- Processed Food

- Liquid Sugar Market

Liquid Sugar Market Size, Share, and Growth Forecast, 2025 - 2032

Liquid Sugar Market by Product Type (Liquid Sucrose, Invert Sugar Syrup, Others), Source (Cane-based Sugar, Beet-based Sugar, Others), Application (Beverages, Bakery, Confectionery, Baby Foods, Pharmaceuticals, Others), and Regional Analysis for 2025 - 2032

Liquid Sugar Market Size and Trends Analysis

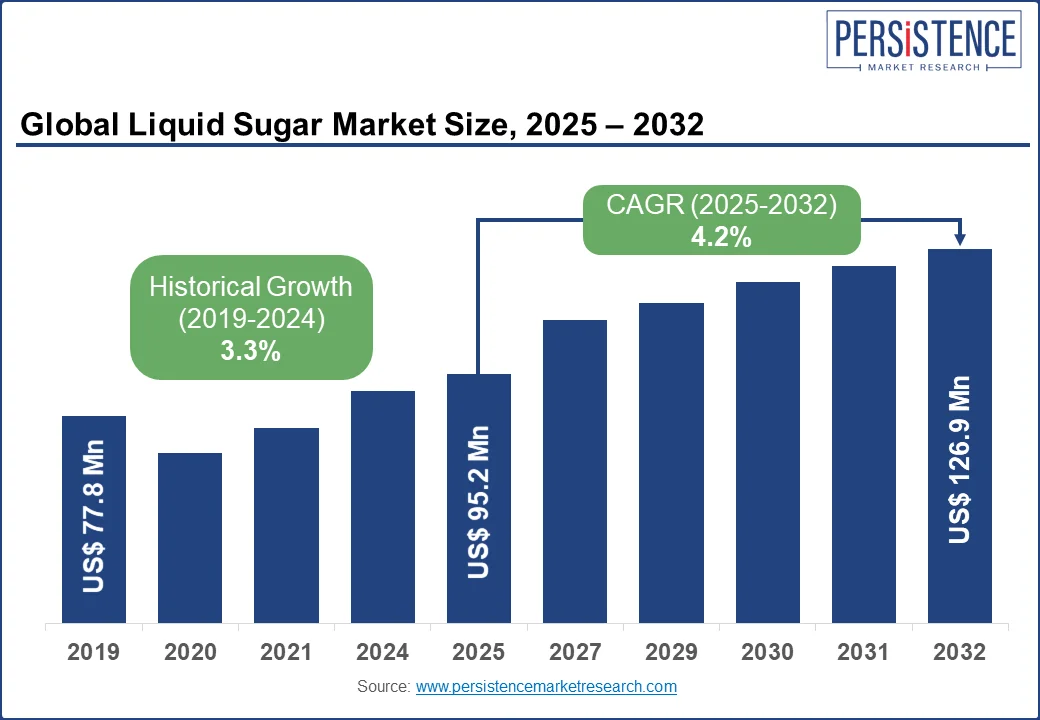

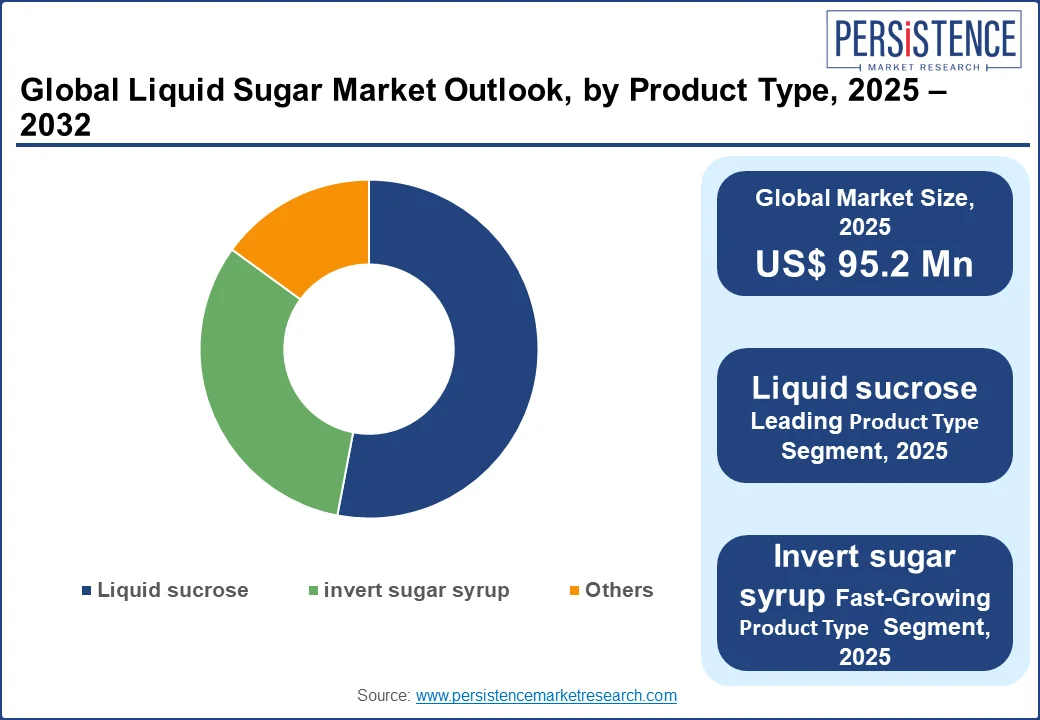

The global liquid sugar market size is likely to be valued at US$95.2 Mn in 2025 and is expected to reach US$126.9 Mn by 2032, growing at a CAGR of 4.2% during the forecast period from 2025 to 2032.

The liquid sugar industry has witnessed steady growth, driven by increasing demand for convenient, ready-to-use sweeteners in the food and beverage industry, advancements in processing technologies, and rising consumer preference for liquid sweeteners over granulated sugar in various applications.

The growing adoption of liquid sugar in beverages, confectionery, and bakery products is particularly prevalent in regions with robust food processing industries. Additionally, the versatility of liquid sugar in industrial applications and its ease of integration into manufacturing processes have further fueled market expansion.

Key Industry Highlights:

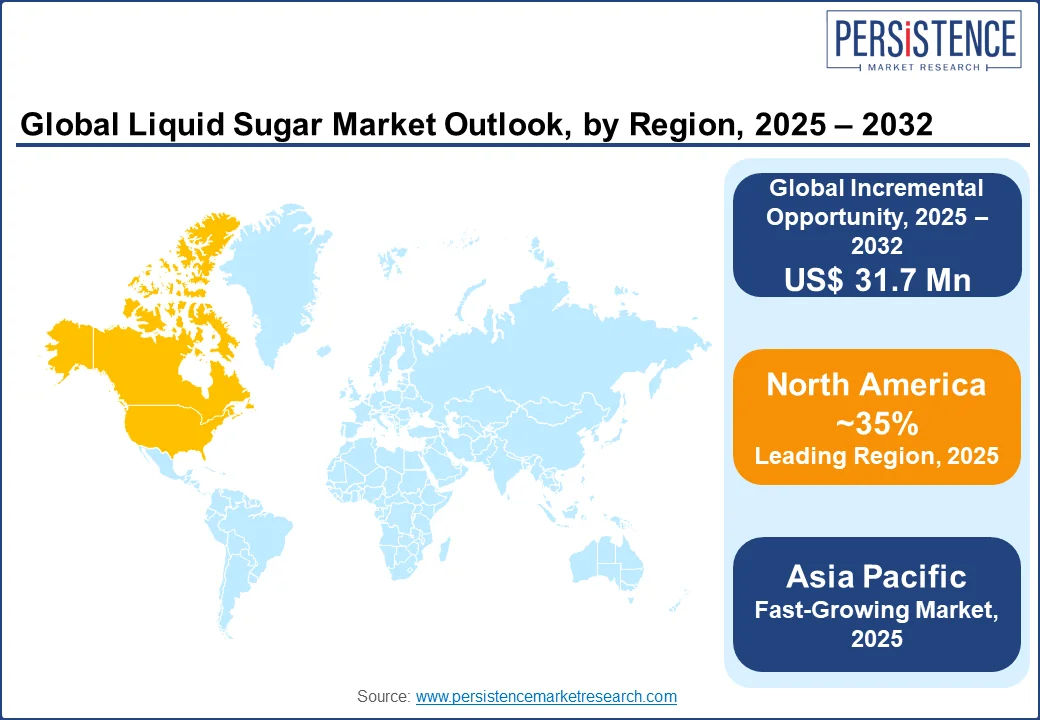

- Leading Region: North America, holding a 35% market share in 2025, driven by the strong presence of food and beverage industries in the U.S., high adoption of liquid sweeteners, and significant investments in food processing innovations.

- Fastest-growing Region: Asia Pacific, emerging as the fastest-growing market, fueled by rapid urbanization, increasing demand for processed foods, and growing investments in food manufacturing in countries such as China and India.

- Dominant Product Type: Liquid Sucrose, commanding nearly 53% market share, due to its widespread use in beverages and confectionery for its ease of blending and consistent sweetness.

- Leading Application: Beverages, accounting for over 45% of market revenue, driven by the rising demand for sweetened drinks and the convenience of liquid sugar in large-scale production.

|

Global Market Attribute |

Key Insights |

|

Liquid Sugar Market Size (2025E) |

US$95.2 Mn |

|

Market Value Forecast (2032F) |

US$126.9 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

4.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.3% |

Market Dynamics

Driver - Rising demand for convenience in food and beverage processing

The increasing demand for convenience in food and beverage manufacturing is a major driver of the liquid sugar market. Unlike crystalline sugar, liquid sugar offers a ready-to-use formulation that eliminates the need for dissolution, filtration, and additional processing steps, thereby saving time and reducing labor costs in production facilities. This convenience is particularly valuable in large-scale operations such as carbonated beverage production, dairy processing equipment, confectionery, and bakery industries, where consistency, speed, and efficiency are critical.

Food and beverage manufacturers also prefer liquid sugar for its uniform sweetness distribution, ease of blending with other ingredients, and ability to maintain product stability. These attributes help improve overall production efficiency while ensuring consistent taste and quality across product lines.

Moreover, liquid sugar supports automation in modern manufacturing plants, making it easier to integrate into streamlined, high-speed production systems. Government policies and food safety regulations are also shaping this trend. For instance, regulatory authorities in markets such as the U.S. and the EU promote standardized sweetener formulations for quality assurance and streamlined manufacturing.

This, in turn, encourages greater adoption of liquid sugar, which meets both efficiency and compliance requirements. As consumer preferences shift toward ready-to-drink beverages, packaged bakery items, and confectionery products, the demand for liquid sugar is expected to rise further, positioning it as a key ingredient that enhances both convenience and scalability in food and beverage processing.

Restraint - Fluctuating raw material prices

Fluctuating raw material prices, particularly for sugarcane and sugar beets, pose a significant restraint on the liquid sugar market. One of the key restraints in the liquid sugar market is the fluctuating price of raw materials, particularly sugarcane and sugar beet.

Since liquid sugar is directly derived from these crops, any volatility in their prices significantly impacts production costs and market stability. Weather conditions, such as droughts, floods, or unexpected frosts, can reduce crop yields, create supply shortages, and drive up raw material prices. Similarly, global trade dynamics, export restrictions, and tariff changes also contribute to pricing uncertainty.

Energy and transportation costs further influence overall production expenses, as refining and processing sugar into liquid form require substantial energy inputs. For instance, rising fuel prices can increase both farming and logistics costs, making liquid sugar less affordable for food and beverage manufacturers.

Government policies often amplify these challenges. For instance, in India, the government’s ethanol blending program redirects a significant share of sugarcane supply toward biofuel production, tightening availability for sugar processing industries.

Similarly, Brazil’s frequent policy shifts regarding ethanol subsidies affect global sugar export volumes. Such interventions disrupt supply-demand balance, intensify raw material price fluctuations, and create difficulties for liquid sugar manufacturers in maintaining consistent pricing and margins.

Opportunity - Growing demand for natural and clean-label sweeteners

The growing consumer preference for natural and clean-label sweeteners presents a significant growth opportunity for the liquid sugar market. With growing health awareness, consumers are actively seeking products free from artificial additives, preservatives, and synthetic sweeteners.

Liquid sugar, derived from natural sources such as sugarcane and sugar beet, is increasingly being positioned as a clean-label ingredient that aligns with this trend. Food and beverage companies are leveraging liquid sugar to cater to the expanding market for organic juices, dairy-based drinks, bakery items, and confectionery products that emphasize natural formulation.

Governments across the globe are also reinforcing this transition toward clean-label and natural ingredients. For instance, the U.S. Food and Drug Administration (FDA) has introduced stricter labeling requirements, compelling manufacturers to provide transparent information about added sugars and natural content.

Similarly, the European Food Safety Authority (EFSA) has been encouraging the use of natural sweeteners in reformulated food products to promote healthier consumption. These regulatory pushes create a favorable landscape for liquid sugar as a naturally derived sweetening solution, opening significant opportunities for innovation and market expansion.

Category-wise Analysis

Product Type Insights

Liquid sucrose dominates, expected to account for approximately 53% share in 2025. Its dominance stems from its widespread use in beverages and confectionery, where its ease of blending and consistent sweetness make it a preferred choice for manufacturers. Liquid sucrose, offered by companies such as Cargill and Tate & Lyle, supports high-volume production and ensures product uniformity, driving its adoption in large-scale food processing.

The invert sugar syrup segment is the fastest-growing, driven by its enhanced functionality in bakery and confectionery applications. Invert sugar syrup prevents crystallization, extends shelf life, and enhances moisture retention, making it ideal for products such as cakes, candies, and soft drinks. The growing demand for premium and artisanal food products is accelerating the adoption of invert sugar syrup, particularly in North America and Europe.

Source Insights

Cane-based Sugar dominates, holding approximately 79% share in 2025. Its dominance is driven by the abundant availability of sugarcane in tropical regions, cost-effective production, and its preferred use in beverages and confectionery. Companies such as Wilmar International and Louis Dreyfus leverage cane-based liquid sugar to cater to global demand, particularly in the Asia Pacific and Latin America.

The beet-based Sugar segment is the fastest-growing, fueled by increasing production in Europe and North America, where sugar beets are a major crop. Advances in beet sugar processing technologies and the rising demand for regionally sourced sweeteners are driving growth in this segment, particularly in countries such as Germany and the U.S.

Application Insights

Beverages led the liquid sugar market, holding a 45% share in 2025. The segment’s dominance is driven by the extensive use of liquid sugar in soft drinks, energy drinks, and ready-to-drink beverages, where it ensures rapid dissolution and consistent sweetness. Companies such as ADM and Südzucker supply liquid sugar to major beverage manufacturers, streamlining production and reducing costs.

The bakery segment is the fastest-growing, fueled by the rising demand for convenience bakery products and the functional benefits of liquid sugar in enhancing texture and shelf life. The global bakery market is driving demand for liquid sugar, particularly in North America and the Asia Pacific, where urbanization and changing consumer preferences are boosting consumption.

Regional Insights

North America Liquid Sugar Market Trends

North America is projected to hold a substantial 35% market share in the global liquid sugar market, driven by the region’s strong food and beverage industry and high adoption of liquid sweeteners. The United States remains the largest contributor, with liquid sugar widely utilized across carbonated soft drinks, ready-to-drink beverages, bakery, dairy, and confectionery sectors.

Major beverage manufacturers in the U.S. and Canada prefer liquid sugar due to its ease of blending, consistent sweetness, and compatibility with large-scale automated processing systems, helping them meet both efficiency and quality standards.

The region is also witnessing increasing investments in food processing innovations and clean-label product development. As consumer preferences shift toward transparency and natural ingredients, manufacturers are reformulating products using liquid sugar as a clean-label sweetener.

Additionally, the growing demand for convenience foods and ready-to-drink beverages supports the expansion of liquid sugar applications. Government initiatives promoting food innovation and transparent labeling, such as the FDA’s Nutrition Facts labeling rules, further enhance adoption. With strong industry presence and regulatory support, North America continues to be a leading hub for liquid sugar demand and innovation.

Europe Liquid Sugar Market Trends

Europe represents a key region in the liquid sugar market, holding a significant share in 2025, supported by the region’s strong bakery, confectionery, and beverage industries. Countries such as Germany, France, the U.K., and Italy are at the forefront, where liquid sugar is extensively used in bakery items, chocolates, dairy products, and soft drinks. European food manufacturers prefer liquid sugar due to its convenience, uniformity, and ability to streamline large-scale production processes while ensuring product consistency.

The region is also witnessing strong consumer demand for clean-label and natural sweeteners, aligning with the rising health-conscious population. Liquid sugar is being increasingly integrated into reformulated food and beverage products that aim to reduce additives and artificial ingredients.

Additionally, Europe’s well-established regulatory frameworks, such as the European Food Safety Authority (EFSA) guidelines, support the use of liquid sugar in compliance with strict quality and labeling requirements. With growing investments in food innovation, automation in processing plants, and rising demand for packaged and convenience foods, Europe is set to remain a strong growth hub for liquid sugar adoption, creating opportunities for both global and regional suppliers.

Asia Pacific Liquid Sugar Market Trends

Asia Pacific is poised to be the fastest-growing region in the liquid sugar market in 2025, underpinned by rapid urbanization, rising disposable incomes, and the expansion of large-scale food and beverage manufacturing. Key demand centers, including China, India, Japan, South Korea, and Southeast Asia, are increasing their liquid sugar usage across various sectors such as ready-to-drink beverages, dairy, bakery, confectionery, and instant foods, where uniform sweetness, easy handling, and compatibility with automated lines are critical. The dominance of sugarcane supply chains in India and Southeast Asia supports stable sourcing and competitive pricing for liquid formats.

Manufacturers are accelerating investments in high-throughput mixing, inline dosing, and CIP-friendly systems, where liquid sugar simplifies operations versus crystalline inputs. Clean-label momentum is also lifting adoption, as brands reformulate for fewer additives while preserving taste and texture.

Government initiatives such as food-processing incentives, cold-chain and park infrastructure programs, and labeling modernization are encouraging capacity additions and process upgrades, particularly in India and China. Meanwhile, the region’s booming e-commerce and HoReCa channels favor liquid ingredients that enable consistent, scalable production. Although cane price swings remain a watchpoint, Asia Pacific’s manufacturing scale, policy support, and evolving consumer preferences position the region as a primary growth engine for liquid sugar through the forecast period.

Competitive Landscape

The global liquid sugar market is marked by intense competition, combining the dominance of global leaders with the presence of numerous regional and niche players. In developed markets such as North America and Europe, companies such as Cargill, ADM, and Tate & Lyle lead with economies of scale, advanced processing capabilities, and strong supply networks.

Meanwhile, the Asia Pacific region is witnessing rapid growth, supported by expanding food processing industries and investments from both global giants such as Wilmar International and local cost-focused vendors. The sector shows a dual structure consolidated at the top, yet fragmented and scattered across regional and mid-sized firms.

To stay competitive, companies emphasize sustainable sourcing, clean-label certifications, innovation in liquid sugar variants, and strategic collaborations, especially as demand rises for organic and premium food products.

Key Developments

- In April 2025, Cargill reopened its revamped Innovation Center in Singapore, supported by EnterpriseSG and EDB, aiming to accelerate product innovation across Asia.

- In May 2024, Tate & Lyle set science-based emissions reduction targets validated by the SBTi: 38% reduction in Scope 1 & 2 and Scope 3 (Energy & Industrial) and 23% reduction in FLAG emissions by 2028.

Companies Covered in Liquid Sugar Market

- Cargill, Incorporated

- Archer Daniels Midland Company (ADM)

- Tate & Lyle PLC

- Südzucker AG

- Nordzucker AG

- Tereos S.A.

- Ingredion Incorporated

- Bunge Limited

- Wilmar International

- Louis Dreyfus Company

- Others

Frequently Asked Questions

The global Liquid Sugar Market is projected to reach US$ 95.2 Mn in 2025.

The rising demand for convenience in food and beverage processing is a key driver.

The liquid sugar market is poised to witness a CAGR of 4.2% from 2025 to 2032.

Growing demand for natural and clean-label sweeteners is a key opportunity.

Cargill, ADM, Tate & Lyle, Südzucker, and Nordzucker are key players.