- Rail

- Platform Screen Doors Market

Platform Screen Doors Market Size, Share, and Growth Forecast, 2025 - 2032

Platform Screen Doors Market by Product Type (Full Height, Semi Height and Half Height), by Station Type (New Metro Stations and Old Metro Stations), by Application (Metro Station, Airport and Bus Stop) and Regional Analysis for 2025 - 2032

Platform Screen Doors Market Size and Trends Analysis

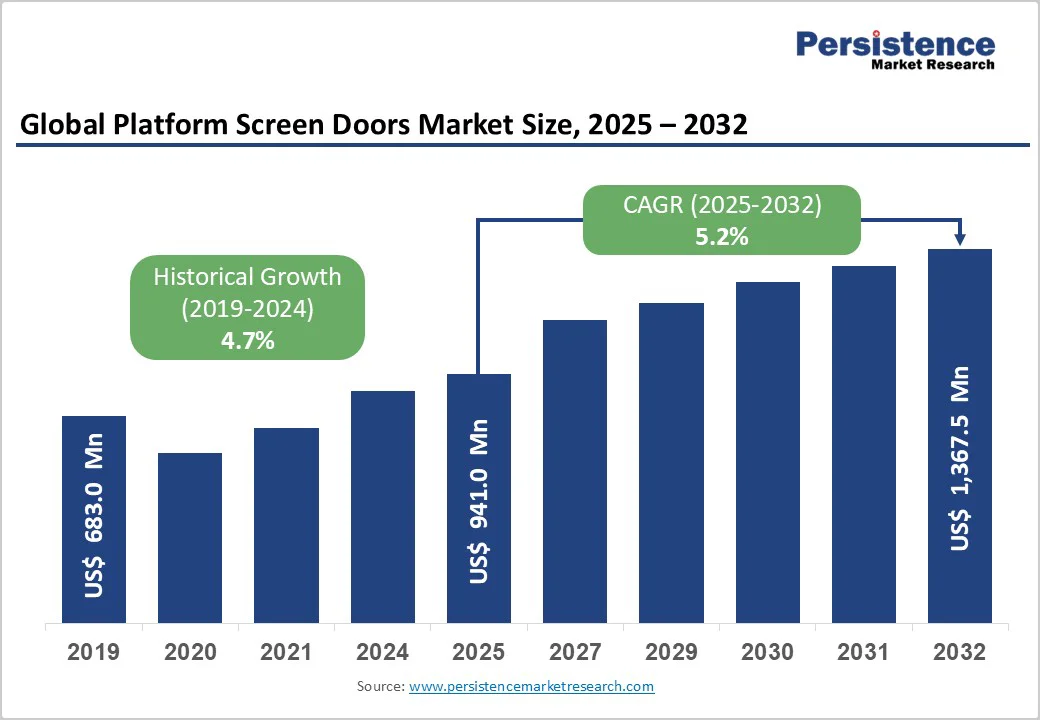

The global platform screen doors market size is likely to value at US$ 941.0 million in 2025 and is projected to reach US$ 1,367.5 million by 2032, growing at a CAGR of 5.2% between 2025 and 2032.

The market expansion is supported by technological advancements in automated door systems, growing investment in public transportation infrastructure, and rising passenger volumes necessitating efficient crowd management solutions across global transit networks. efficiency.

Key Industry Highlights:

- Station Development Dynamics: New Metro Stations account for 63.3% share through integrated design and construction approaches, with Old Metro Stations demonstrating the fastest growth supported by retrofit initiatives and safety compliance requirements.

- Application Market Evolution: Metro Stations maintain 37.5% market leadership through established transit network demand, while Airport applications achieve the fastest growth driven by passenger traffic increases and automated system adoption.

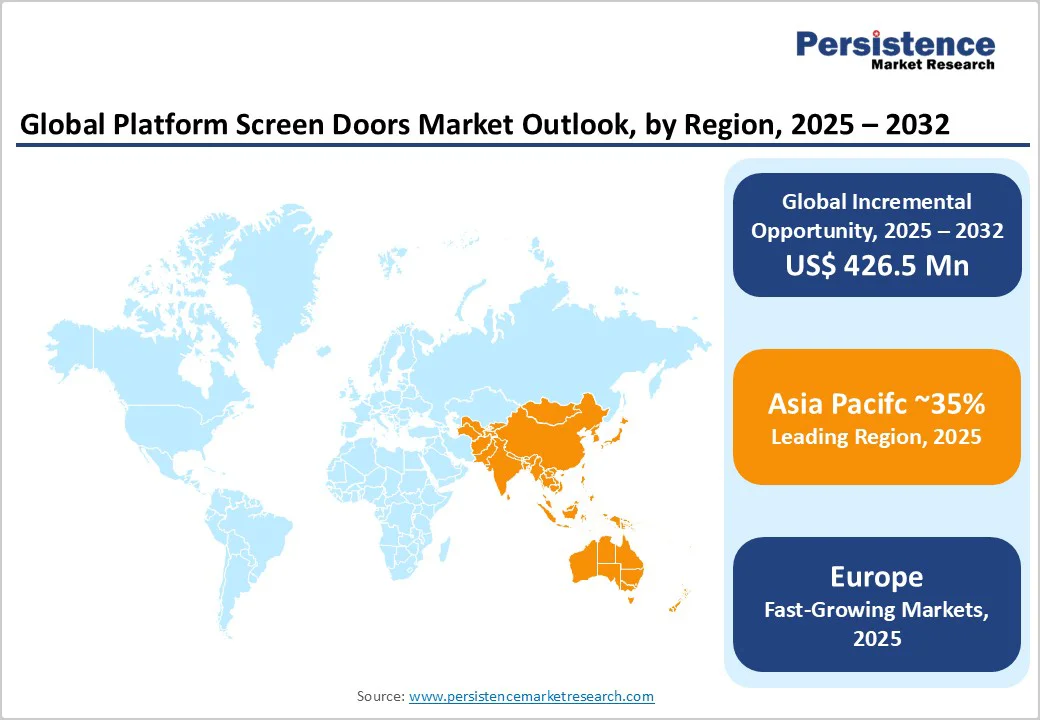

- Regional Growth Patterns: Asia Pacific dominates with 55% share valued at $518 million through massive infrastructure investment and rapid urbanization, while North America and Europe focus on modernization and safety compliance initiatives.

- Strategic Market Developments: Panasonic's advanced sensor technology launch, Sydney Metro's 288-door installation, and ZHUZHOU CRRC's smart maintenance platform demonstrate industry focus on innovation, large-scale deployment, and intelligent system integration.

- Technology Evolution: IoT connectivity, predictive maintenance capabilities, and smart transportation integration transform traditional platform screen doors into intelligent safety and operational management systems, creating premium market opportunities and comprehensive solution offerings.

| Key Insights | Details |

|---|---|

| Platform Screen Doors Market Size (2025E) | US$ 941.0 Mn |

| Market Value Forecast (2032F) | US$ 1,367.5Mn |

| Projected Growth (CAGR 2025 to 2032) | 5.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.7% |

Market Dynamics

Drivers - Accelerating Global Urbanization and Metro Network Expansion

Global urbanization trends create substantial demand for advanced transit safety systems, with the World Bank projecting that 68% of the global population will reside in urban areas by 2050. According to the International Association of Public Transport (UITP), over 28,000 new urban rail cars are expected to be introduced globally by 2025, directly driving platform screen door integration requirements.

China leads this expansion with over 3,500 metro stations already equipped with platform screen doors, while countries including India, Vietnam, and Mexico are establishing comprehensive metro networks requiring safety infrastructure.

The automation of metro systems, with over 60% of new urban rail lines being driverless, necessitates platform edge doors to ensure platform integrity and operational safety. Government infrastructure investment programs, including China's $1 trillion Belt and Road Initiative and India's Smart Cities Mission, create sustained demand for platform screen door installations across emerging markets.

Stringent Safety Regulations and Government Mandates

International safety standards and government regulations increasingly mandate platform screen door installations to prevent accidents and enhance passenger security.

The European Union Agency for Railways and the U.S. Federal Transit Administration implement strict safety standards, encouraging metro authorities worldwide to adopt platform screen doors as mandatory infrastructure components. According to industry data, platform screen doors can prevent up to 90% of platform-related accidents, including accidental falls and intentional access to tracks.

Government incentives supporting smart city initiatives and sustainable transportation solutions provide funding mechanisms for platform screen door projects, with over $50 billion allocated globally for urban transit safety improvements through 2030. Regulatory mandates for disability accessibility and enhanced passenger flow management further drive adoption, as platform screen doors facilitate controlled boarding and improved station efficiency.

Market Restraints - High Capital Investment and Installation Costs

Platform screen door installations require substantial upfront investment, with comprehensive full-height systems costing $200,000-$500,000 per platform depending on station configuration and technology requirements. Retrofitting existing transportation infrastructure creates additional complexity and expense, particularly for aging subway systems requiring structural modifications and electrical upgrades.

Maintenance and monitoring costs add ongoing operational expenses, including sensor calibration, door mechanism servicing, and integration with existing station management systems. The high manufacturing costs associated with specialized materials, precision engineering, and safety certification processes create price barriers for transit authorities in developing markets where budget constraints limit infrastructure investment capacity.

Integration Complexity and Technical Challenges

The complexity of integrating platform screen door systems with diverse existing transit infrastructures creates implementation challenges across different technological standards and operational requirements. Variations in train door configurations, platform dimensions, and electrical systems across metro networks necessitate customized solutions, increasing project complexity and delivery timelines.

Compatibility issues with legacy signaling systems, communication protocols, and safety management platforms require extensive testing and validation processes. Technical challenges, including electromagnetic interference, structural load requirements, and emergency override systems demand specialized engineering expertise and can extend installation schedules by 6-12 months beyond planned completion dates.

Market Opportunities - Emerging Market Infrastructure Development

Developing economies in Asia-Pacific, Latin America, and Middle East regions present substantial growth opportunities, with collective metro system expansion projects valued at over $200 billion through 2030.

Countries including India, Indonesia, and Brazil are implementing comprehensive urban transit programs requiring modern safety infrastructure including platform screen doors. Government-backed financing programs and international development bank funding create favorable conditions for platform screen door adoption in emerging markets experiencing rapid urbanization.

The expanding middle class in developing regions, combined with government emphasis on public transportation development, generates sustained demand for advanced transit safety systems. Market penetration rates for platform screen doors remain below 25% in many emerging economies, representing significant expansion potential for manufacturers and system integrators.

Airport and Multi-Modal Transportation Applications

The aviation sector represents the fastest-growing application segment, with airports implementing platform screen doors for automated people mover systems, gate boarding bridges, and baggage handling facilities. Global air passenger traffic growth, projected at 4.3% annually through 2030, drives demand for advanced passenger flow management and safety systems at airports worldwide.

Bus rapid transit (BRT) systems and light rail networks increasingly adopt platform screen door technologies to enhance safety and operational efficiency, creating new market segments beyond traditional metro applications. The integration of platform screen doors with smart building management systems enables comprehensive facility automation and energy optimization across diverse transportation hubs.

Category-wise Analysis

Product Type Analysis - Full Height Systems Lead While Semi Height Designs Drive Flexible Growth

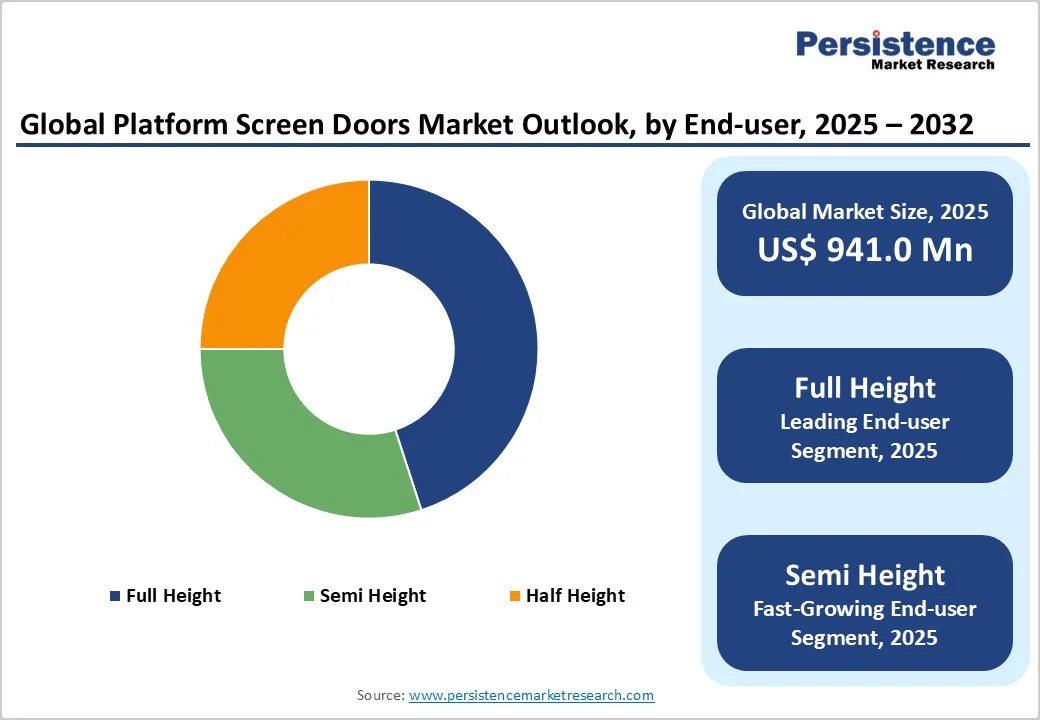

Full height platform screen doors dominate the market with 47.2% share, driven by superior passenger safety, complete environmental separation, and energy efficiency benefits. Extending from platform floor to ceiling, these systems offer full protection against accidents, unauthorized access, and external disturbances while supporting precise climate control and operational sustainability. The segment’s growth is reinforced by proven reliability and widespread adoption in high-traffic metro and rail stations.

Semi height platform screen doors represent the fastest-growing product segment, offering strong safety performance with lower capital costs and easier installation. Their modular, lightweight designs enable cost-effective deployment in retrofit projects and smaller stations. Technological advancements in sensors, automation, and system integration further enhance performance, flexibility, and adaptability across varied transit infrastructure needs.

Station Type Analysis - New Metro Stations Lead While Retrofit Projects Drive Accelerated Growth

New metro stations account for 63.3% of the market share, driven by the integration of platform screen doors as standard infrastructure in modern transit development. Incorporating these systems during initial design ensures seamless alignment with architectural, electrical, and operational systems-enhancing passenger safety, energy efficiency, and station automation. The segment benefits from global metro expansion projects emphasizing smart, safe, and sustainable urban mobility.

Old metro stations represent the fastest-growing segment, fueled by large-scale retrofit programs and modernization initiatives in established networks. Governments and transit authorities increasingly mandate platform screen door installations to upgrade safety, accessibility, and operational reliability. Despite technical integration challenges, retrofit projects create strong market opportunities supported by regulatory compliance requirements and funding for transit infrastructure renewal.

Application Analysis - Metro Stations Lead, While Airports Drive Rapid Expansion

Metro stations hold 37.5% market share, serving as the primary application segment for platform screen door technology across global urban rail networks. These systems are integral to subway and underground operations, ensuring passenger safety, minimizing track incidents, and improving energy efficiency. The segment benefits from standardized installation practices, mature supply chains, and integration with automated train control systems supporting smart city infrastructure development.

Airports represent the fastest-growing application segment, driven by rising air passenger volumes and the growing adoption of automated people mover systems. Platform screen doors in airport environments enhance passenger safety, streamline boarding, and support advanced crowd management. Integration with building automation, access control, and security systems combined with a focus on contactless and efficient transit drives significant growth potential in aviation infrastructure.

Regional Market Insights

North America Focuses on Modernization and Safety Compliance

North America accounts for around 20% of the global platform screen doors market, valued at USD 188 million in 2025 and expected to reach USD 273 million by 2032.

The United States leads regional demand, driven by modernization of aging subway systems in cities such as New York, Washington D.C., and San Francisco. These initiatives emphasize passenger safety, ADA compliance, and operational efficiency. The region benefits from a mature supplier base, strong regulatory frameworks, and active infrastructure investments.

Major projects, including New York MTA’s pilot installations and Toronto TTC’s Line 1 upgrades, sustain long-term demand. Strict safety, accessibility, and environmental mandates by the Federal Transit Administration support adoption of advanced, energy-efficient screen door systems, encouraging innovation and technology integration across North American transit networks.

Europe Leads in Safety, Modernization, and Smart Transit Integration

Europe holds about 25% of the global platform screen doors market, valued at USD 235 million in 2025 and projected to reach USD 342 million by 2032. Growth is driven by metro network modernization and stringent European safety regulations.

Germany, the United Kingdom, and France lead adoption through extensive urban transit development and strong passenger safety commitments. The region benefits from advanced engineering, sustainability focus, and alignment with smart city initiatives.

EU directives promoting accessibility, energy efficiency, and harmonized safety standards ensure consistent technology integration. Major infrastructure projects such as London’s Elizabeth Line, Paris Metro expansions, and Berlin U-Bahn upgrades strengthen demand. Key players including KONE and Schindler compete via innovation, digitalization, and predictive maintenance solutions supporting long-term operational efficiency and environmental goals.

Asia Pacific Leads Global Market Through Rapid Urbanization and Infrastructure Expansion

Asia Pacific dominates the global platform screen doors market with around 40% share, valued at USD 518 million in 2025 and projected to reach USD 752 million by 2032, growing at 6.8% CAGR. China drives regional leadership with over 3,500 equipped metro stations and continuous expansion across major cities.

Massive infrastructure investments, rapid urbanization, and strong government support for public transit modernization underpin growth. Japan, South Korea, India, and ASEAN countries contribute significant demand through metro development and safety upgrades.

The market features both international and regional manufacturers such as Fangda Group, Kangni, and Shanghai Electric leveraging cost advantages and local expertise. Innovation hubs in Japan and South Korea advance automation, sensor integration, and smart transit technologies, supported by strong localization and supply chain expansion initiatives.

Competitive Landscape

The competitive landscape for global platform screen doors market features both international manufacturers establishing regional production facilities and strong local players including Fangda Group, Kangni, and Shanghai Electric leveraging market knowledge and cost advantages. Technology innovation centers in Japan and South Korea drive advancement in automated control systems, sensor integration, and smart transportation applications.

Investment trends emphasize manufacturing capacity expansion, local supply chain development, and technology transfer partnerships supporting market localization and cost optimization strategies.

Government infrastructure programs including China's urban rail development plans and India's metro expansion initiatives create sustained long-term demand supporting regional market leadership through continued urbanization and transportation modernization.

Key Industry Developments

- In January 2023, Gilgen Door Systems AG acquired the operations and personnel of French automatic door expert Copas Systèmes SAS as part of its growth strategy. The business, established in 1992, specializes in the selling, setup, and upkeep of safety and autonomous access door systems. With 190 employees, Copas Systèmes is a prominent player in southeast France, and has a network of seven branches to offer consumers a full range of services.

- In April 2023, Chennai Metro Rail Ltd signed a contract with Zhuzhou CRRC Times Electric Co. Ltd. worth USD 12.14 million for the installation of passenger screen doors at Chennai Metro. The installation of half-height PSDs will be at 36 platforms, whereas full-height PSDs will be installed at 18 platforms.

Companies Covered in Platform Screen Doors Market

- Nabtesco Corporation

- Nanjing Kangni Mechanical & Electrical Co., Ltd.

- Zhuzhou CRRC Times Electric Co., Ltd.

- Knorr-Bremse AG

- Nippon Signal Co., Ltd.

- Kyosan Electric Manufacturing Co., Ltd.

- Overhead Door Corporation

- Westinghouse Air Brake Technologies Corp (Wabtec Corporation)

- Samjung Tech Co., Ltd.

- Singapore Technologies Engineering Ltd

- Schaltbau Holding AG

- Others Key Players

Frequently Asked Questions

The Platform Screen Doors market is estimated to be valued at US$ 941.0 Mn in 2025.

The key demand driver for the Platform Screen Doors (PSD) market is the rising emphasis on passenger safety and operational efficiency in urban transit systems.

In 2025, the Asia Pacific region will dominate the market with an exceeding 35% revenue share in the global Platform Screen Doors market.

Among the Product Type, Full Height holds the highest preference, capturing beyond 47.2% of the market revenue share in 2025, surpassing other parts.

The key players in Platform Screen Doors are Nabtesco Corporation, Knorr-Bremse AG, Nippon Signal Co., Ltd. and Overhead Door Corporation.