- Specialty & Fine Chemicals

- Asbestos Cement Pipe Market

Asbestos Cement Pipe Market Size, Share, and Growth Forecast, 2026 - 2033

Asbestos Cement Pipe Market By Product Type (Pressure Pipes, Non-Pressure Pipes), Application (Water Supply, Sewerage Systems, Drainage), End-user (Municipal, Industrial, Agriculture), and Regional Analysis for 2026 – 2033

Asbestos Cement Pipe Market Size and Trends Analysis

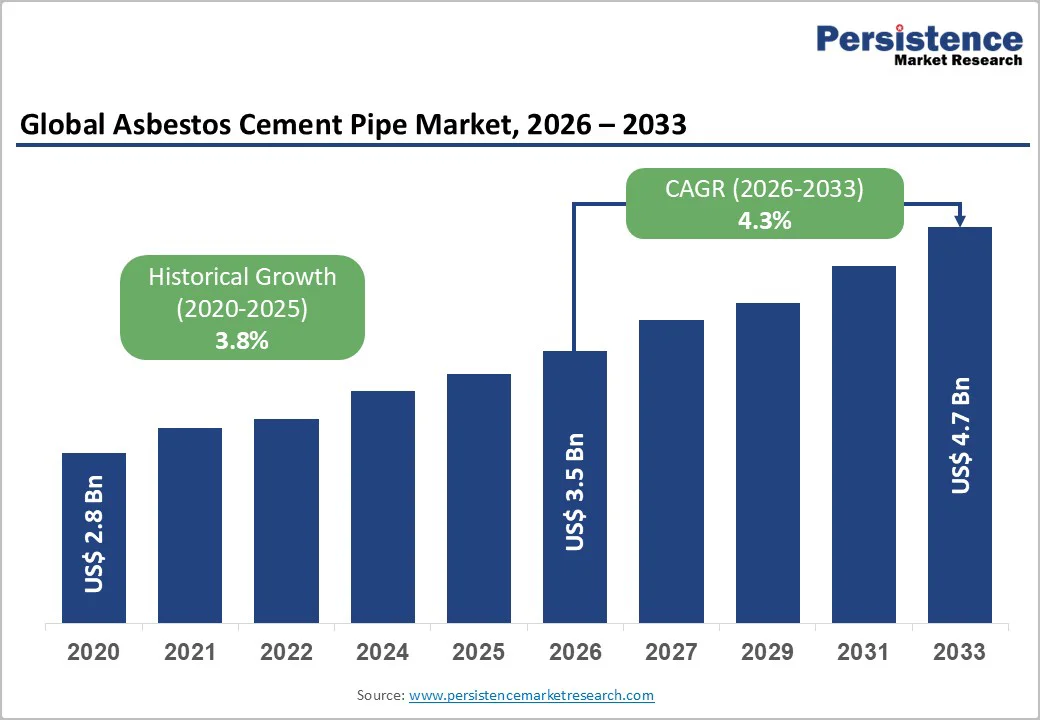

The global asbestos cement pipe market size is likely to be valued at US$3.5 billion in 2026, and is expected to reach US$4.7 billion by 2033, growing at a CAGR of 4.3% during the forecast period from 2026 to 2033, driven by the increasing demand for cost-effective piping solutions in water supply and sewerage systems, rising adoption of pressure and non-pressure pipes in municipal infrastructure, and the enduring durability of asbestos cement materials in harsh environments. Despite health and environmental concerns, asbestos cement pipes remain common in developing regions due to their corrosion resistance, long lifespan, and low cost. Legacy installations and use in agriculture and industry sustain demand, while rapid urbanization, projected to reach 68% by 2050, drives growth in reliable drainage and irrigation, especially across Asia Pacific.

Key Industry Highlights:

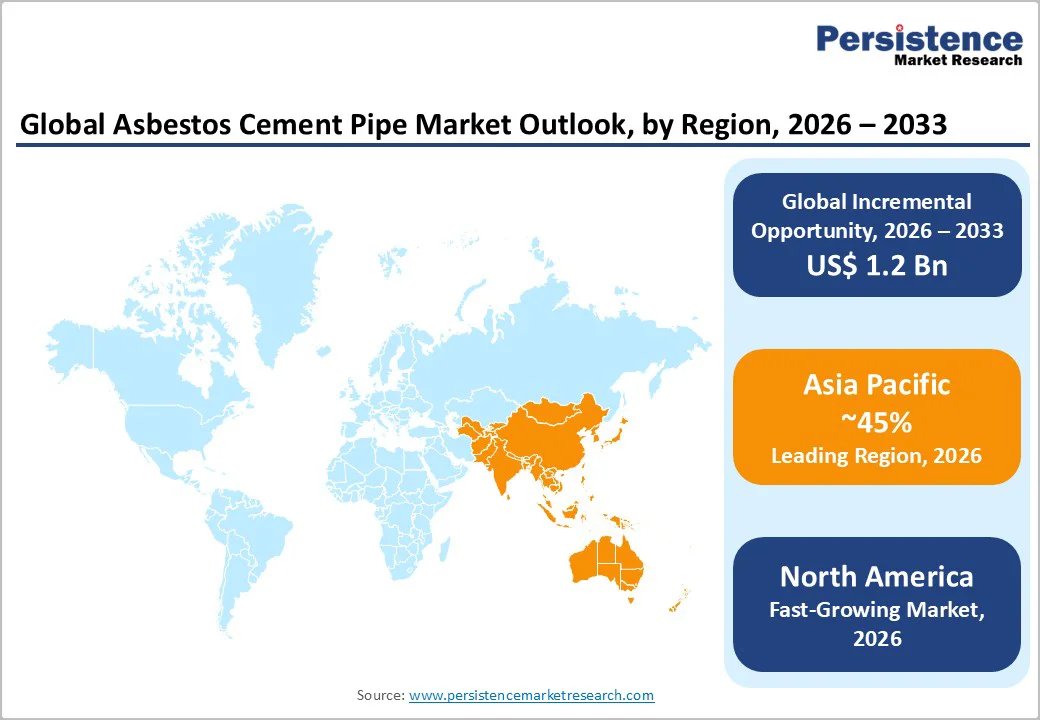

- Leading Region: Asia Pacific, anticipated to account for a 45% market share in 2026, driven by massive infrastructure development, high prevalence of municipal water projects, and cost-sensitive adoption in China and India.

- Fastest-growing Region: North America is likely to be the fastest-growing, fueled by renovation of aging infrastructure, rising awareness of pipe replacement programs, and growing investments in sustainable alternatives in the U.S.

- Dominant Product Type: Pressure pipes, to hold approximately 55% of the market share, as they are essential for high-pressure water distribution networks.

- Leading Application: Water supply, accounting for over 45% of the market revenue, due to expanding urban water distribution systems.

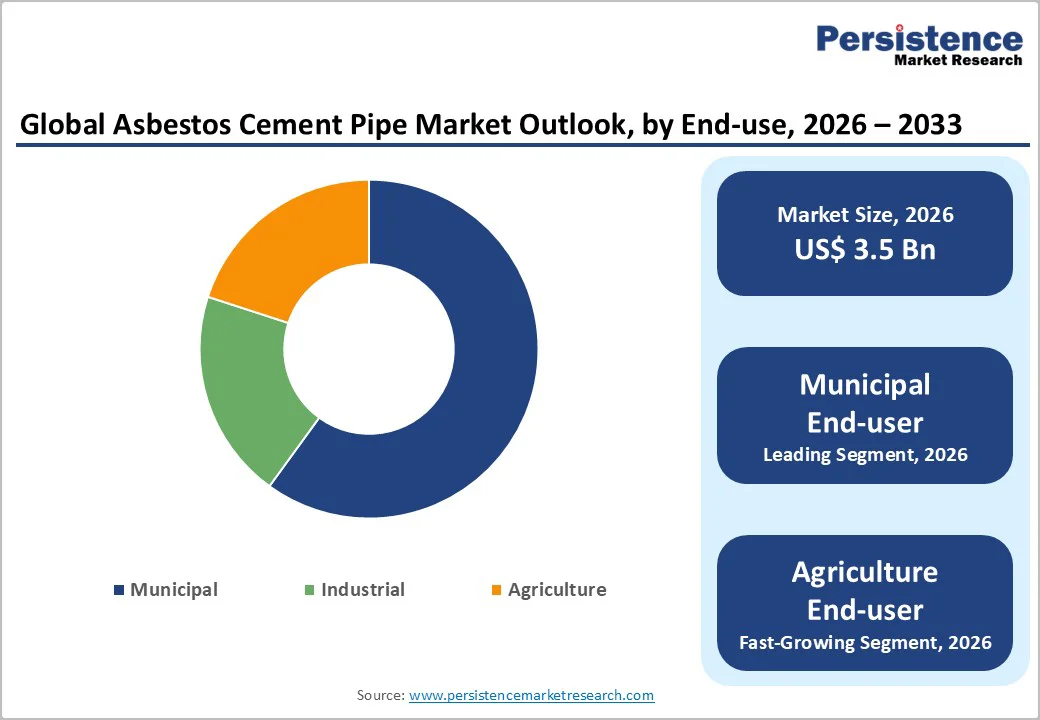

- Leading End-user: Municipal, to contribute nearly 60% of the market revenue, due to government-funded infrastructure initiatives.

| Key Insights | Details |

|---|---|

|

Asbestos Cement Pipe Market Size (2026E) |

US$3.5 Bn |

|

Market Value Forecast (2033F) |

US$4.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Demand for Cost-Effective Piping Solutions in Water Supply and Sewerage Systems

Rising demand for cost-effective piping solutions in water supply and sewerage systems is becoming a key driver of market growth, particularly as urbanization and infrastructure development accelerate across both developed and emerging economies. Municipalities and utility providers are under growing pressure to expand water distribution networks, upgrade aging pipelines, and improve wastewater management while keeping project costs under control. Cost-effective piping materials such as fiber cement, PVC, and HDPE are increasingly preferred as they offer long service life, ease of installation, and lower maintenance requirements compared to traditional metal pipes.

These materials also provide strong resistance to corrosion, chemical exposure, and environmental stress, making them ideal for large-scale water supply and sewage applications. Governments are heavily investing in sustainable water infrastructure to meet rising population needs and to reduce leakage and non-revenue water losses. Rural water development programs and smart city initiatives further boost the adoption of affordable piping systems.

High Regulatory Scrutiny and Health Concerns

High regulatory scrutiny and health concerns present significant challenges for the market, especially in sectors involving materials with potential environmental or human health risks. Governments and regulatory bodies are increasingly enforcing strict guidelines on the production, handling, and usage of certain construction and industrial materials to reduce exposure to toxic substances. This heightened oversight stems from growing awareness of the long-term health effects associated with hazardous fibers, chemicals, and airborne particulates, which can lead to respiratory illnesses, cancers, and chronic health conditions.

Manufacturers face rigorous compliance requirements, frequent inspections, and mandatory certifications, increasing operational costs and slowing product approvals. Many countries have also introduced bans or phased restrictions on materials linked to health hazards, pushing industries to transition toward safer, compliant alternatives. Public concern and pressure from environmental organizations further amplify scrutiny, influencing policy decisions and market perceptions. Companies that fail to meet evolving safety standards risk legal penalties, recalls, or reputational damage.

Advancements In Asbestos-Free Cement Composites and Pipe Rehabilitation Technologies

Advancements in asbestos-free cement composites and pipe rehabilitation technologies are creating major opportunities for modern infrastructure development. As regulations tighten and health concerns grow, industries are rapidly shifting toward safer, high-performance alternatives to traditional asbestos-containing materials. New asbestos-free cement composites made using cellulose fibers, synthetic reinforcements, and advanced binders offer excellent strength, durability, and resistance to moisture and chemicals, making them ideal for pipes, roofing, and construction applications. These innovations not only meet stringent safety standards but also reduce environmental impact, supporting global sustainability goals.

Pipe rehabilitation technologies such as cured-in-place pipe (CIPP) lining, spray-on polymer coatings, and trenchless repair systems are transforming the way aging water supply and sewer networks are maintained. These solutions allow pipelines to be restored without excavation, lowering costs and minimizing disruption to urban environments. Improved composite materials enhance the lifespan of rehabilitated pipelines, offering corrosion resistance and leak prevention.

Category-wise Analysis

Product Type Insights

Pressure pipes are anticipated to dominate the market, expected to account for approximately 55% of the share in 2026, as they are essential for high-pressure water distribution in urban and municipal networks. Their ability to withstand burst pressures of up to 20 bar ensures reliable performance in demanding environments, reducing leakage and maintenance needs. These pipes are widely used in large water supply grids, irrigation systems, and industrial fluid transport. For example, many city water authorities use high-pressure fiber-cement or HDPE pressure pipes to maintain stable water flow across long-distance distribution lines.

Non-pressure pipes represent the fastest-growing segment, driven by rapid sewerage expansion and increasing adoption in drainage and stormwater management systems. Their ability to support gravity flow without requiring high-pressure resistance makes them ideal for cost-sensitive infrastructure projects. Lightweight designs, easy installation, and lower material costs further accelerate adoption, especially in Asia Pacific and Africa, where urban development is rising quickly. For example, non-pressure fiber-cement or PVC pipes are commonly used in municipal drainage channels to efficiently manage rainwater flow and reduce flooding risks in expanding cities.

Application Insights

Water supply is expected to lead the market, holding approximately 45% of the share in 2026, driven by large-scale infrastructure development and the continuous need to expand and modernize distribution networks. Governments are increasingly investing in pipelines to ensure clean, reliable water access for growing urban and rural populations. Water supply pipes are preferred for their durability, corrosion resistance, and long operational life, making them essential for both new installations and pipeline replacement programs. For example, many municipal water boards use high-strength fiber-cement or HDPE pipelines to improve long-distance water distribution and reduce leakage in aging networks.

Sewerage systems represent the fastest-growing segment, driven by government-led sanitation initiatives and rising adoption in urban areas to improve public health and environmental management. Pipes designed for sewerage applications offer excellent corrosion resistance, durability, and sufficient flow capacity, making them ideal for wastewater and stormwater transport. The ease of installation and long service life further support rapid adoption, especially in developing regions where urbanization is accelerating. For example, many municipal sewerage projects utilize non-pressure PVC or fiber-cement pipes to efficiently manage wastewater flow, prevent leaks, and ensure sustainable sanitation infrastructure in growing cities.

End-user Insights

The municipal segment is expected to dominate the market, contributing nearly 60% of the revenue in 2026, due to extensive use in urban infrastructure and strong government funding for public works. Municipal projects require durable, high-capacity piping solutions for water supply, sewerage, and stormwater management, making them a preferred choice for large-scale installations. The segment benefits from economies of scale, long-term investment, and standardized specifications that ensure reliability and efficiency. For example, city authorities in major urban centers often use high-strength HDPE or fiber-cement pipes for municipal water distribution and sewerage networks to support growing populations and reduce maintenance costs.

Agriculture is likely to be the fastest-growing segment, driven by rising demand for efficient irrigation systems and expanding rural development projects. Farmers and agricultural organizations increasingly adopt durable and cost-effective piping solutions to support water distribution for crops, livestock, and aquaculture. Pipes designed for agricultural use resist corrosion, UV exposure, and varying soil conditions, ensuring long-term performance in diverse environments. For example, HDPE or PVC irrigation pipes are widely used in large-scale farmland projects in Asia Pacific to deliver water efficiently, reduce wastage, and improve crop yields, making them a preferred choice for sustainable agriculture.

Regional Insights

North America Asbestos Cement Pipe Market Trends

North America is driven by the need to upgrade aging water supply and sewerage infrastructure while adhering to stringent regulatory standards. Historically, asbestos cement pipes were widely used due to their durability, corrosion resistance, and cost-effectiveness. However, growing health concerns regarding asbestos exposure have led to strict regulations, phased bans, and increased scrutiny in both the U.S. and Canada. Many municipalities and utility providers are thereby replacing older asbestos cement pipelines with safer alternatives such as HDPE, PVC, and fiber-reinforced composites.

Despite regulatory restrictions, legacy asbestos cement pipes still form a significant portion of existing networks, driving demand for rehabilitation, maintenance, and safe disposal solutions. Trenchless technologies, cured-in-place pipe (CIPP) lining, and other pipe rehabilitation methods are being increasingly adopted to minimize disruption while extending the life of existing systems. The emphasis on sustainable infrastructure and reduced environmental impact is pushing utilities to adopt non-asbestos materials. Investments in smart water management, leak detection, and urban development projects continue to influence market dynamics.

Europe Asbestos Cement Pipe Market Trends

Europe is anticipated to undergo a steady transformation by modernizing its aging water infrastructure and implementing stringent environmental and safety regulations. Many countries across Western and Northern Europe are prioritizing the replacement of legacy asbestos cement pipelines installed between the 1950s and 1980s. This is driven by increased public awareness of asbestos-related health risks and stringent EU directives focused on safe handling, controlled removal, and disposal of asbestos-containing materials. The market is thereby witnessing sustained demand for inspection, maintenance, and safe removal services rather than new pipe installations.

Government-funded water quality improvement programs, leak-reduction initiatives, and urban infrastructure upgrades are supporting market activity. Eastern Europe shows comparatively slower progress, but rising investments in municipal water networks and international funding support are accelerating remediation projects. The increasing use of trenchless rehabilitation technologies, such as cured-in-place pipe (CIPP) lining, is also reshaping the market by offering cost-effective and less disruptive alternatives to full pipe replacement.

Asia Pacific Asbestos Cement Pipe Market Trends

Asia Pacific is likely to dominate with a 45% market share in 2026, led by China and India. The market is shaped by contrasting dynamics across developing and developed economies. In fast-growing countries such as India, Indonesia, Vietnam, and the Philippines, asbestos cement pipes continue to be used in certain low-pressure water distribution and drainage applications due to their affordability, durability, and ease of installation. Rapid urbanization, expansion of rural water supply schemes, and government-led sanitation programs are supporting replacement and limited new installation activity in these regions. However, rising health concerns and increasing global pressure to phase out asbestos are prompting policymakers to reassess long-term reliance on asbestos-based materials.

Developed markets such as Japan, Australia, and South Korea have already banned or severely restricted asbestos use, shifting their focus toward large-scale pipe replacement projects. This has boosted demand for inspection services, safe removal contractors, and modern alternatives such as PVC, HDPE, and ductile iron pipes. Cross-border investments, infrastructure loans from development banks, and growing emphasis on sustainable water management are accelerating modernization efforts across emerging markets.

Competitive Landscape

The global asbestos cement pipe market is highly competitive, dominated by established players such as Eternit S.A. and Visaka Industries, which benefit from longstanding manufacturing expertise, extensive distribution networks, and strong compliance capabilities. These companies have successfully maintained market relevance by aligning with evolving regulatory frameworks and adopting proactive risk-management practices in countries where asbestos use remains controlled rather than banned. As global regulations tighten, leading manufacturers are increasingly prioritizing asbestos-free innovations, investing in fiber-reinforced cement technology, alternative composite materials, and high-durability non-asbestos pipes to ensure long-term sustainability.

A key competitive strategy involves securing international certifications related to environmental safety, quality management, and occupational health standards. Such certifications enhance credibility in both domestic and export markets, particularly in regions transitioning to safer water infrastructure solutions. Additionally, market leaders are focusing on modernizing production processes, improving worker safety protocols, and offering specialized training for safe handling and installation. Partnerships with government water agencies and infrastructure contractors further strengthen their market position by enabling project-based revenue streams.

Key Industry Developments

- In January 2024, Visaka Industries Limited launched its new fiber-cement roofing and piping solutions, expanding beyond traditional asbestos cement products to include cellulose fiber alternatives, targeting markets with evolving safety regulations while maintaining cost competitiveness for infrastructure projects.

- In March 2024, Eternit S.A. announced a US$45 million investment in advanced dust control systems across its Brazilian manufacturing facilities, implementing state-of-the-art filtration and containment technologies to minimize fiber exposure during production processes while maintaining product quality standards.

Companies Covered in Asbestos Cement Pipe Market

- Eternit S.A.

- Visaka Industries Limited

- Ramco Industries Limited

- Everest Industries Limited

- Saint-Gobain PAM

- Ural Asbest

- Kazasbest

- Thai-German Ceramic Industry Public Company Limited

- PT Eternit Gresik

- Betomax

Frequently Asked Questions

The global asbestos cement pipe market is projected to reach US$3.5 billion in 2026.

The rising demand for cost-effective piping solutions in water supply and sewerage systems is the key driver.

The asbestos cement pipe market is poised to witness a CAGR of 4.3% from 2026 to 2033.

Advancements in asbestos-free cement composites and pipe rehabilitation technologies are the key opportunities.

Eternit S.A., Visaka Industries Limited, Ramco Industries Limited, Everest Industries Limited, and Saint-Gobain PAM are the key players.