- Inks, Coatings, Adhesives & Sealants (ICAS)

- Pipe Coating Market

Pipe Coating Market Size, Share, and Growth Forecast, 2026 - 2033

Pipe Coating Market By Product Type (Fusion-Bonded Epoxy (FBE) Coatings, Others), Formulation (Solvent-Based Coatings, Others), Functionality (Corrosion Protection, Others), End-use (Oil and Gas, Water and Wastewater, Others), and Regional Analysis for 2026 - 2033

Pipe Coating Market Size and Trends Analysis

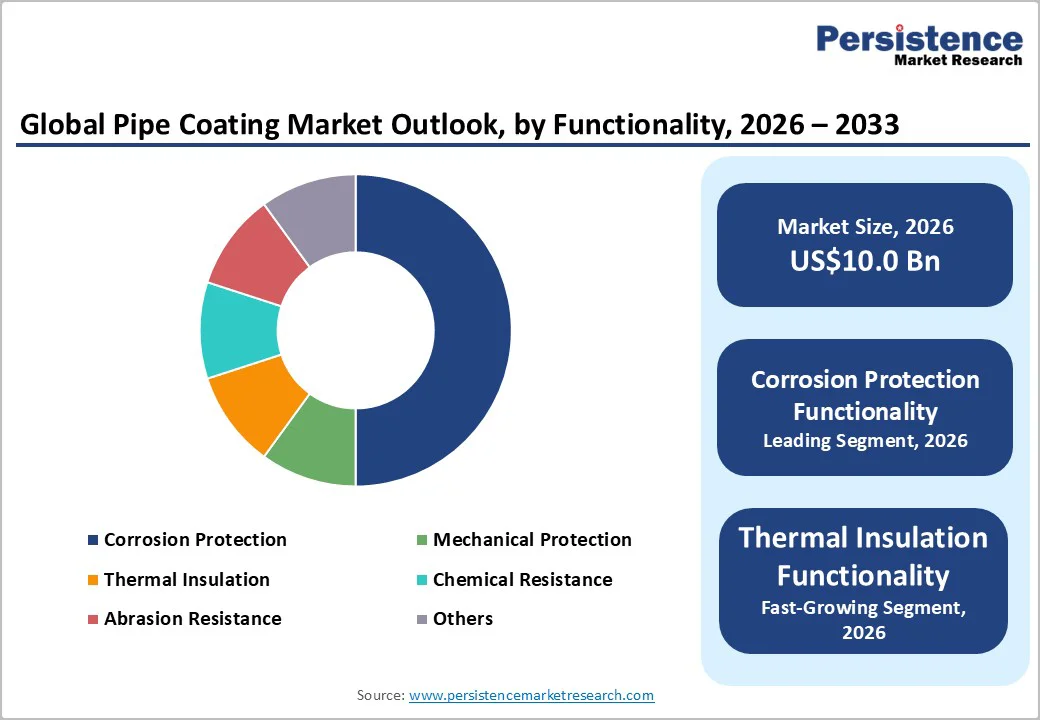

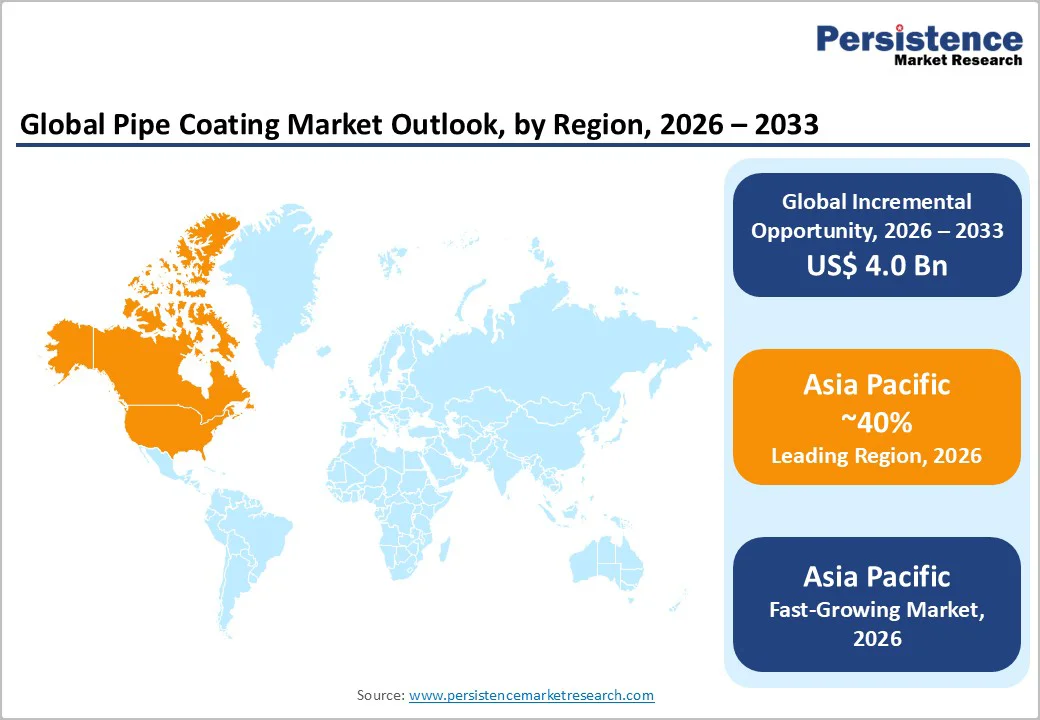

The global pipe coating market size is likely to be valued at US$10.0 billion in 2026, expected to reach US$14.0 billion by 2033, growing at a CAGR of 4.9% during the forecast period from 2026 to 2033, driven by surging infrastructure investments in oil and gas pipelines, rising demand for corrosion-resistant solutions in water management, and advancements in eco-friendly formulations such as water-based coatings. The pipe coating market is driven by innovations in FBE and PE coatings for durability and corrosion protection, while embracing green standards to cut maintenance costs up to 30% and enable energy-efficient transport.

Key Industry Highlights:

- Leading Region: Asia Pacific is expected to capture a 40% market share in 2026, fueled by extensive pipeline developments in China and India alongside rapid urbanization.

- Fastest-growing Region: Asia Pacific, fueled by oil and gas booms and water infrastructure projects in Southeast Asia.

- Dominant Product Type: Fusion-Bonded Epoxy (FBE) coatings, expected to capture about 35% of the market share, due to superior adhesion in high-pressure applications.

- Leading Formulation: Solvent-based coatings, anticipated to account for over 45% of revenue, are valued for chemical resistance in industrial settings.

- Leading Functionality: Corrosion protection, estimated to contribute nearly 50% of the market, is essential for extending pipeline lifespans.

- Leading End-user: Oil & gas, likely to account for approximately 45% market share in 2026, amid global energy demands and offshore developments.

| Key Insights | Details |

|---|---|

|

Pipe Coating Market Size (2026E) |

US$10.0 Bn |

|

Market Value Forecast (2033F) |

US$14.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for Corrosion-Resistant Pipelines in Oil & Gas and Water Infrastructure

Corrosion-resistant pipelines are witnessing growing demand globally, driven by the pressing need for durable, low-maintenance infrastructure in both oil & gas and water/wastewater sectors. In the oil & gas industry, pipelines transport crude oil, natural gas, saltwater, and other corrosive media under high pressure and often harsh environments, making corrosion resistance indispensable to prevent leaks, failures, and costly downtime.

In water and sanitation infrastructure, especially in developing countries, corrosion-resistant steel and stainless steel pipelines are increasingly adopted for their longevity and reliability. For instance, in India, the consumption of stainless steel, widely used in corrosion-resistant pipes, reached 4.8?million tonnes in FY25, marking an 8% year-on-year growth. Rising urbanization, replacement of ageing infrastructure, and government water-supply programs are key factors driving this demand. The integration of advanced coatings and materials in pipelines helps reduce long-term maintenance costs, improve safety, and enhance the overall resilience of both oil & gas and municipal water networks.

High Raw Material Volatility and Environmental Compliance Costs

High raw material volatility and rising environmental compliance costs are increasingly weighing on the steel and pipeline?materials sector and, by extension, on infrastructure projects using steel pipelines. In India, the primary raw materials for steel, iron ore, and coking coal often face global supply disruptions, shifting export-import dynamics, and price swings. The Ministry of Steel (MoS) reports that while iron ore demand is satisfied largely through domestic supply, coking coal requirements are “mainly met through imports.” Dependence on imported coal exposes steel producers to international price fluctuations, freight?tariff variations, and currency risks, which can rapidly escalate production costs. As noted in industry analyses, raw materials can account for roughly 70% of production cost in steelmaking, making volatility in input costs a major margin risk.

Environmental compliance adds another layer of cost. Under India’s regulatory framework, as enforced by the Central Pollution Control Board (CPCB) in coordination with the Ministry of Steel, steel plants must adhere to strict norms for air and water emissions, waste handling, noise, and pollution control. To meet these standards, investments in pollution control equipment, cleaner technologies, emission monitoring systems, wastewater treatment, and regulatory reporting become mandatory. As per the government’s 2025 roadmap on sustainable steel production (the Greening the Steel Sector in India: Roadmap and Action Plan), shifting to “green steel” and low-carbon production methods entails additional costs and capital expenditure for plants across the country.

Advancements in Eco-Friendly and Multi-Functional Coatings

The rise of eco-friendly and multi-functional coatings presents a significant growth opportunity in the pipeline and infrastructure sectors. Increasing regulatory emphasis on sustainability, particularly in reducing VOC emissions and carbon footprints, is driving demand for water-borne, high-solids, and bio-based coatings. For instance, water-borne coatings can reduce VOC emissions by up to 90% compared to traditional solvent-based systems. This regulatory push creates a strong incentive for pipeline operators and manufacturers to adopt greener materials, creating a large addressable market.

The development of multi-functional coatings combining corrosion protection, chemical resistance, mechanical robustness, thermal stability, and even self-healing properties enables infrastructure that lasts longer and requires less maintenance. Nanotechnology-enhanced coatings, embedding nanoparticles or nanocomposites, further improve adhesion, hardness, and durability.

Category-wise Analysis

Product Type Insights

Fusion-bonded epoxy (FBE) coatings are anticipated to dominate the market, accounting for approximately 35% of the market share in 2026. Their dominance stems from exceptional adhesion and thermal stability, making them ideal for oil and gas pipelines under high temperatures. FBE coatings provide uniform protection, resist cathodic disbondment, and support field jointing, suiting large-scale deployments. For example, Trans Enterprises provides internal and external FBE coating services for pipelines used in the oil, gas, and water industries. Their FBE coatings are designed to deliver maximum adhesion and corrosion protection even under aggressive operating conditions, highlighting the practical application and reliability of this technology in real-world infrastructure projects.

Polyethylene (PE) coatings represent the fastest-growing segment, due to their flexibility and cost-effectiveness in water and wastewater applications. Their low permeability excels in humid environments, with innovations in three-layer systems enhancing mechanical protection. Rapid adoption in Asia Pacific, where pipeline miles double by 2030, drives this growth. For instance, Ratnamani Metals & Tubes Ltd. in India offers “3LPE” (three-layer polyethylene) coated pipes, combining a base anti-corrosion layer, an adhesive intermediary, and an outer polyethylene layer that are widely used for water, wastewater, oil, and gas pipelines.

Formulation Insights

Solvent-based coatings lead the market, holding approximately 45% of the share in 2026, propelled by superior penetration in complex geometries and durability in chemical processing. Their quick cure times suit high-volume production, and they are widely used, especially in oil & gas, to ensure seamless flow assurance. For example, Tnemec Company, Inc. supplies solvent and high solids coating systems (such as their Series?425 Epoxoline ARO and Series?431 Perma Shield PL) for pipelines and industrial piping formulations that offer high abrasion and chemical resistance, even in aggressive or buried environments. Their coatings are used in heavy-duty pipeline and wastewater applications, demonstrating how solvent-based systems remain central where durability and reliable chemical protection are key.

Water-based coatings emerge as the fastest-growing, driven by regulatory pushes for low VOC alternatives in Europe and North America. Their eco profile helps reduce emissions (by as much as 40%), making them attractive for water infrastructure projects where sustainability is prioritized. Advances such as latex emulsions and water-based epoxies are improving adhesion, corrosion resistance, and application safety, per various standard tests. For example, Tnemec Company, Inc. offers water-based epoxy coatings (e.g., their “Series?1220 HydroLine” and “Series 90 75 Tneme Zinc”) that are low odor, low VOC, and engineered for durability even under immersion or high humidity conditions. These waterborne coatings are suitable for pipelines, reservoirs, tanks, and concrete or steel surfaces, aligning well with sustainability goals in modern water and wastewater infrastructure projects.

Functionality Insights

Corrosion protection is estimated to dominate with a 50% share in 2026, driven by the growing need to extend pipeline life and prevent asset losses in oil, gas, and water infrastructure. Rising exposure to harsh soils, moisture, chemicals, and high-pressure conditions makes protective coatings essential for reducing maintenance costs and preventing leaks. For example, AkzoNobel offers its Intergard and Interthane corrosion-protection coating systems, widely used on steel pipelines and industrial structures. These coatings deliver long-term resistance against rust, abrasion, and chemical attack, showcasing how industry leaders rely on advanced corrosion-resistant solutions to enhance pipeline reliability and performance.

Thermal insulation is the fastest-growing, driven by the rising demand for temperature-stable pipelines in oil, gas, and district-heating networks. As industries transport fluids at extreme temperatures, insulation reduces heat loss, prevents energy waste, and safeguards system efficiency. Growth accelerates further in LNG, chemical processing, and cold-climate water infrastructure. For example, Shawcor provides advanced thermal insulation coatings such as its Thermotite® range, designed for deep-water and high-temperature pipelines. These systems maintain thermal stability, prevent condensation, and improve operational reliability, reflecting why insulated pipeline coatings are rapidly gaining adoption worldwide.

End-user Insights

The oil and gas segment is anticipated to lead with 45% share in 2026, driven by extensive pipeline expansions, rising energy demand, and the need for reliable long-distance transport of crude oil, natural gas, and refined products. The sector depends heavily on high-performance coatings to withstand corrosion, high pressure, and extreme temperatures. For example, Jindal SAW Ltd. supplies large-diameter steel pipes with 3LPE and FBE coatings specifically engineered for oil and gas transmission, ensuring long-term corrosion protection and field durability.

Water and wastewater are the fastest-growing, driven by accelerating urbanization, rising utility investments, and the urgent need to upgrade aging pipeline networks. Governments are prioritizing leak-proof, corrosion-resistant, and long-lasting pipeline systems to improve water quality and reduce transmission losses. Advanced coatings such as PE, epoxy, and polyurethane are increasingly used to enhance durability in corrosive and high-moisture environments. For example, Electrosteel Castings Ltd. supplies ductile iron water-pipeline systems with internal epoxy coatings designed to resist corrosion, chemical exposure, and microbial attack, making them suitable for municipal water supply and sewerage projects across India and international markets.

Regional Insights

North America Pipe Coating Market Trends

Growth in North America is driven by expanding oil and gas pipeline projects, rising shale production, and the modernization of the aging infrastructure. The region increasingly relies on advanced coating technologies such as fusion-bonded epoxy (FBE), polyethylene, polypropylene, and polyurethane to boost corrosion resistance, improve flow efficiency, and extend pipeline lifespan in challenging environments. Strict regulatory standards from agencies such as the EPA and PHMSA encourage the use of high-performance, low-VOC, and environmentally responsible coatings.

Significant investments in water and wastewater pipeline rehabilitation, supported by the U.S. Infrastructure Investment and Jobs Act, further accelerate demand for durable internal and external coating systems. Technological innovations such as multi-layer thermoplastic coatings and abrasion-resistant overlays also support market expansion. For example, PPG Industries, a major coatings manufacturer in the region, supplies high-performance pipeline coatings for oil, gas, municipal water, and industrial pipelines across North America.

Europe Pipe Coating Market Trends

In Europe, growth is driven by strict environmental regulations, rapid infrastructure modernization, and the region’s transition toward cleaner energy systems. Countries across the EU are increasingly enforcing low-VOC requirements, which is accelerating the shift from solvent-based formulations to water-based, powder, and high-solids coatings. This transition is especially prominent in water supply, wastewater management, and district heating networks, where governments are prioritizing eco-friendly materials and long-term corrosion resistance.

The region is also investing heavily in hydrogen-ready and renewable-energy pipeline networks, which require advanced coatings capable of resisting permeation, stress, and fluctuating temperatures. As many European cities upgrade aging pipeline networks, demand for abrasion-resistant, multi-layer polymer coatings is rising, particularly for underground gas transmission and high-pressure water pipelines. Growth is further supported by EU-backed infrastructure funds and national efforts to strengthen energy security. For example, AkzoNobel N.V. supplies protective epoxy, polyurethane, and water-borne pipeline coatings widely used in European water infrastructure refurbishment projects. Its products support compliance with EU sustainability targets while delivering strong corrosion protection and long-term durability in diverse soil and climate conditions.

Asia Pacific Pipe Coating Market Trends

Asia Pacific is likely to be the leading and fastest-growing region, accounting for approximately 40% in 2026, due to rapid industrialization, expanding energy demand, and major government-led investments in water and wastewater infrastructure. Countries such as India, China, Indonesia, and Vietnam are constructing extensive new oil & gas transmission corridors, urban water networks, and industrial piping systems, all of which require high-performance coatings to prevent corrosion and extend asset life.

The region shows a growing preference for cost-efficient and durable coating solutions such as fusion-bonded epoxy (FBE), polyurethane, and multi-layer polyethylene systems, which perform well across diverse soil types, coastal environments, and high-humidity conditions. Rising environmental regulations are encouraging the adoption of low-VOC and long-life coating technologies. Infrastructure expansion in petrochemicals, desalination, and power plants further accelerates the coating demand. For Example, Welspun Corp Limited, a major pipe manufacturer in India, applies advanced FBE and three-layer polyethylene coatings for large cross-country oil and gas pipeline projects, ensuring long-term corrosion protection under harsh monsoon, saline soil, and high-temperature conditions.

Competitive Landscape

The global pipe coating market is highly competitive, shaped by a diverse ecosystem of coating formulators, pipe manufacturers, contract coaters, and engineering firms that support large infrastructure projects. Competition is driven primarily by technological capability, cost efficiency, regulatory compliance, and the ability to deliver high-performance coatings for demanding environments such as offshore pipelines, cross-country transmission lines, and urban water networks.

Companies distinguish themselves through advancements in coating chemistry, such as high-adhesion epoxies, multi-layer polyolefin systems, abrasion-resistant overlays, and eco-friendly low-VOC formulations. As governments worldwide tighten environmental and safety regulations, firms that can supply durable coatings with long service life gain a competitive advantage. Service capability is also a major differentiator: players offering integrated solutions, including surface preparation, automated coating lines, field joint coating, inspection, and long-term maintenance, often secure larger project contracts.

Key Industry Developments

- In March 2024, Hardide Coatings introduced the first product in a new range of ready-coated and enhanced components. The launch involves a JP-5000 4-copper nozzle used in High-Velocity Oxy Fuel (HVOF) thermal spray coating.

- In May 2023, Shawcor Ltd. (TSX: SCL) (Shawcor or the Company) announced today that its pipe coating division, Pipeline Performance Group (PPG), has received five formal contract awards and one letter of intent (LOI) for development projects in South America, Mexico, and the Ivory Coast.

Companies Covered in Pipe Coating Market

- AkzoNobel

- BASF

- The Sherwin-Williams Company

- Axalta Coating Systems

- 3M Company

- Shawcor Ltd.

- Arkema Group

- LyondellBasell Industries

- Valspar Corporation

- PPG Industries, Inc.

- Wasco Energy Group of Companies

- Solvay

- Denso Group

- The Bayou Companies LLC

- Jotun A/S

Frequently Asked Questions

The global pipe coating market is projected to reach US$10.0 billion in 2026.

Key drivers include infrastructure investments and corrosion prevention needs in the energy sectors. Replacement for aging systems in emerging markets sustains demand, offsetting material costs.

The pipe coating market is projected to grow at a CAGR of 4.9% between 2026 and 2033.

Opportunities encompass eco-friendly water-based innovations and recycling for legacy pipelines. Thermal insulation in renewables offers growth in regulated regions such as Europe.

Prominent players include AkzoNobel, BASF, Sherwin-Williams, and Shawcor Ltd. They command a 50% share through production scale and strategic shifts to compliant variants.