- Food Ingredients & Additives

- Food Grade Salt Market

Food Grade Salt Market Size, Share, and Growth Forecast, 2026 - 2033

Food Grade Salt Market by Salt Type (Sodium Chloride, Potassium Chloride, Others), Application (Dairy Products, Bakery Products, Others), Distribution Channel (Direct Sales, Distributors, Retail Stores, Online Platforms), and Regional Analysis for 2026 - 2033

Food Grade Salt Market Size and Trends Analysis

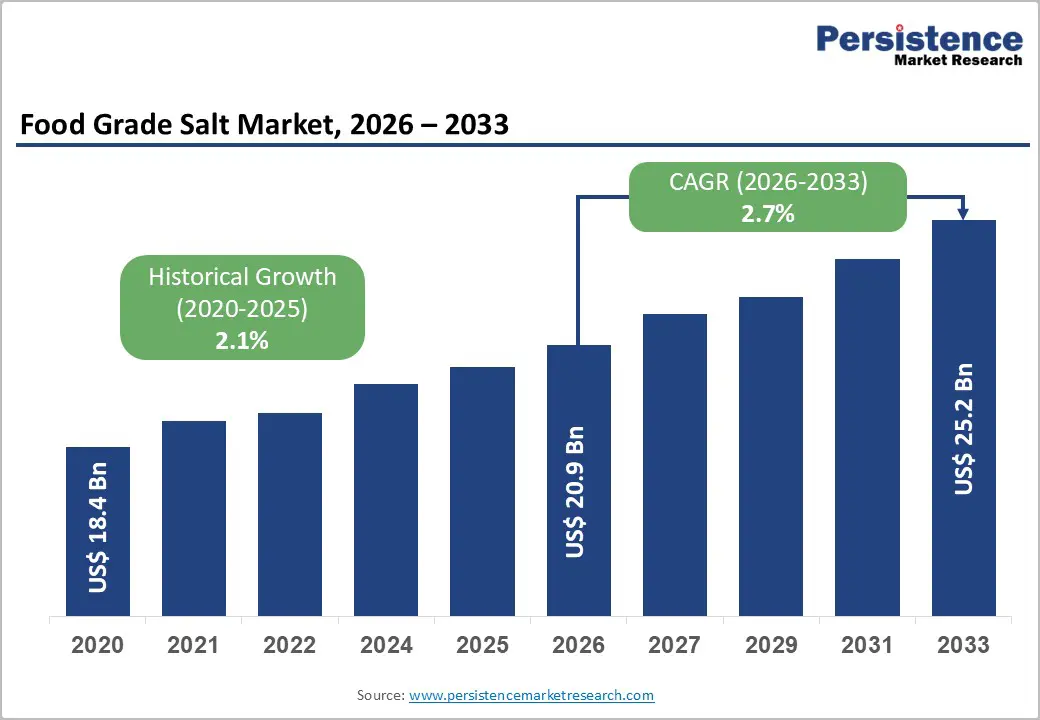

The global food-grade salt market size is likely to be valued at US$20.9 billion in 2026, and is expected to reach US$25.2 billion by 2033, growing at a CAGR of 2.7% during the forecast period from 2026 to 2033, driven by the increasing prevalence of processed food consumption, rising demand for clean-label preservatives, and advancements in specialty salt formulations.

Growing demand for high-purity, functional food-grade salt, especially sodium chloride in food processing, is accelerating adoption across applications. Advances in low-sodium and mineral-enriched variants are further boosting uptake by offering more health-focused options. Increasing recognition of food-grade salt as critical for flavor enhancement and shelf-life extension in emerging markets remains a major driver of market growth.

Key Industry Highlights:

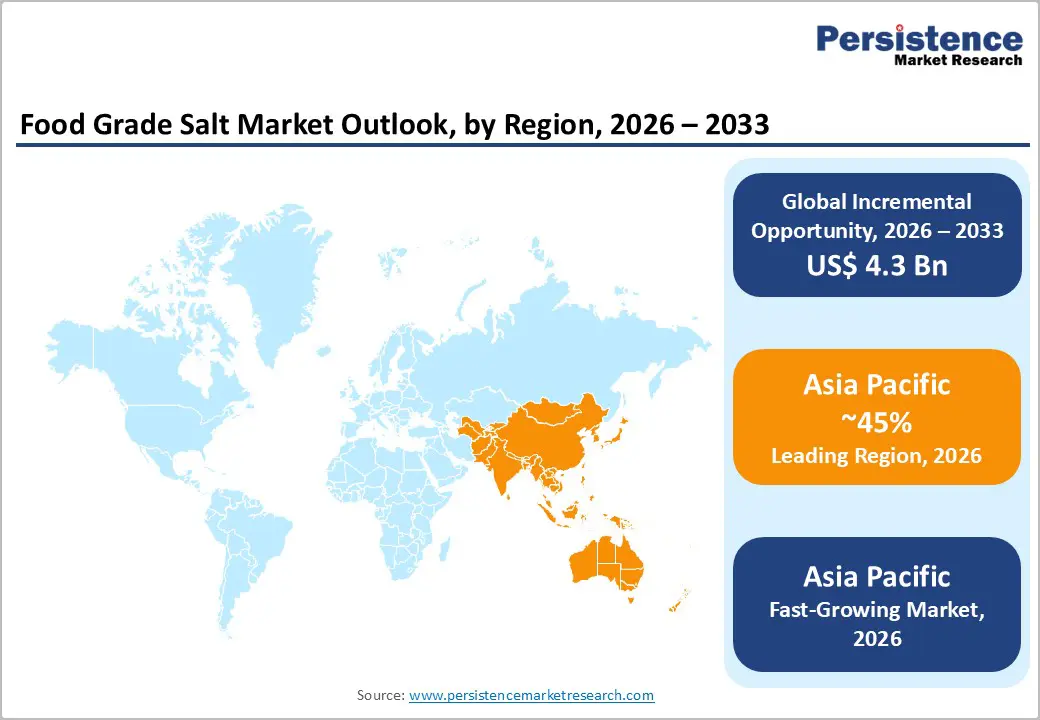

- Leading Region: Asia Pacific, anticipated to account for a 45% market share in 2026, driven by massive food processing growth, high population, and strong demand in China and India.

- Fastest-growing Region: Asia Pacific, fueled by urbanization, rising packaged food sales, and growing investments in food manufacturing.

- Dominant Salt Type: Sodium chloride, to hold approximately 80% of the market share in 2026, as it provides essential flavor and preservation.

- Leading Application: Food processing, accounting for over 50% of market revenue in 2026, due to its role in seasoning and preservation.

- Leading Distribution Channel: Distributors, to contribute nearly 40% of the market revenue in 2026, due to bulk supply to industrial users.

| Key Insights | Details |

|---|---|

| Food Grade Salt Market Size (2026E) | US$20.9 Bn |

| Market Value Forecast (2033F) | US$25.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 2.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Processed Food Consumption

The rising prevalence of processed food consumption is a significant global trend shaped by changing lifestyles, urbanization, and evolving consumer preferences. As work schedules become increasingly demanding, consumers are gravitating toward foods that offer convenience, longer shelf life, and minimal preparation time. Ready-to-eat meals, packaged snacks, frozen foods, and instant products fit well into fast-paced daily routines, making them a preferred choice across both developed and developing economies.

Growth in disposable incomes, especially among urban populations, has further supported this shift by increasing access to branded and value-added food products. Aggressive marketing, attractive packaging, and widespread retail availability through supermarkets, convenience stores, and e-commerce platforms have also enhanced the visibility and appeal of processed foods. Advancements in food processing technologies have improved taste, texture, and consistency, helping processed foods closely match consumer expectations for quality and flavor.

Health Concerns over Sodium Intake

Health concerns about sodium intake are a major restraint on the food-grade salt market, driven by growing awareness of the link between high salt consumption and chronic health conditions. Excessive sodium intake is widely associated with elevated blood pressure, which significantly raises the risk of heart disease, stroke, and other cardiovascular disorders. As these conditions become more prevalent globally, consumers are becoming more cautious about their daily salt intake and overall dietary habits.

Public health campaigns and dietary guidelines issued by health authorities increasingly emphasize sodium reduction as a preventive health measure. This has encouraged consumers to read nutritional labels more carefully and limit the use of added salt in home cooking and packaged foods. The demand for conventional food-grade salt is being indirectly constrained, particularly in mature markets with high health awareness. Food manufacturers are also responding to these concerns by reformulating products to contain lower sodium levels or by using alternative flavor enhancers to maintain taste. Such reformulation efforts reduce the overall volume of food-grade salt used in processed foods.

Advancements in Low-Sodium and Specialty Delivery Platforms

Advancements in low-sodium and specialty food-grade salt delivery platforms are transforming the global seasoning landscape by addressing two major challenges: sodium reduction barriers and flavor loss. Low-sodium platforms are engineered to achieve a 30-50% reduction in sodium, reducing reliance on full-sodium salt and enabling health claims in processed foods. Innovations, such as potassium blends, mineral fortification, crystal modification, and flavor enhancers, significantly improve taste and reduce hypertension risks, lowering reformulation costs for brands and consumer campaigns.

Progress in specialty platforms, including Himalayan pink salt, sea salt flakes, smoked variants, and organic grades, supports a more premium positioning by stimulating gourmet appeal, the product’s first line of defense against commoditization. These formats eliminate blandness, enhance visual appeal, and allow versatile use without additives, making them highly suitable for mass bakery programs. New technologies such as micro-encapsulation, bio-adhesive crystals, and VLP-based blending further enhance flavor and health response.

Category-wise Analysis

Salt Type Insights

Sodium chloride is expected to dominate the market, accounting for roughly 80% of revenue in 2026. Its widespread use is driven by its essential flavor-enhancing and preservative properties, combined with cost-effectiveness, making it a preferred choice in food processing. Sodium chloride offers versatile functionality, affordability, and high-volume availability, making it ideal for large-scale food production. For example, Morton® TOP FLAKE Topping Salt, a food-grade sodium chloride product, is formulated to provide strong adhesion and uniform salt distribution in baked goods, cured meats, and other processed foods, demonstrating how sodium chloride remains a functional and economical staple in commercial food manufacturing.

Potassium chloride is likely to be the fastest-growing segment, owing to its low-sodium profile and rising use in health-conscious products. Its heart-friendly properties make it an attractive option for sodium reduction, helping to mitigate hypertension risks. Innovations in flavor blending have improved its taste, accelerating adoption across North America and Europe, where demand for reduced-sodium alternatives is rising. Cargill Salt’s Potassium Pro® Ultra Fine Potassium Chloride exemplifies such innovation, offering food manufacturers a healthful solution to lower sodium content while boosting potassium levels in their products.

Application Insights

The food processing segment is projected to lead the market, capturing approximately 50% of revenue in 2026. This growth is driven by the need for preservation and seasoning, large-scale industrial programs, and strong global demand for processed foods. Its dominance is reinforced as manufacturers continue to expand packaged product lines. Increasing adoption in dairy fortification and extended bakery initiatives highlights the growing focus on multi-sector applications. Cargill, a global leader in food ingredients, supplies a broad portfolio of food processing salts used by major manufacturers. These products are designed to enhance flavor, improve texture, regulate fermentation, and extend shelf life across a variety of applications, including bread, cheese, deli meats, sauces, and snacks, demonstrating salt’s functionality beyond simple seasoning in food production.

The pharmaceutical segment is expected to be the fastest-growing, driven by rising use as an excipient and expanding inclusion in formulations. The shift toward clean excipient platforms and higher-purity products is accelerating adoption. Advances in pharmaceutical-grade salts and the continued development of tablet blends undergoing regulatory trials are fueling market growth. K+S Aktiengesellschaft is a leading supplier of pharmaceutical-grade sodium and potassium chloride tailored for the industry. Its high-purity products, such as APISAL® sodium chloride (GMP quality) and potassium chloride 99.9% Ph.Eur./USP, are widely used as excipients and active pharmaceutical ingredients in critical drug formulations, intravenous solutions, dialysis fluids, and electrolyte infusions. Manufactured under strict quality controls to meet and exceed international pharmacopoeia standards (USP, EP, BP), K+S’s pharmaceutical salts are trusted by drug manufacturers worldwide to ensure formulation stability and patient safety.

Distribution Channel Insights

Distributors are projected to lead, accounting for nearly 40% of the revenue share in 2026. Their dominance stems from serving as the central hub for bulk supply, managing large B2B programs, and handling industrial volumes that require consistent, reliable delivery. Strong logistics capabilities, trained networks, and expertise in managing high-volume or specialized blends drive higher consumption. Distributors are at the forefront of industrial rollouts and also support emerging retail trials. For example, Morton Salt, a major producer and marketer, maintains an extensive network of approved independent distributors across the U.S., supplying bulk and packaged food-grade salt to industrial and commercial customers. These distributors ensure timely delivery and continuity of regional supply for food processors, food service companies, and industrial buyers.

Online platforms are expected to be the fastest-growing segment, fueled by their strong digital presence and expanding role in direct-to-consumer sales. They provide convenient, quick, and easily accessible purchasing options, appealing to buyers who prefer low-contact or home delivery solutions. Increased e-commerce initiatives, broader product availability, and a focus on both routine and premium salts are accelerating adoption, particularly in urban and semi-urban areas. Platforms such as Flipkart, BigBasket, Amazon, and Zepto have become key channels for salt purchases in India, offering consumers a wide range of options, from standard iodized salts to premium and specialty products such as rock and Himalayan pink salt, enabling easy browsing, comparison, and home delivery.

Regional Insights

North America Food Grade Salt Market Trends

North America’s market growth is driven by the region’s advanced food processing infrastructure, robust research and development capabilities, and high consumer awareness of the benefits of sodium reduction. Well-developed processing systems in the U.S. and Canada support extensive salt programs, ensuring the broad availability of food-grade salt across food & beverage, pharmaceutical, and other industries. Rising demand for low-sodium, convenient, and easy-to-use salt formats is further accelerating adoption, as these solutions promote health and help overcome challenges associated with high-sodium diets.

Ongoing innovations in food-grade salt technology, including stable potassium blends, enhanced purity, and targeted functional improvements, are attracting substantial investments from both public and private sectors. Government initiatives and health-focused campaigns continue to encourage sodium reduction, address hypertension, processed-food risks, and broader wellness concerns, thereby supporting sustained market demand. The increasing focus on pharmaceutical-grade and specialty applications, particularly in bakery and other segments, is expanding the range of opportunities for food-grade salt.

Europe Food Grade Salt Market Trends

Europe’s market growth is driven by increasing awareness of health benefits, strong food systems, and government-led sodium reduction programs. Countries such as Germany, France, and the U.K. have well-established nutrition frameworks that encourage routine salt use and the adoption of innovative delivery formats, including food-grade salt. These carefully managed formulations are especially appealing to food manufacturers, health-conscious consumers, and pharmaceutical users, supporting better compliance and coverage.

Technological advancements in food-grade salt, such as low-sodium blends, application-specific delivery systems, and specialty grades, are further enhancing market potential. European authorities are actively promoting research and trials to optimize salt for both standard and specialized uses, boosting confidence across the market. The growing emphasis on convenient, reduced-sodium options aligns with preventive health goals and efforts to lower cardiovascular risks. Public awareness campaigns and promotional initiatives are expanding reach in both urban and rural areas, while suppliers continue to invest in refining and innovating products to improve performance and effectiveness.

Asia Pacific Food Grade Salt Market Trends

Asia Pacific is expected to be both the largest and fastest-growing market, accounting for approximately 45% of the share in 2026. Growth is driven by rising awareness of processed foods, increasing government initiatives, and expanding application programs across the region. Countries such as India, China, Japan, and Southeast Asian nations are actively promoting salt campaigns to support industrial food production and address emerging health needs. Food-grade salt is particularly appealing in these markets due to its essential functionality, scalability, and suitability for large-scale processing in both urban and rural areas.

Technological advancements are enabling the development of stable, efficient, and easy-to-use food-grade salt that performs reliably under challenging production conditions while minimizing contamination risks. These innovations are especially important for reaching remote facilities and improving overall quality coverage. Strong demand across food & beverage, pharmaceuticals, and other applications is further driving market expansion. Public-private partnerships, increased food expenditure, and rising investments in refining technologies and manufacturing capacity are accelerating growth, while improved purity and convenient delivery position food-grade salt as a preferred choice across the region.

Competitive Landscape

The global food-grade salt market features competition between established mining leaders and emerging specialty suppliers. In North America and Europe, Cargill Incorporated and K+S AG lead through strong R&D, distribution networks, and industry ties, bolstered by innovative grades and supply programs. In the Asia Pacific, China National Salt Industry Corporation advances with localized solutions, enhancing accessibility. Low-sodium delivery boosts health, cuts risks, and enables mass integrations across regions. Strategic partnerships, collaborations, and acquisitions merge expertise, expand mining operations, and accelerate commercialization. Specialty formulations solve sodium issues, aiding penetration in health-focused areas.

Key Industry Developments

- In March 2025, The Michigan Potash & Salt Co. (Michigan Salt) announced the launch of a new salt business, planning to produce 1 million tons of food-quality salt at a strategic location within a high-demand region of the U.S.

- In May 2024, ITC Aashirvaad Salt introduced its new Himalayan Pink Salt, also known as Sendha Namak or Saindhava Lavana in India, sourcing it naturally from Himalayan salt mines.

Companies Covered in Food Grade Salt Market

- Cargill Incorporated

- K+S AG

- Compass Minerals

- Morton Salt

- Tata Chemicals

- Dampier Salt

- Salinen Austria AG

- China National Salt Industry Corporation

Frequently Asked Questions

The global food grade salt market is projected to reach US$20.9 billion in 2026.

The rising prevalence of processed food consumption and demand for clean-label preservatives are the key drivers.

The food grade salt market is poised to witness a CAGR of 2.7% from 2026 to 2033.

Advancements in low-sodium and specialty delivery platforms are key opportunities.

Cargill Incorporated, K+S AG, Compass Minerals, Morton Salt, and Tata Chemicals are the key players.