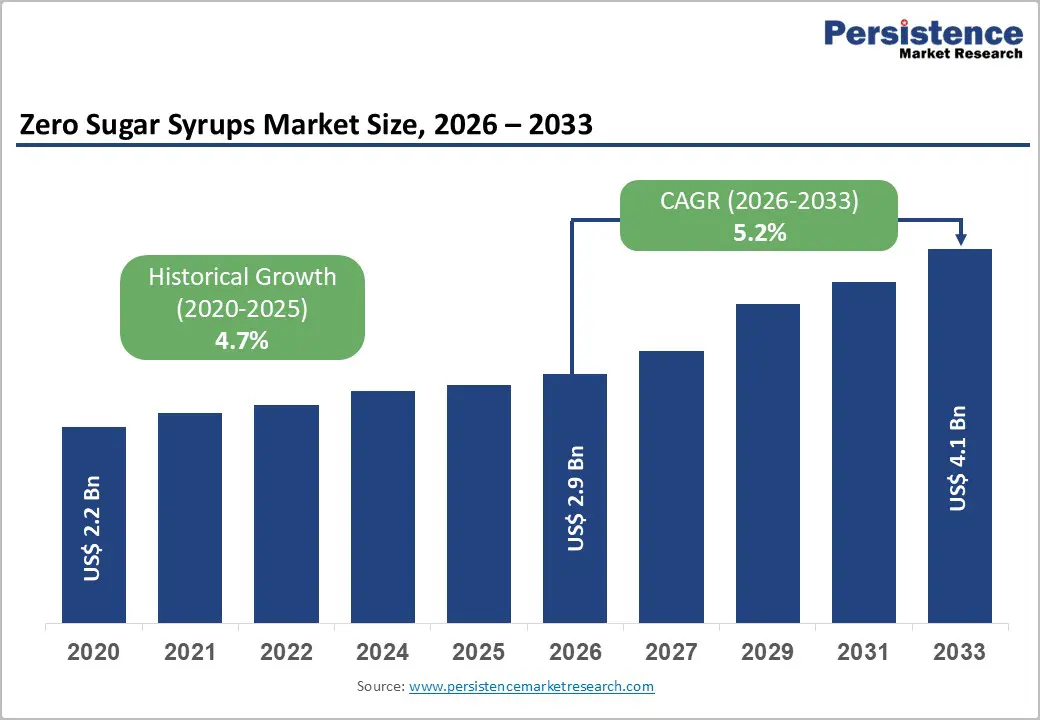

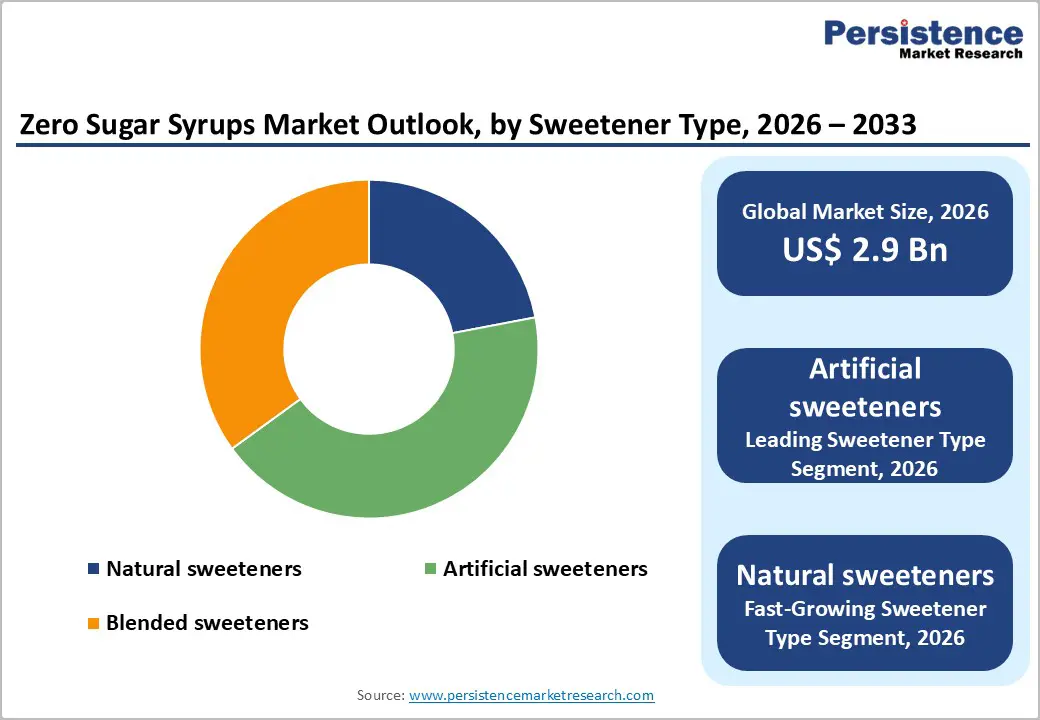

The global zero sugar syrups market size is expected to be valued at US$ 2.9 billion in 2026 and projected to reach US$ 4.1 billion by 2033, growing at a CAGR of 5.2% between 2026 and 2033.

The market's robust growth trajectory is primarily driven by the rise in global health concerns related to obesity and diabetes, with the World Health Organization (WHO) reporting that 890 million adults were living with obesity in 2022, representing a dramatic increase from 1990 levels. These rising obesity rates are pushing consumers and policymakers alike to focus on reducing added sugar intake in everyday diets, accelerating the shift towards sugar-free and reduced-sugar food and beverage alternatives. In parallel, the International Diabetes Federation (IDF) estimates that about 589 million adults aged 20-79 years were living with diabetes globally in 2024, with this figure expected to reach approximately 853 million by 2050, further intensifying demand for sugar substitutes and diabetic-friendly formulations. Health-conscious lifestyles, the popularity of ketogenic and low-carb diets, and the rapid spread of specialty coffee culture among millennials and Gen Z who seek both indulgence and calorie control are reinforcing sustained demand for zero sugar syrups across retail, foodservice, and industrial channels.

Key Industry Highlights:

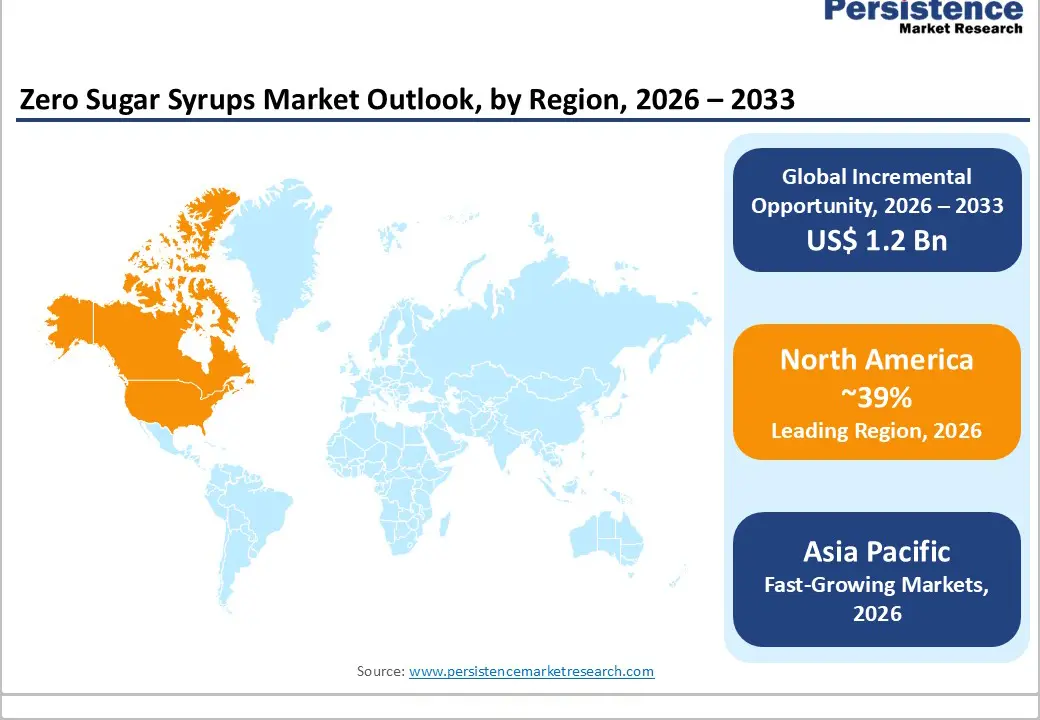

- North America remains the largest regional market, with around 39% share in 2025, driven by high obesity and diabetes prevalence, strong specialty coffee culture, significant foodservice penetration, and a supportive regulatory environment that recognizes key high-intensity and natural sweeteners as safe, enabling rapid expansion of sugar-free offerings across retail and out-of-home channels.

- Asia Pacific is projected to be the fastest-growing region through 2032, underpinned by rapid urbanization, rising disposable incomes, high concentration of the global diabetic population, sugar tax and labelling policies, and the aggressive expansion of café chains, bubble tea outlets, and modern retail that introduce consumers to zero sugar syrups as part of a broader shift toward healthier beverage choices.

- Liquid syrups are the dominant product type, accounting for roughly 68% share in 2025, due to their versatility, ease of dosing, quick solubility in hot and cold beverages, and the extensive flavor innovation by leading brands, making them a core ingredient for coffeehouses, bars, restaurants, and at-home beverage preparation.

- Natural sweeteners are expected to be the fastest-growing sweetener type segment, even though artificial sweeteners currently hold about 43% share, as clean-label demands, regulatory recognition of ingredients like stevia and monk fruit, and high-profile adoption by major beverage companies accelerate the shift toward plant-based sweetness in zero sugar syrups.

- The convergence of foodservice expansion and natural sweetener innovation represents a key market opportunity, enabling manufacturers to supply cafés, restaurants, and beverage brands with zero sugar syrups that offer both indulgent flavors and “better-for-you” credentials, particularly in high-growth markets such as Asia Pacific, where localized flavors and digital-first distribution strategies can unlock significant incremental demand.

| Key Insights | Details |

|---|---|

| Zero Sugar Syrups Size (2026E) | US$ 2.9 Bn |

| Market Value Forecast (2033F) | US$ 4.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.7% |

Market Dynamics

Drivers - Rising Health Consciousness and Regulatory Push Toward Sugar Reduction

Escalating awareness about the health risks of high sugar intake, including obesity, type 2 diabetes, and cardiovascular diseases, is one of the most powerful growth drivers for the zero sugar syrups market. The WHO has consistently highlighted that overweight and obesity affect hundreds of millions of adults worldwide, with global obesity nearly tripling since 1975, pushing governments to introduce sugar reduction policies and front-of-pack labelling to nudge healthier choices. In Europe, Regulation (EU) No 1169/2011 on food information to consumers tightened nutrition labelling rules and increased transparency on sugar content, while recent European Parliament moves in 2024 to modify directives on juices and jams have effectively lowered sugar levels in several categories.

In parallel, the U.S. Food and Drug Administration (FDA) recognizes several high-intensity sweeteners such as steviol glycosides from stevia and highly purified monk fruit extracts as Generally Recognized as Safe (GRAS) for use in foods and beverages, paving the way for sugar-free formulations that still deliver sweetness. With consumers increasingly reading labels and actively seeking “no added sugar” or “sugar-free” claims, brands across beverages, desserts, and sauces are incorporating zero sugar syrups to maintain taste while complying with evolving nutritional expectations and regulatory scrutiny.

Expanding Foodservice Industry and Specialty Coffee Culture Proliferation

The rapid expansion of the global foodservice industry, particularly café chains and specialty coffee outlets, is significantly boosting demand for zero sugar syrups. Flavored coffee and customizable beverages have become mainstream, and syrups are central to delivering the variety and indulgence consumers expect. Industry data indicates the broader coffee flavor syrup space is growing steadily, with the global coffee flavor syrup market estimated in the mid-single-digit billions of U.S. dollars and projected to advance at an annual growth rate of around 5-6% in the next decade, supported by café culture and home barista trends. Surveys from beverage and coffee industry stakeholders suggest that roughly one-quarter of café consumers choose flavored syrups in their beverages, and a rising proportion specifically request sugar-free or “skinny” options to manage calorie intake without sacrificing flavor.

Major chains such as Starbucks, Costa Coffee, and Dunkin’ now routinely offer zero sugar vanilla, caramel, and seasonal variants, normalizing sugar-free syrups in mainstream menus. In parallel, the India flavored syrups market is projected to grow from around US$ 3.2 billion in 2024 to nearly US$ 5.8 billion by the mid-2030s, expanding at an estimated 5-6% CAGR, reflecting rapid urbanization, rising café penetration, and experimentation with cold beverages and mocktails. As foodservice operators seek operational efficiency, consistency, and menu differentiation, zero sugar syrups are increasingly preferred over granulated sweeteners because they dose accurately, dissolve instantly in hot and cold beverages, and support premium pricing while appealing to health-conscious consumers.

Restraints - Consumer Perception Challenges Regarding Artificial Sweeteners and Aftertaste

Despite strong momentum, the zero sugar syrups market faces consumer perception hurdles, particularly related to synthetic sweeteners and taste quality. While regulatory agencies such as the FDA, European Food Safety Authority (EFSA) and other national bodies have repeatedly confirmed the safety of approved high-intensity sweeteners within established acceptable daily intakes, segments of consumers remain wary of artificial sweeteners like aspartame, saccharin, acesulfame-K, and sucralose due to media coverage, legacy controversies, or skepticism toward “chemical-sounding” ingredients. Sensory drawbacks also weigh on adoption: some high-intensity sweeteners can leave a bitter, metallic, or lingering aftertaste, especially at higher inclusion levels, making it difficult to fully replicate the rounded sweetness and mouthfeel of sucrose. Even natural-origin sweeteners such as stevia can exhibit herbal or licorice-like notes that certain consumers find noticeable. This creates a barrier in indulgent categories where taste is the top purchase driver, and any perceived compromise versus traditional sugar-based syrups may limit repeat purchase. As a result, brands using zero sugar syrups must invest in careful formulation, flavor masking, and blended sweetener systems to overcome taste challenges and maintain consumer satisfaction.

Premium Pricing and Raw Material Cost Volatility

Another key restraint is the relatively higher cost structure of zero sugar syrups compared with conventional sugar-based syrups. Many of the sweeteners used in zero sugar formulations-such as high-purity stevia extracts, monk fruit (luo han guo) extracts, erythritol, and allulose-are more expensive than refined sugar due to factors including limited cultivation zones, specialized extraction and purification processes, and patent or technology licensing in some cases. For example, the monk fruit sweetener market has been valued in the hundreds of millions of U.S. dollars and is forecast to grow at around 4-5% CAGR this decade, reflecting both rising demand and premium pricing sustained by supply constraints and concentration of production in China.

Agricultural risks, climate variability, and geopolitical issues can further impact harvest yields and ingredient costs. In price-sensitive developing markets, higher shelf prices for sugar-free syrups can slow mass-market adoption, especially when consumers perceive them as discretionary or premium products. At the industrial level, manufacturers must balance the cost of zero sugar sweeteners with competitive pricing and margin targets, which may limit formulation upgrades or delay the introduction of natural sweetener-based variants despite clear demand trends.

Opportunity - Rapid Growth in Natural Sweetener Adoption and Clean-Label Product Development

The accelerating shift toward natural-origin sweeteners and clean-label products presents a significant opportunity for zero sugar syrup manufacturers. Consumers increasingly favor labels that feature recognizable, plant-based ingredients over synthetic-sounding compounds, even within sugar-free products. The natural sweeteners space-including stevia, monk fruit, erythritol, and allulose-is expanding quickly; for instance, the India natural sweeteners market has been estimated at close to US$ 0.9-1.0 billion in 2024 and is expected to nearly double by early 2030s, advancing at a CAGR above 7%, reflecting strong growth in foods, beverages, and nutraceuticals. Regulatory developments are also supporting this trend: in 2024, authorities in the European Union and United Kingdom clarified that certain monk fruit preparations (decoctions of Siraitia grosvenorii) are “not novel,” lowering regulatory hurdles for their use in foods and beverages. Major beverage companies such as The Coca-Cola Company have tested new diet soft drink formulations sweetened with stevia and monk fruit instead of aspartame, signaling confidence in natural high-intensity sweeteners for mainstream applications.

Zero sugar syrup producers that develop proprietary blends combining stevia, monk fruit, and bulk sweeteners like erythritol or allulose can offer improved taste and mouthfeel, minimized aftertaste, and fully “natural” or “plant-based” positioning. This opens attractive premium price tiers and aligns with the clean-label strategies of better-for-you beverage brands, sports nutrition companies, and health-focused cafés.

Asia Pacific Market Expansion and Emerging Consumer Base Development

Asia Pacific offers one of the most compelling long-term opportunities for zero sugar syrups, thanks to demographic, economic, and epidemiological shifts. The International Diabetes Federation estimates that roughly 60% of the world’s diabetic population lives in Asia, with China, India, and countries across Southeast Asia recording rapidly rising diabetes and obesity burdens due to changing diets and urban lifestyles. At the same time, disposable incomes are rising, urban middle classes are expanding, and Western-style café culture is spreading beyond capital cities into secondary urban centers. Market estimates suggest that the Asia-Pacific sugar-free confectionery and candy sector alone is projected to grow from around US$ 2.5billion in the mid-2020s to more than US$ 4.0 billion by early 2030s, demonstrating strong appetite for sugar-reduced products. In India, flavored syrup usage in cafés, quick-service restaurants, and home consumption is forecast to rise steadily, with the broader flavored syrup market expected to reach nearly US$ 5.8 billion by around 2035. For zero sugar syrup manufacturers, this creates opportunities to localize flavor portfolios (for example, matcha, taro, rose, mango, or regional dessert-inspired flavors), collaborate with fast-growing café and bubble tea chains, and leverage e-commerce platforms in markets like China, India, and Indonesia to reach digitally savvy, health-conscious consumers. Companies that combine strong regional partnerships with tailored formulations that align with local taste profiles and regulatory requirements can capture outsized growth in these emerging markets.

Category-wise Analysis

Product Type Insights

Liquid syrups are the leading product type in the zero sugar syrups market, accounting for an estimated 68% share in 2025. Their dominance is rooted in ease of use, rapid solubility, and broad applicability across both cold and hot beverages, as well as desserts and toppings. Foodservice operators favor liquid formats because they enable consistent dosing using pumps or shot systems, minimize preparation time, and reduce training complexity for staff in cafés, quick-service restaurants, and bars. Major brands such as Monin, Torani, and DaVinci Gourmet have built extensive flavor portfolios almost entirely around liquid syrups, offering classic options such as vanilla, caramel, and hazelnut as well as seasonal and limited-edition profiles such as pumpkin spice or peppermint mocha. Packaging innovation, ranging from shelf-stable PET bottles and glass bottles to bag-in-box formats for high-volume outlets, further strengthens the appeal of liquid products. From a formulation standpoint, liquids also allow better integration of flavor compounds, acidity regulators, and functional ingredients to emulate the body and mouthfeel of sugar, which is particularly important in zero sugar variants.

Sweetener Type Insights

Within the sweetener type segmentation, artificial sweeteners currently represent the leading share, at about 43% of the zero sugar syrups market in 2025. Widely used sweeteners such as sucralose, aspartame, acesulfame potassium (Ace-K), and saccharin offers intensifies the sweetness, enabling very low use levels and competitive cost-in-use, which is critical for large-scale foodservice and industrial applications. Regulatory bodies, including the FDA and EFSA, have extensively evaluated these sweeteners and established acceptable daily intakes, providing manufacturers with a robust safety framework. As a result, artificial sweeteners remain prevalent in mainstream zero sugar syrups, particularly where affordability and broad consumer familiarity are key. However, natural sweeteners such as stevia and monk fruit are the fastest-growing sweetener segment, supported by clean-label demand and regulatory advances such as the EU and UK decisions on monk fruit preparations. The broader natural sweeteners market globally is expected to rise from roughly the mid-tens of billions of U.S. dollars in the mid-2020s to well above US$ 50 billion by 2030, indicating a powerful shift that will increasingly influence zero sugar syrup formulations and positioning.

Application Insights

Beverages are the dominant application for zero sugar syrups, accounting for an estimated 52% market share in 2025. Syrups are deeply embedded in the value proposition of specialty coffees, iced teas, flavored waters, carbonated soft drinks, cocktails, mocktails, smoothies, and functional drinks. The global sugar-free beverages segment is growing rapidly, with some analyses estimating that sugar-free or no-sugar-added beverages could exceed US$ 190-200 billion in value by the mid-2030s, rising from about US$ 70-80 billion in the mid-2020s at a high single- to low double-digit CAGR. Beverage giants such as The Coca-Cola Company, PepsiCo, and Nestlé are expanding their portfolios of zero-sugar carbonated drinks, flavored waters, and energy drinks, often relying on syrup bases during manufacturing or in fountain systems. The success of brands such as Zevia, which has sold more than 1.9 billion cans sweetened with stevia and monk fruit rather than sugar, further demonstrates consumer willingness to adopt sugar-free drinks when taste expectations are met. Zero sugar syrups are also used in alcoholic beverage mixers and low- or no-alcohol cocktails, supporting the “better-for-you” trend in bars and hospitality.

End-user Insights

Food & beverage manufacturers represent the leading end-user group, with an estimated 46% share of zero sugar syrup consumption in 2025. Large-scale producers of ready-to-drink beverages, dairy products, ice cream, yogurt, breakfast cereals, and bakery items use zero sugar syrups as flavoring and sweetening components to reformulate products in line with sugar reduction targets and voluntary health pledges. Policies such as the EU Farm to Fork Strategy, national sugar taxes in several countries, and retailer-led nutrition score schemes push brands to lower added sugars while preserving sensory quality. Industrial users demand syrups with specific functional properties such as thermal stability, pH tolerance, freeze-thaw resilience, and compatibility with existing processes prompting suppliers like The J.M. Smucker Company and specialty ingredient firms to develop tailored solutions. The foodservice segment, including cafés, restaurants, hotels, and quick-service outlets, is the fastest-growing end-user group, with growth rates estimated above 6% CAGR through the early 2030s, reflecting the rising number of outlets worldwide and the expanding range of sugar-free menu options. Household users also contribute to growth as consumers adopt home brewing and home café culture, purchasing zero-sugar syrups via retail and e-commerce to replicate coffeehouse-style beverages at home.

Regional Insights

North America Zero Sugar Syrups Market Trends and Insights

North America is the leading regional market, accounting for approximately 39% share in 2025, anchored by the United States. High obesity and diabetes prevalence, combined with strong purchasing power and a well-developed café culture, create ideal conditions for zero sugar syrup adoption. The CDC has reported that roughly 4 out of 10 U.S. adults are living with obesity, and at least 19 states have adult obesity rates above 35%, underscoring the urgency of dietary sugar reduction. In parallel, the FDA’s recognition of high-intensity sweeteners like stevia and monk fruit extracts as GRAS supports aggressive sugar-free innovation across beverages, dairy, and snacks.

The U.S. is one of the world’s largest markets for premium coffee, with hundreds of thousands of coffee-focused outlets and a high share of consumers purchasing espresso-based and flavored beverages. Brands including Monin, Torani, DaVinci Gourmet, Jordan’s Skinny Mixes, Walden Farms, ChocZero, Lakanto, and SweetLeaf have built strong positions by serving both foodservice chains and the at-home consumer via grocery and online channels.

Asia Pacific Zero Sugar Syrups Market Trends and Insights

Asia Pacific is the fastest-growing region for zero-sugar syrups, expected to post the highest CAGR between the mid-2020s and early 2030s. The region combines some of the world’s highest and fastest-growing burdens of diabetes with strong growth in modern retail and foodservice. The IDF highlights that China, India, and Pakistan are among the countries with the largest diabetic populations, and rising incidence among younger age groups is spurring public health campaigns focusing on sugar reduction. Governments in countries such as Thailand, Philippines, and Malaysia have introduced sugar taxes on sweetened beverages, while authorities in Singapore and others have implemented labeling and advertising restrictions on high-sugar drinks, directly boosting industry interest in zero sugar formulations.

Simultaneously, café culture and Western-style beverage concepts are expanding rapidly. In China, the proliferation of domestic and international coffeehouse chains, tea shops, and bubble tea brands has generated strong demand for flavored syrups, including sugar-free variants for calorie-conscious urban consumers. In India, the flavored syrups market is growing at around 5-6% CAGR, reflecting the expansion of café chains, fast casual dining, and at-home experimentation, with local flavors such as cardamom, rose, and mango gaining traction alongside international favorites. E-commerce channels in markets like China (via platforms such as Tmall and JD.com) and India (via Amazon and Flipkart) enable both global players and regional brands to reach consumers beyond tier-1 cities, accelerating category awareness. Fitness and wellness trends, increased gym memberships, and the rise of protein shakes and functional drinks further support zero sugar syrup use in health & fitness foods.

Competitive Landscape

The zero sugar syrups market is highly competitive, driven by innovation in sweetener technology and flavor variety. Competitors focus on product differentiation through clean-label formulations, unique taste profiles, and enhanced natural ingredient blends to attract health-conscious consumers. Price, distribution strength, and branding play key roles in market positioning, with premium offerings competing against value-driven alternatives. Marketing emphasizes low-calorie, sugar-free benefits and lifestyle alignment. Strategic partnerships with foodservice channels and e-commerce growth further intensify rivalry. Continuous R&D into better-tasting and more natural formulations drives ongoing competition, while regulatory compliance and consumer trust remain critical for market success.

Key Developments:

- In July 2025, Jordan’s Skinny Mixes, the brand known for enhancing everyday routines, launched of its new Energy Syrup line. The bold, fruit-forward syrups were introduced in three crave-worthy flavors Wild Berry, Peach Mango, and Strawberry Dragonfruit, designed to mix seamlessly into water, sparkling water, teas, smoothies, or any beverage of choice.

Companies Covered in Zero Sugar Syrups Market

- Monin

- Torani

- Jordan’s Skinny Mixes

- DaVinci Gourmet

- Walden Farms

- ChocZero

- Maple Grove Farms

- The J.M. Smucker Company

- SweetLeaf

- Nature’s Hollow

- Lakanto

- Paleo Powder

- Other

Frequently Asked Questions

The global zero sugar syrups market is expected to be valued at about US$ 2.9 billion in 2026, supported by growing health consciousness, widespread sugar reduction initiatives, and rising demand for sugar-free flavored beverages across retail and foodservice channels.

Key growth drivers include rising global obesity and diabetes prevalence, highlighted by WHO and IDF data, regulatory pressure to cut added sugars, shifting consumer preference toward lower-calorie and clean-label products, and the expansion of specialty coffee culture, where flavored sugar-free syrups enable indulgent yet health-conscious beverage customization.

North America is the leading region, with an estimated 39% share in 2025, driven by a mature café ecosystem, high consumption of flavored coffee and soft drinks, strong regulatory clarity around sweeteners, and a large health-conscious consumer base that actively seeks sugar-free alternatives across multiple food and beverage categories.

A major opportunity lies in combining natural sweeteners such as stevia and monk fruit with flavor innovation and localized product development, especially in fast-growing Asia-Pacific markets, to deliver clean-label, great-tasting zero sugar syrups that meet regulatory expectations and appeal to consumers seeking healthier beverages and desserts without compromising on indulgence.

Prominent companies include Monin, Torani, Jordan’s Skinny Mixes, DaVinci Gourmet, Walden Farms, ChocZero, Maple Grove Farms, The J.M. Smucker Company, SweetLeaf, Nature’s Hollow, Lakanto.