- Inks, Coatings, Adhesives & Sealants (ICAS)

- Screen Printing Mesh Market

Screen Printing Mesh Market Size, Share, and Growth Forecast 2026 - 2033

Screen Printing Mesh Market by Material (Polyarylate, Polyester, Nylon, Steel), Filament Type (Mono, Multi, Other), Mesh Count (Below 80 TPI, 80-110 TPI, 110-220 TPI, 220-305 TPI, Above 305 TPI), Substrate (Metal, Plastic, Fabric, Glass, Paper & Paperboard), End-use Industry (Textile, Packaging, Glass & Ceramics, Electronics & Electrical, Advertising & Marketing), and Regional Analysis for 2026 - 2033

Screen Printing Mesh Market Size and Trend Analysis

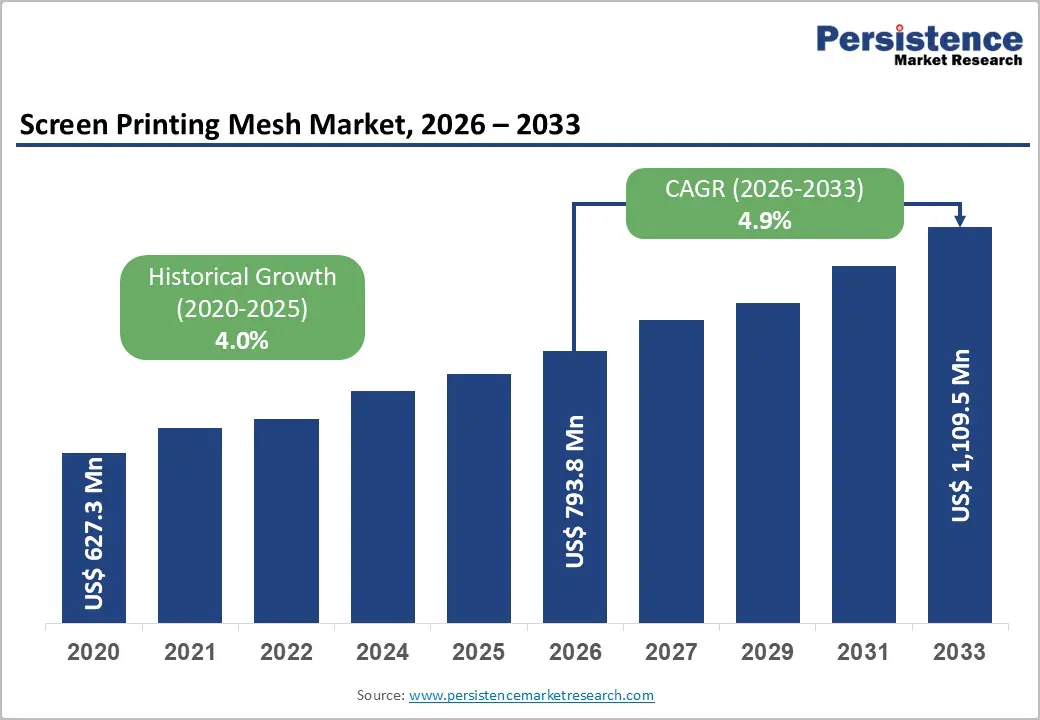

The global screen printing mesh market size is supposed to be valued at US$ 793.8 Mn in 2026 and is projected to reach US$ 1,109.5 Mn by 2033, growing at a CAGR of 4.9% between 2026 and 2033.

The market growth is primarily driven by the accelerating demand for customized and high-quality printing across textiles, electronics, and packaging industries. The shift toward digitalization in printing operations and the integration of automation technologies are enhancing operational efficiency and reducing wastage. The screen printing technique's proven cost-effectiveness for large-volume production, combined with its superior durability and vibrancy compared to alternative printing methods, continues to sustain robust demand across established and emerging markets.

Key Market Highlights

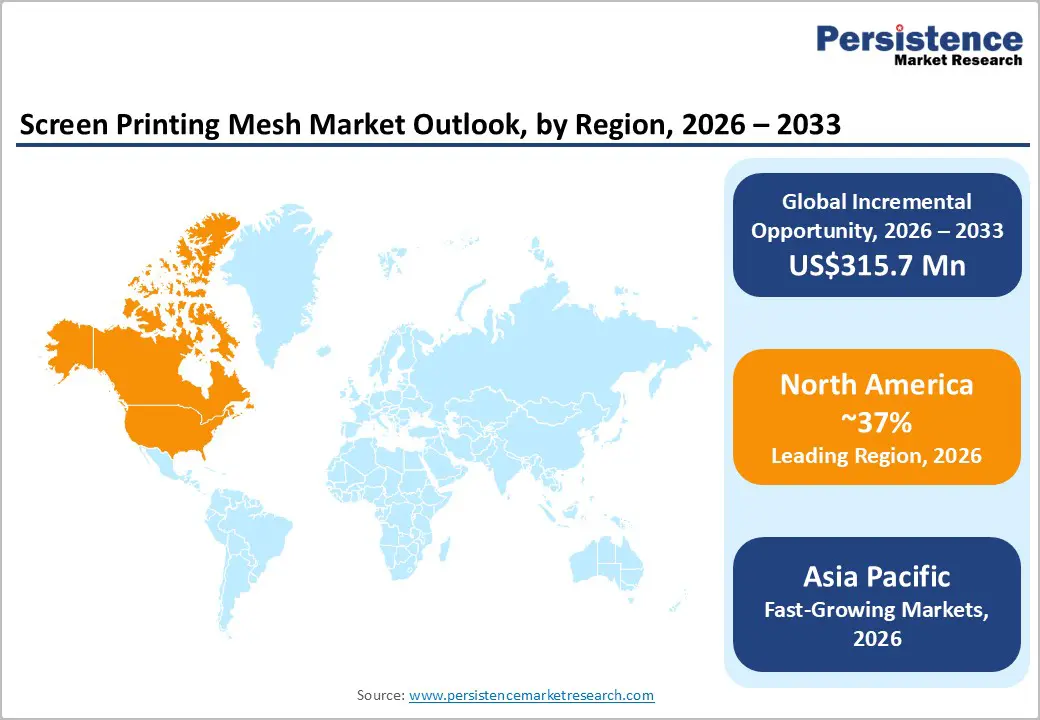

- Regional Leader: North America dominates the screen printing mesh market with 37% market share, driven by strong manufacturing infrastructure, technological innovation, and robust demand from textile, electronics, and packaging sectors, supporting sustained market growth through premium application focus.

- Fastest Growing Region: Asia Pacific experiences accelerated expansion, propelled by rapid industrialization, expanding textile manufacturing capacity, and a booming e-commerce sector generating substantial demand for customized apparel and decorative products.

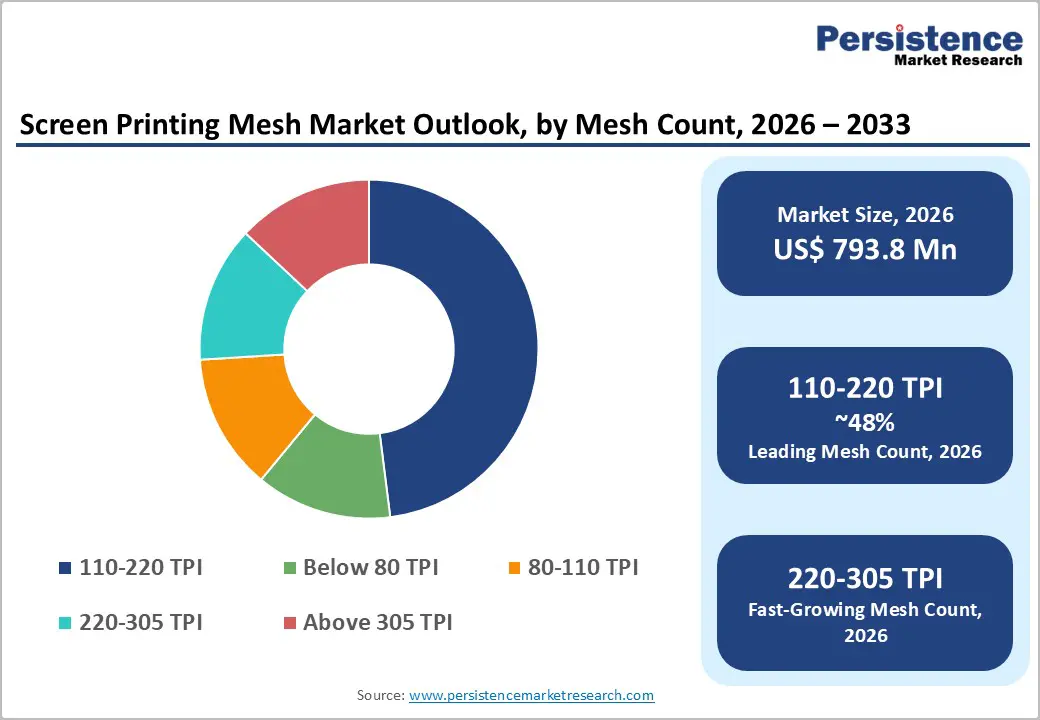

- Leading Segment: The 110-220 TPI mesh count segment dominates market demand, capturing approximately 48% market share due to its exceptional versatility in textile printing, promotional products, and moderate-detail graphic work.

- Fastest Growing Segment: The 220-305 TPI segments represent the fastest-growing mesh count categories, experiencing accelerated demand in electronics, fine-line printing, photographic halftones, and printed circuit board applications.

- Key Market Opportunity: Sustainability-driven innovations and eco-friendly mesh solutions present substantial market opportunities, including the development of recycled polyester meshes, water-based ink systems, and energy-efficient curing technologies.

| Key Insights | Details |

|---|---|

|

Screen Printing Mesh Size (2026E) |

US$ 793.8 Mn |

|

Market Value Forecast (2033F) |

US$ 1,109.5 Mn |

|

Projected Growth CAGR (2026-2033) |

4.9% |

|

Historical Market Growth (2020-2025) |

4.0% |

Market Dynamics

Market Growth Drivers

Rising Demand for Customization and Personalization

The global screen printing mesh market is experiencing significant growth, primarily driven by the rising demand for customized and personalized products across consumer and commercial sectors. Organizations and individuals increasingly favor branded apparel and promotional items that convey identity and corporate values.

The custom t-shirt printing segment alone is projected to grow at a CAGR of 11.5% between 2025 and 2030, with the commercial segment contributing 56% of revenue in 2024, largely due to corporate branding and event merchandise. This trend extends to promotional goods and specialty items across diverse industries. To meet these requirements, manufacturers are adopting advanced mesh technologies that ensure precise color registration and fine-detail reproduction. Additionally, e-commerce expansion, particularly in emerging markets such as India, has broadened access to personalized printing services globally.

Electronics and Functional Printing Expansion

The rapid growth of printed electronics and functional printing applications is a major driver of market expansion. In 2025, screen printing is expected to account for 41% of printed electronics production technologies, owing to its capability to deposit thick layers of functional materials with exceptional precision and consistency. This method is widely utilized in the manufacturing of printed circuit boards (PCBs), flexible electronics, RFID antennas, and photovoltaic modules.

Recent advancements in screen printing mesh design include improved dimensional stability, enhanced tension control, and specialized surface treatments that deliver superior stencil performance and extended screen life. The introduction of low-elongation polyester meshes and hybrid material combinations has optimized high-speed printing operations across electronics, automotive, and medical device sectors. These innovations enable the production of finer mesh counts exceeding 305 TPI, supporting intricate components such as PCBs, RFID tags, and flexible electronic displays.

Market Restraints

Competition from Alternative Printing Technologies

The screen printing mesh market is encountering growing competitive pressure from alternative printing technologies, notably direct-to-garment (DTG), direct-to-film (DTF), and digital printing. These methods offer distinct advantages for short-run customization and rapid turnaround, enabling them to capture approximately 44% of the custom t-shirt printing segment and challenge the dominance of traditional screen printing.

Digital printing, in particular, eliminates stencil preparation and significantly reduces setup time, making it highly appealing for businesses seeking flexibility and quick delivery. Despite these challenges, screen printing retains key advantages, including cost efficiency for large-volume production, superior color vibrancy on dark fabrics, and exceptional durability of printed designs, which continue to mitigate competitive pressures.

Raw Material Price Volatility and Environmental Regulations

The use of synthetic mesh materials, particularly polyester and nylon, poses significant environmental challenges that increasingly restrict market growth. These non-biodegradable materials contribute to plastic waste, attracting heightened scrutiny from regulatory authorities and consumer advocacy groups. The European Union’s Ecodesign for Sustainable Products Regulation (ESPR), effective July 2024, mandates product designs that prioritize durability, repairability, and recyclability, compelling manufacturers to reassess material compositions and production processes.

Furthermore, the Corporate Sustainability Reporting Directive (CSRD) requires companies with over 500 employees to disclose environmental impacts, adding compliance costs and operational burdens. These stringent regulations have driven substantial research and development investments in eco-friendly alternatives, diverting resources from expansion initiatives.

Market Opportunities

Sustainability-Driven Innovation and Eco-Friendly Solutions

The screen printing mesh industry presents a significant opportunity through the development and adoption of sustainable solutions. Growing emphasis on water-based inks, energy-efficient processes, and material recycling is reshaping market dynamics. Regulatory mandates and rising consumer demand for eco-friendly products are expected to drive a 20% increase in sustainable practices over the next decade. Manufacturers are investing in bio-based mesh materials, recycled polyester alternatives, and meshes compatible with water-based inks, alongside closed-loop water filtration systems and biodegradable emulsion removers.

The transition toward sustainability offers substantial potential for companies innovating in recycled meshes, biodegradable materials, and energy-efficient coating technologies. As environmental awareness and corporate sustainability commitments intensify, demand for eco-certified screen printing meshes is projected to accelerate, enabling differentiation and access to premium market segments.

High-Precision Applications in Electronics and Industrial Manufacturing

The rapid evolution of semiconductor manufacturing, microelectronics, and flexible electronics is creating significant opportunities for high-precision screen printing mesh producers. Mesh counts exceeding 305 TPI are increasingly essential for fine-line printing on printed circuit boards, display panels, and photovoltaic cells. The Asia-Pacific region, which accounted for 37.3% of the industrial screen printing market in 2025, is witnessing accelerated growth driven by robust electronics manufacturing in China, Japan, South Korea, and emerging economies such as Vietnam and India.

Furthermore, the printed electronics market, projected to grow at a CAGR of 10.4% through 2035, is fueling demand for specialized mesh products offering superior tensile strength, dimensional stability, and chemical resistance. Manufacturers developing advanced high-tension stainless steel meshes with exceptional precision and durability are well-positioned to capture substantial opportunities in this high-growth segment.

Category-wise Insights

Material Analysis

Polyester remains the dominant material in the screen printing mesh market, accounting for approximately 55% of the total share due to its optimal combination of tensile strength, moderate elasticity, and superior tension stability. Polyester monofilament mesh is widely regarded as the industry standard for apparel, textile, and graphic printing applications, offering consistent thread diameters, smooth surface finishes, reliable emulsion coating, and cost-effectiveness compared to alternatives. Its versatility supports a broad range of mesh counts, from plain weaves to highly specialized configurations, enabling applications from heavy ink deposits to fine halftone printing.

Compatibility with modern automatic presses and high-speed production lines further reinforces polyester’s leadership. Meanwhile, nylon and stainless steel segments are gaining traction for specialized uses, with stainless steel increasingly preferred for high-precision electronics, semiconductor manufacturing, and applications requiring exceptional dimensional accuracy and chemical resistance.

Filament Type Analysis

The monofilament segment accounts for approximately 72% of the screen printing mesh market, making it the dominant filament type. Monofilament threads are single, continuous filaments woven into fabric, offering superior properties such as uniform pore geometry, predictable ink flow, excellent tension retention, and non-adhesive surfaces that simplify emulsion coating and stencil edge definition. Their smooth structure minimizes particle adhesion during printing, ensuring consistent ink deposits and image quality over long production runs.

Monofilament polyester mesh remains the preferred choice for textile, apparel, and general-purpose printing due to its versatility and reliability. In contrast, multifilament meshes, composed of multiple fine fibers twisted together, provide enhanced flexibility and particle retention, making them suitable for specialty applications requiring conformity to irregular surfaces and for filtration processes demanding fine particle capture.

Mesh Count Analysis

The 110–220 TPI mesh count segment dominates the market, accounting for approximately 48% share due to its versatility across textile printing, promotional products, moderate-detail graphics, and industrial applications requiring balanced ink deposition and image clarity. Within this range, 110 TPI serves as the industry standard for general-purpose printing, while 156 and 196 TPI meshes are increasingly preferred for greater detail.

The 80–110 TPI segment supports heavy ink deposits, metallic inks, and thick-film printing for athletic wear and specialty materials. High-precision categories, including 220–305 TPI and above 305 TPI, collectively represent around 20% share and exhibit the fastest growth, driven by demand in electronics, fine-line printing, photographic halftones, and PCB applications where resolution-critical performance is essential.

Substrate Analysis

The fabric segment holds the largest share of substrate utilization, accounting for approximately 42% of the market, driven by the screen printing mesh industry’s strong foundation in textiles and apparel. Key substrates include polyester, cotton, silk, and specialty synthetic fabrics, with screen printing delivering superior color vibrancy, durability, and unique effects such as puff and metallic finishes that are difficult to achieve with alternative methods. Demand continues to rise in fashion, promotional apparel, sportswear, and branded merchandise.

Plastic substrates cover rigid plastics, flexible polymers, and specialized materials for automotive components, electronics packaging, and industrial marking. Glass and ceramics serve decorative tableware, architectural glass, automotive glazing, and ceramic tiles. Screen printing’s ability to handle three-dimensional and irregular surfaces reinforces its preference.

End-Use Industry Analysis

The textile and apparel industry represents the largest end-use segment, accounting for approximately 38% of market share, driven by sustained demand for printed garments, fashion items, and branded apparel. Growth is supported by the rising custom t-shirt printing market and rising consumer preference for personalized, self-expressive clothing.

The packaging segment is fueled by increasing demand for printed labels, decorative packaging, and branding on corrugated cartons and flexible materials. Electronics and electrical applications are the fastest-growing segment, with a projected CAGR exceeding 6% through 2033, covering PCB legends, conductive ink printing, touchscreen components, and functional assemblies.

Regional Insights

North America Screen Printing Mesh Trends

North America maintains a mature and well-developed screen printing ecosystem, with 37% market share, supported by advanced manufacturing capabilities and strong demand across textiles, promotional products, and electronics sectors. The region is characterized by high automation adoption, stringent regulatory compliance, and established production practices. The U.S. leads the market, driven by significant demand for custom promotional products where screen printing offers cost-effective solutions for corporate branding and event merchandise.

Innovation in automated systems and integration with digital technologies is increasingly prevalent, with manufacturers adopting hybrid approaches that combine traditional screen printing with digital enhancements to optimize efficiency. Strict environmental regulations governing chemical usage and waste management are accelerating the adoption of water-based inks, LED UV curing systems, and sustainable mesh materials. Additionally, robust supply chain infrastructure and comprehensive technical support further strengthen the region’s competitive position.

Europe Screen Printing Mesh Trends

Europe is a key market for screen printing meshes, supported by strong manufacturing bases in Germany, France, Spain, and the U.K., serving diverse industrial applications. Germany, renowned for precision engineering and stringent quality standards, drives substantial demand for high-precision mesh products in electronics, automotive, and specialty sectors. European manufacturers emphasize sustainability and regulatory compliance, with growing adoption of eco-certified meshes, water-based inks, and waste reduction technologies.

Southern Europe’s textile and fashion industries continue to generate robust demand, while the region’s established glass and ceramics sector sustains applications in decorative and functional products such as tableware, tiles, and architectural glass. Strategic partnerships and R&D investments underscore technological innovation and market consolidation, while well-defined regulatory frameworks and quality certifications enhance competitiveness and facilitate international trade.

Asia Pacific Screen Printing Mesh Trends

The Asia-Pacific region represents the fastest-growing region, with a market share of 35%. China leads as the largest producer, supported by its role as a global manufacturing hub with cost-efficient production and extensive textile exports. Smart manufacturing initiatives and rapid industrialization further accelerate adoption. India is projected to grow at a CAGR of 6.3% through 2035, driven by an expanding textile sector, rising demand for customized apparel, and e-commerce growth requiring printed packaging.

Japan and South Korea focus on high-precision applications such as PCBs, display panels, and flexible electronics. Competitive advantages stem from low labor costs, robust infrastructure, and government programs like “Make in India.” Additionally, Southeast Asian nations, including Vietnam, Thailand, and Indonesia, are increasingly integrated into apparel and electronics supply chains, fueling regional demand.

Competitive Landscape

The screen printing mesh market is moderately consolidated, featuring a balanced mix of global leaders and regional players. The top five companies collectively hold approximately 44% of the market, reflecting a competitive environment with opportunities for both established manufacturers and emerging entrants. Leading firms such as Sefar AG, NBC Meshtec, Saati S.p.A., Asada Mesh, and Haver & Boecker OHG leverage extensive manufacturing capabilities, global distribution networks, and advanced R&D investments to sustain their competitive edge. Differentiation is achieved through product innovation, specialized mesh designs, superior quality standards, and comprehensive technical support. Market growth is further driven by technological advancements, including high-tension mesh development, nanotechnology integration, and sustainability initiatives. Vertical integration strategies, exemplified by Sefar’s acquisition of Monosuisse, strengthen value chain control. Additionally, emerging business models emphasize customization, rapid prototyping, and digital integration to meet evolving customer requirements.

Key Market Developments

- January 2024: Sefar AG Announces Strategic Partnership with Leading Textile Manufacturer to develop innovative printing solutions enhancing product quality and sustainability standards, demonstrating market emphasis on collaborative innovation and eco-friendly advancements.

- July 2025: Jiamei Screen Printing Technology participates in the Vietnam International Printing Packaging Exhibition 2025, showcasing the latest innovations in textile and industrial printing equipment, reflecting regional manufacturing expansion and technology transfer to emerging markets.

- September 2025: NBC Meshtec Inc. launches an advanced mesh product line featuring enhanced tensile strength and dimensional stability characteristics designed for precision electronics applications and high-end functional printing, reflecting market emphasis on specialized high-precision solutions.

Top Companies in Screen Printing Mesh

Sefar AG (Switzerland) is recognized as a global technology leader headquartered in Switzerland, with a legacy spanning 200 years in precision mesh manufacturing. The company maintains manufacturing facilities across 25 countries on 6 continents and demonstrates vertical integration through control of the entire value chain from raw materials to finished products. Sefar's competitive advantages include advanced weaving technologies, a comprehensive product portfolio serving diverse industries including electronics, filtration, and textiles, and substantial research and development investments in sustainable solutions.

NBC Meshtec Inc. (Tokyo, Japan) represents a Japanese market leader founded in 1934, specializing in high-definition mesh technologies utilizing synthetic and metal fibers. The company operates multiple subsidiaries and manufacturing facilities globally, including operations in the United States, China, Indonesia, Thailand, and Germany. NBC's market position is strengthened by ISO 9001 certification, specialized V-Screen™ technology featuring exceptional tensile strength and dimensional stability, and comprehensive service capabilities for electronics and thick-film applications.

Saati S.p.A. (Italy) is renowned for advanced synthetic meshes and screen printing solutions featuring innovative looms enabling rapid customization and superior dimensional stability. The company differentiates through advanced finishing techniques, sustainable production practices, and specialized mesh surface treatments, enhancing stencil performance and tension characteristics. Saati maintains a significant market presence, particularly in European and emerging markets, emphasizing product quality, innovation, and customer-centric solutions.

Companies Covered in Screen Printing Mesh Market

- Sefar AG

- NBC Meshtec Inc.

- Nippon Tokushu Fabric Inc.

- Nakanuma Art Screen Co., Ltd.

- Weisse & Eschrich GmbH & Co. KG

- Asada Mesh Co., Ltd.

- Maishi Manufacture (Group) Limited

- Saati S.p.A.

- Extris Srl

- Haver & Boecker OHG

- Shanghai Shangshai Bolting Cloth Manufacturing Co., Ltd

Frequently Asked Questions

The global screen printing mesh market is projected to reach US$ 1,109.5 Mn by 2033 from a 2026 valuation of US$ 793.8 Mn, representing a compound annual growth rate of 4.9% during this forecast period.

The market is primarily driven by rising demand for customization and personalized products across the apparel and promotional sectors, with the custom t-shirt printing market growing at 11.5% CAGR through 2030.

The 110-220 TPI mesh count segment dominates with approximately 48% market share, serving diverse applications including textile printing, promotional products, and moderate-detail graphic work.

North America leads the market with approximately 35% market share, supported by mature manufacturing infrastructure, technological innovation, and substantial demand from textile, electronics, and packaging sectors.

The printed electronics sector presents the most transformative growth opportunity, where screen printing technology commands 41% market share for producing advanced components, including printed sensors, photovoltaic modules, flexible displays, and wearable electronics.