- Smart Packaging

- Plastic Bag Market

Plastic Bag Market Size, Share, and Growth Forecast, 2026 - 2033

Plastic Bag Market by Material (Polyethylene, PET, Others), Bag Type (T-Shirt Bags, Gusseted Bags, Others), End-user, and Regional Analysis for 2026 - 2033

Plastic Bag Market Size and Trends Analysis

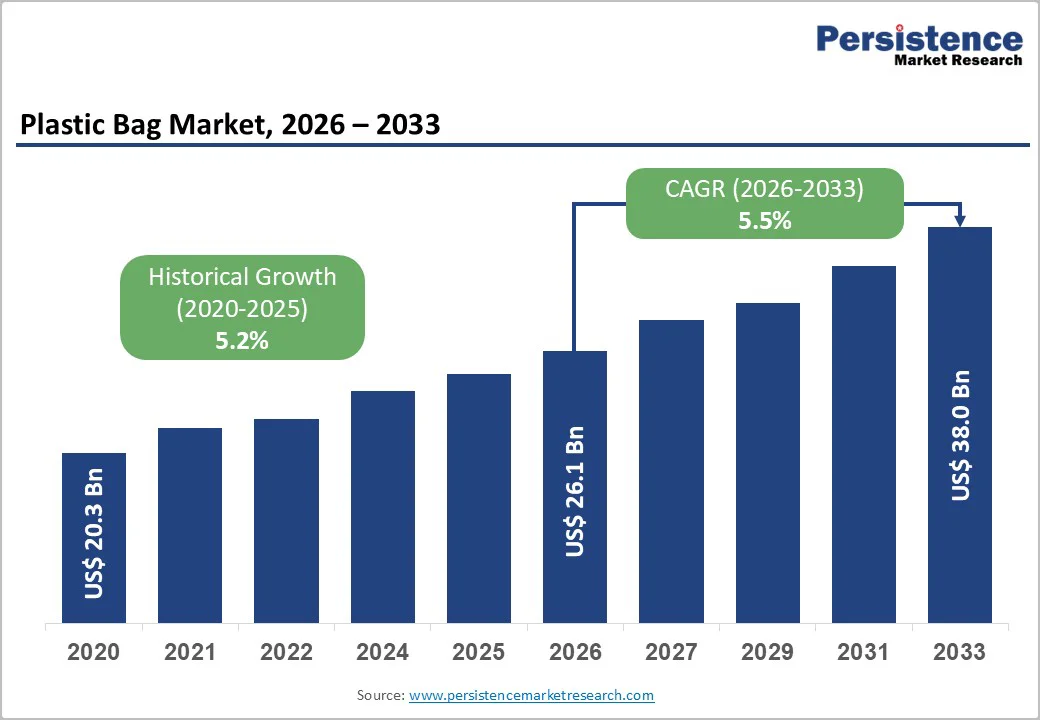

The global plastic bag market size is likely to be valued at US$26.1 billion in 2026 and is expected to reach US$38.0 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033, driven by steady demand from retail and industrial packaging, rising e-commerce activity, and ongoing product innovation focused on downgauging and recycled-content films.

The cost competitiveness of polyethylene, along with large-scale manufacturing advantages in Asia Pacific, and increasing investments in recycling and circular economy processes, continue to support growth.

Key Industry Highlights

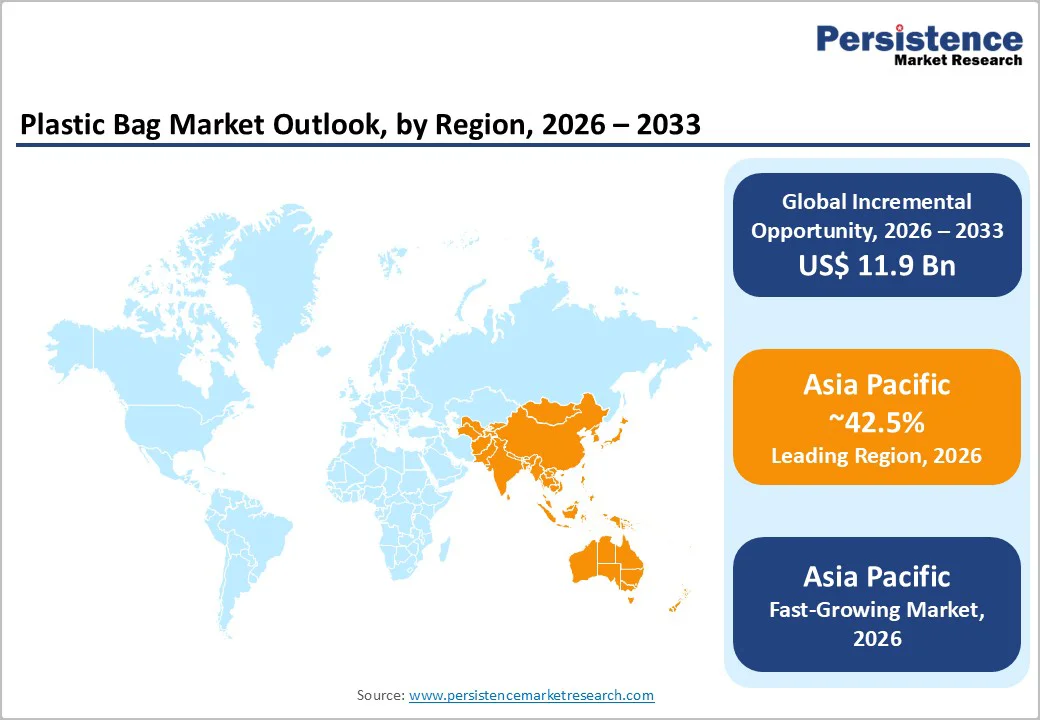

- Leading Region: Asia Pacific is projected to lead the market, accounting for over 42.5% of total revenue, supported by large-scale manufacturing capacity, cost-efficient production, and strong demand from retail, industrial, and e-commerce sectors.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, driven by expanding domestic consumption in China, India, and ASEAN economies, along with continued investment in recycling infrastructure and compliant production technologies.

- Investment Plans: Industry investment is focused on recycling capacity expansion, recycled-content integration, and downgauging technologies, particularly in Asia Pacific, Europe, and North America, as manufacturers align production with regulatory requirements and cost optimization goals.

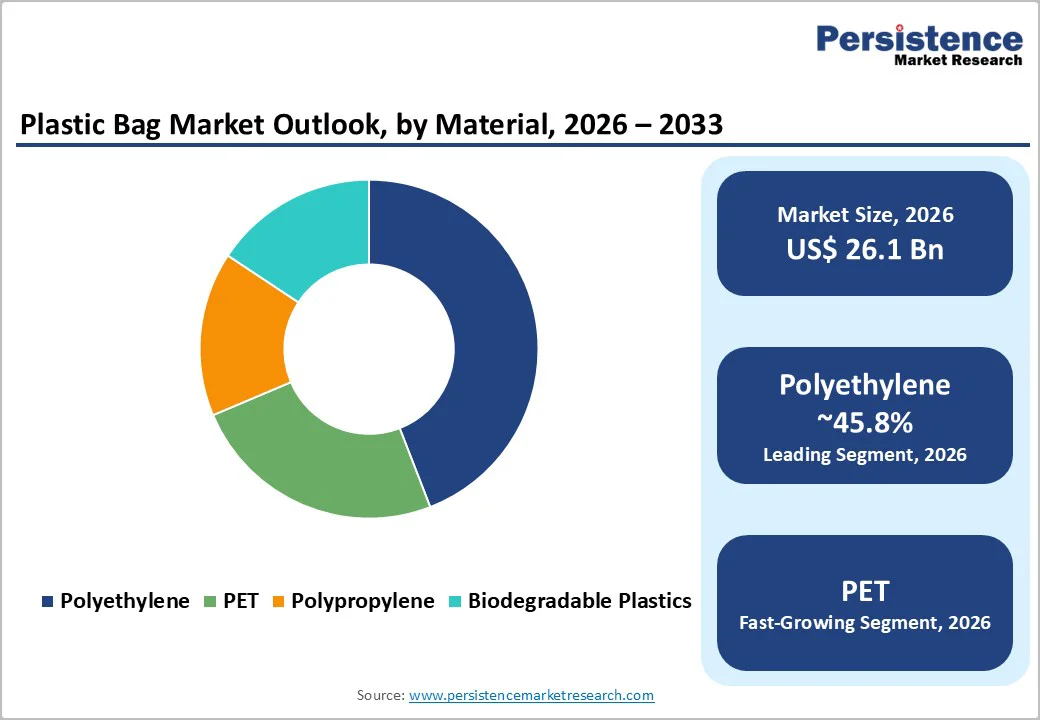

- Dominant Material: Polyethylene is anticipated to dominate, holding approximately 45.8% market share, due to its cost efficiency, processing flexibility, and suitability across retail, household, and industrial applications.

- Leading Bag Type: T-shirt bags are estimated to represent the leading bag type, accounting for about 30.4% of market demand, supported by widespread use in grocery and convenience retail and high-volume production economics.

| Key Insights | Details |

|---|---|

| Plastic Bag Market Size (2026E) | US$26.1 Bn |

| Market Value Forecast (2033F) | US$38.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Durable Demand from Retail and E-Commerce

Retail and e-commerce account for the largest share of plastic bag consumption due to their low unit cost, logistics efficiency, and ability to protect goods across complex supply chains. The continued expansion of last-mile delivery networks, growth in packaged food consumption, and proliferation of online retail platforms sustain baseline demand for flexible containment and transport solutions.

Plastic bags remain cost-effective compared to many alternative materials, particularly in applications requiring moisture resistance and puncture durability. This persistent demand base limits downside risk to overall market value and supports continued investment in downgauging and recycled-content technologies to balance cost efficiency with regulatory compliance.

Polyethylene Dominance and Material Economics

Polyethylene remains the dominant material in plastic bag manufacturing; its leadership is supported by low production costs, versatile mechanical properties, and a globally established resin supply chain. Polyethylene grades such as LDPE, HDPE, and LLDPE enable manufacturers to address a wide range of applications, from lightweight retail carry bags to heavy-duty industrial sacks.

While resin price movements directly influence margins, relatively stable feedstock availability and modest global capacity additions provide predictable supply conditions. Manufacturers increasingly focus on downgauging, optimized resin blends, and recycled-content integration to reduce cost exposure while meeting sustainability and procurement requirements.

Sustainability Regulation and Circular-Economy Incentives

Government policies and retailer procurement standards increasingly promote recycled content mandates, extended producer responsibility programs, and restrictions on certain single-use products. These measures create a dual market effect; they stimulate demand for recycled and alternative materials while raising compliance costs for conventional products.

In regions with mature collection and recycling infrastructure, manufacturers can transform regulatory obligations into higher-value offerings through certified recycled-content bags. In markets where infrastructure remains underdeveloped, compliance costs and substitution risks can constrain margins. Overall, companies that align product portfolios with circular-economy objectives gain access to preferred procurement channels and reduce long-term regulatory exposure.

Barrier Analysis - Regulatory Fragmentation and Single-Use Bans

Regulatory approaches to plastic bag usage vary widely across countries and regions. While some jurisdictions impose strict bans or levies on thin single-use bags, others allow continued usage subject to recycling or thickness requirements.

This fragmentation increases compliance complexity for manufacturers operating across multiple markets and can lead to abrupt demand declines in specific urban or national markets. In several cases, localized bans or levies have resulted in double-digit volume reductions within 12 to 24 months. Manufacturers with concentrated exposure to restricted regions face revenue volatility and must invest in product redesign or portfolio diversification to remain compliant.

Raw-Material Price Volatility and Feedstock Constraints

Plastic bag manufacturers remain exposed to fluctuations in petrochemical feedstock prices. Sudden increases in resin prices compress margins and often require cost pass-through to customers, which can dampen demand in price-sensitive segments.

Supply chain disruptions, including plant outages or logistics bottlenecks, may also create short-term shortages and increase working capital requirements. Historically, resin price fluctuations of 10-20% have translated into comparable margin pressure across flexible packaging producers and have delayed capacity expansion decisions. Effective mitigation requires diversified sourcing strategies and procurement risk management.

Opportunity Analysis - High-Value Recycled-Content and Certified Products

A significant growth opportunity exists in certified recycled-content plastic bags that comply with regulatory thresholds and retailer sourcing standards. Conservative assessments suggest that recycled-content product lines could account for 10-15% of incremental market value by the late 2020s in regions with strong policy enforcement.

These products command price premiums and offer more stable demand through long-term procurement contracts. Actionable strategies include vertical integration into recycling operations, long-term supply agreements with recyclers, and third-party certification to ensure traceability and compliance.

Emerging Markets and Downgauging Technologies

Emerging economies across Asia and parts of Africa present strong growth potential due to rising per-capita packaging consumption. Adoption of downgauging technologies allows manufacturers to produce thinner films with equivalent performance, delivering both cost and sustainability benefits.

Accelerated adoption of downgauged films could reduce resin usage per unit by 10-30%, improving margins while maintaining competitive pricing. Strategic investment in modern film extrusion equipment and localized manufacturing capacity enables suppliers to capture growing demand in price-sensitive, high-volume markets.

Category-wise Analysis

Material Insights

Polyethylene is projected to lead, accounting for approximately 45.8% of the revenue share in 2025, maintaining its leadership due to superior cost efficiency, scalability, and processing versatility. Its major variants, LDPE, HDPE, and LLDPE, support a wide range of applications, including lightweight grocery and retail carry bags, poly mailers used in e-commerce, and heavy-duty industrial and agricultural sacks.

The material’s compatibility with high-speed extrusion, printing, and sealing technologies enables manufacturers to achieve consistent quality at high volumes. In addition, polyethylene’s adaptability to downgauging and recycled-content integration strengthens its cost-to-performance advantage, making it the preferred choice for mass-market retail and logistics-driven packaging formats.

PET and advanced material blends are likely to be the fastest-growing material segment, driven by increasing demand for enhanced barrier properties, mechanical strength, and visual clarity. Growth is particularly evident in food packaging liners, specialty retail bags, and applications requiring improved moisture and oxygen resistance.

The expanding availability of recycled PET (rPET) has further strengthened adoption, especially in regions with recycled-content mandates and strong collection infrastructure. Manufacturers investing in rPET sourcing, multilayer film structures, and barrier lamination technologies are increasingly deploying PET-based solutions in premium and regulation-sensitive applications, positioning this segment for sustained above-average growth.

Bag Type Insights

T-shirt bags are expected to lead, accounting for approximately 30.4% of the total market demand, making them the most widely used bag type globally. Their dominance is driven by extensive adoption in grocery stores, convenience outlets, and traditional retail formats, where low unit cost, ease of handling, and high-volume availability are critical.

T-shirt bags are commonly used for point-of-sale carry applications and short-distance transport of consumer goods. The format also supports branding through surface printing, allowing retailers to use bags as low-cost promotional tools. Established production infrastructure and streamlined distribution further reinforce the segment’s leading position.

Gusseted bags are anticipated to be the fastest-growing bag type, supported by rising demand from industrial, agricultural, and e-commerce applications.

Their expandable side or bottom panels increase load capacity and improve stacking and palletization efficiency, making them suitable for bulk packaging, construction materials, and large-format retail goods. In e-commerce logistics, gusseted designs are increasingly used for shipping apparel, household products, and bulk consumer items.

The ongoing shift from rigid to flexible packaging in industrial supply chains, driven by weight reduction and transportation efficiency, continues to accelerate the adoption of gusseted bag formats across multiple end-use sectors.

Regional Insights

North America Plastic Bag Market Trends - Value-Added, Regulation-Ready Retail and E-commerce Packaging

North America represents a substantial share of the market share, supported by higher average selling prices and a premium product mix that includes printed retail bags, specialty food packaging, and high-performance household bags.

Growth in the region is largely replacement-driven, with steady demand from grocery chains, big-box retailers, and e-commerce platforms requiring poly mailers and protective packaging. The rapid expansion of online retail has increased demand for durable, lightweight shipping bags, particularly for apparel and consumer goods fulfillment.

Regulatory diversity across U.S. states and municipalities has shaped product strategies, with manufacturers offering thicker reusable bags, recycled-content carry bags, and compliant alternatives for restricted jurisdictions. Retail brands have increasingly specified recycled-content requirements in procurement, accelerating the adoption of post-consumer resin blends.

In response, several large packaging producers have expanded partnerships with domestic recyclers and invested in upgraded printing and film extrusion capabilities. These investments have strengthened regional supply resilience while enabling faster customization for private-label retail programs, reinforcing North America’s focus on value-added and regulation-ready plastic bag solutions.

Europe Plastic Bag Market Trends - Sustainability-Driven, Reusable and Recycled-Content Bag Adoption

Europe maintains a strong and structurally resilient market position, underpinned by well-established retail infrastructure and stringent sustainability regulations. The region’s harmonized policy environment encourages the use of recyclable, reusable, and recycled-content plastic bags, increasing demand for higher-quality materials and certified products.

Supermarket groups and consumer brands across countries such as Germany, the U.K., France, and Spain have actively reduced thin single-use bags, replacing them with heavier-gauge reusable formats and recycled-content alternatives.

Manufacturers operating in Europe have responded by investing heavily in mono-material designs, advanced recycling compatibility, and traceability systems that support regulatory compliance. Several European packaging groups have expanded mechanical recycling capacity or entered long-term supply agreements to secure recycled resin feedstock.

These moves have reduced dependence on virgin polymers and improved compliance with regional sustainability targets. Supply chain optimization within Europe has also gained importance, with producers consolidating manufacturing footprints to reduce cross-border complexity and logistics costs. As a result, Europe continues to favor technologically advanced, regulation-aligned plastic bag solutions over commoditized products.

Asia Pacific Plastic Bag Market Trends - High-Growth Manufacturing Hub Driven by Scale, E-commerce, and Regulatory Transition

Asia Pacific is projected to lead the market, accounting for over 42.5% of revenue, and remains the fastest-growing regional market. Growth is driven by large-scale manufacturing capacity, cost advantages, and expanding domestic consumption, particularly in China, India, and Southeast Asia.

China continues to dominate regional production, supplying both domestic demand and export markets through extensive film extrusion and converting infrastructure. India and ASEAN countries are experiencing rapid growth due to retail modernization, urbanization, and rising e-commerce penetration.

Regulatory approaches vary significantly across the region. China has progressively tightened restrictions on certain single-use plastics while simultaneously expanding recycling infrastructure, prompting manufacturers to upgrade materials and invest in recycled-content products.

In India, nationwide restrictions on thin plastic bags have accelerated demand for compliant, thicker, and alternative-material bags, creating transition opportunities for organized manufacturers. Across Southeast Asia, export-oriented converters have expanded the capacity to serve global retail and industrial customers.

Investments in the region increasingly target recycling, downgauging technology, and capacity expansion, with both regional players and multinational companies establishing joint ventures and localized production hubs. These developments strengthen Asia Pacific’s role as a long-term growth engine and a critical manufacturing base for the market.

Competitive Landscape

The global plastic bag market exhibits moderate concentration at the global level, with large multinational players competing alongside numerous regional and local manufacturers. Scale, access to recycled feedstock, and technical capabilities such as advanced printing and lamination define competitive positioning.

Recent years have seen major consolidation among leading packaging producers, aimed at expanding scale, enhancing innovation capabilities, and securing recycling access. Additional strategic activity includes investments in recycled-content product lines, recycling partnerships, and geographic expansion to serve high-growth markets.

Leading players prioritize scale consolidation, vertical integration, product differentiation, and cost leadership. Certified recycled content, supply reliability, and rapid customization for retail clients serve as key competitive differentiators.

Key Industry Developments

- In August 2025, Novolex Holdings announced the launch of new recyclable and reusable tote bags under its Hilex brand for supermarkets, restaurants, and retail packaging, reinforcing its sustainability portfolio and expanding product offerings in compliant retail segments.

- In March 2025, Berry Global expanded its biodegradable resin integration program, increasing the use of biodegradable materials in flexible bags by more than 40%, enhancing product durability while reducing the carbon footprint of its packaging portfolio.

Companies Covered in Plastic Bag Market

- Berry Global Group, Inc.

- Novolex Holdings, LLC

- Sealed Air Corporation

- Mondi Grou

- Amcor plc

- Coveris Holdings S.A.

- Smurfit Kappa Group

- Inteplast Group

- Reynolds Consumer Products

- Huhtamaki Oyj

- Sigma Plastics Group

- Glenroy, Inc.

- Flexopack S.A.

- Clondalkin Group

- Thantawan Industry Public Company Limited

- Sahachit Watana Plastic Industry Co., Ltd.

- PolyPak Packaging

- Superbag Corporation

- International Plastics Inc.

- Aluflexpack Group

Frequently Asked Questions

The global plastic bag market is projected to be valued at US$26.1 billion in 2026.

By 2033, the plastic bag market is forecast to reach a value of US$38.0 billion.

Key trends include increased use of recycled-content materials, downgauging to reduce material consumption, growing demand for e-commerce and logistics packaging, and a shift toward regulation-compliant and reusable bag formats across major regions.

Polyethylene is the leading material segment, accounting for approximately 45.8% market share, while T-shirt bags dominate by bag type with around 30.4% share, driven by high-volume retail usage.

The plastic bag market is expected to grow at a CAGR of 5.5% between 2026 and 2033.

Major players include Berry Global Group, Inc., Novolex Holdings, LLC, Sealed Air Corporation, Coveris Holdings S.A., and Mondi Group.