- Non-food Packaging

- Plastic Vials and Ampoules Market

Plastic Vials and Ampoules Market Size, Share, and Growth Forecast, 2026 - 2033

Plastic Vials and Ampoules Market By Material (Polyethylene, Polypropylene, Others), Product Type (Vials, Plastic Ampoules, Others), End-user, and Regional Analysis for 2026 - 2033

Plastic Vials and Ampoules Market Size and Trends Analysis

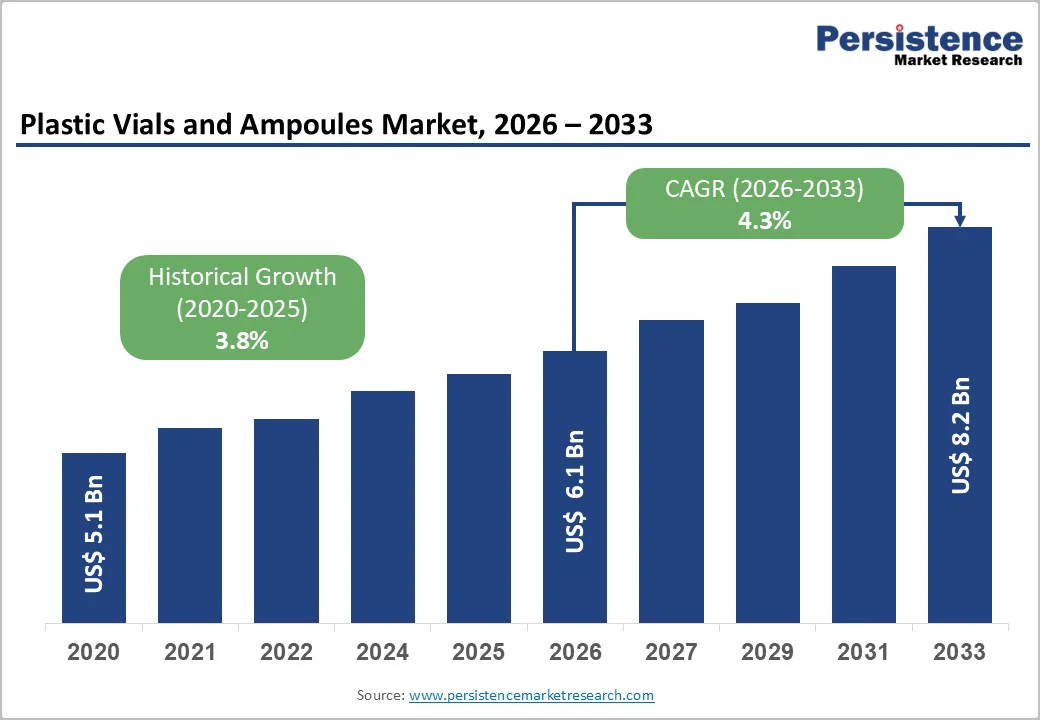

The global plastic vials and ampoules market size is likely to be valued at US$6.1 billion in 2026 and is expected to reach US$8.2 billion by 2033, growing at a CAGR of 4.3% between 2026 and 2033, driven by increasing demand for sterile and parenteral packaging, supported by pharmaceutical pipeline expansion, rising biologics adoption, and gradual substitution of glass with plastic formats.

Additional momentum comes from the growing use of prefilled and single-dose injectables, innovations in polymers such as COC, COP, and engineered polypropylene, and the expansion of contract manufacturing and fill-finish capacity in Asia Pacific. These factors are driving higher volumes and premiumization toward low-extractable polymer solutions, while ongoing cost sensitivity continues to support demand for commodity polyethylene and polypropylene.

Key Industry Highlights

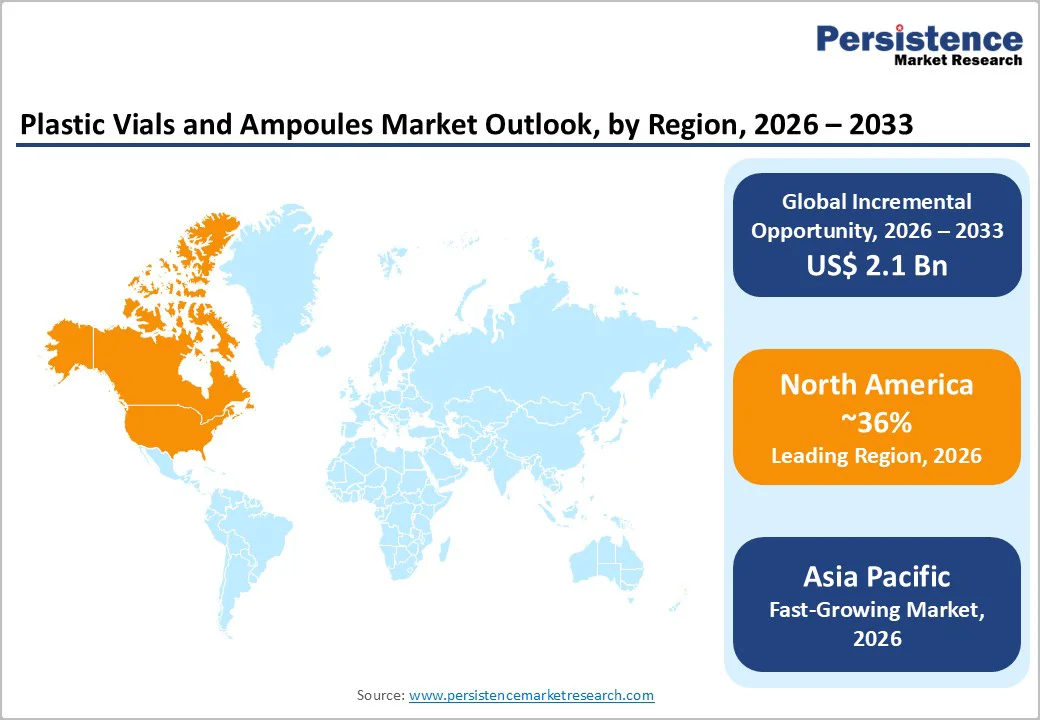

- Leading Region: North America is projected to account for approximately 36% of market share, supported by a strong pharmaceutical manufacturing base, advanced biotechnology activity, and high adoption of validated polymer packaging for sterile and parenteral applications.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing market, driven by capacity additions in China and India, increasing vaccine production, and rapid expansion of contract manufacturing and fill-finish infrastructure.

- Investment Plans: Ongoing investments are focused on sterile fill-finish expansion, polymer conversion facilities, and regional manufacturing hubs, particularly in Asia Pacific and North America. Capital deployment is increasingly directed toward low-extractable polymer formats and integrated packaging-plus-validation capabilities to support injectable drug pipelines.

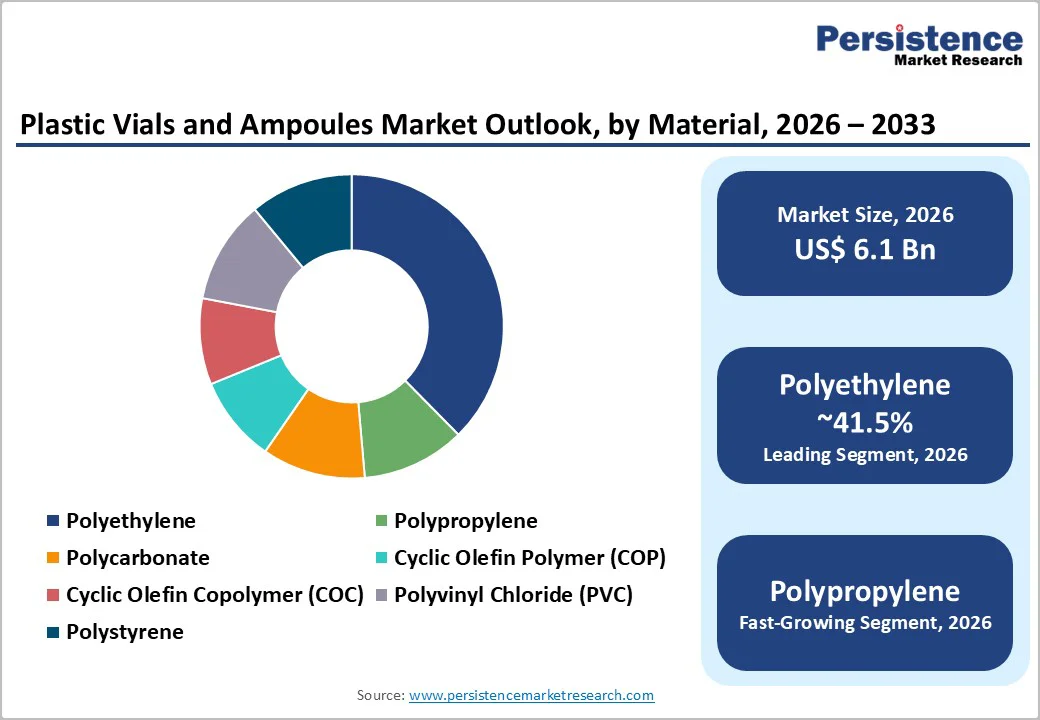

- Dominant Material: Polyethylene is estimated to remain the dominant material, holding approximately 41.5% market share, due to its cost efficiency, high-volume processing suitability, and continued use in non-parenteral and low-risk pharmaceutical applications.

- Leading Product Type: Vials are anticipated to represent the leading product category, accounting for over 59.6% of market demand, driven by widespread use in hospitals, clinics, vaccine storage, and multi-dose injectable formulations.

| Key Insights | Details |

|---|---|

| Plastic Vials and Ampoules Market Size (2026E) | US$6.1 Bn |

| Market Value Forecast (2033F) | US$8.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Growth in Parenteral Drug Production and Biologics Pipeline

Global demand for parenteral packaging continues to rise as injectable therapies and biologics gain a larger share of pharmaceutical development pipelines.

Injectable drug formats are increasingly preferred for high-value biologics, vaccines, oncology treatments, and specialty therapeutics due to their higher bioavailability and targeted delivery. This shift directly increases demand for plastic vials, ampoules, and single-use containers that meet stringent sterility and low-extractable performance requirements.

Growth in self-administered injectable therapies further supports higher per-unit packaging value, as these products require enhanced safety, precision dosing, and user-friendly designs. Regulatory emphasis on container-closure integrity and drug-container compatibility reinforces the adoption of validated polymer solutions for injectable drug storage, transport, and administration.

Polymer Innovation Enabling Glass Replacement

Advancements in polymer science have significantly improved the performance profile of plastic primary packaging. Cyclic olefin copolymer (COC) and cyclic olefin polymer (COP) offer glass-like transparency, low moisture permeability, and minimal extractables, reducing adsorption and interaction risks for sensitive biologic formulations.

These materials address key limitations associated with glass, including delamination, breakage, and particulate contamination. Improved process ability allows manufacturers to develop innovative vial and ampoule designs, including prefilled formats and integrated closure systems.

Faster cycle times, lower container weight, and improved logistics efficiency further enhance the economic attractiveness of advanced polymer packaging, supporting premiumization within the plastic vials and ampoules segment.

Capacity Expansion and Cost Advantages in Asia Pacific

Significant investments in fill-finish facilities, blow-molding, and injection stretch blow molding infrastructure across China, India, and ASEAN countries are strengthening Asia Pacific’s position as a global manufacturing hub for plastic primary packaging. Lower capital expenditure requirements and operating costs, combined with improving regulatory alignment, are enabling efficient large-scale production of polymer vials and ampoules.

Regional capacity expansion shortens lead times and reduces landed costs for global pharmaceutical customers. As a result, plastic packaging formats are gaining market share in regions that have traditionally relied on glass containers, accelerating adoption and enhancing competitiveness for suppliers with localized manufacturing footprints.

Barrier Analysis - Regulatory and Validation Complexity

Plastic vials and ampoules used in parenteral applications are subject to extensive regulatory scrutiny. Manufacturers must provide comprehensive container-closure system documentation, extractables and leachables studies, and container-closure integrity validation. These requirements extend development timelines and increase compliance costs, particularly for small and mid-sized manufacturers transitioning from glass to polymer solutions.

The need for qualified materials, validated suppliers, and regulatory-ready documentation creates high technical barriers to entry. For legacy drug products already approved in glass packaging, the cost and effort required for revalidation can delay or limit conversion to plastic formats.

Performance Perception and Raw Material Volatility

Despite technological progress, certain drug formulations continue to rely on glass due to long-term stability data or regulatory precedent. Glass remains perceived by some stakeholders as the benchmark for parenteral sterility and chemical inertness.

In parallel, price volatility and supply constraints affecting specialty polymer resins can pressure margins and disrupt production planning. Limited availability of high-performance grades such as COP and COC increases procurement risk, making inventory management and dual sourcing strategies essential for suppliers seeking to scale premium polymer offerings.

Opportunity Analysis - Premiumization through Low-Extractable Polymer Formats

Demand for low-extractable, high-purity polymer vials is expanding faster than that for commodity plastics. Premium COC and COP containers enable suppliers to command higher average selling prices while meeting the needs of biologics developers focused on minimizing container-drug interactions.

If premium polymer formats increase their share of total unit volumes to 10-15% by 2030 from less than 5% currently, the resulting sub-market would represent several hundred million dollars in incremental value globally by the early 2030s. This opportunity is particularly attractive for suppliers with validated materials, in-house testing capabilities, and regulatory expertise.

Integrated Fill-Finish and Value-Added Services

Packaging providers offering integrated solutions that combine container supply with sterile fill-finish, validation support, serialization, and on-site quality testing are well-positioned to capture higher margins. These bundled services reduce customer onboarding complexity and accelerate time-to-market for pharmaceutical companies.

Strategic partnerships between polymer suppliers, converters, and contract manufacturing organizations support differentiated offerings tailored to biologics and specialty injectables. Investments in regional fill-finish capacity across Asia, Eastern Europe, and Latin America create additional opportunities to serve local markets efficiently while supporting global supply chains.

Category-wise Analysis

Material Insights

Polyethylene is estimated to account for approximately 41.5% of the global plastic vials and ampoules market, making it the dominant material segment by volume. Its leadership is driven by low raw material cost, widespread processing familiarity, and suitability for non-parenteral and low-risk pharmaceutical applications.

High-density polyethylene (HDPE) and low-density polyethylene (LDPE) are extensively used in bulk pharmaceutical containers, oral liquid packaging, topical formulations, and ancillary healthcare products such as saline, disinfectants, and diagnostic reagents.

The material’s compatibility with high-speed blow-molding and form-fill-seal processes enables efficient large-volume production, supporting favorable unit economics for manufacturers. Polyethylene’s continued dominance reflects sustained demand from high-volume applications where advanced moisture or oxygen barrier performance is not critical, and cost efficiency remains a primary purchasing criterion.

Polypropylene represents the fastest-growing mainstream resin segment in the plastic vials and ampoules market, supported by its superior thermal stability, enhanced barrier properties, and compatibility with sterilization techniques such as autoclaving and gamma irradiation. These attributes make polypropylene increasingly suitable for a broader range of pharmaceutical and healthcare applications, including selected parenteral and diagnostic uses.

Engineered polypropylene blends further improve chemical resistance and dimensional stability while maintaining a cost advantage over premium polymers such as COP and COC. Growth is reinforced by product reformulations aimed at replacing glass in low- to medium-risk injectable formats and by rising investments in polypropylene-specific tooling for aseptic and terminal sterilization workflows within pharmaceutical manufacturing facilities.

Product Type Insights

Vials are estimated to represent the largest product type segment, accounting for 59.6% of market share within plastic vials and ampoules. Their dominance is supported by widespread use across hospitals, clinics, vaccine storage programs, and pharmaceutical manufacturing lines. Larger sterile vials, particularly those with capacities of 8 mL and above, are extensively used for injectable drugs, diluents, biologics, and multi-dose formulations.

Plastic vials are fully compatible with automated filling lines, vacuum stoppering systems, and standardized dosing protocols, ensuring operational efficiency and regulatory compliance. Their suitability for institutional healthcare settings and high-throughput pharmaceutical production reinforces strong and recurring demand, sustaining their leading market position.

Plastic ampoules are the fastest-growing product sub-segment, driven by increasing adoption of single-use dosing formats and the expansion of outpatient and home-based care. One-point cut, flame-cut, and closed plastic ampoules reduce contamination risk while enabling precise, single-dose administration for ophthalmic solutions, respiratory therapies, and emergency injectables.

Compared with glass, plastic ampoules offer lower breakage rates, lighter weight, and improved safety during handling and transportation. These advantages make them particularly suitable for field use, ambulatory care, and self-administration applications. Continuous improvements in seal integrity, opening mechanisms, and material clarity are further accelerating acceptance across clinical and pharmaceutical applications.

Regional Insights

North America Plastic Vials and Ampoules Market Trends - CDMO-Led Injectable Demand and High-Barrier Regulatory Compliance

North America is anticipated to lead the global plastic vials and ampoules market, accounting for approximately 36% of market share, with the U.S. representing the largest contributor. The region benefits from a mature pharmaceutical manufacturing base, a strong biotechnology ecosystem, and high per-capita healthcare expenditure.

Growth is supported by sustained production of injectable drugs, vaccines, and biologics, particularly within contract development and manufacturing organizations (CDMOs). Regulatory rigor, including strict container-closure integrity and extractables testing requirements, raises entry barriers but favors established packaging suppliers with validated polymer solutions and proven compliance capabilities.

Recent investments in sterile fill-finish capacity across the U.S. have reinforced demand for high-quality plastic vials and ampoules. Several leading pharmaceutical packaging manufacturers have expanded domestic production lines to reduce reliance on imports and improve supply chain resilience following pandemic-era disruptions.

Innovation in cyclic olefin polymer and high-purity polypropylene containers has accelerated adoption in biologics and specialty injectables, while partnerships between packaging suppliers and CDMOs support integrated solutions for clinical and commercial manufacturing. These developments strengthen North America’s leadership position and sustain premium pricing for compliant, high-performance polymer containers.

Europe Plastic Vials and Ampoules Market Trends - Sustainability-Aligned, Validated Polymer Packaging for Generics and Biologics

Europe represents a significant share of global demand for plastic vials and ampoules, led by Germany, the U.K., France, and Spain. The region’s market is shaped by a strong generics industry, expanding biologics production, and harmonized regulatory standards that emphasize product safety, traceability, and quality assurance.

European pharmaceutical manufacturers increasingly favor validated plastic primary packaging for selected injectable and diagnostic applications, particularly where breakage risk reduction and lightweight logistics offer operational advantages over glass.

Environmental policy plays a central role in shaping regional market dynamics. Circular economy initiatives and sustainability regulations are influencing material selection, driving innovation in recyclable polymers and downgauged packaging formats. Several European packaging producers have introduced mono-material vial and ampoule solutions designed to improve recyclability without compromising sterility or performance.

Investments in advanced testing laboratories and extractables and leachables capabilities are enabling suppliers to meet evolving regulatory expectations, particularly for biologics and high-value injectables. As a result, Europe continues to favor technologically advanced, compliance-driven packaging solutions over low-cost alternatives.

Asia Pacific Plastic Vials and Ampoules Market Trends - Rapid Capacity Expansion and Localization of Pharmaceutical Packaging

Asia Pacific is the fastest-growing regional market for plastic vials and ampoules, supported by rapid pharmaceutical manufacturing expansion, government-backed localization initiatives, and rising vaccine and injectable drug demand.

China and India dominate regional production, benefiting from large domestic markets, cost-competitive manufacturing, and expanding export capabilities. Japan, in contrast, focuses on high-specification applications, with demand concentrated in precision-engineered polymer containers for advanced pharmaceutical and diagnostic use.

Recent capacity additions across China and India have significantly increased regional output of plastic primary packaging, particularly for polyethylene and polypropylene formats used in oral liquids, diagnostics, and selected injectable applications. Several multinational packaging suppliers have established or expanded production facilities in ASEAN countries to serve regional pharmaceutical hubs and reduce lead times.

Regulatory alignment efforts, including stricter quality standards and harmonization with global pharmaceutical guidelines, are improving acceptance of Asia-manufactured plastic vials and ampoules in international markets. Combined with ongoing investments in sterile infrastructure and polymer processing technology, these developments are accelerating adoption and reinforcing Asia Pacific’s role as a global growth engine for the market.

Competitive Landscape

The plastic vials and ampoules market features a mix of large multinational packaging groups and specialized pharmaceutical container manufacturers. While several global players hold meaningful shares, the overall structure remains moderately fragmented.

Competition centers on material expertise, regulatory readiness, and the ability to provide integrated sterile solutions. Regional specialists and niche suppliers continue to find opportunities in customized formats and local markets.

Recent developments include the qualification and commercialization of advanced COP and COC vial formats, the expansion of manufacturing capacity in Asia Pacific, and increased strategic partnerships between packaging suppliers, contract manufacturers, and testing service providers. These initiatives aim to reduce qualification timelines, improve supply reliability, and support premium biologics packaging requirements.

Key strategies include innovation in low-extractable polymers, vertical integration of packaging and fill-finish services, and geographic expansion into high-growth regions. Cost leadership remains important in commodity segments, while differentiation drives pricing power in premium polymer applications.

Key Industry Developments

- In April 2025, AptarGroup introduced a new passive-fill ampoule packaging platform with enhanced break resistance and serialized tracking features to improve safety and traceability in injectable applications.

- In May 2025, Gerresheimer completed the acquisition of Bormioli Pharma’s primary packaging business, expanding its plastics and vial production portfolio in Europe and strengthening its position in both polymer and glass packaging formats.

Companies Covered in Plastic Vials and Ampoules Market

- Gerresheimer AG

- West Pharmaceutical Services, Inc.

- Stevanato Group

- SCHOTT AG

- Amcor Plc

- Berry Global, Inc.

- Nipro Corporation

- SGD Pharma

- Origin Pharma Packaging

- DWK Life Sciences

- Alpha Packaging

- Corning Incorporated

- Plastipak Packaging

- AptarGroup, Inc.

- Amscan International

- Romaco Group

- Adelphi Healthcare Packaging

- Comar, LLC

- Tekni-Plex, Inc.

- Shenzhen Zhenghao Plastic & Mold Co., Ltd.

Frequently Asked Questions

The market is estimated to be valued at US$6.1 billion in 2026.

By 2033, the market is projected to reach US$8.2 billion.

Key trends include growing adoption of single-dose and prefilled parenteral packaging, increasing use of low-extractable polymer materials for sensitive drug formulations, and continued capacity expansion in Asia Pacific.

By product type, vials represent the leading segment, accounting for over 59.6% of total market demand, driven by widespread use in hospitals, clinics, and vaccine storage. By material, polyethylene remains dominant with approximately 41.5% market share.

The market is expected to grow at a CAGR of 4.3% between 2026 and 2033.

Major players with strong product portfolios and global presence include Gerresheimer AG, West Pharmaceutical Services, Stevanato Group, Berry Global, and Amcor Plc.