- Specialty & Fine Chemicals

- Sodium Lactate Market

Sodium Lactate Market Size, Share, and Growth Forecast 2025 - 2032

Sodium Lactate Market by Grade (Electronic, Technical), Application (Electrolyte Solvent, Cosmetics & Personal Care, Pharmaceutical Intermediates, Textiles & Dyeing), Industry (Paints & Coatings, Industrial Manufacturing & Chemicals, Others), and Regional Analysis 2025 - 2032

Sodium Lactate Market Share and Trends Analysis

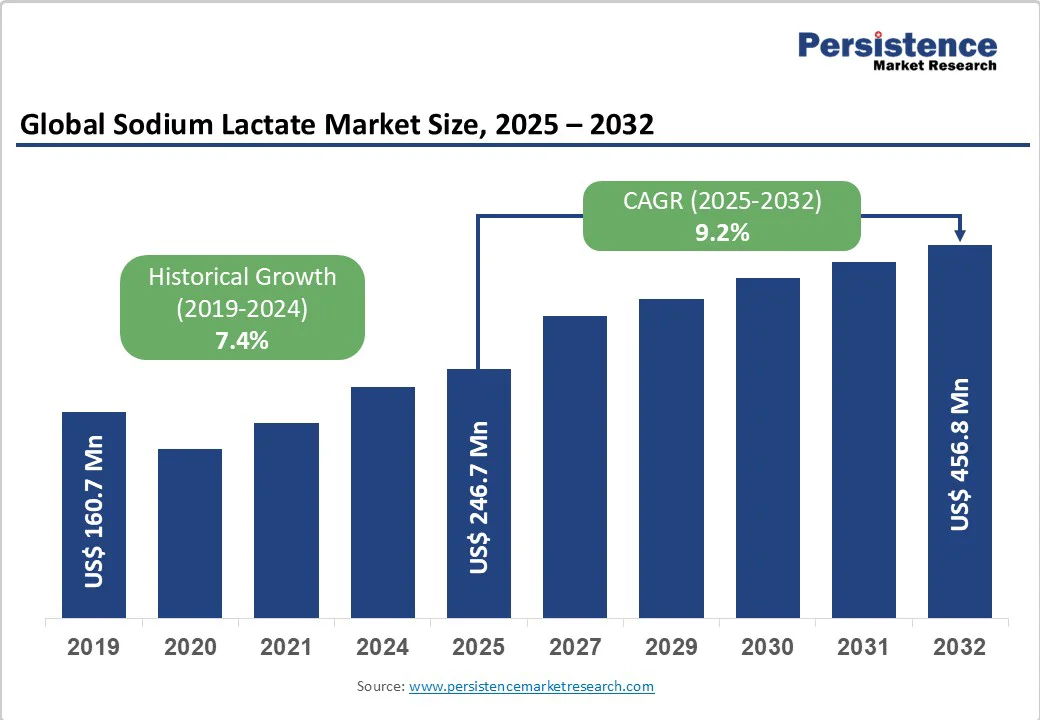

The global Sodium Lactate Market size is likely to reach US$246.7 Million in 2025 and is projected to reach US$456.8 Million by 2032, growing at a CAGR of 9.2% between 2025 and 2032. Market expansion is driven by rising demand for clean-label preservatives and the multifunctionality of sodium lactate as a pH regulator, humectant, and antimicrobial agent, bolstered by stringent food safety regulations worldwide.

Furthermore, the increasing adoption in the pharmaceutical and personal care industries, owing to its biocompatibility, supports sustained growth. Technological advancements in fermentation processes and the expansion of industrial-grade production capacities underpin forecasted market acceleration.

Key Highlights:

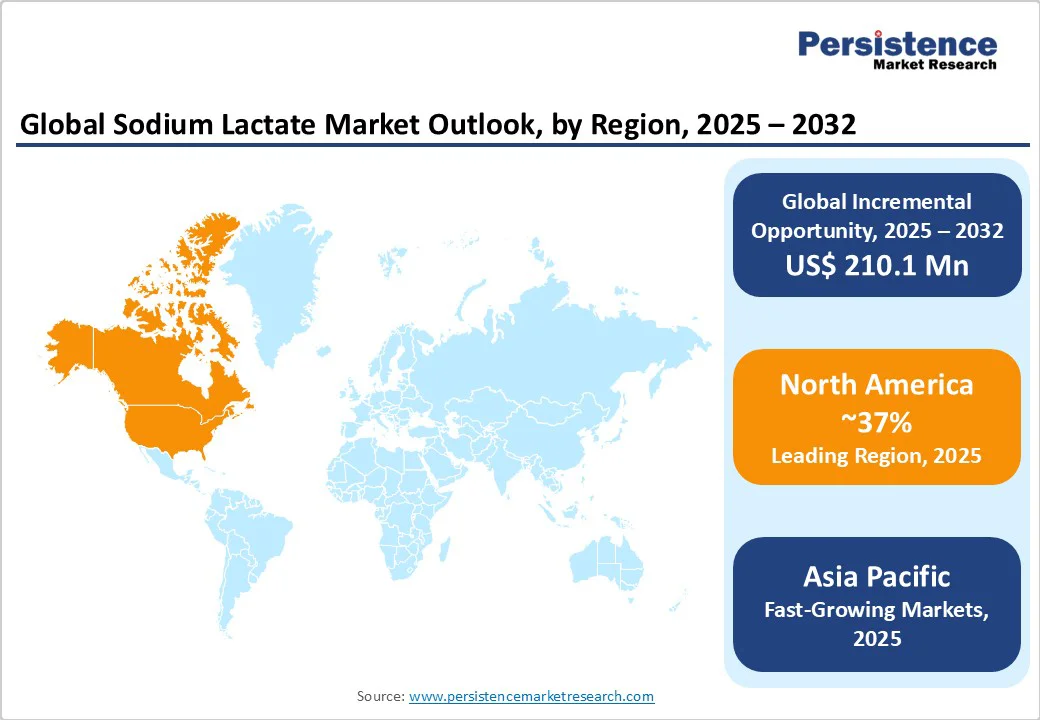

- Leading region: North America leads the Sodium Lactate Market, supported by advanced food processing infrastructure and stringent FDA validation, ensuring high adoption rates.

- Fastest growing region: Asia Pacific exhibits the fastest growth, driven by government incentives in biotechnology and expanding food and pharmaceutical industries.

- Dominant segment: The preservative and antimicrobial agent application dominates due to critical shelf-life extension and clean-label demand.

- Fastest growing segment: Pharmaceutical/USP Grade shows rapid growth, fueled by increasing injectable formulations and stringent pharmacopeia standards.

- Key market opportunity: Expansion of powder sodium lactate offerings for specialty applications presents significant revenue potential across cosmetics and food industries.

| Key Insights | Details |

|---|---|

|

Sodium Lactate Market Size (2025E) |

US$246.7 Million |

|

Market Value Forecast (2032F) |

US$456.8 Million |

|

Projected Growth CAGR (2025–2032) |

9.2% |

|

Historical Market Growth (2019–2024) |

7.4% |

Market Dynamics

Driver - Clean-Label Consumer Trends Driving Preservative Demand

Consumers worldwide are increasingly seeking transparent ingredient labels in their food products, with a Nielsen survey indicating that 73% of global consumers actively avoid products containing artificial preservatives. This shift has elevated demand for naturally derived alternatives, such as sodium lactate, which both the U.S. FDA and EFSA recognize as a safe, clean-label preservative. Its antimicrobial efficacy against pathogens like Listeria monocytogenes and Staphylococcus aureus extends shelf life by up to 30 days in processed meats and ready-to-eat foods, bolstering manufacturer adoption.

In North America alone, usage of sodium lactate as a food preservative grew by 9% in 2024, driven by retail chains enforcing stricter clean-label mandates. This trend is mirrored in Europe, where retailer-led initiatives have standardized “no artificial preservatives” claims. As food safety regulations tighten in the Asia Pacific—particularly in China and India—local processors are investing in fermentation facilities to produce food-grade sodium lactate domestically. These combined forces of regulatory endorsement, consumer preference, and proven efficacy establish clean-label demand as a primary growth driver for the sodium lactate market.

Expansion of Pharmaceutical and Personal Care Applications

The sodium lactate market’s pharmaceutical and personal care segments are experiencing robust growth due to the compound’s multifunctionality. In pharmaceuticals, USP-grade sodium lactate is employed in intravenous infusions to correct metabolic acidosis and in buffer formulations, with the global infusion therapy market projected to grow at 8.5% CAGR through 2030. The dermatology and skincare sectors leverage sodium lactate’s humectant properties; a 2024 report highlighted a 12% year-over-year increase in demand for clinical-grade humectants for moisturizers targeting xerosis and sensitive skin. Its pH-regulating function ensures formulation stability, making it indispensable in both OTC creams and prescription topical treatments.

Brands in North America and Europe have reformulated popular moisturizers to include sodium lactate, boosting product sales by 10%. In Asia, rising urbanization and disposable income have spurred cosmetic consumption, with India’s skincare market expanding at a 14% CAGR. As biocompatibility and regulatory approval remain critical, pharmaceutical and personal care companies continue to prioritize sodium lactate in new product pipelines, reinforcing its role as a key market driver.

Restraint - Raw Material Price Volatility and Supply Chain Risks

Sodium lactate production hinges on lactic acid, predominantly sourced from corn or sugarcane feedstocks. Price fluctuations in these commodities—driven by weather events, biofuel policies, and geopolitical tensions—have introduced significant cost volatility. In 2024, lactic acid prices oscillated by ±15%, directly compressing margins for sodium lactate producers. Regional disparities exacerbate the issue: North America’s reliance on U.S. corn contrasts with Europe’s reliance on imported feedstocks, creating supply chain imbalances.

Moreover, the ongoing logistics disruptions since 2022 have elevated shipping costs for bulk lactic acid by 20%, prompting some mid-scale producers to delay facility expansions. Smaller players, lacking integrated lactic acid production, face higher exposure to spot-price swings, hindering competitive pricing. Efforts to diversify feedstock sources—such as utilizing lignocellulosic biomass—are in nascent stages, with pilot projects underway but no commercial breakthroughs. Until alternative feedstocks are scalable, raw material price instability remains a critical restraint, limiting margin expansion and deterring capacity investments in the sodium lactate market.

Regulatory Complexity and Compliance Burdens

While sodium lactate enjoys broad approvals in key markets, the heterogeneity of regional regulations poses compliance challenges. Under the EU’s REACH framework, manufacturers must register sodium lactate for each specific use category, incurring registration fees and extensive testing requirements. In contrast, North America’s FDA GRAS status simplifies approval for food applications but still mandates separate filings for pharmaceutical and cosmetic uses.

Emerging markets such as Brazil and Southeast Asia lack harmonized standards—Brazil’s ANVISA requires local bioequivalence studies for USP-grade sodium lactate. At the same time, some ASEAN countries have no clear guidelines, creating uncertainty for exporters. Labeling mandates also vary: the U.K. requires explicit declaration of “lactic acid salts,” potentially confusing consumers, whereas Germany allows the umbrella term “preservative system.” These divergent requirements drive up administrative and legal costs, particularly for companies operating globally. Non-compliance risks include product recalls and fines up to €500,000 in the EU. Consequently, regulatory complexity deters small and mid-sized enterprises from scaling internationally, constraining market growth outside major regions.

Opportunity - Growth in Emerging Regional Bioproduction Hubs

Asia Pacific emerges as a new bioproduction hub with China and India leading in lactic acid capacity expansions. In 2024, China added 150,000 tons of fermentation capacity, representing a 20% increase, while India’s government allocated US$50 million in grants for biotech infrastructure. These initiatives aim to localize feedstock processing and reduce reliance on European and North American lactic acid imports. Southeast Asian countries-Thailand and Vietnam-are forming public-private partnerships to establish integrated lactic acid-to-sodium lactate facilities, driven by lower labor costs and favorable tax incentives.

Such localization reduces logistics costs by up to 30% and mitigates raw material price volatility. For global players, joint ventures with regional producers offer access to high-growth domestic markets, enabling co-development of application-specific grades. Additionally, local production can facilitate faster regulatory approvals under national standards. As food and pharmaceutical consumption in emerging economies grows at over 10% CAGR, capacity expansions in bioproduction hubs present a strategic opportunity to capture market share and drive down unit costs.

Innovative Formulations and Niche Applications

Technological advancements in encapsulation and delivery systems present significant opportunities for sodium lactate. Microencapsulation techniques, recently commercialized by Galactic S.A., enable controlled release of sodium lactate in food and cosmetic formulations, enhancing preservative efficacy while minimizing flavor impact. Early trials indicate microencapsulated sodium lactate reduces microbial growth by 40% more effectively than its liquid counterpart. In pharmaceuticals, nanoparticle-based delivery systems are under investigation for targeted pH buffering in intravenous therapies, potentially improving patient outcomes in patients with metabolic acidosis.

The introduction of powder sodium lactate grades tailored for high-temperature processing expands applicability in bakery and extrusion-based snack production, where liquid salts are less practical. Furthermore, research into conjugating sodium lactate with antimicrobial peptides could create hybrid preservatives with synergistic activity. These innovations command premium pricing-up to 20% above standard grades-and open new revenue streams in high-value markets. Companies investing in R&D for specialized formulations can differentiate their portfolios and capitalize on the growing demand for advanced functional ingredients. Category-wise Insights

Category-wise Insights

Grade Analysis

Among Food Grade, Pharmaceutical/USP Grade, and Industrial Grade, Food Grade (FCC-certified) holds the leading share at 42% owing to heavy utilization as a preservative in processed meats, dairy, and bakery products. Regulatory endorsements and consumer demand for clean-label products support adoption. The robust food processing industry in North America and Europe further cements Food Grade dominance.

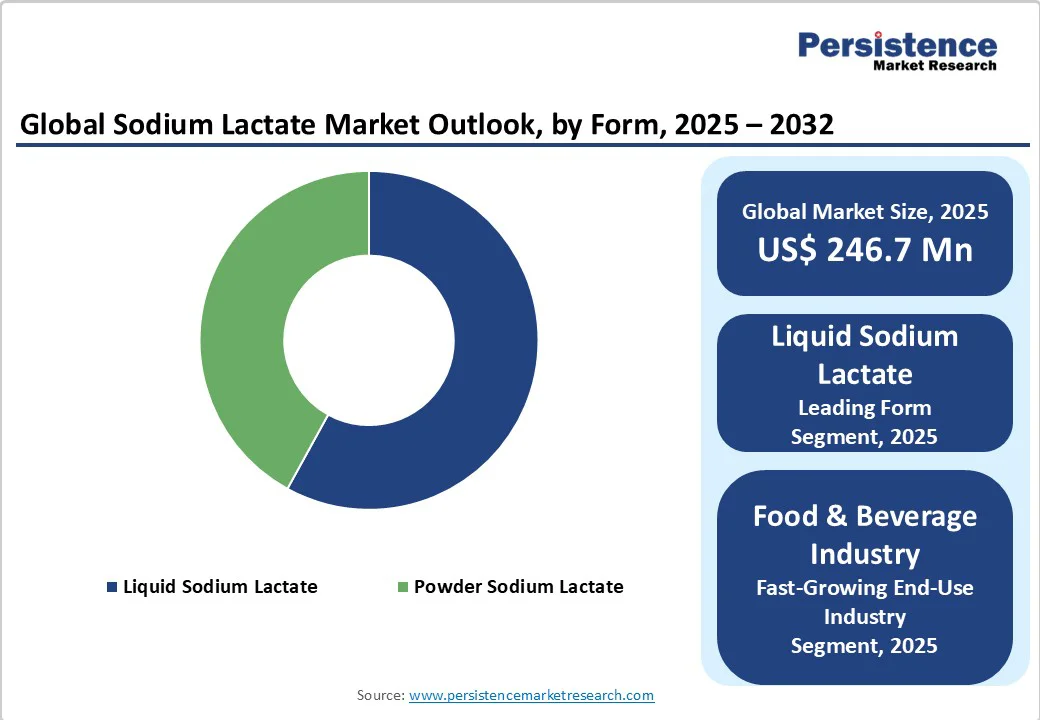

Form Analysis

Between Powder Sodium Lactate and Liquid Sodium Lactate, the Liquid form holds a 58% share due to its ease of incorporation into wet formulations across food, cosmetics, and pharmaceutical applications. Liquid formulations offer uniform distribution and lower processing costs, making them preferred in high-throughput manufacturing settings.

Packaging Type Analysis

In Bottles and Small Containers (≤5 L), Drums (25–200 L), Intermediate Bulk Containers (IBCs), and Bulk Tankers, Drums (25–200 L) lead with 36% share, balancing manageable handling for mid-scale processors and cost-effectiveness. Drums cater to both regional distributors and end users who require intermediate volumes without bulk tanker infrastructure.

Application Analysis

Within Preservative and Antimicrobial Agent, pH Regulator and Buffering Agent, Humectant and Moisturizing Agent, Flavoring and Acidity Regulator, Bulking and Emulsifying Agent, and Other, the Preservative and Antimicrobial Agent segment accounts for 45% share, driven by stringent shelf-life requirements and zero-chemical label trends in food and beverage. Its dual role of preservation and safety enhancement underpins this leadership.

Industry Analysis

Across the Food & Beverage Industry, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Construction & Building Materials, Chemical & Industrial Applications, and Others, the Food & Beverage Industry dominates with a 48% share. High-volume consumption of sodium lactate as a preservative and flavor stabilizer in meat and baked goods cements its top position.

Regional Insights

North America Sodium Lactate Market Trends

The United States leads the North American market, driven by robust food processing and stringent FDA regulations that promote the use of safe preservatives. Recent developments in clean-label mandates by major food retailers have accelerated the adoption of sodium lactate, with usage in deli meats increasing by 9% year-on-year.

Canada’s growing cosmetic sector has also embraced sodium lactate for its skin-hydrating properties, contributing to increased imports. Partnerships between bioprocessing firms and corn-syrup producers aim to localize lactic acid production, reducing supply chain risks and supporting regional price stability.

Europe Sodium Lactate Market Trends

Germany, the U.K., France, and Spain collectively account for the majority of European demand. The EU’s REACH regulation reaffirmation of sodium lactate’s safety has streamlined approvals across member states, enabling harmonized labeling and easier cross-border trade.

In France, dairy processors have increased sodium lactate usage by 7% to inhibit spoilage in soft cheeses. The U.K.’s personal care industry is leveraging sodium lactate in vegan formulations, aligning with sustainability targets and driving growth in the cosmetic segment.

Asia Pacific Sodium Lactate Trends

China has emerged as the fastest-growing market, supported by government incentives for biotechnology projects and rising domestic demand for processed foods. Local lactic acid manufacturers expanded capacity by 20% in 2024 to meet demand from the food and pharmaceutical sectors.

India’s pharmaceutical industry, the world’s third-largest, has increased adoption of sodium lactate in injectable formulations, boosting the Pharmaceutical/USP Grade segment by 10%. ASEAN countries are also investing in fermentation infrastructure, offering competitive cost advantages for export-oriented production.

Competitive Landscape

The global sodium lactate market is moderately consolidated, with top players holding approximately 55% share. Leading companies focus on capacity expansions, backward integration into lactic acid production, and R&D in specialized grades. Key differentiators include purity levels, regulatory certifications, and sustainable sourcing. Emerging players are exploring biorefinery partnerships and proprietary fermentation strains to enhance yield and reduce production costs.

Key Market Developments

- In March 2025, Corbion N.V. inaugurated a new fermentation plant in Thailand to boost supply in Asia Pacific.

- In October 2024, Galactic S.A. launched food-grade microencapsulated sodium lactate for controlled-release preservation.

- In June 2024, Merck KGaA expanded its USP-grade production facility in Germany to support pharmaceutical demand.

Companies Covered in Sodium Lactate Market

- Jungbunzlauer Suisse AG

- Hefei TNJ Chemical Industry Co., Ltd.

- Foodchem International Corporation

- Luoyang Longmen Pharmaceutical Co., Ltd.

- Shandong Baisheng Biotechnology Co., Ltd.

- Henan Jindan Lactic Acid Technology Co., Ltd.

- Loba Chemie Pvt. Ltd.

- Dr. Paul Lohmann GmbH & Co. KGaA

- JIAAN BIOTECH

- Qingdao Great Biological Engineering Co., Ltd.

- Corbion N.V.

- Galactic S.A.

- Merck KGaA

- Jindan Lactic Acid Technology Co., Ltd

- Cargill

Frequently Asked Questions

The global sodium lactate market is likely to be valued at US$ 246.7 Million in 2025.

Rising clean-label trends and regulatory mandates for safe preservatives have fueled a 60% increase in sodium lactate usage as an antimicrobial agent.

The Preservative and Antimicrobial Agent segment dominates with 45% share, driven by shelf-life extension needs.

North America leads due to advanced food processing infrastructure and stringent regulatory approvals.

Development of powder sodium lactate for specialty controlled-release applications presents significant growth potential.

Corbion N.V., Galactic S.A., and Merck KGaA are leading the market with integrated production capabilities and R&D focus.