- Industrial Machinery

- Powder Bed Fusion Market

Powder Bed Fusion Market Size, Share, and Growth Forecast, 2026 - 2033

Powder Bed Fusion Market by Material Type (Metals, Polymers, Ceramics), Application (Aerospace & Defense, Automotive, Healthcare, Industrial, Consumer Goods, Education & Research), and Regional Analysis for 2026 - 2033

Powder Bed Fusion Market Size and Trends Analysis

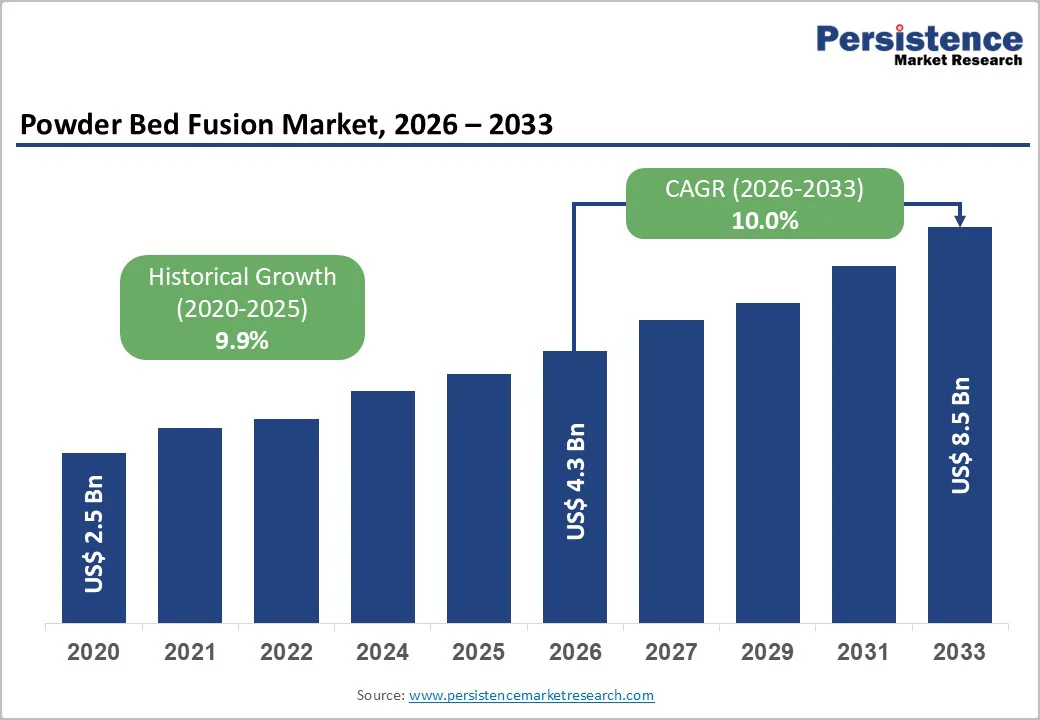

The global powder bed fusion market size is likely to be valued at US$4.3 billion in 2026 and is expected to reach US$8.5 billion by 2033, growing at a CAGR of 10.0% during the forecast period from 2026 to 2033, driven by the rising adoption of additive manufacturing for high-performance, lightweight, and geometrically complex components, particularly in the aerospace, defense, and automotive industries.

Continuous technological advancements in laser- and electron-beam-based powder bed fusion (PBF) systems, including multi-laser architectures, improved process monitoring, and broader material compatibility, are enhancing production speed, accuracy, and repeatability. Increasing demand for patient-specific medical implants, prostheses, and surgical instruments is accelerating the adoption of PBF in the healthcare sector.

Key Industry Highlights:

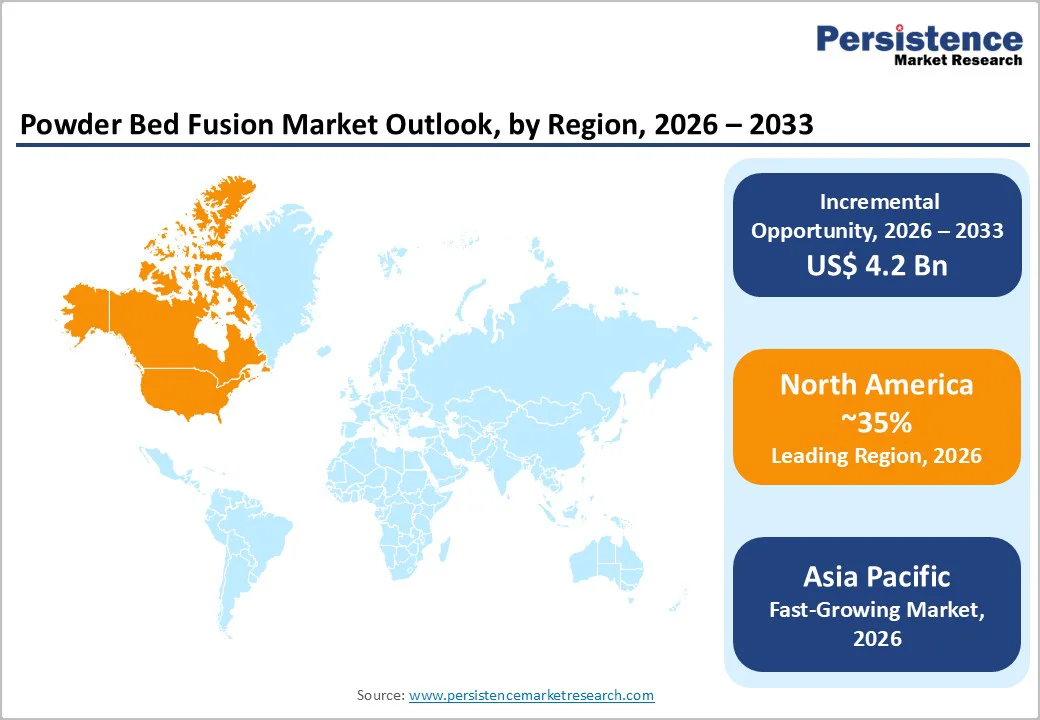

- Leading Region: North America is expected to be the leading region, accounting for 35% market share in 2026, driven by strong adoption in aerospace and healthcare, advanced R&D infrastructure, supportive regulatory frameworks, and the presence of major industry players fostering continuous innovation.

- Fastest-growing Region: Asia Pacific is expected to be the fastest-growing region for powder bed fusion technologies in 2026, driven by large-scale manufacturing in China and Japan and rising demand in the aerospace and medical sectors in India.

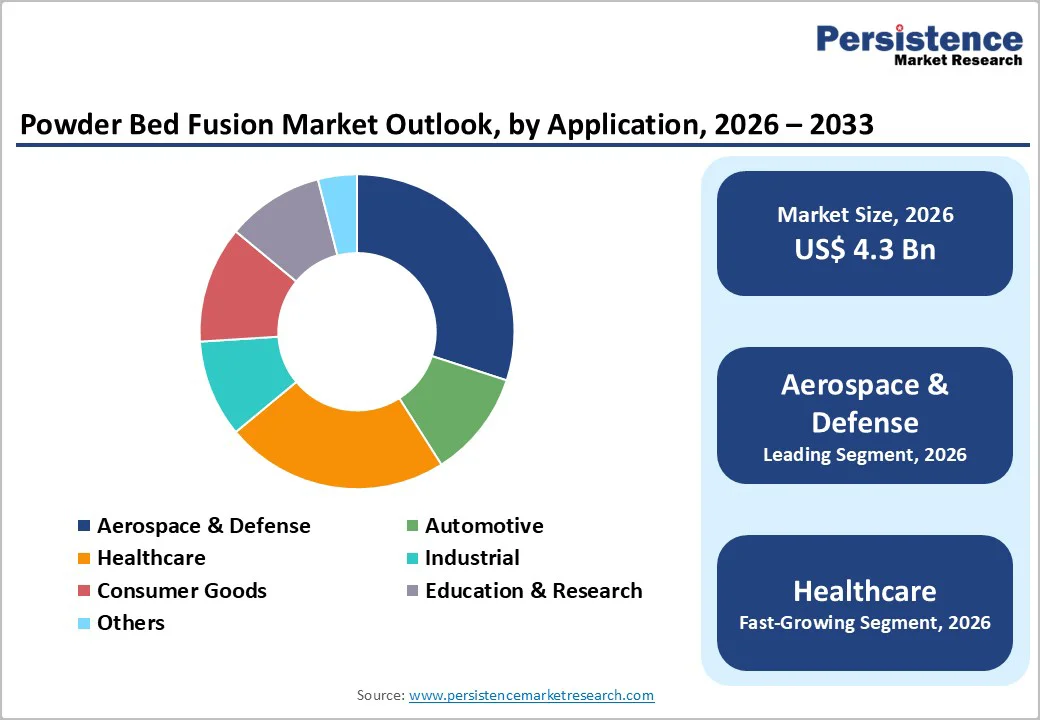

- Leading Material Type: Metals are projected to be the leading material type in 2026, accounting for 60% of revenue share, driven by high-performance applications in aerospace, defense, and automotive that require strength and durability.

- Leading Application: Aerospace & defense is expected to be the leading application type, accounting for over 40% of revenue share in 2026, driven by strong demand for lightweight, complex, and certified components.

| Key Insights | Details |

|---|---|

|

Powder Bed Fusion Market Size (2026E) |

US$4.3 Bn |

|

Market Value Forecast (2033F) |

US$8.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

10.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

9.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Demand for Lightweight and Complex Geometries in Aerospace and Defense

Manufacturers seek to improve fuel efficiency, payload capacity, and overall system performance. Powder bed fusion enables the production of highly intricate, topology-optimized components that significantly reduce part weight while maintaining structural integrity. Aerospace OEMs increasingly rely on PBF to consolidate multiple parts into a single complex assembly, minimizing fasteners, reducing failure points, and lowering overall production and maintenance costs. The ability to manufacture internal channels, lattice structures, and thin-walled designs makes powder bed fusion especially valuable for aircraft engines, structural brackets, and defense components where precision and performance are critical.

The aerospace and defense industry places strong emphasis on material performance and certification, areas where powder bed fusion has made substantial progress. Advanced metal powders such as titanium and aluminum alloys offer exceptional strength-to-weight ratios, corrosion resistance, and thermal stability, aligning with stringent aerospace standards. Improvements in process control, repeatability, and in-situ monitoring have enhanced part quality and reliability, accelerating certification and adoption for flight-critical components. Defense agencies and aerospace manufacturers pursue next-generation platforms.

Throughput and Scalability Constraints of Powder Bed Fusion

Powder bed fusion (PBF) is a layer-by-layer, point-based process, which inherently slows it down compared to conventional manufacturing methods such as casting or machining. Even with advances such as multi-laser configurations, build times remain long for large or high-density parts, limiting throughput and increasing per-unit costs. As a result, PBF is less suited to mass production and is primarily used for low- to medium-volume, high-value components, where design complexity and performance benefits justify longer production cycles. Additional factors such as extended cooling periods, scan strategy constraints, and layer-by-layer powder recoating further slow overall production.

Machine size constraints, powder handling complexity, and extensive post-processing requirements further limit scalability. Larger build volumes demand higher energy output, precise thermal control, and consistent powder distribution, increasing system cost and operational complexity. Post-processing steps, including heat treatment, support removal, and surface finishing, add significant time and labor, reducing manufacturing efficiency. Maintaining quality consistency across larger builds also requires advanced monitoring and validation systems. Although automation and parallel processing are being developed to address these challenges, achieving high-volume production with PBF remains a significant barrier to broader industrial adoption.

Integration with Digital Technologies and Hybrid Manufacturing

Modern powder bed fusion (PBF) systems are increasingly integrated with advanced digital technologies, including software platforms, digital twins, artificial intelligence, and real-time process monitoring, to improve build accuracy, consistency, and quality control. End-to-end digital workflows, from design and simulation to in-situ monitoring and post-processing, enable predictive maintenance, minimize downtime, and accelerate part qualification. These capabilities are particularly valuable in highly regulated sectors such as aerospace and healthcare, where traceability and process validation are essential. As manufacturers move toward smart factories and data-driven production, digitally enabled PBF systems are becoming a cornerstone of next-generation manufacturing strategies.

Hybrid manufacturing, which combines PBF with subtractive methods such as CNC machining, further expands production possibilities. This approach allows near-net-shape components to be additively built and then precisely finished in a single workflow, reducing lead times and enhancing dimensional accuracy. Hybrid systems are particularly advantageous for complex metal parts that require tight tolerances and superior surface quality. By embedding PBF into hybrid and digitally connected manufacturing ecosystems, companies can boost productivity, minimize material waste, and support scalable, flexible production, driving broader adoption of powder bed fusion technologies over the long term.

Category-wise Analysis

Material Type Insights

The metals segment is projected to dominate the powder bed fusion market, contributing around 60% of total revenue by 2026. This leadership is driven by the widespread adoption of metal PBF in high-value, performance-critical applications. Industries such as aerospace, defense, and automotive depend heavily on metal PBF for producing lightweight yet structurally strong components with complex internal designs. Titanium and aluminum alloys are the most widely used materials in this segment due to their excellent strength-to-weight ratios, corrosion resistance, and thermal stability. Compared with conventional machining, metal PBF supports part consolidation, minimizes material waste, and enhances overall functional performance. A notable example is GE Aviation, which employs metal PBF to produce jet engine fuel nozzles, achieving substantial weight reduction and consolidating multiple parts into a single component, underscoring the metals segment’s significant revenue contribution within the PBF ecosystem.

The polymers segment is expected to be the fastest-growing segment by 2026, fueled by rapid progress in high-performance polymer powders and a widening range of end-use applications. Materials such as PA12, TPU, and reinforced composites are seeing increased adoption due to their design versatility, durability, and cost efficiency. Polymer powder bed fusion is extensively used for functional prototyping, low-volume manufacturing, and customized parts, making it especially appealing to the consumer goods, healthcare, and industrial sectors. Ongoing material innovations are enhancing mechanical strength, thermal stability, and biocompatibility, further driving market uptake. For instance, HP’s Multi Jet Fusion polymer technology is widely used in the production of customized medical devices and consumer products, underscoring the strong growth trajectory of polymers in the PBF market.

By Application Insights

The aerospace and defense segment is expected to lead the market, accounting for approximately 40% of total revenue by 2026, driven by strong demand for lightweight, complex, and high-performance components. Powder bed fusion allows the production of topology-optimized parts that reduce aircraft weight, enhance fuel efficiency, and improve overall operational performance. Its capability to create intricate internal structures, cooling channels, and consolidated assemblies makes PBF particularly valuable for aircraft engines, structural components, and defense systems. Ongoing investments in digital manufacturing and qualification frameworks further strengthen this segment’s market position. For instance, Boeing utilizes powder bed fusion to produce certified metal components for both commercial and military aircraft, highlighting aerospace and defense as the largest revenue-generating application area.

Healthcare is expected to be the fastest-growing application segment in 2026, driven by rising demand for patient-specific, customized medical solutions. Powder bed fusion allows precise production of implants, prosthetics, orthopedic devices, and surgical tools tailored to individual anatomy, enhancing outcomes and recovery. The technology’s compatibility with biocompatible metals and polymers, along with shorter lead times and localized production, boosts responsiveness and reduces inventory needs. For example, Materialise leverages PBF to create patient-specific orthopedic implants, highlighting healthcare as a rapidly expanding segment in the PBF market.

Regional Insights

North America Powder Bed Fusion Market Trends

North America is expected to lead the market, capturing a 35% share by 2026, driven by its well-established innovation ecosystem. The region benefits from substantial R&D investments, early adoption of industry best practices, and strong collaboration among OEMs, research institutions, and technology providers. Aerospace and defense continue to be the primary demand drivers, as manufacturers increasingly leverage PBF to produce lightweight, complex, and certified metal components that enhance fuel efficiency and performance. Supportive regulations and established qualification pathways further promote commercialization. For instance, GE Additive has expanded the use of metal PBF for aerospace engine components, while 3D Systems provides certified PBF solutions for defense and space applications, reinforcing North America’s dominance in high-value applications.

North America is witnessing a shift from prototyping to serial production, driven by advancements in multi-laser systems, automation, and process monitoring. Adoption in healthcare is also accelerating, with PBF increasingly used for patient-specific implants and surgical devices. Investments are focused on developing new materials, integrating software solutions, and scaling production to reduce costs and enhance throughput. Both startups and established companies are bolstering domestic manufacturing capabilities to strengthen supply chain resilience. For example, HP Inc. continues to advance polymer PBF solutions for industrial-scale production, while Materialise supports North American hospitals with customized PBF-based medical implants, underscoring the region’s diversification from aerospace into healthcare and industrial applications.

Europe Powder Bed Fusion Market Trends

Europe is expected to be a significant market for powder bed fusion (PBF) in 2026, driven by strong adoption across aerospace, automotive, and industrial manufacturing, supported by advanced engineering expertise and a mature additive manufacturing ecosystem. European manufacturers prioritize high-precision production, making PBF a preferred technology for complex and lightweight components. The region also benefits from coordinated research initiatives, cross-border collaborations, and robust standardization efforts, which accelerate industrial adoption. For example, Airbus utilizes metal PBF for structural aircraft components, while EOS GmbH provides advanced PBF systems and materials across Europe, reinforcing the region’s technological leadership.

Europe is increasingly integrating PBF into serial production and sustainable manufacturing strategies. Automotive OEMs are adopting PBF for lightweight components, tooling, and low-volume production, while industrial users leverage it for spare parts and digital inventories. Sustainability objectives drive interest in material efficiency and waste reduction, aligning with PBF’s advantages. Investments are focused on automation, process monitoring, and the development of new alloys to improve scalability. For instance, BMW has incorporated PBF into automotive component production, and Renishaw continues to expand metal PBF solutions for industrial and medical applications, highlighting Europe’s balanced growth across multiple end-use sectors.

Asia Pacific Powder Bed Fusion Market Trends

The Asia Pacific region is projected to be the fastest-growing market for powder bed fusion (PBF) in 2026, driven by robust manufacturing expansion, government-led industrialization initiatives, and rising adoption of advanced manufacturing technologies. Key sectors such as aerospace, automotive, and industrial are leveraging PBF to produce complex, lightweight, and high-precision components while minimizing material waste. Supportive government programs promoting domestic additive manufacturing and the localization of high-value components further accelerate market growth. For instance, Farsoon Technologies in China has expanded its metal and polymer PBF offerings for industrial and aerospace applications, while Japan’s Mitsubishi Heavy Industries employs PBF for advanced aerospace and energy components, demonstrating strong industrial uptake.

The region is also seeing increased participation from emerging economies, including India and ASEAN countries, where PBF adoption is growing across healthcare, education, and prototyping applications. Healthcare applications are expanding through patient-specific implants and medical devices, while universities and research institutions drive innovation and workforce development. Investments are increasingly focused on scaling production capacity, enhancing material quality, and improving automation. For example, India’s aerospace research organizations are utilizing PBF for indigenous component development, while Chinese medical device manufacturers employ polymer PBF for customized implants, reflecting the region’s diverse and rapidly evolving market landscape.

Competitive Landscape

The global powder bed fusion market exhibits a moderately fragmented structure, driven by rapid technology specialization, diverse end-use requirements, and rising demand across aerospace, automotive, and healthcare. With key leaders including EOS GmbH, 3D Systems, GE Additive, SLM Solutions, Renishaw, and Farsoon, the landscape blends long-standing OEMs, fast-scaling regional players, and materials specialists. The market comprises a mix of established global players and emerging regional manufacturers. Fragmentation is influenced by the presence of multiple technology variants and material specializations, allowing companies to focus on specific applications, performance requirements, and regional markets.

Market players compete by continuously innovating in machine architecture, materials development, and process automation, while investing in software integration and quality monitoring solutions. Strategic efforts, such as forming partnerships with end-use industries, expanding production-grade systems, and developing certified application workflows, are increasingly defining the competitive landscape. Companies are also prioritizing improvements in build speed, scalability, and cost efficiency to facilitate the shift from prototyping to serial production.

Key Industry Developments:

- In November 2025, Additive Industries announced the launch of its new flagship metal powder bed fusion system, the MetalFab 420K, aimed at addressing demanding industrial additive manufacturing applications. The automated and modular system is equipped with four 1 kW lasers, enabling significantly higher productivity while maintaining consistent material quality. The MetalFab 420K features full-field laser coverage across a 420 × 420 × 400 mm build volume, supporting high-throughput production for sectors such as aerospace, space, automotive, and high-tech manufacturing.

- In April 2025, metal additive manufacturing specialist ADDiTEC announced a significant expansion of its technology portfolio with the launch of the FUSiON S system at RAPID+TCT, marking its official entry into Laser Powder Bed Fusion (LPBF). With this addition, ADDiTEC joins a select group of global companies offering all three major metal 3D printing technologies, LPBF, Laser Directed Energy Deposition (LDED), and Liquid Metal Jetting (LMJ), further strengthening its position in the industrial metal additive manufacturing market.

Companies Covered in Powder Bed Fusion Market

- EOS GmbH

- 3D Systems Corporation

- SLM Solutions Group AG

- Renishaw plc

- GE Additive

- Trumpf GmbH + Co. KG

- Concept Laser GmbH

- ExOne Company

- Materialise NV

- HP Inc.

- Stratasys Ltd.

- Farsoon Technologies

- Desktop Metal Inc.

- Velo3D Inc.

- Xerion Advanced Battery Corporation

- Prodways Group

Frequently Asked Questions

The global powder bed fusion market is projected to reach US$4.3 billion in 2026.

The demand for lightweight, complex, and high-performance components is increasing across aerospace, automotive, healthcare, and industrial applications.

The powder bed fusion is expected to grow at a CAGR of 10.0% from 2026 to 2033.

The powder bed fusion market offers opportunities in healthcare for customized implants and medical devices, as well as in developing advanced metal and polymer materials for high-performance, complex components across multiple industries.

EOS GmbH, 3D Systems Corporation, SLM Solutions Group AG, Renishaw plc, and GE Additive are the leading players.