- Healthcare

- Global Prolotherapy Market

Global Prolotherapy Market Size, Share, and Growth Forecast 2026 - 2033

Prolotherapy Market by Product Type (Dextrose, Platelet Rich Plasma, Bicellular prolo), by Application (Joint Injection Prolotherapy, Ligament Prolotherapy, Tendon Reconstruction Prolotherapy), by End-user, by Regional Analysis, 2026-2033.

Prolotherapy Market Size and Trend Analysis

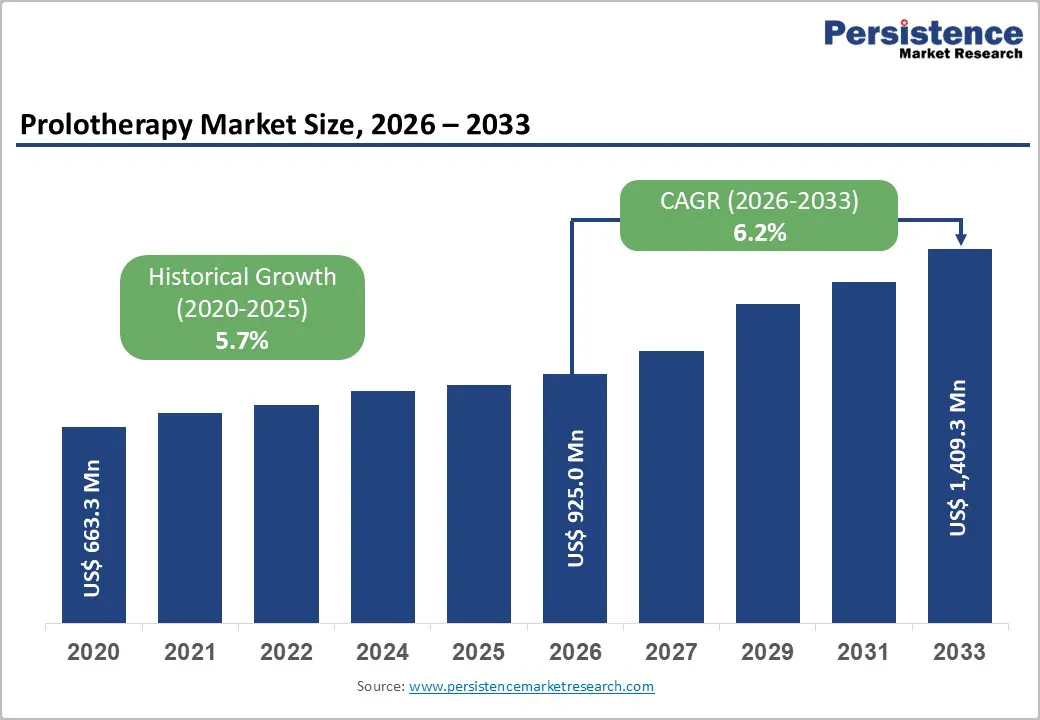

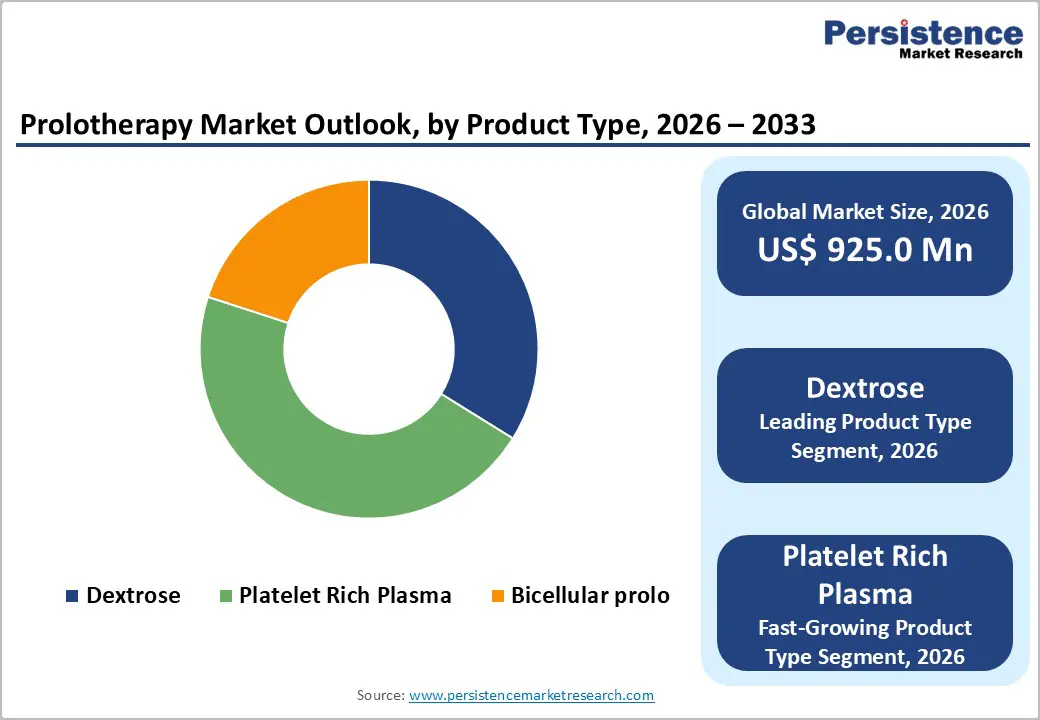

The global prolotherapy market size is expected to be valued at US$ 925.0 million in 2026 and projected to reach US$ 1,409.3 million by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

Prolotherapy, also known as proliferation or regenerative therapy, involves injecting a natural irritant into the body to stimulate the healing process and promote normal cell growth. The procedure includes growth factor injections, growth factor stimulation, and controlled inflammation to form healthy tissue. Typically performed as an outpatient procedure under local or general anesthesia, multiple prolotherapy injections target areas of musculoskeletal pain, commonly in joints affected by arthritis. According to the National Institutes of Health (NIH), knee pain affects 32.2% of men and 58% of women with arthritis, highlighting a significant patient population for treatment.

The global prolotherapy market is expected to grow steadily, driven by rising geriatric populations, increasing diagnosis and treatment adoption, changing lifestyles, and higher obesity prevalence. Technological advancements and R&D investments, including FDA approvals for products like dextrose injections, support market expansion. However, COVID-19-related procedural delays, limited adoption in underdeveloped regions, and potential side effects such as infection or needle injuries pose challenges to growth.

Key Industry Highlights

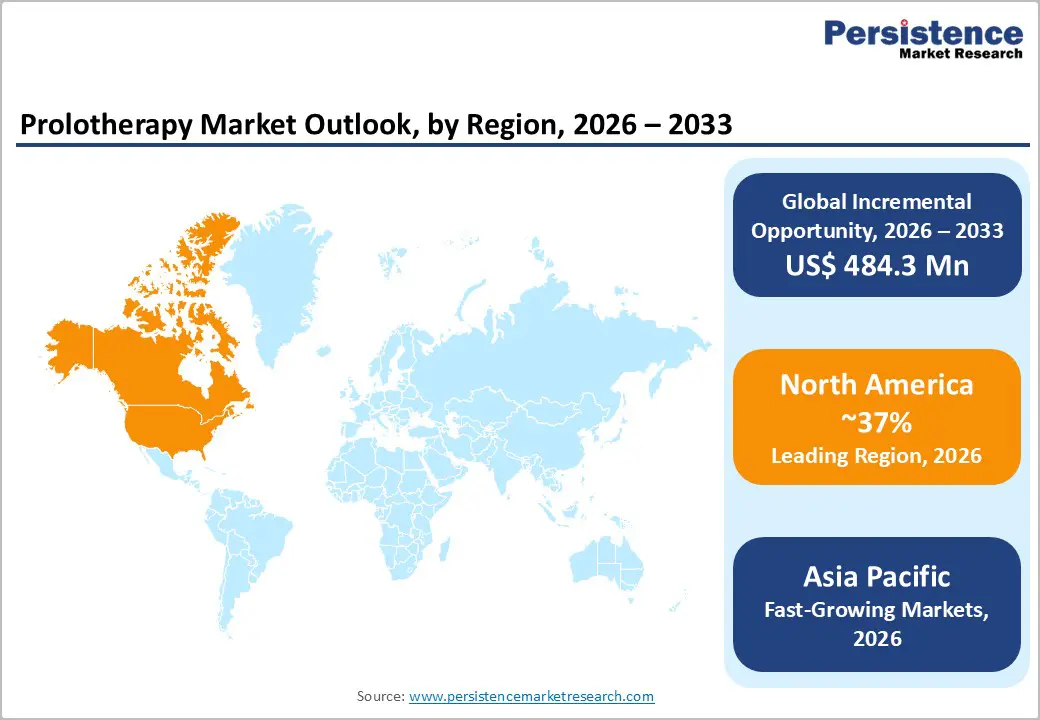

- Leading Region: North America leads the global prolotherapy market, supported by high healthcare expenditure, strong sports medicine and orthopedic infrastructure, and early adoption of regenerative injection therapies.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by rapid population aging, rising osteoarthritis and sports injury prevalence, expanding private healthcare facilities, and growing awareness of non-surgical pain management options.

- Dominant Segment: Dextrose-based prolotherapy is the dominant product segment, owing to its long clinical history, low cost, favorable safety profile, and wide use in osteoarthritis and chronic musculoskeletal pain management.

- Fastest Growing Segment: Platelet-rich plasma (PRP) prolotherapy is the fastest-growing segment, supported by increasing use in sports medicine, rising interest in biologic regenerative treatments, and expanding clinical evidence for tendon and ligament repair.

| Global Market Attributes | Key Insights |

|---|---|

| Prolotherapy Market Size (2026E) | US$ 925.0 Mn |

| Market Value Forecast (2033F) | US$ 1,409.3 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.2% |

| Historical Market Growth (CAGR 2020 to 2024) | 5.7% |

Market Dynamics

Driver – Growing musculoskeletal disease burden and preference for non-surgical therapies

A key driver of the global prolotherapy market is the rising burden of musculoskeletal disorders, particularly osteoarthritis, tendon injuries, and ligament damage, which affect millions worldwide and are among the leading causes of disability. Patients with chronic joint pain often seek treatments that avoid invasive surgeries, long-term opioid use, or joint replacement. Clinical studies demonstrate that hypertonic dextrose prolotherapy can significantly reduce pain and improve function. For example, a study involving 92 knee osteoarthritis patients reported a decrease in VAS pain scores from 7.12 to 3.06 and halving of WOMAC scores over 24 weeks without serious adverse effects. Such evidence highlights the effectiveness of injectable regenerative therapies in outpatient orthopedic and rehabilitation settings, where procedures are repeatable and minimally disruptive.

Another growth driver is the increasing adoption of platelet-rich plasma (PRP) in tendon and ligament pathologies, supporting the broader concept of regenerative prolotherapy. Meta-analyses involving over 1,000 participants indicate that PRP injections reduce pain by 0.7–0.8 points on standardized VAS scales, particularly in rotator cuff, ACL, and lateral epicondylitis injuries. Annually, more than 86,000 athletes in the U.S. and Europe receive PRP, illustrating growing acceptance among clinicians. This trend fosters familiarity with prolotherapy techniques and encourages wider adoption of both dextrose and PRP-based injections across general and sports medicine practices.

Restraints – Limited guideline endorsement and heterogeneous evidence base

A significant restraint for the prolotherapy market is the limited endorsement in clinical guidelines and the heterogeneous quality of supporting evidence. While studies suggest benefits for pain relief and functional improvement, many systematic reviews emphasize the high risk of bias, small sample sizes, and variable study designs. For instance, dextrose prolotherapy for knee osteoarthritis shows promise but lacks robust randomized controlled trials to warrant broad guideline recommendation. Similarly, professional associations and payer policies highlight insufficient evidence for indications such as low back pain, limiting coverage and reimbursement.

This cautious stance affects routine clinical integration, particularly in regions with strict insurance and procedural approval frameworks. The lack of standardized treatment protocols, variations in injection techniques, and inconsistent reporting of outcomes further constrain adoption among healthcare providers. Consequently, many patients continue to rely on conventional therapies or conservative management, which delays market expansion. Additionally, concerns over procedural safety, including potential injection-site reactions or minor complications, contribute to clinician hesitation, particularly in underdeveloped regions where training and oversight may be limited. These factors collectively restrain the global proliferation of prolotherapy despite growing interest in regenerative treatment approaches.

Opportunity – Emerging clinical data in osteoarthritis and chronic joint pain

The global prolotherapy market presents substantial opportunities through emerging clinical evidence supporting its efficacy in osteoarthritis and chronic joint pain. Recent systematic reviews and prospective cohort studies from 2021 to 2024 show that hypertonic dextrose injections significantly reduce pain and improve function in patients with early to moderate knee osteoarthritis. Evidence indicates that benefits can be achieved within 4–24 weeks, offering a non-surgical, low-risk alternative to conventional treatments. These findings enable market participants to build credibility and confidence among orthopedic and rheumatology practitioners, encouraging broader adoption in hospitals, ambulatory care centers, and specialized orthopedic clinics.

Another opportunity lies in the development of standardized prolotherapy formulations and delivery systems. Companies producing prefilled syringes, consistent dextrose concentrations, and training programs for clinicians can simplify procedural application, improve reproducibility, and expand the addressable patient population. Additionally, the rising prevalence of musculoskeletal disorders, growing awareness of regenerative therapies, and increasing acceptance of outpatient procedures provide favorable conditions for market growth. Leveraging clinical data, expanding educational initiatives, and integrating prolotherapy into value-based care models can help manufacturers and service providers capture incremental market share, particularly in regions with emerging orthopedic and sports medicine infrastructure.

Category-wise Analysis

By Product Type Analysis

Within the product type segment, dextrose remains the dominant choice in the global prolotherapy market due to its established clinical history, cost-effectiveness, and favorable safety profile. Hypertonic dextrose solutions are widely used in the management of knee osteoarthritis, low back pain, and peripheral joint or ligament injuries. Multiple randomized controlled trials and prospective cohorts have demonstrated that dextrose injections provide meaningful improvements in pain and functional outcomes compared with saline or exercise alone. Systematic reviews support its use as a safe adjunct therapy, reporting reductions in WOMAC scores and improved patient mobility without major adverse events. Dextrose is easy to prepare, has regulatory familiarity, and integrates smoothly into existing prolotherapy protocols. Its versatility in treating diverse musculoskeletal conditions, combined with evidence-based effectiveness and low complication risk, reinforces its position as the leading product type, forming the backbone of prolotherapy treatments in hospitals, outpatient clinics, and specialized orthopedic centers.

By End-user Analysis

Hospitals are the leading end-user segment for prolotherapy, reflecting their capacity to manage complex musculoskeletal cases and provide coordinated multidisciplinary care. Facilities often combine rheumatology, orthopedics, sports medicine, and pain management departments, enabling comprehensive assessment and image-guided injections for patients with advanced joint degeneration or multiple comorbidities. Academic and research hospitals play a key role in generating clinical evidence through randomized trials and prospective studies that evaluate dextrose and PRP efficacy, particularly in conditions such as knee osteoarthritis. This early adoption in hospitals helps standardize treatment protocols and fosters clinical confidence in prolotherapy techniques. Additionally, hospitals offer advanced procedural support, postoperative monitoring, and rehabilitation services, making them suitable for more complex or high-risk patients. While ambulatory care centers and specialty clinics are expanding access for routine injections, hospitals remain central to market growth due to their expertise, infrastructure, and role in early adoption of innovative regenerative therapies.

Region-wise Insights

North America Prolotherapy Market Trends

North America represents a mature and well-established prolotherapy market, led by the U.S. due to high healthcare spending, strong orthopedic and sports medicine infrastructure, and early acceptance of regenerative injection therapies. Prolotherapy is commonly offered in sports medicine clinics, pain management centers, and academic hospitals, particularly for tendon, ligament, and joint disorders. The widespread use of platelet-rich plasma in athletic and rehabilitation settings has increased familiarity with biologic injections, supporting broader adoption of prolotherapy concepts. Academic institutions and integrated health systems continue to evaluate dextrose and PRP-based protocols for osteoarthritis and chronic musculoskeletal pain, often alongside structured physiotherapy programs. Reimbursement remains selective, with some payers classifying prolotherapy as investigational for certain indications, influencing adoption patterns. However, ongoing clinical studies, professional training programs, and continuing medical education initiatives are steadily strengthening the regional provider base and supporting incremental market expansion.

Asia and Pacific Prolotherapy Market Trends

Asia Pacific is emerging as the fastest-growing prolotherapy market, driven by rapid population aging, increasing sports participation, and expanding private healthcare infrastructure. Countries such as China, Japan, India, and several ASEAN nations are witnessing rising demand for non-surgical management of osteoarthritis and soft-tissue injuries. Growing awareness among patients and clinicians has led to wider use of dextrose and PRP injections in orthopedic and sports medicine centers, particularly in major urban hubs. Clinical studies conducted within the region have demonstrated meaningful pain reduction and functional improvement with hypertonic dextrose prolotherapy, strengthening confidence in its application. Cost-effective local manufacturing of injectables and procedural kits supports affordability and access, while private hospitals increasingly incorporate regenerative injections into comprehensive musculoskeletal care packages. In addition, medical tourism destinations in Asia Pacific are leveraging prolotherapy as part of differentiated orthopedic offerings, contributing to rapid procedural growth across the region.

Market Competitive Landscape

The prolotherapy market is moderately fragmented, with a mix of large multinational pharmaceutical and medical device companies supplying injectables and kits, alongside numerous regional manufacturers and specialized PRP system providers. Major firms such as Pfizer Inc., Baxter International, B. Braun, Johnson & Johnson, Terumo Corporation, and Aurobindo Pharma participate via dextrose solutions, local anesthetics, and injection devices that are used in prolotherapy protocols, while niche players focus on PRP preparation systems and regenerative medicine kits for orthopedic and sports clinics. Competitive strategies emphasize product safety, ease of preparation, standardized platelet concentration, and clinical education partnerships with hospitals and academic institutes, along with emerging business models that bundle consumables with training and technical support.

Key Industry Developments:

- In June 2025, The University of Bridgeport, Goodwin University, and TulsiHub Institute jointly introduced a CE-certified regenerative medicine training program in the U.S. to enhance clinician skills in prolotherapy and related regenerative injection therapies.

Companies Covered in Global Prolotherapy Market

- Pfizer Inc.

- Baxter International

- B. Braun

- Johnson & Johnson

- Arthex Inc.

- Terumo Corporation

- Aurobindo Pharma

- Shandong Qidu Pharmaceuticals

- Amphastar Pharmaceuticals Inc.

- Sanctus drugs & Pharmaceuticals

- Hospira Pharmaceutical Company

- Others

Frequently Asked Questions

The global market is projected to be valued at US$ 925.0 Mn in 2026.

Rising musculoskeletal disorders, preference for non-surgical pain management, aging populations, sports injuries, and expanding regenerative medicine adoption.

The global market is poised to witness a CAGR of 6.2% between 2026 and 2033.

Growing clinical evidence, expansion in emerging markets, standardized formulations, outpatient adoption, and integration into orthopedic care pathways.

Key companies include Pfizer Inc., Baxter International, B. Braun, Johnson & Johnson, and Arthex Inc.