- Advanced Materials

- Salt Hydrate Market

Salt Hydrate Market Size, Share, and Growth Forecast 2026 - 2033

Salt Hydrate Market by Salt Hydrate Type (Sodium-based salt hydrates, Calcium-based salt hydrates, Magnesium-based salt hydrates, Lithium-based salt hydrates, Other inorganic salt hydrates), Technology, Application, Industry, Regional Analysis, 2026 - 2033

Salt Hydrate Market Size and Trend Analysis

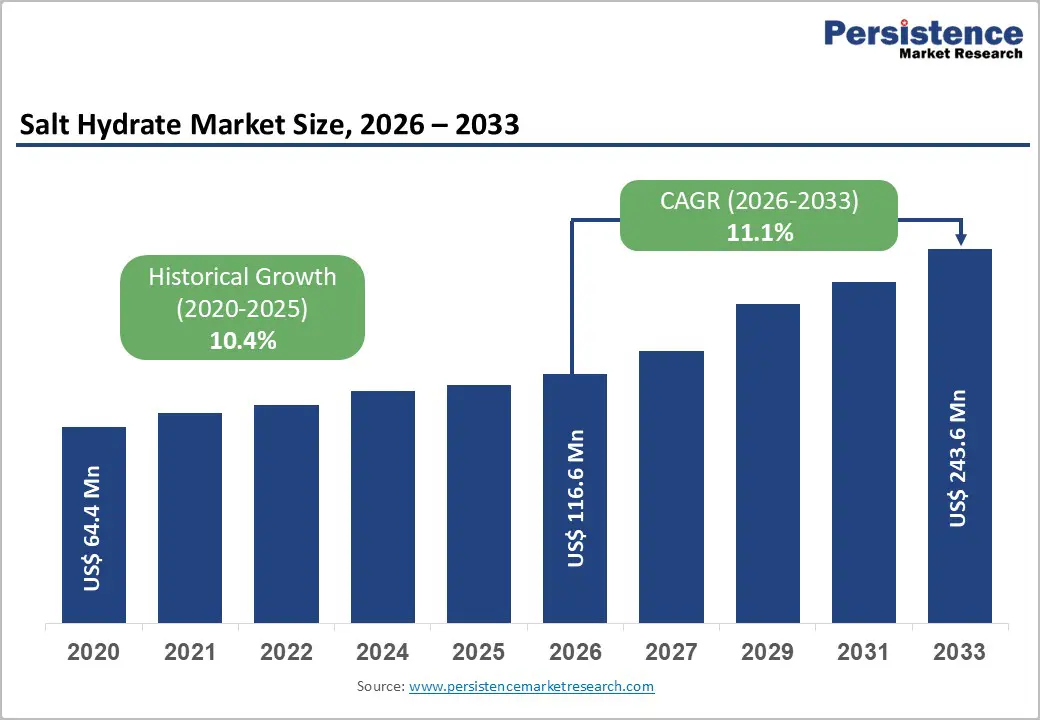

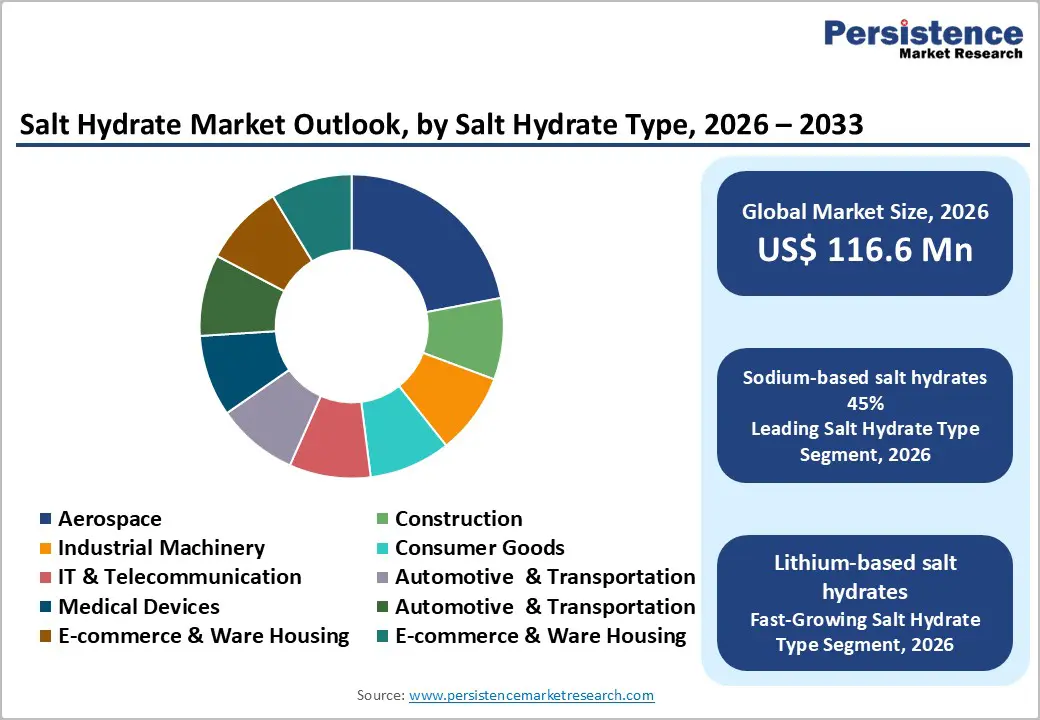

The global salt hydrate market size is expected to be valued at US$ 116.6 million in 2026 and projected to reach US$ 243.6 million by 2033, growing at a CAGR of 11.1% between 2026 and 2033. This growth is primarily driven by rising demand for salt hydrate-based phase change materials in thermal energy storage, owing to their high latent heat capacity and cost efficiency.

Increasing adoption of energy-efficient building solutions and renewable energy systems further supports market expansion. In addition, advances in encapsulation and material-stabilization technologies are improving performance reliability by reducing issues such as phase separation and supercooling, thereby broadening the application potential of construction, HVAC, refrigeration, and industrial thermal management systems.

Key Industry Highlights:

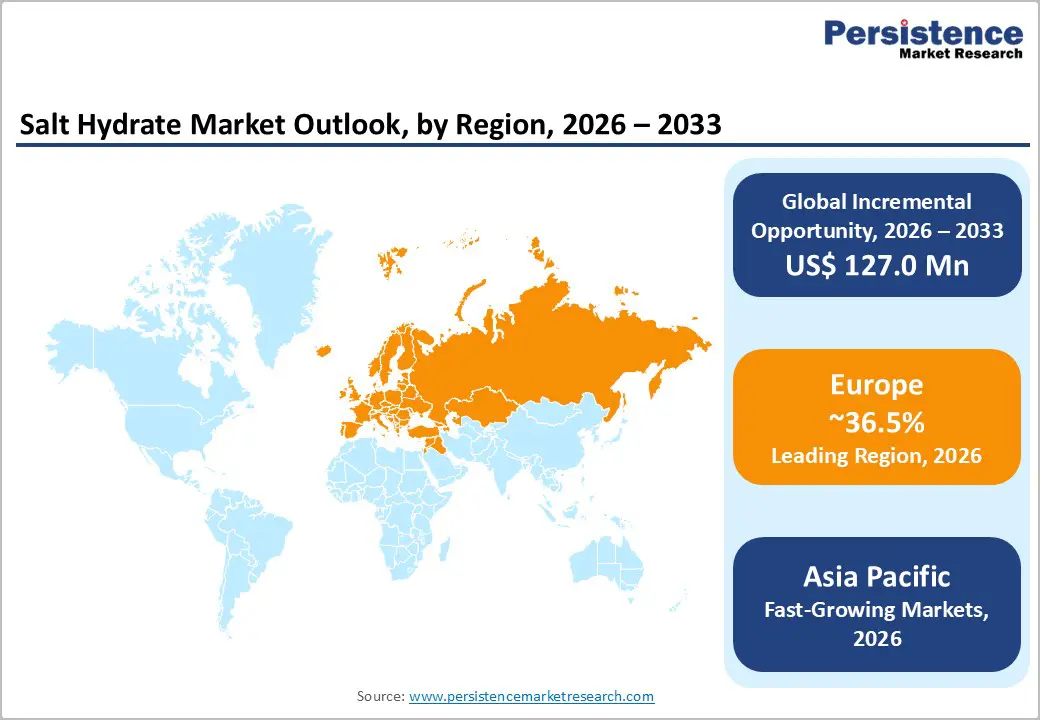

- Leading Region: Europe accounts for approximately 36.5% of the salt hydrate market in 2025, supported by stringent energy-efficiency regulations and strong adoption of PCM-based thermal storage in buildings.

- High-Growth Region: Asia Pacific accounts for nearly 32.4% of the market in 2025, driven by rapid urbanization, large-scale construction activity, and expanding manufacturing capacity across China, India, and Southeast Asia.

- Leading Technology: Encapsulated salt hydrates dominate the market with about 50% share in 2025, owing to superior phase stability, leakage prevention, and suitability for building-integrated thermal storage systems.

- Fastest-Growing Application: Refrigeration and cold chain applications represent the fastest-growing segment, driven by demand for stable, non-flammable thermal storage solutions in food and pharmaceutical logistics.

- Key Market Opportunity: Encapsulation innovations are projected to achieve a 15%+ CAGR in refrigeration, unlocking DOE-backed thermal gains.

| Key Insights | Details |

|---|---|

| Salt Hydrate Size (2026E) | US$ 116.6 million |

| Market Value Forecast (2033F) | US$ 243.6 million |

| Projected Growth CAGR (2026 - 2033) | 11.1% |

| Historical Market Growth (2020 - 2025) | 10.4% |

Market Dynamics

Drivers - Growing Emphasis on Energy-Efficient Thermal Energy Storage Systems

The increasing global focus on energy efficiency is a major driver for the salt hydrate market, particularly in thermal energy storage applications. Salt hydrates are widely used as phase change materials due to their high latent heat capacity and strong volumetric energy density, enabling efficient heat absorption and release. Their ability to reduce peak energy demand makes them suitable for HVAC systems, refrigeration, and temperature-controlled environments across residential, commercial, and industrial buildings.

In addition, salt hydrates offer cost advantages, non-flammability, and a safer profile compared with many organic alternatives. Government initiatives promoting net-zero buildings and energy-efficient infrastructure further support adoption. As energy costs rise and sustainability targets tighten, salt hydrate-based thermal storage solutions are increasingly preferred to enhance overall energy performance and operational efficiency.

Expansion of Green Building Regulations and Sustainable Construction Practices

The expansion of green building regulations and sustainability-focused construction standards is another key driver supporting the growth of the salt hydrate market. Regulatory frameworks increasingly mandate energy-efficient materials for passive heating and cooling, encouraging the integration of phase change materials in building envelopes. Salt hydrates meet these requirements through effective thermal regulation, thereby reducing heating and cooling loads while maintaining indoor comfort.

Rapid urbanization and infrastructure development amplify demand, as developers seek materials that support green building certifications and long-term operational cost reduction. Furthermore, ongoing technological advancements, such as improved encapsulation methods and reduced supercooling effects, enhance performance reliability. These improvements make salt hydrates more suitable for widespread use in modern, energy-efficient construction projects.

Restraints - High Production Costs and Supply Chain Volatility Impacting Scalability

High production costs and supply chain volatility pose notable restraints on the salt hydrate market, particularly compared with alternative phase change materials. The manufacturing of salt hydrates requires precise formulation and controlled processing to prevent phase separation and performance degradation. These additional processing requirements increase overall production costs, thereby reducing the competitiveness of salt hydrate solutions in cost-sensitive applications such as residential buildings and small-scale thermal storage systems.

Moreover, fluctuating prices of key raw materials and dependence on mining-based supply chains contribute to inconsistent availability and quality. Supply disruptions and logistical challenges further increase costs, limiting large-scale adoption despite the long-term energy-efficiency benefits of salt-hydrate-based thermal storage solutions.

Corrosion, Stability, and Long-Term Performance Limitations

Corrosion and stability challenges significantly restrain the broader adoption of salt hydrates in thermal energy storage applications. Many salt hydrates exhibit corrosive behavior toward common metals, necessitating the use of specialized containment materials and protective coatings, which increases maintenance and system costs. Inadequate material compatibility can reduce system service life, discouraging use in long-duration and residential installations.

Issues such as supercooling, phase segregation, and leakage reduce cycling reliability when proper encapsulation is not employed. These performance limitations raise concerns about long-term operational stability, particularly in applications that require consistent thermal performance over extended service periods.

Opportunities - Advancements in Encapsulated Salt Hydrate Technologies for Buildings

Innovation in encapsulated salt hydrate technologies presents a significant growth opportunity, particularly within the rapidly expanding green building and HVAC sectors. Advanced encapsulation methods improve thermal conductivity, enhance heat transfer rates, and address long-standing issues such as leakage and phase separation. These improvements enable faster charge-discharge cycles, making salt hydrates more suitable for dynamic thermal management in commercial and residential buildings.

As global construction increasingly prioritizes energy efficiency and sustainable design, demand for high-performance phase change materials continues to rise. Asia Pacific offers strong growth potential due to rapid urbanization and supportive energy-efficiency policies. Manufacturers that invest in advanced encapsulation and composite formulations are well-positioned to capitalize on this expanding market opportunity.

Rising Adoption in Renewable and Long-Duration Energy Storage Systems

The expansion of renewable energy systems creates substantial opportunities for salt hydrates in thermal and thermochemical energy storage applications. Salt hydrates offer high energy-storage density, making them suitable for seasonal and long-duration storage solutions that support solar thermal and industrial heat-recovery systems. Their ability to store and release energy efficiently aligns well with the intermittent nature of renewable power generation.

Policy-driven initiatives aimed at decarbonization and energy security are accelerating research and deployment of advanced storage technologies. Additionally, growing demand from the refrigeration and cold-chain industries supports further adoption, as stable salt hydrate composites enable reliable temperature control while advancing carbon-neutrality and sustainability goals across multiple end-use sectors.

Category-wise Analysis

Salt Hydrate Type Insights

Sodium-based salt hydrates dominate the salt hydrate market, accounting for around 45% share in 2025 due to their favorable thermal properties, wide availability, and cost-effectiveness. Materials such as sodium sulfate decahydrate are extensively used in building thermal storage applications, offering suitable melting temperatures and high latent heat capacity. Their proven cycling stability and compatibility with construction materials support strong adoption across residential and commercial energy-efficient buildings.

Looking ahead, lithium-based and advanced composite salt hydrates are emerging as the fastest-growing category. These materials are gaining attention for their precise temperature control, improved stability, and suitability for specialized thermal storage applications. Growing demand from high-performance HVAC systems, electronics cooling, and renewable energy storage is expected to accelerate innovation and adoption of these advanced salt hydrate formulations.

Technology Insights

Encapsulated salt hydrates constitute the leading technology segment, holding approximately 50% of the market in 2025. Their dominance is driven by superior leakage prevention, enhanced thermal reliability, and improved resistance to phase separation and supercooling. Advanced encapsulation structures enable better heat transfer and consistent performance, making them the preferred choice for dynamic applications such as HVAC systems and building-integrated thermal storage solutions.

Non-encapsulated and hybrid composite technologies are expected to be the fastest-growing segment as manufacturers seek lower-cost alternatives and simplified system designs. Ongoing material engineering efforts focus on stabilizing bulk salt hydrates using additives and surface treatments. These innovations are expanding their applicability in industrial heat management and large-scale thermal storage installations.

Application Insights

Building and construction applications lead the salt hydrate market with approximately 40% share in 2025, supported by strong demand for energy-efficient materials that reduce heating and cooling loads. Salt hydrates are widely integrated into walls, ceilings, and concrete structures to enable passive thermal regulation. Regulatory emphasis on sustainable construction and green building standards continues to reinforce their dominant position.

The refrigeration and cold-chain segment is emerging as the fastest-growing application area. Rising demand for temperature-controlled logistics, pharmaceuticals, and food preservation is driving adoption of salt hydrate-based thermal storage solutions. Their non-flammable nature, stable temperature control, and ability to maintain cold conditions efficiently make them increasingly attractive for modern cold storage infrastructure.

Industry Insights

The industrial sector leads the salt hydrate market, accounting for approximately 35% of the market in 2025, driven by strong demand from manufacturing, refrigeration, and pharmaceutical processing facilities. Industries benefit from the high energy density and non-flammable nature of salt hydrates, which support safe and efficient thermal management. Improved composite formulations further enhance durability and performance in harsh industrial environments.

The commercial building sector is expected to be the fastest-growing Industry. Increasing investments in energy-efficient offices, hospitals, data centers, and retail spaces are driving demand for advanced thermal storage solutions. Salt hydrates are gaining traction as part of integrated HVAC and energy management systems that support sustainability goals and long-term operational cost reduction.

Regional Insights

North America Salt Hydrate Market Trends and Insights

North America represents a mature and innovation-driven salt hydrate market, led primarily by the United States. The region benefits from a strong R&D ecosystem supported by federal funding, with research institutions advancing encapsulation technologies to improve energy density and cycling stability. Salt hydrate phase change materials are increasingly integrated into HVAC systems, cold chain logistics, and energy-efficient buildings, supported by structured standards and incentive-based adoption frameworks.

North America is also the fastest-growing developed market, supported by rising investments in sustainable construction and temperature-controlled logistics. The region is projected to grow at a CAGR of around 11.5%, driven by the growing deployment of PCMs in commercial buildings, data centers, and refrigeration infrastructure. Continued policy support for energy efficiency and decarbonization sustains long-term growth momentum.

Europe Salt Hydrate Market Trends and Insights

Europe holds a significant position in the global salt hydrate market, accounting for approximately 36.5% share in 2025. Germany leads regional adoption, supported by strong manufacturing capabilities and established PCM suppliers, while France, the UK, and Nordic countries drive demand through building retrofits and energy-efficient housing initiatives. Strict environmental regulations and coordinated climate policies strongly favor the integration of salt hydrates.

Europe is also among the most innovation-intensive regions, with rapid adoption of salt hydrate PCMs in green buildings, district heating, and solar thermal systems. Countries such as Spain and Italy are increasingly leveraging salt hydrates for renewable energy integration. Ongoing investments in sustainable infrastructure and stringent building energy codes are expected to sustain steady growth across both residential and commercial sectors.

Asia Pacific Salt Hydrate Market Trends and Insights

Asia-Pacific is a high-growth region, accounting for approximately 32.4% of the global salt hydrate market in 2025. China and India dominate regional demand due to rapid urbanization, expanding construction activity, and rising adoption of energy-efficient building technologies. Japan contributes through advanced refrigeration and thermal management applications, particularly in the cold chain and industrial sectors.

Asia Pacific is also the most dynamic growth region, driven by large-scale manufacturing expansion and cost-competitive production of salt hydrate materials. Southeast Asian countries are increasingly adopting salt hydrates for export-oriented cold storage and logistics applications. Government initiatives supporting energy efficiency, coupled with rising infrastructure investment, continue to accelerate adoption across construction, refrigeration, and renewable energy storage applications.

Competitive Landscape

The salt hydrate market is moderately consolidated, with competition shaped by technological capabilities and product performance rather than scale alone. Leading participants focus on developing advanced salt hydrate formulations that offer improved thermal stability, higher energy density, and reliable cycling performance. Continuous investment in research and development, particularly in encapsulation and material stabilization, is a key strategy used to strengthen product differentiation and maintain competitive positioning.

Companies are expanding their market presence through strategic collaborations, technology partnerships, and application-specific solutions. Emerging competitive approaches emphasize sustainable material development, including bio-based composites and tailored eutectic formulations. These innovations address performance limitations while aligning with growing demand for environmentally responsible and customized thermal energy storage solutions.

Key Developments:

- In 2024, Rubitherm Technologies introduced an enhanced SP-line of salt hydrate phase change materials designed for thermal storage systems, focusing on improved phase stability, reduced supercooling behavior, and higher cycling reliability across building and HVAC energy management applications.

- In 2023, Lawrence Berkeley National Laboratory conducted advanced screening of salt hydrates for thermochemical material applications, demonstrating energy storage densities of up to 500 kWh/m³ for building heating systems, supporting long-duration and seasonal thermal energy storage solutions.

- In March 2021, the U.S. Department of Energy awarded US$1.2 million to Oak Ridge National Laboratory and Phase Change Energy Solutions to advance microencapsulation of salt hydrates, targeting an improved thermal conductivity of approximately 1.5 W/m·K for high-performance thermal energy storage applications.

Companies Covered in Salt Hydrate Market

- Climator Sweden AB

- Phase Change Energy Solutions Inc.

- Rubitherm Technologies GmbH

- PCM Products Ltd.

- Pluss Advanced Technologies Pvt. Ltd.

- BASF SE

- Croda International Plc

- Axiotherm GmbH

- Salca BV

- PureTemp LLC

- TEAP Energy Solutions

- Sunamp Ltd

- Mitsubishi Chemical Corporation

- Henkel AG & Co. KGaA

- Honeywell International Inc.

Frequently Asked Questions

The global salt hydrate market is projected to reach US$ 116.6 million in 2026, supported by rising adoption of phase change materials in buildings, refrigeration, and industrial thermal storage.

Growing demand for energy-efficient thermal storage in buildings, where salt hydrates enable passive temperature regulation and reduce heating and cooling loads, is a primary market driver.

Europe leads with around 36.5% market share in 2025, driven by strict energy-efficiency regulations, green building mandates, and strong integration of salt hydrate PCMs across construction and heating systems.

Encapsulated salt hydrate technologies present a major opportunity, particularly in refrigeration and cold chain applications, as they improve phase stability, leakage resistance, and thermal reliability.

Leaders include Rubitherm Technologies, PCM Products Ltd, and Phase Change Energy Solutions.