- Food Ingredients & Additives

- Celtic Salt Market

Celtic Salt Market Size, Share, and Growth Forecast, 2025 - 2032

Celtic Salt Market By Material Type (Coarse Celtic Salt, Fine Celtic Salt), Product Type (Conventional, Organic Certified), Application, Distribution Channel, and Regional Analysis for 2025 - 2032

Celtic Salt Market Size and Trends Analysis

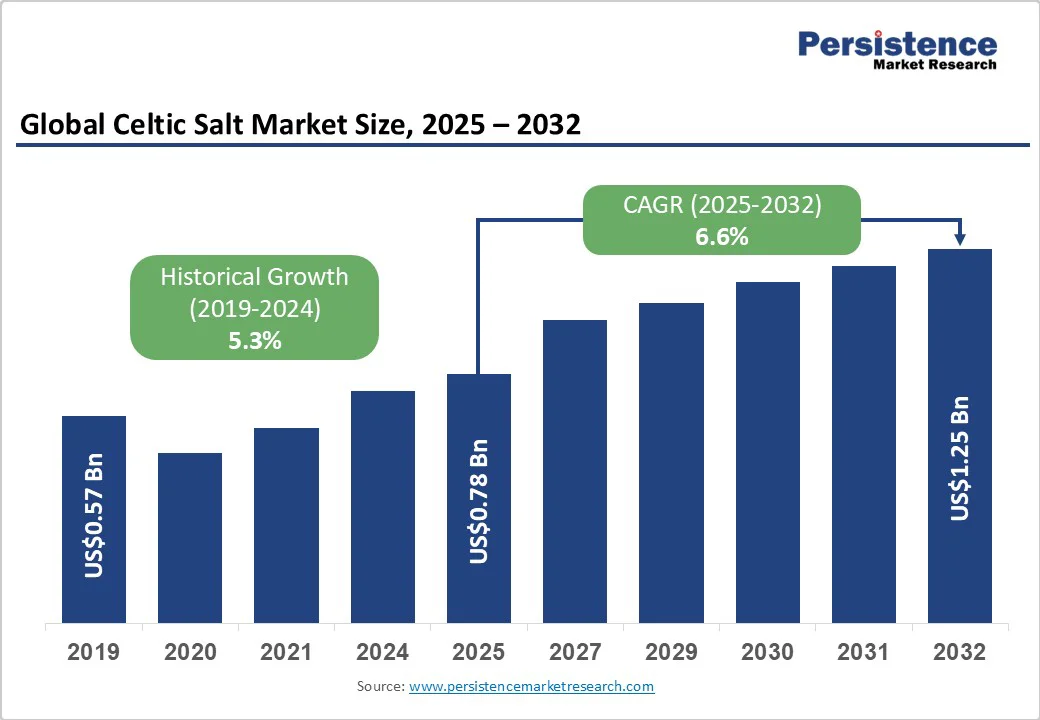

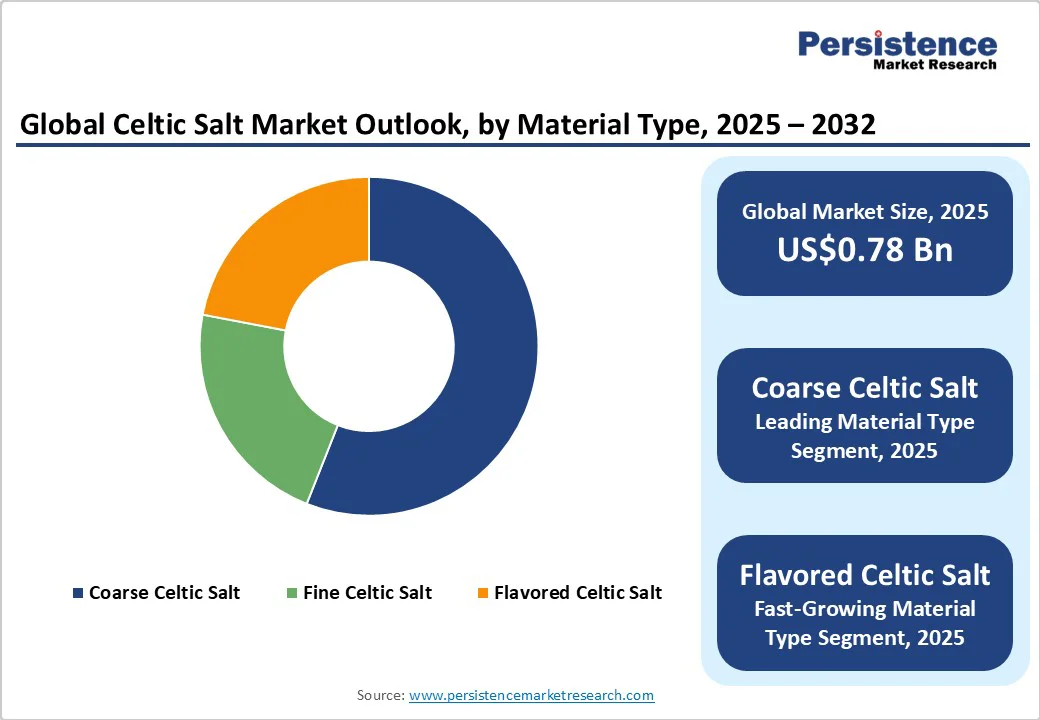

The global Celtic salt market size is likely to be valued at US$0.78 Bn in 2025. It is expected to reach US$1.25 Bn by 2032, growing at a CAGR of 6.6% during the forecast period from 2025 to 2032, driven by the intersection of culinary premiumization, health-conscious consumer preferences, and growing adoption in personal-care products.

Key Industry Highlights

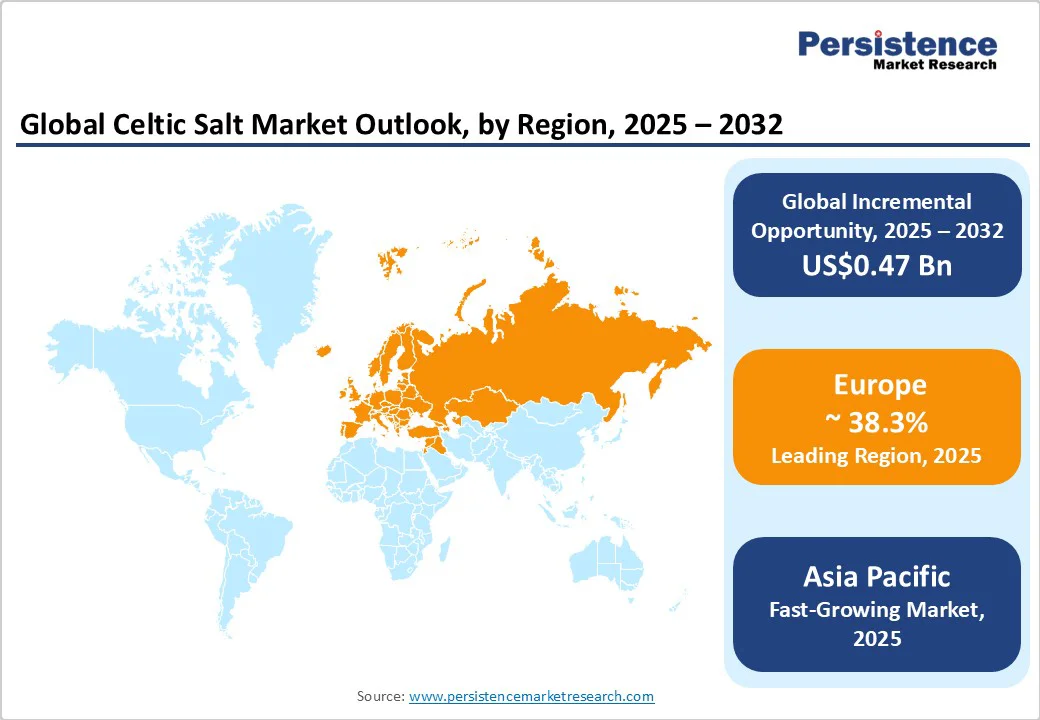

- Leading Region: Europe is expected to account for 38.3% of global revenue in 2025, driven by artisanal salt production in France and strong consumer preference for natural, minimally processed salts.

- Fastest-growing Region: Asia Pacific is projected to grow at a 6.6% CAGR (2025–2032), supported by rising disposable incomes, health-conscious diets, and expanding e-commerce channels in China, Japan, and India.

- Investment Plans: Increasing capital flow into organic-certified Celtic salt production and flavored product innovation, with a focus on premium retail and wellness-driven applications across North America and Europe.

- Dominant Material Type: Coarse Celtic Salt is anticipated to lead, with 55.4% share in 2025, owing to its broad use in foodservice, gourmet cooking, and artisanal applications.

- Leading Product Type: Conventional Celtic Salt is likely to account for 92.7% of sales in 2025, supported by its affordability, scalability, and entrenched retail and foodservice distribution channels.

| Key Insights | Details |

|---|---|

|

Celtic Salt Market Size (2025E) |

US$0.78 Bn |

|

Market Value Forecast (2032F) |

US$1.25 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Premiumization, Foodservice Demand, and Wellness Consumer Trends

Celtic salt has established a strong foothold in the premium culinary category, reflecting its role as both a finishing salt in gourmet restaurants and a premium ingredient in packaged foods. Chefs and foodservice distributors prioritize Celtic salt due to its mineral content, texture, and unique flavor profile. The global rise of culinary tourism, cooking shows, and gourmet dining trends has reinforced the demand.

Consumers are increasingly shifting toward minimally processed, natural, and “clean-label” products. Celtic salt is perceived as healthier because it has lower sodium and higher trace mineral content than refined salt. This aligns with global health-conscious purchasing patterns. Surveys show that over 60% of consumers in North America and Europe are willing to pay a premium for natural or organic food products. As hypertension and cardiovascular health remain top public health concerns, the demand for alternatives to refined salt is expected to continue rising.

Traditionally dominated by bulk B2B supply to restaurants and gourmet distributors, the sector has seen significant acceleration in e-commerce. Online grocery platforms, specialty retailers, and direct-to-consumer websites now provide greater visibility and consumer access. Supermarket private-label brands are also entering the premium salt segment, often partnering with regional suppliers to launch Celtic-style offerings.

Seasonal Harvesting, Supply Constraints, and Legal Risks

Celtic salt is harvested using traditional evaporation methods in coastal salt marshes, particularly in Brittany (Guérande). These processes are seasonal and highly dependent on climatic conditions. A poor harvest season can reduce availability and trigger price increases. Because production is geographically concentrated, global supply is vulnerable to localized weather disruptions. This limited scalability restricts mass-market penetration and may discourage large-scale industrial buyers who prioritize stable supply and pricing.

The market also faces heightened regulatory exposure. In the U.S., California's Proposition 65 requirements have drawn attention to potential levels of heavy metals in some unrefined salts. Recent class-action lawsuits and regulatory filings have increased compliance costs for suppliers, particularly smaller brands that lack dedicated quality assurance budgets. These risks impact financial performance through legal costs, also damaging brand reputation and leading to retailer delistings. Stricter labeling requirements, mandatory testing, and greater transparency requirements are expected across multiple jurisdictions, which could slow smaller entrants and favor larger, better-capitalized companies.

Expansion into Personal-Care and Wellness Products to Create New Opportunities

Beyond its culinary uses, Celtic salt is increasingly used in personal care products, such as bath salts, scrubs, and mineral-rich cosmetics. As natural and mineral-based ingredients gain popularity in the spa and beauty sector, suppliers who certify their products as cosmetic-grade will capture incremental value. Cross-branding opportunities with skincare companies further enhance market potential.

Certified organic Celtic salt is expected to grow rapidly among product categories. This growth reflects consumer demand for traceable, verified products. Flavored variants, infused with herbs, spices, or smoke, are another fast-growing sub-segment, growing at a fast CAGR. Together, organic and flavored products offer opportunities for higher-margin growth.

Category-wise Analysis

Material Type Insights

Coarse celtic salt is anticipated to be the market leader, accounting for 55.4% of revenue in 2025. Its large crystals and distinctive texture make it highly valued in gourmet cooking, artisanal baking, and professional foodservice applications. The bulk supply format, combined with consumer demand for authentic, minimally processed salt, ensures a steady demand. Coarse varieties are also preferred in curing and roasting due to their slow dissolution rate, which enhances flavor retention. This entrenched position across both commercial and household kitchens solidifies coarse salt as the largest revenue contributor through 2032.

Flavored Celtic salts, infused with herbs, spices, or smoke, represent the most dynamic sub-category. This growth is supported by rising consumer interest in novelty, gifting products, and premium culinary experiences. Flavored salts are gaining popularity in direct-to-consumer e-commerce, subscription boxes, and gourmet retail outlets. Their strong branding potential, combined with higher unit margins than conventional coarse or fine salts, makes them attractive to producers. As global flavor experimentation increases, this segment is expected to drive incremental revenue and capture a larger share of the retail-focused Celtic salt market. For example, Jacobsen Salt Co. introduced a range of citrus- and spice-infused Celtic salts, targeting gourmet retail and gift markets, and expanded partnerships with upscale kitchenware stores.

Product Type Insights

Conventional Celtic salt dominates the product type category, accounting for 92.7% of the revenue in 2023. Its leadership is reinforced by widespread availability, affordability, and entrenched supply chains, particularly for restaurants and food manufacturers. Conventional Celtic salt benefits from scalability, strong supermarket and foodservice distribution, and its perception as a healthier alternative to refined table salt. The category’s price competitiveness ensures its continued market leadership, especially in developing regions where certified organic variants remain a niche market. Conventional products are expected to continue generating baseline demand growth through 2032.

Organic-certified Celtic salt is projected to expand at a high CAGR from 2024 to 2030, the highest across all product categories. Rising consumer demand for traceability, certification, and premium-quality natural foods underpins this growth. Retailers are allocating more shelf space to certified organic products, while export markets are increasingly requiring organic labels for entry. The premium positioning of organic salts allows companies to secure higher margins and brand loyalty. As consumers align their food choices with sustainability and wellness trends, the organic-certified segment is expected to expand rapidly, reshaping the product mix and opening new revenue streams for producers. For example, SaltWorks Inc. recently launched a certified organic Celtic salt line, emphasizing traceability and sustainability. The product gained quick traction in organic grocery chains and wellness-focused online retailers.

Regional Insights

Europe Celtic Salt Market Trends

In 2025, Europe accounted for 38.3% of global revenue, making it the largest regional market for premium and natural salts. Both historical significance and modern regulatory alignment underpin the region’s dominance. France, in particular, is a pivotal player thanks to its salt-producing regions of Brittany and Guérande, which enjoy Protected Geographical Indication (PGI) status. Countries, including Germany, the U.K., and Spain, contribute significantly to consumption, driven by demand in both home cooking and upscale hospitality.

The European Union's regulatory framework is highly developed, emphasizing traceability, comprehensive labeling, and organic certification standards, which present compliance challenges but also create market entry barriers that favor authentic and certified producers. The cooperative model used by French salt harvesters ensures fair trade, quality control, and strong links to cultural heritage, factors that reinforce consumer trust and justify premium pricing. European brands are increasingly investing in sustainable harvesting practices, biodegradable or recyclable packaging, and scaling export operations to markets in Asia and North America. Marketing strategies often tie into local terroir, traditional methods, and culinary prestige, making European sea salts a benchmark for quality.

Asia Pacific Celtic Salt Market Trends

Asia Pacific is currently the fastest-growing market, with a 6.6% CAGR projected through 2032. This surge is being led by China and Japan, where there is a strong affinity for gourmet ingredients and fine dining that values umami-rich, mineral-enhanced salts. Simultaneously, countries including India, Indonesia, and Vietnam are experiencing rapid growth through online grocery platforms, health-focused marketplaces, and the expanding influence of food bloggers and chefs on social media.

Rising disposable incomes, urbanization, and increased exposure to global culinary trends are accelerating awareness and adoption of premium salts, particularly among the urban middle class. Brands are responding by adopting localized packaging, language customization, and digital-first marketing strategies, including influencer collaborations and livestream commerce.

While the region still contends with tariffs, import logistics, and variable food safety standards, the long-term outlook is positive. By 2032, the Asia Pacific is projected to contribute nearly 25% of the incremental global demand for natural and gourmet salts. Local production is also beginning to scale up in regions, including the Himalayan foothills (India and Pakistan) and coastal Japan, offering potential for both domestic sourcing and export-oriented growth.

North America Celtic Salt Market Trends

The U.S. leads in the North American premium salt market. Growth is driven by a combination of strong e-commerce infrastructure, increasing interest in clean-label and natural products, and a willingness among health-conscious consumers to pay a premium for artisanal or mineral-rich salts. The region faces intensifying regulatory oversight, particularly under California’s Proposition 65, which requires warning labels for products that contain trace levels of heavy metals or other listed substances. This has led to legal action and compliance costs for brands such as Celtic Sea Salt and underscores the importance of stringent third-party testing and transparent sourcing practices.

Key players include Selina Naturally (Celtic Sea Salt), Eden Foods, and SaltWorks, each leveraging differentiated value propositions, from origin stories to mineral content and sustainability. Recent investment trends highlight a focus on advanced packaging solutions (e.g., moisture-resistant, compostable materials), lab verification, and direct-to-consumer (DTC) models that allow brands to build community and loyalty through storytelling and educational content.

Competitive Landscape

The global celtic salt market is moderately fragmented. Global players, including Selina Naturally and SaltWorks, coexist with artisanal producers in France and U.K.-based specialty brands. Regional private-label growth adds further competition. While coarse and conventional products dominate volume, innovation and certification are reshaping competitive dynamics. Provenance, flavor innovation, and compliance capabilities are the primary differentiators.

Leading players emphasize premium branding, certification, e-commerce channel expansion, and traceability investments. Cost leadership plays a secondary role, as differentiation and provenance are the main drivers of market share.

Key Industry Developments:

- In August 2025, Cornish Sea Salt Co. (U.K.) partnered with a major European wellness brand to launch a Celtic salt-based spa and bath line, marking its entry into the personal-care segment.

- In November 2024, Cornish Sea Salt launched TekSalt, a mineral-balanced Celtic sea mineral salt product for food manufacturers. This salt delivers flavor while helping to lower sodium, targeting industrial-scale seasoning and formulation needs.

Companies Covered in Celtic Salt Market

- Le Guérandais

- SaltWorks Inc.

- Cornish Sea Salt Co.

- Celtic Sea Salt Company

- Maldon Salt Company

- Cargill Inc.

- The San Francisco Salt Company

- Jacobsen Salt Co.

- Morton Salt Inc.

- Murray River Salt

- Cheetham Salt Ltd.

- Natures Cargo

- Himalayan Chef

- Pacific Salt International

- Dominion Salt Ltd.

- Alaska Pure Sea Salt Co.

- Redmond Life

- Oregon Sea Salt Co.

- Artisan Salt Company

Frequently Asked Questions

The celtic salt market size is estimated to be at US$0.78 Bn in 2025.

By 2032, the celtic salt market is projected to reach US$1.25 Bn, growing steadily over the forecast horizon.

Key trends are the rising adoption of organic-certified and flavored Celtic salts in premium food segments and the growing penetration of personal care and wellness applications (bath salts, scrubs).

By material type, coarse celtic salt is projected to dominate with 55.4% market share in 2025, driven by demand in gourmet cooking and foodservice.

The market is projected to grow at a CAGR of 6.6% between 2025 and 2032.

Some of the leading companies in the Celtic salt market include Selina Naturally, Le Guérandais, SaltWorks Inc., Cornish Sea Salt Co., and Celtic Sea and Salt Company.