- Biotechnology

- Saliva-based Screening Market

Saliva-based Screening Market Size, Share, and Growth Forecast 2026 - 2033

Saliva-based Screening Market by Product (Saliva collection kits, Detection kits (PCR, rapid tests), Nucleic acid purification kits), by Test (PCR-based tests, RT-qPCR, Lateral flow assays (strip tests), Biosensors / NGS-based tests), by Application (Infectious disease detection, Genetic/genomic testing, Hormone testing, Drug & alcohol testing, Others), by End User (Hospitals & clinics, Diagnostic labs, Research & academic institutions, Pharma / CROs, Home users / direct-to-consumer), by Regional Analysis, 2026-2033

Saliva-Based Screening Market Size and Trend Analysis

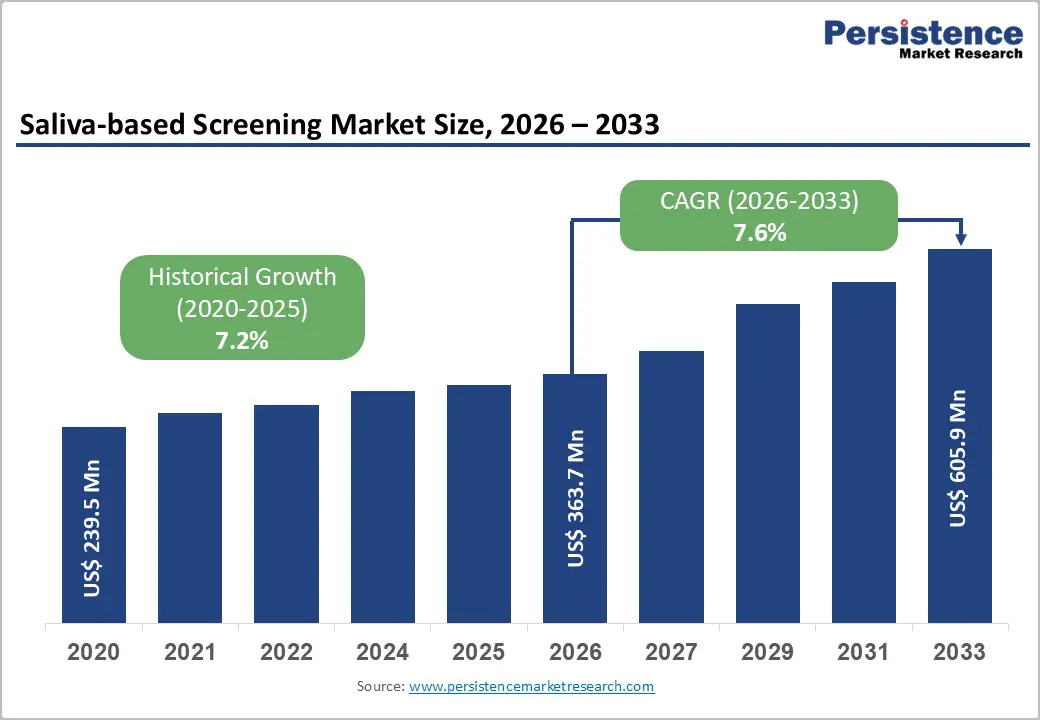

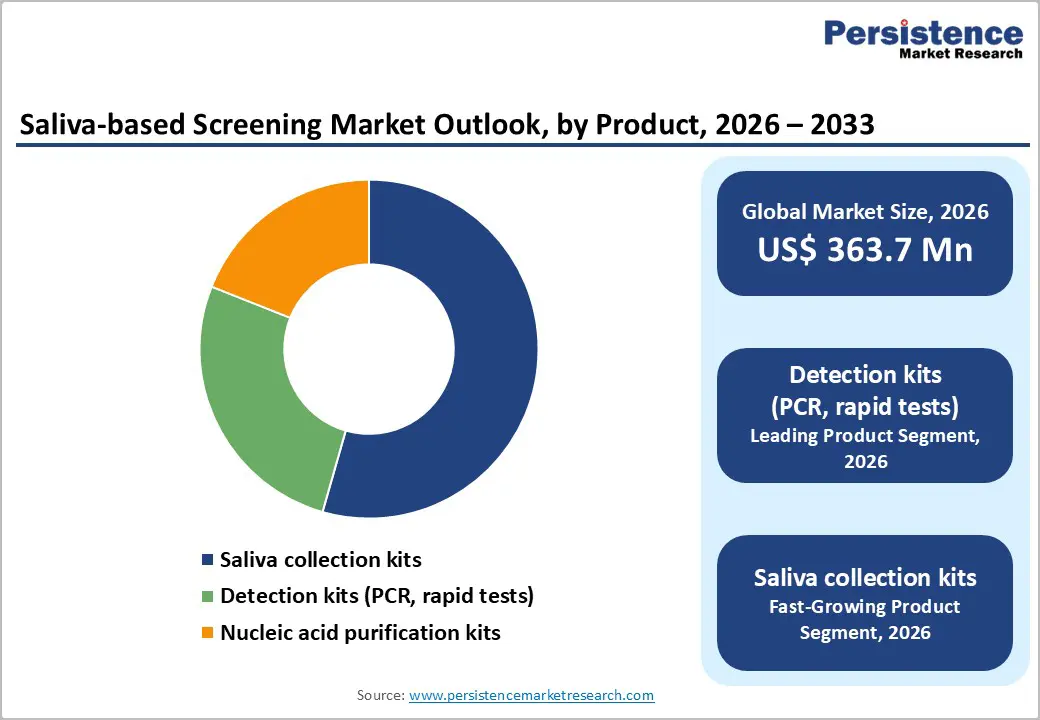

The global Saliva-based Screening Market size is expected to be valued at US$ 363.7 million in 2026 and projected to reach US$ 605.9 million by 2033, growing at a CAGR of 7.6% between 2026 and 2033. Rising demand for non-invasive diagnostics drives this growth, supported by advancements in PCR technologies and saliva's high biomarker correlation with blood. The COVID-19 pandemic accelerated adoption, with FDA approvals for saliva tests demonstrating up to 94% accuracy in viral detection, boosting scalability for mass screening.

Key Market highlights

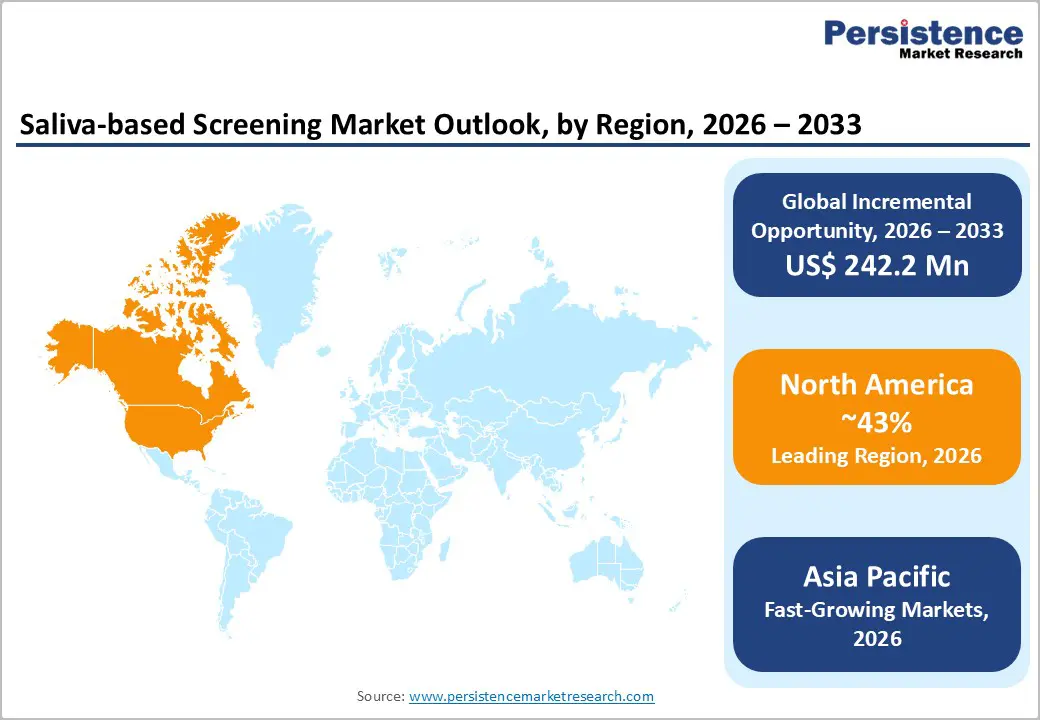

- Asia Pacific dominates with 43% share in 2025, driven by manufacturing hubs and population-scale screening needs.

- Latin America emerges fastest-growing, boosted by Brazil's non-invasive policies for viral detection.

- Detection kits (PCR, rapid tests) lead products at 43% share, excelling in infectious accuracy.

- Saliva collection kits grow fastest, enabling home and POC scalability post-pandemic.

- POC biosensors offer key opportunity for rapid hormone and drug screening in emerging markets.

| Global Market Attributes | Key Insights |

|---|---|

| Saliva-based Screening Market Size (2026E) | US$ 363.7 million |

| Market Value Forecast (2033F) | US$ 605.9 million |

| Projected Growth CAGR(2026-2033) | 7.6% |

| Historical Market Growth (2020-2025) | 7.2% |

Market Dynamics

Non-Invasive Sample Collection

Non-invasive sample collection is a major growth driver for the saliva-based screening market, as it significantly improves patient comfort and compliance compared to blood draws or nasopharyngeal swabs. Saliva collection is painless, needle-free, and stress-free, making it especially suitable for children, elderly patients, and individuals with chronic conditions who require frequent testing. Unlike invasive procedures, saliva sampling can be performed without trained healthcare professionals, reducing dependency on hospital infrastructure and lowering overall testing costs. The ability to self-collect samples at home has further strengthened adoption, particularly during infectious disease outbreaks when minimizing physical contact is critical. Saliva-based testing also reduces the risk of exposure for healthcare workers, as it eliminates close contact during sample collection. This advantage became highly visible during the COVID-19 pandemic, accelerating acceptance among public health authorities and consumers. Additionally, saliva samples are easy to transport and store, supporting large-scale screening and surveillance programs. As healthcare systems increasingly emphasize patient-centric and decentralized testing models, the convenience and safety of non-invasive saliva collection continue to drive widespread adoption across diagnostic, monitoring, and preventive healthcare applications.

Technological Advancements in Detection

Technological advancements in detection methods have substantially strengthened the reliability and clinical acceptance of saliva-based screening. Innovations in PCR and RT-qPCR technologies have significantly improved the sensitivity and specificity of saliva tests, enabling performance levels comparable to traditional blood- or swab-based diagnostics. Enhanced reagents, optimized primers, and direct-to-PCR workflows have reduced processing time while maintaining high analytical accuracy. These advancements have expanded the use of saliva testing beyond infectious diseases into areas such as hormonal analysis, drug monitoring, and genetic screening. Improved biomarker detection techniques have demonstrated strong correlations between salivary and serum biomarker levels, reinforcing saliva as a viable diagnostic matrix. Regulatory approvals from agencies such as the FDA and EMA for saliva-based molecular tests have further validated these technologies and encouraged commercial adoption. Additionally, the integration of automation, multiplex testing, and rapid detection platforms has increased throughput and scalability for laboratories. As research continues to identify new salivary biomarkers and refine detection platforms, technological progress remains a key driver supporting long-term growth and broader clinical application of saliva-based screening solutions.

Market Restraints

Sample Variability and Sensitivity Issues

Sample variability is a key restraint limiting the widespread adoption of saliva-based screening. The composition of saliva can vary significantly between individuals and even within the same individual at different times of the day, influenced by factors such as diet, hydration levels, oral hygiene, smoking, and underlying oral health conditions. Variations in salivary flow rate and viscosity can affect sample volume and analyte concentration, leading to inconsistent test results. At low biomarker or viral load levels, these variations may reduce assay sensitivity, increasing the risk of false-negative outcomes. Studies have reported measurable discordance between saliva-based tests and nasopharyngeal swabs, particularly in early or asymptomatic infections where viral concentration is low. Additionally, saliva contains natural inhibitors such as mucins, food debris, and enzymes that can interfere with PCR amplification if not adequately controlled. The absence of standardized collection protocols and pre-analytical handling methods further complicates reproducibility, especially in decentralized or field testing environments, limiting reliability and clinical confidence.

Regulatory and Validation Hurdles

Regulatory and validation challenges present a significant barrier to the growth of the saliva-based screening market. Health authorities such as the FDA and EMA require extensive clinical validation to demonstrate that saliva-based assays consistently match or exceed the performance of established reference methods. Variability in test accuracy across symptomatic and asymptomatic populations often necessitates large, multi-center clinical trials, increasing development timelines and costs. These stringent requirements can delay product approvals and limit the rapid introduction of innovative saliva-based tests, particularly during public health emergencies. Furthermore, regulatory agencies often require robust evidence for analytical sensitivity, specificity, and reproducibility across diverse populations and use settings. For resource-limited laboratories, compliance with regulatory standards may require specialized equipment, trained personnel, and quality control systems, creating additional barriers to adoption. As a result, despite clear advantages such as non-invasive sampling, regulatory complexity and validation demands continue to slow market penetration and widespread clinical implementation.

Market Opportunities

Expansion in Point-of-Care Biosensors

The development and expansion of point-of-care (POC) biosensors represent a major growth opportunity for the saliva-based screening market. These devices allow rapid, on-site analysis of saliva samples, providing timely diagnostic results for infectious diseases, hormonal imbalances, and other health indicators. Innovations in microfluidics and lab-on-a-chip technologies have improved biomarker detection speed and sensitivity, making POC biosensors more reliable and scalable for diverse clinical and non-clinical settings. The COVID-19 pandemic further highlighted the need for decentralized testing solutions, driving adoption of saliva-based POC devices, particularly in remote and underserved areas where laboratory access is limited. Studies demonstrating up to 94% accuracy in RT-PCR saliva assays have bolstered confidence in these tools. Additionally, integration with artificial intelligence and digital health platforms enables real-time data analysis and personalized screening recommendations, enhancing patient engagement and compliance. With increasing consumer interest in home testing and self-monitoring, POC biosensors are positioned to capture high-growth segments and facilitate frequent, convenient, and non-invasive health monitoring worldwide.

Emerging Markets for Drug and Hormone Testing

Emerging markets present significant opportunities for saliva-based screening, particularly in drug and hormone testing applications. Increasing prevalence of substance abuse, workplace compliance testing, and roadside drug monitoring is driving demand for non-invasive, rapid saliva-based detection methods. Companies like OraSure have developed saliva kits that allow safe and convenient drug testing without blood draws or urine collection, reducing privacy concerns and improving compliance. Hormonal disorders, including thyroid imbalances and reproductive health issues, also create expanding demand for saliva-based assays that correlate strongly with serum levels. Policy shifts in regions such as Latin America, including Brazil’s approval of saliva-based SARS-CoV-2 testing, highlight regulatory openness and create pathways for saliva diagnostic adoption in other genetic, hormonal, and endocrine panels. Improved accessibility in underserved areas further fuels growth, as portable, easy-to-use saliva tests bypass infrastructure limitations. Combined with increasing awareness of the advantages of non-invasive testing, these trends support robust market expansion with strong CAGR potential in emerging geographies.

Category-wise Insights

Product Analysis

Detection kits, including PCR and rapid tests, are the leading product segment in the saliva-based screening market, capturing approximately 43% of the market share in 2025. Their dominance is driven by their direct diagnostic value, offering high sensitivity and accuracy in detecting viral pathogens from raw saliva. For instance, CDC data demonstrates that saliva-based tests achieve up to 94% accuracy for COVID-19, reinforcing confidence among healthcare providers and patients. Regulatory support, such as multiple FDA Emergency Use Authorizations (EUA), further validates the reliability of these detection kits for infectious disease testing. Compared to saliva collection kits or nucleic acid purification tools, detection kits deliver immediate actionable results, making them the preferred choice in clinical settings. This segment’s combination of proven performance, regulatory backing, and patient convenience underpins its market leadership and positions it for continued growth in both centralized and decentralized testing environments.

Test Analysis

PCR-based tests dominate the saliva-based screening landscape, maintaining a substantial market share in 2025 due to their superior sensitivity and specificity. Raw saliva samples, when processed via PCR, consistently demonstrate strong positive agreement with nasopharyngeal swabs, with studies reporting over 90% concordance. RT-qPCR validations provide low cycle threshold (Ct) values, indicating high viral load detection even in asymptomatic individuals, which is critical for early diagnosis and surveillance programs. The robustness of PCR-based methods allows their use across multiple infectious diseases, hormonal assays, and genetic testing, making them versatile for clinical laboratories. The high-throughput capability of PCR platforms further strengthens their adoption in large-scale testing initiatives. As technology continues to advance with optimized reagents and automated workflows, PCR-based saliva tests remain the benchmark for reliability, accuracy, and broad applicability, driving sustained preference in hospitals, diagnostic labs, and research institutions worldwide.

Application Analysis

Infectious disease detection remains the leading application for saliva-based screening, capturing a significant market share in 2025. The COVID-19 pandemic highlighted saliva’s utility for mass testing, enabling scalable, non-invasive, and accurate diagnostics with reported 94% accuracy per CDC guidelines. Saliva testing allows frequent sampling with minimal patient discomfort, supporting outbreak management and surveillance programs. Beyond COVID-19, saliva-based assays are being increasingly adopted for influenza, RSV, and other respiratory viruses, with WHO endorsements recognizing their role in public health initiatives. The non-invasive nature also facilitates testing in pediatric, elderly, and home-based settings, extending its reach to previously underserved populations. Combined with rapid deployment capabilities, ease of sample transport, and integration with point-of-care platforms, infectious disease detection continues to be the core driver of saliva-based applications, positioning the segment as a critical component in both routine screening and emergency response frameworks.

End User Analysis

Diagnostic laboratories lead the end-user segment for saliva-based screening, capturing the largest share in 2025. Their dominance is supported by high-throughput PCR processing capabilities, enabling rapid and large-scale testing for COVID-19 and other infectious diseases. Laboratories equipped with CLIA certifications and partnerships with hospitals and public health authorities ensure standardized quality control and regulatory compliance. The ability to process raw saliva directly with RT-PCR has demonstrated over 83% sensitivity, making labs the preferred choice for reliable diagnostic output. These facilities also benefit from integrated automation and advanced data management, facilitating quick turnaround times and efficient reporting. As demand for accurate and frequent testing grows, diagnostic labs remain at the forefront of adoption, leveraging their technical expertise and infrastructure to support large-scale surveillance, research applications, and emerging home-based and point-of-care testing solutions.

Regional Insights

North America Saliva-based Screening Market Trends and Insights

North America dominates the saliva-based screening market, driven by strong innovation and regulatory support. In the U.S., the FDA authorized SalivaDirect and issued multiple Emergency Use Authorizations (EUA) for SARS-CoV-2 saliva tests, enabling universities like Yale to implement large-scale mass testing. Regulatory backing has accelerated point-of-care adoption, especially for chronic disease monitoring. Private investments, alongside research funding from organizations like the NBA, have strengthened surveillance and diagnostic ecosystems. High healthcare infrastructure, advanced laboratories, and increasing awareness of non-invasive testing further support market growth. These factors collectively position North America as the leading region for saliva-based screening, both in technological development and market penetration.

Asia Pacific Saliva-based Screening Market Trends and Insights

Asia Pacific holds a significant 43% share of the global saliva-based screening market in 2025. China leads through large-scale manufacturing capabilities, producing cost-effective kits for both domestic and export markets. India drives growth via public health initiatives targeting tuberculosis and COVID-19 screening. Japan contributes through advanced innovation, leveraging next-generation sequencing (NGS) for genomic applications. ASEAN countries are adopting saliva tests to meet population-driven demand, benefiting from affordable kits and expanding healthcare access. Rising awareness of non-invasive diagnostics, government support, and growing investments in research and infrastructure collectively boost market adoption, making Asia Pacific a rapidly expanding and high-potential region in the global saliva-based screening market.

Competitive Landscape

Market Structure Analysis

The saliva-based screening market is highly competitive, driven by rapid technological advancements and increasing demand for non-invasive diagnostics. Companies focus on developing high-sensitivity PCR and rapid detection kits to meet regulatory standards and consumer expectations. Innovation in point-of-care devices, microfluidics, and AI-integrated diagnostics is intensifying, with emphasis on faster, accurate, and user-friendly solutions. Strategic partnerships, collaborations, and licensing agreements are common to expand geographic reach and product portfolios. Price competitiveness, scalability, and regulatory compliance are key differentiators, while ongoing R&D ensures new applications in infectious disease, hormone, and drug testing. Overall, market players compete through technology leadership, quality, and accessibility.

Key Market Developments

- In August 2025, Delhi-based Guttify, a gut health startup by Lifechart, launched of the country’s first saliva-based test for gut health the Gut Scan Kit. Designed specifically for Indian biology and lifestyle, the kit offered a non-invasive, at-home solution to assess gut health in just 24 hours, eliminating the need for complex lab visits or stool samples.?

Companies Covered in Saliva-based Screening Market

Thermo Fisher Scientific, Inc., Abbott Laboratories, OraSure Technologies, Inc., Quest Diagnostics Incorporated, Laboratory Corporation of America (LabCorp), Salimetrics, LLC, Neogen Corporation, Hologic, Inc., F. Hoffmann-La Roche Ltd, QIAGEN N.V., Oasis Diagnostics Corporation, Takara Bio, Inc.

Frequently Asked Questions

The market is expected to reach US$ 363.7 million in 2026.

Non-invasive collection boosts compliance, with 94% COVID-19 accuracy per CDC.

Asia Pacific with 43% share in 2025, via manufacturing and population screening.

POC biosensors for rapid infectious and hormone testing in high-growth regions.

Leaders include Thermo Fisher, Abbott, and OraSure driving PCR innovations.