- Healthcare Services

- Newborn Screening Market

Newborn Screening Market Size, Share, and Growth Forecast 2026 - 2033

Newborn Screening Market by Product Type (Instruments, Reagents), Technology (Tandem Mass Spectrometry, Pulse Oximetry, Enzyme-based Assay, DNA Assay, Electrophoresis, Others), Test Type (Dry Blood Spot Test, CCHD, Hearing Screen), by Regional Analysis, 2026 - 2033

Newborn Screening Market Size and Trend Analysis

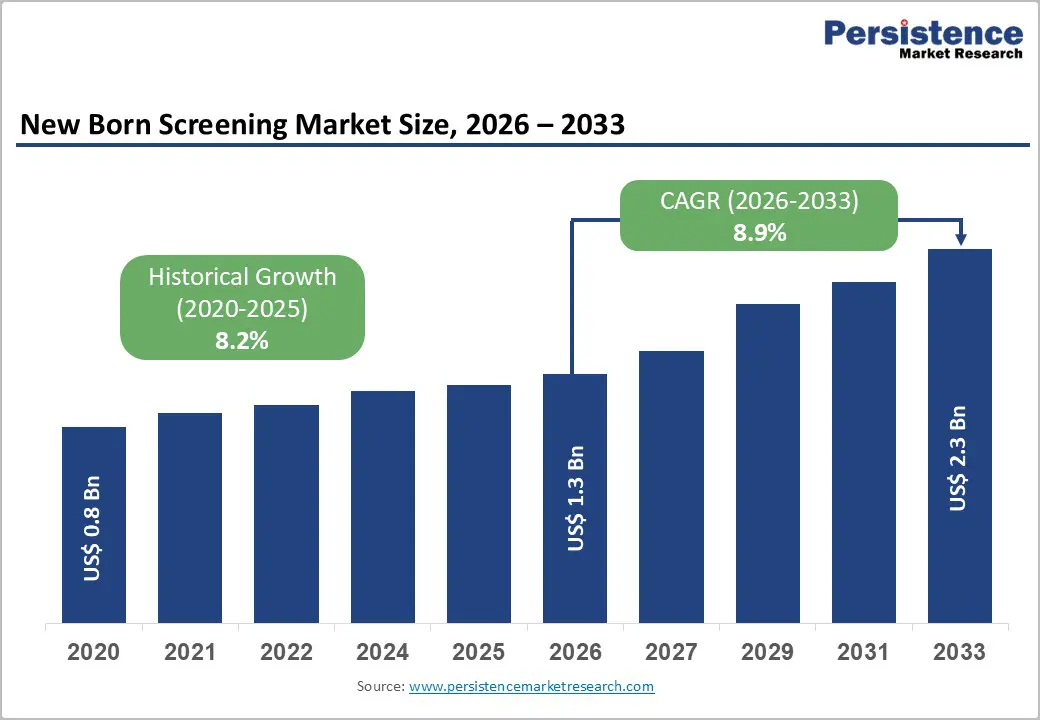

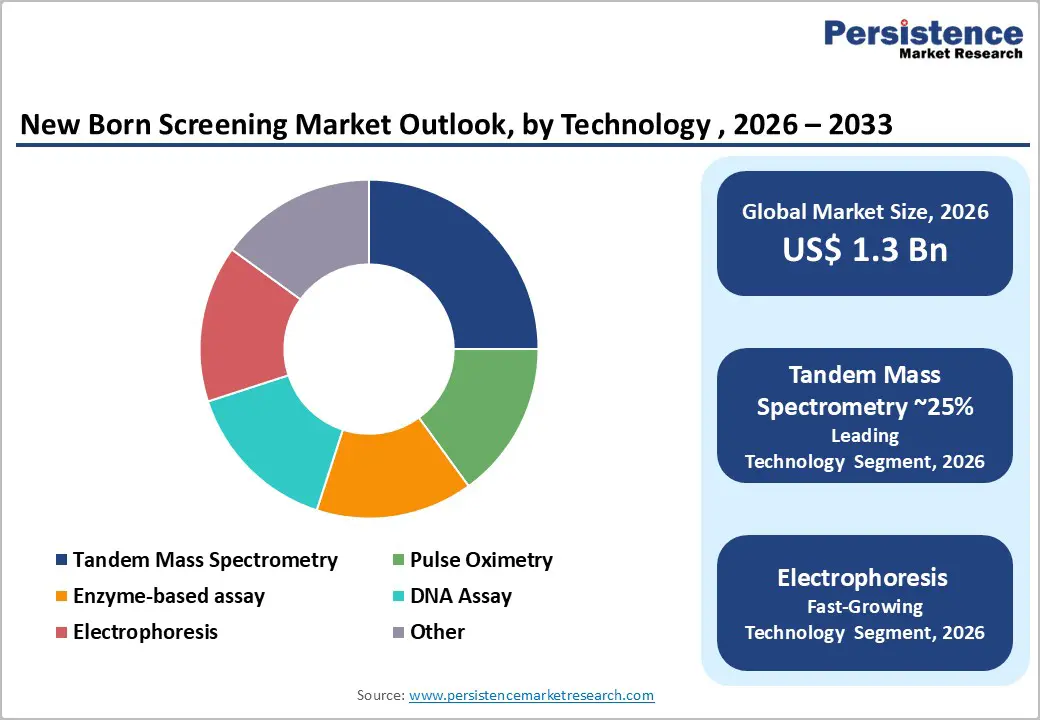

The global newborn screening market size is expected to be valued at US$ 1.3 billion in 2026 and projected to reach US$ 2.3 billion by 2033, growing at a CAGR of 8.9% between 2026 and 2033.

The newborn screening market is expanding due to the increasing global birth rate and rising prevalence of congenital disorders. According to the United Nations Department of Economic and Social Affairs (UN DESA) World Population Prospects, about 132.4 million babies were born worldwide in 2024. Additionally, the World Health Organization (WHO) estimates that congenital disorders affect nearly 6% of all births globally. The growing burden of genetic and metabolic disorders has increased the need for early detection through newborn screening programs. Furthermore, technological advancements, such as the EONIS Q system launched by Revvity, Inc. in 2023, are improving diagnostic capabilities and expanding screening adoption across healthcare systems worldwide.

Key Market Highlights

- North America leads the newborn screening market due to universal state programs, the RUSP framework, and extensive coverage of metabolic, hearing, and CCHD screening.

- Asia Pacific is the fastest-growing region, driven by high birth rates, rising healthcare spending, and expanding newborn screening programs across China, India, and Indonesia.

- Reagents dominate the product segment due to recurring demand for assay kits, calibrators, and consumables used extensively across multiple newborn screening tests.

- CCHD and newborn hearing screening are among the fastest-growing test types, supported by mandatory pulse oximetry screening policies and initiatives expanding global newborn hearing coverage.

- Technological advancements in tandem mass spectrometry and DNA assays create opportunities as multi-condition screening panels and molecular diagnostics become more cost-effective and widely adopted.

| Key Insights | Details |

|---|---|

|

Newborn Screening Market Size (2026E) |

US$ 1.3 billion |

|

Market Value Forecast (2033F) |

US$ 2.3 billion |

|

Projected Growth CAGR (2026–2033) |

8.9% |

|

Historical Market Growth (2020–2025) |

8.2% CAGR |

Market Dynamics

Drivers - Rising Incidence of Congenital Disorders Drives Newborn Screening Market

The escalating prevalence of congenital disorders significantly fuels the newborn screening market, as early detection of genetic disorders in infants is vital for preventing long-term disabilities. The World Health Organization reports that approximately 7.9 million infants are born each year with congenital disorders, including conditions such as newborn screening for cystic fibrosis, congenital hypothyroidism, and sickle cell disease, which can lead to severe health issues if not addressed early. This high incidence highlights the urgent need for comprehensive infant screening programs to identify disorders promptly, enabling timely interventions that enhance infant health outcomes. For instance, the CDC notes that U.S. newborn screening programs detect around 12,900 infants annually with conditions such as phenylketonuria (PKU), underscoring the importance of congenital anomaly detection. Advancements such as tandem mass spectrometry improve neonatal diagnostics precision, propelling market growth. As awareness of congenital disorders increases, the demand for accessible, effective newborn screening continues to surge, ensuring healthier outcomes for infants globally.

Government Mandates Fuel Newborn Screening Market Growth

Mandatory newborn screening programs and public health initiatives significantly drive the newborn screening market by promoting early detection of genetic disorders in infants. Over 70 countries, including the U.S., Canada, and European nations such as the UK and Germany, enforce mandatory newborn screening programs to identify congenital disorders early, preventing long-term health issues.

For instance, the U.S. Health Resources and Services Administration (HRSA) recommends infant screening for over 30 disorders, including newborn screening for cystic fibrosis and severe combined immunodeficiency (SCID), ensuring standardized neonatal testing across states. According to the CDC, nearly 4 million U.S. newborns are screened annually, boosting market adoption. In Canada, programs such as Ontario’s Newborn Screening, which tests for 29 conditions, as noted by the Canadian Pediatric Society, enhance early intervention efforts for infant health.

The UK’s NHS Newborn Blood Spot Screening Programme, focusing on genetic screening for nine rare disorders, exemplifies how public health initiatives increase accessibility and awareness. Advanced neonatal diagnostics, such as next-generation sequencing, further improve diagnostic precision, supporting market growth.

Restraints - Coverage Gaps and Infrastructure Limitations in Low- And Middle-Income Countries

Despite clear benefits, limited infrastructure and funding in low- and middle-income countries significantly restrain global market expansion. According to ISNS estimates, only about 39 million out of 140 million annual births worldwide receive newborn screening, with coverage highest in North America and Europe, but very limited in regions like Africa, where fewer than 1 million of approximately 30 million births annually are currently screened. In parts of Asia Pacific, including large birth-cohort countries such as India, only around 5 million babies per year are offered screening, leaving the majority without access to organized programs. Many countries lack centralized laboratories, cold-chain logistics, and trained personnel to run complex technologies like MS/MS or DNA-based assays and must prioritize essential services within constrained healthcare budgets. These gaps slow adoption of advanced technologies and limit per-capita test volumes, especially for expanded panels.

Opportunities - Advances in Tandem Mass Spectrometry and DNA-Based Assays

Rapid technological innovation, particularly in tandem mass spectrometry (MS/MS) and DNA-based assays, is creating compelling opportunities for industry and laboratories. MS/MS is recognized as an ethical, safe, and reliable screening method that can simultaneously analyze numerous amino acids and acylcarnitines, detecting significantly more inborn errors of metabolism than traditional clinical screening; in one cohort, MS/MS nearly doubled the detection rate of congenital metabolic errors compared with historical clinical methods. PerkinElmer Inc. has introduced the NeoBase 2 non-derivatized MS/MS kit, which can measure up to 57 analytes from a single dried blood spot punch, including markers for X-linked adrenoleukodystrophy and ADA-SCID, with a streamlined three-step workflow and integrated workstation software. More recently, Revvity, Inc. (PerkinElmer’s diagnostics-focused successor) and SCIEX announced a distribution agreement combining NeoBase™ 2 and NeoLSD™ reagents with SCIEX mass spectrometers to enhance robustness and precision for expanded newborn screening, enabling detection of more than 40 conditions via MS-based panels. Parallel growth in DNA-based assays, as shown in cost analyses of SMA carrier and diagnostic testing using digital PCR and MLPA, is further broadening the test menu and deepening the role of molecular technologies in this market.

Category-wise Insights

Product Type Analysis

Instruments dominate the newborn screening market, which has a 76% market share which is driven by the adoption of advanced equipment such as tandem mass spectrometers and next-generation sequencing platforms in developed markets, supporting neonatal diagnostics. These instruments enable high-throughput screening, critical for detecting multiple disorders efficiently. The high cost of instruments, coupled with recurring maintenance and calibration needs, contributes to their significant revenue share.

Reagents is the fastest-growing segment. Their recurring demand for tests such as dry blood spot and enzyme-based assays ensures steady market contribution to infant health. Advances in reagent formulations, such as those by Bio-Rad Laboratories, improve test sensitivity, further driving adoption.

Technology Analysis

Tandem mass spectrometry leads the technology segment, capturing 25% of the newborn screening market share in 2025 due to its ability to screen multiple congenital disorders simultaneously with high accuracy. Widely used in developed markets such as the U.S. and Germany, this technology benefits from continuous improvements by companies such as Waters Corporation, enhancing its diagnostic capabilities and market dominance.

Pulse oximetry is the fastest-growing technology. Its non-invasive nature and ability to detect critical congenital heart defects (CCHD) drive its adoption, particularly in regions mandating CCHD screening, such as the U.S. and U.K. Innovations by Masimo, including portable and cost-effective devices, are expanding its use in low-resource settings, contributing to rapid growth.

Test Type Analysis

Dry blood spot tests hold the largest share, at 46% in 2026, due to their widespread use in newborn screening for metabolic congenital disorders such as phenylketonuria (PKU) and hypothyroidism. Its simplicity, requiring only a few drops of blood collected on filter paper, makes it cost-effective and scalable, especially in large-scale programs.

CCHD screening is the fastest-growing test type, driven by mandatory newborn screening programs in over 40 countries and the rising prevalence of congenital heart defects affecting infant health. Pulse oximetry-based CCHD tests, which are non-invasive and quick, are increasingly integrated into newborn screening protocols.

Regional Insights

North America Newborn Screening Market Trends and Insights

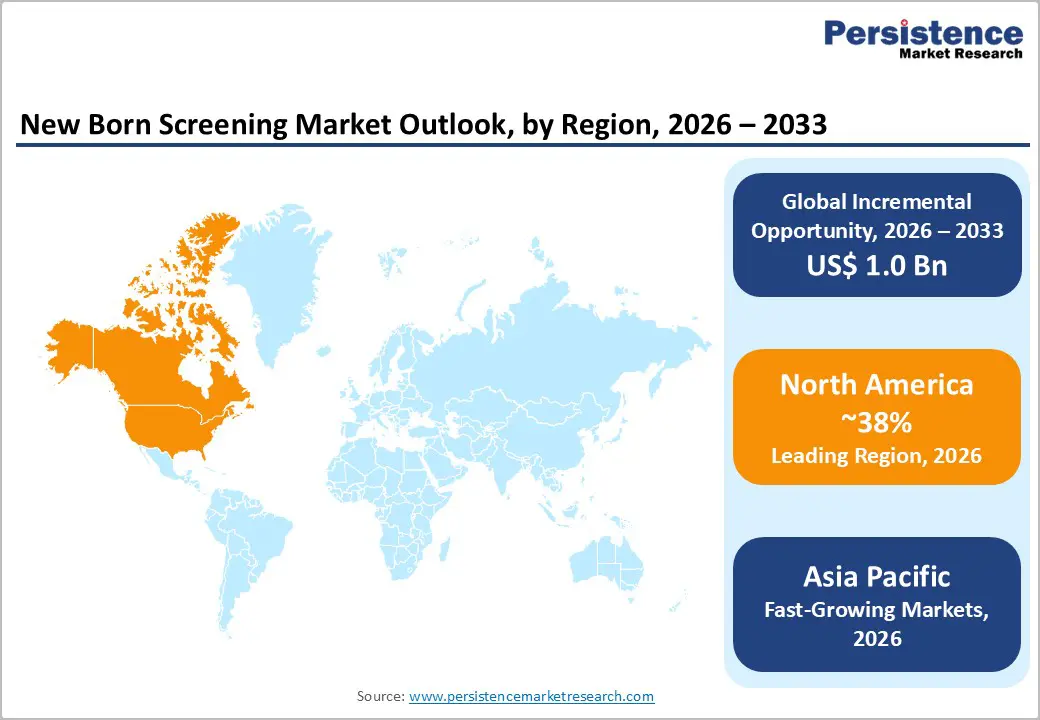

North America is the leading regional market, accounting for an estimated 38% share of global newborn screening revenues in 2026, anchored by the U.S. comprehensive programs and Canada’s strong provincial initiatives. The HRSA’s RUSP currently lists about 64 conditions that the U.S. Department of Health and Human Services recommends for inclusion in state screening panels, and most states now screen for most of these disorders. Large programs such as Texas screen roughly 400,000 newborns annually for 55 laboratory-tested conditions, plus universal hearing and CCHD screening, illustrating the high-throughput environment that drives demand for reliable instruments, MS/MS platforms, and assay kits. All 50 U.S. states have mandated CCHD screening using pulse oximetry, and national coverage for newborn hearing screening is also near universal.

Regulatory and professional bodies further shape market dynamics. The AAP and HRSA regularly update clinical and policy guidance, while state laboratories adhere to Clinical Laboratory Improvement Amendments (CLIA) and, in many cases, ISO 15189-aligned quality standards for laboratory accreditation. Innovation is robust: companies such as PerkinElmer/Revvity, SCIEX, Natus Medical Inc., and Masimo use the region as a launchpad for new MS/MS platforms, newborn hearing screeners, and neonatal pulse oximetry solutions. The combination of high screening coverage, continuous panel expansion (for example, adding lysosomal storage disorders and SCID), and emphasis on outcomes research positions North America as the benchmark market for advanced newborn screening solutions.

Asia Pacific Newborn Screening Market Trends and Insights

Asia Pacific is projected to be the fastest-growing newborn screening market, supported by very high birth cohorts, rising health expenditures, and gradual policy shifts towards universal screening. The region accounts for roughly 68.5 million of the 136.7 million annual global births, yet large countries such as China, India, Indonesia, Bangladesh, and Pakistan still lack fully organized programs for at least half of their newborns. ISNS estimates that only about 5 million babies in Asia Pacific currently receive newborn screening each year, underlining the gap between potential and realized coverage. Nonetheless, several countries are actively expanding programs: for example, China has developed provincial networks and increased the number of conditions beyond minimum government recommendations, while other countries in the region are proposing new laboratories and policies for national roll-outs.

Demand is further boosted by the inclusion of CCHD and hearing screening in hospital-based programs in urban centers, growing middle-class expectations for high-quality perinatal care, and the burden of conditions such as thalassemia and G6PD deficiency in parts of South Asia and Southeast Asia. International guidelines and collaborations encourage adoption of cost-effective technologies like dried blood spot MS/MS for multi-disease panels and pulse oximetry for CCHD screening, which are well suited to high-volume settings. As governments in China, Japan, India, and ASEAN countries invest in laboratory infrastructure, workforce training, and screening awareness campaigns, Asia Pacific is expected to post the highest CAGR among all regions, presenting significant growth opportunities for both global players and regional manufacturers.

Competitive Landscape

The global newborn screening market is highly competitive. Companies such as Bio-Rad and Waters Corporation are investing in R&D to develop cost-effective reagents and portable instruments for neonatal testing. Trivitron Healthcare collaborates with regional governments in Asia to expand newborn screening access. GE Lifesciences and Masimo are focusing on emerging markets, establishing distribution networks in India and China for infant health solutions. These companies dominate due to their extensive product portfolios and global presence in pediatric healthcare and neonatal diagnostics.

Key Market Developments

- In January 2025, QIAGEN N.V. partnered with Genomics England to support a program sequencing 100,000 newborn genomes in England, enabling early detection of over 200 rare diseases using expert-curated genomic content.

- In October 2025, Quantabio launched the sparQ Lysis Kit, expanding its newborn screening workflow for sequencing dried blood spots and showcasing the complete DBS-seq process at the APHL Newborn Screening Symposium 2025.

- In August 2024, Masimo highlighted its signal extraction technology pulse oximetry, widely used in leading U.S. hospitals, improving screening accuracy and monitoring over 200 million patients worldwide annually.

Companies Covered in Newborn Screening Market

- Agilent Technologies Inc.

- AB SCIEX

- Natus Medical Inc.

- Covidien plc

- Trivitron Healthcare

- GE Lifesciences

- Masimo

- Waters Corporation

- PerkinElmer Inc.

- Bio-Rad Laboratories Inc.

- Others

Frequently Asked Questions

The global newborn screening market size is projected to reach approximately US$ 1.3 billion in 2026.

Rising incidence of congenital disorders and mandatory newborn screening programs, such as the U.S. RUSP, are key drivers.

North America leads the global newborn screening market, supported by universal state‑level programs, the RUSP framework, and newborn hearing screening in U.S.

Development of cost-effective neonatal diagnostics and expansion in emerging markets such as India and China are key opportunities.

Agilent Technologies Inc., AB SCIEX, Natus Medical Inc., Covidien plc, Trivitron Healthcare, GE Lifesciences, Masimo, Waters Corporation, PerkinElmer Inc., and Bio-Rad Laboratories Inc.