- Oil & Gas

- Pipeline Integrity Management Market

Pipeline Integrity Management Market Size, Share, and Growth Forecast 2026 - 2033

Pipeline Integrity Management Market by Component (Software, Hardware, Services), Solution (Inspection Solutions, Corrosion Control Solutions, Leak Detection Systems, Risk Assessment & Integrity Analysis, Data Management & Monitoring Platforms, Predictive Maintenance & Analytics), Pipeline Type (Crude Oil Pipelines, Natural Gas Pipelines, LNG Pipelines, Refined Product Pipelines, Water & Wastewater Pipelines, Chemical Transport Pipelines), Location (Onshore, Offshore), Industry (Oil & Gas, Water & Wastewater Utilities, Chemical & Petrochemical, Energy & Power, Others), and Regional Analysis, 2026 - 2033

Pipeline Integrity Management Market Size and Trend Analysis

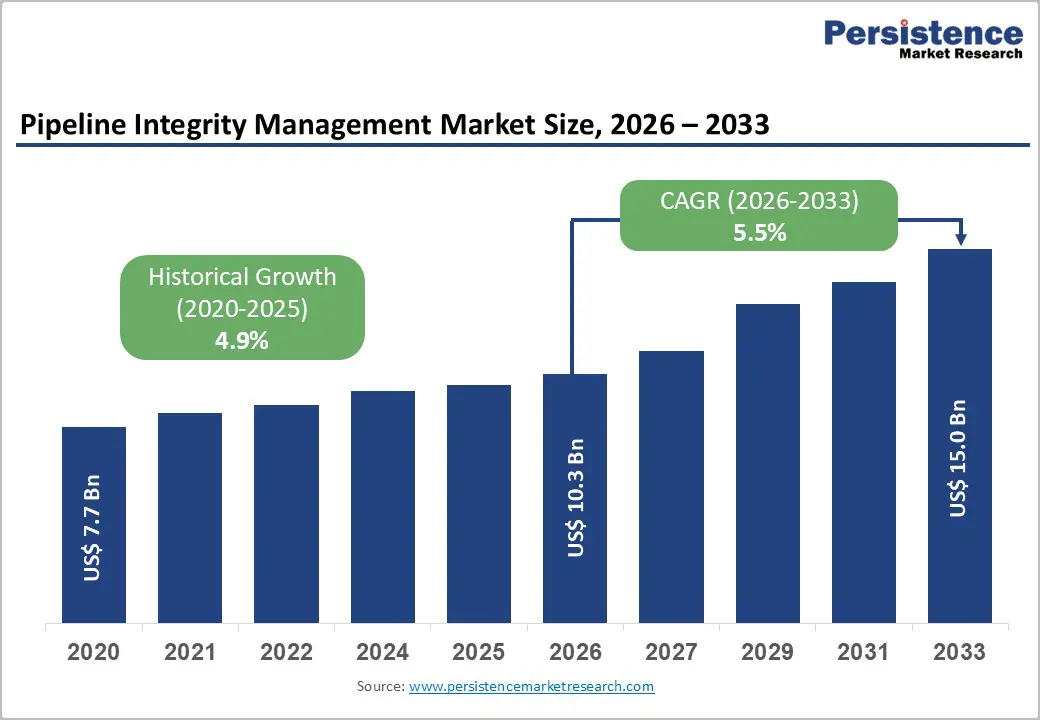

The global pipeline integrity management market size is expected to be valued at US$ 10.3 billion in 2026 and projected to reach US$ 15.0 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033.

Growth in regulatory mandates for pipeline safety, the critical need to manage aging pipeline networks, and the rapid integration of advanced digital inspection and monitoring technologies are the primary catalysts driving market expansion. The U.S. Department of Transportation’s Pipeline and Hazardous Materials Safety Administration (PHMSA) has significantly tightened safety rules, compelling operators to invest in end-to-end integrity management systems. Parallel growth in global LNG infrastructure, offshore pipeline development, and increasing energy demand across Asia Pacific and the Middle East & Africa further underpin sustained market momentum through 2033.

Key Industry Highlights

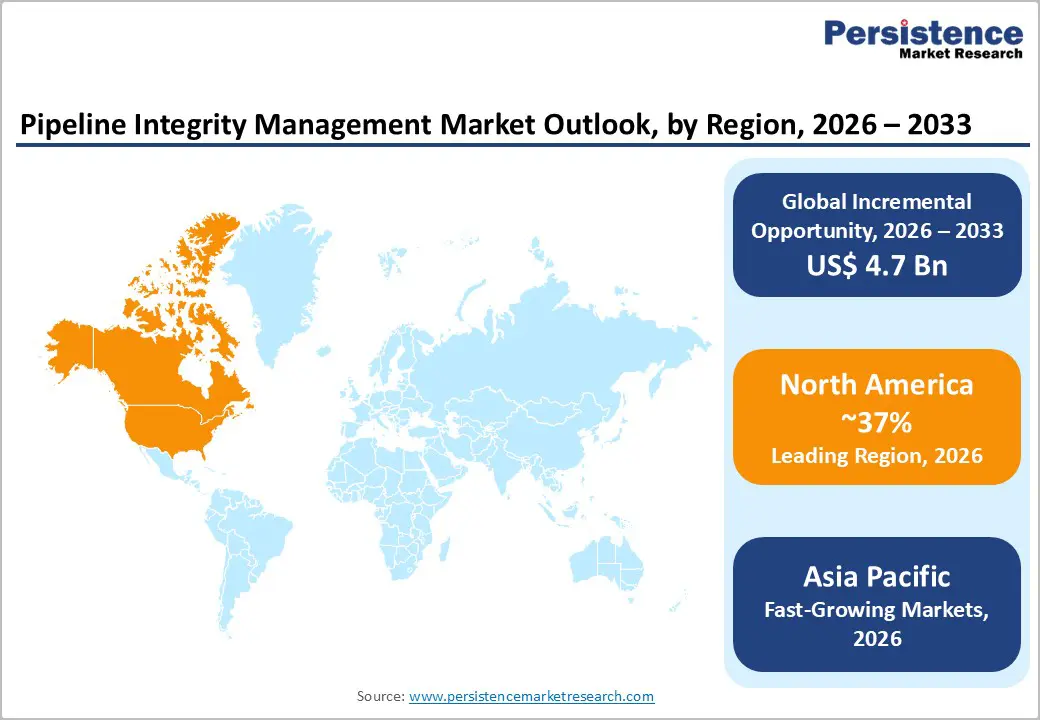

- Leading Region: North America leads the global Pipeline Integrity Management market with approximately 37% share in 2025, supported by PHMSA regulations, the PIPES Act of 2020, and extensive operator investments in digital inspection platforms across the U.S. and Canada.

- Fastest Growing Region: Asia Pacific is the fastest growing regional market during 2026 -2033, driven by China’s gas network expansion target of 300,000 km by 2030, India’s National Gas Grid initiative, and rapid LNG infrastructure development across Southeast Asia.

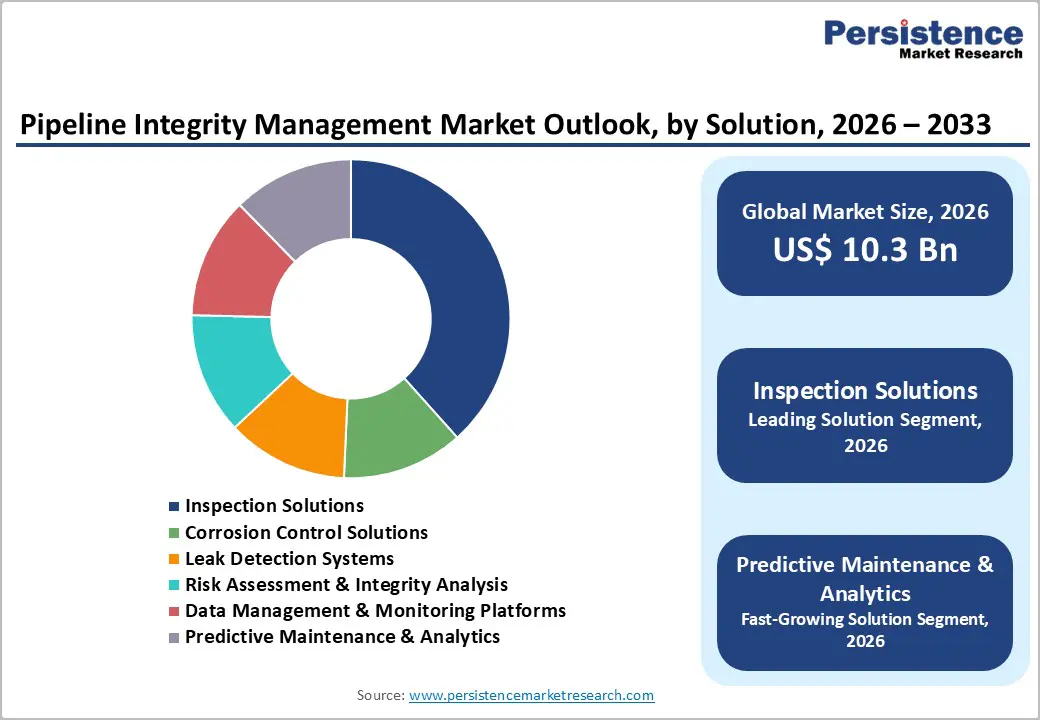

- Dominant Segment: Inspection solutions dominate the solution category with approximately 35% market share in 2025, driven by mandatory ILI requirements under PHMSA, API Standard 1163, and ASME B31.8S for high-consequence area pipelines across North America and Europe.

- Fastest Growing Segment: Predictive Maintenance & Analytics is the fastest growing solution segment, fueled by accelerating AI and IIoT adoption, DOE-funded digital monitoring research, and operator demand for reduced inspection downtime and enhanced remaining-life prediction accuracy.

- Key Opportunity: The rapid global expansion of LNG infrastructure, with IGU projecting sustained trade volume growth beyond 400 million tonnes annually, presents the most significant near-term commercial opportunity for specialized inspection and monitoring solution providers in the Pipeline Integrity Management market.

| Key Insights | Details |

|---|---|

| Pipeline Integrity Management Market Size (2026E) | US$ 10.3 Billion |

| Market Value Forecast (2033F) | US$ 15.0 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.5% |

| Historical Market Growth (2020 - 2025) | 4.9% |

Market Dynamics

Stringent Regulatory Frameworks and Aging Pipeline Infrastructure

One of the most powerful drivers of the Pipeline Integrity Management market is the expanding web of regulatory mandates governing pipeline safety across major economies. In the United States, PHMSA’s PIPES Act of 2020 and subsequent rulemakings have extended integrity management requirements to gas distribution pipelines and previously unregulated gathering lines, covering an estimated more than 2.7 million miles of pipelines across the country. In Europe, Directive 2009/73/EC and its amendments require systematic risk assessment and inspection protocols for natural gas transmission infrastructure. These regulations compel pipeline operators to adopt sophisticated integrity management platforms, inline inspection (ILI) tools, and corrosion monitoring systems. According to PHMSA, pipeline incidents in the U.S. have cost the industry over US$ 8 billion in property damage over the past decade, reinforcing the economic urgency of proactive integrity management investments.

Accelerating Digitalization and Adoption of Advanced Inspection Technologies

The transition from reactive to predictive pipeline integrity management, powered by Industrial Internet of Things (IIoT), artificial intelligence (AI), machine learning (ML), and digital twin technologies, is reshaping the competitive dynamics of the market. Modern inline inspection tools, or smart pigs, now incorporate multi-sensor platforms capable of detecting corrosion, cracks, and deformations at sub-millimeter resolution. The International Energy Agency (IEA) has highlighted digital infrastructure investment as a core pillar of energy security strategy, with global upstream oil and gas digital spending exceeding US$ 30 billion annually by 2024. Companies such as Baker Hughes and ROSEN have integrated AI-driven analytics into their inspection platforms, significantly reducing false-positive rates and enabling more accurate remaining-life assessments. This shift toward condition-based, data-driven integrity management is a structural growth driver that will sustain market expansion well through 2033.

High Capital Investment and Complex Deployment Challenges

Despite strong demand, the Pipeline Integrity Management market faces a significant barrier in the form of elevated capital requirements for deploying comprehensive integrity solutions. Inline inspection tools, fiber-optic distributed sensing systems, and real-time leak detection platforms involve substantial upfront investment, often ranging from hundreds of thousands to several million dollars per pipeline segment. Smaller regional operators and utilities in emerging markets frequently struggle to justify such expenditures within constrained operational budgets. According to the American Petroleum Institute (API), small and midsize pipeline operators account for a considerable portion of the U.S. network, yet many lack dedicated integrity management budgets, limiting market penetration in these segments.

Shortage of Skilled Workforce and Technical Expertise

The effective implementation of advanced pipeline integrity management programs demands a highly specialized workforce proficient in non-destructive testing (NDT), data analytics, pipeline engineering, and regulatory compliance. However, the global oil and gas sector is grappling with a well-documented talent shortage, exacerbated by the energy transition and demographic retirements. The World Economic Forum (WEF) has identified skills gaps in the energy sector as a critical systemic risk, noting that over 45% of energy companies report difficulty recruiting qualified inspection engineers and data scientists. This talent deficit delays project execution, inflates labor costs, and constrains the ability of pipeline operators to fully leverage the capabilities of sophisticated integrity management platforms, thereby moderating market growth in technically demanding geographies.

Expansion of LNG Infrastructure and Offshore Pipeline Networks

The rapid global expansion of liquefied natural gas (LNG) infrastructure represents a high-value opportunity for Pipeline Integrity Management solution providers. According to the International Gas Union (IGU), global LNG trade volumes surpassed 400 million tonnes in 2023 and are projected to grow substantially through the decade as Europe diversifies away from Russian pipeline gas and Asian economies accelerate LNG imports. New LNG import terminals, regasification facilities, and associated pipeline networks across Europe, Southeast Asia, and South Asia necessitate state-of-the-art integrity management solutions capable of handling cryogenic conditions and high-pressure environments. Companies investing in specialized LNG pipeline inspection technologies, cryogenic sensor arrays, and dedicated integrity analytics software stand to capture significant market share as Qatar, Australia, the United States, and Canada ramp up LNG export capacity through 2033.

AI and Machine Learning Integration Enabling Predictive Maintenance Models

The integration of AI and ML into pipeline integrity management is unlocking a new paradigm of predictive and prescriptive maintenance that presents a compelling commercial opportunity for technology vendors and service providers. Predictive maintenance models trained on historical inspection data, corrosion rates, pressure cycling, and environmental variables can forecast failure probabilities with significantly higher accuracy than rule-based approaches, reducing unplanned shutdowns and costly emergency repairs. The U.S. Department of Energy (DOE) has actively funded research into AI-based pipeline monitoring under its Advanced Research Projects Agency-Energy (ARPA-E) program. Emerson Electric and Schneider Electric have both expanded their AI-integrated pipeline monitoring portfolios in recent years, demonstrating strong commercial viability. With AI adoption in industrial asset management projected to grow rapidly through the forecast period, vendors offering embedded analytics capabilities within integrity platforms are well-positioned to command premium pricing and long-term service contracts.

Category-wise Analysis

Component Insights

The Services segment dominated the pipeline integrity management market with an estimated share of approximately 40% in 2025, driven by the persistent demand for inspection services, consulting, and ongoing maintenance and support across the global pipeline network. Pipeline operators, particularly in mature markets such as North America and Western Europe, tend to outsource specialized integrity functions to third-party service providers given the high technical complexity and regulatory sensitivity involved. According to PHMSA, annual pipeline inspection activity in the U.S. has grown consistently, with thousands of miles of high-consequence area (HCA) pipelines subject to mandatory periodic assessments. The breadth and diversity of services, ranging from inline inspection runs and cathodic protection surveys to data interpretation and regulatory reporting, make this segment the largest revenue contributor, supported by long-term service agreements with major operators including Enbridge, TC Energy, and international NOCs.

Solution Insights

Inspection Solutions, encompassing inline inspection (ILI), ultrasonic testing, magnetic flux leakage (MFL) inspection, and drone-based aerial inspection, held the leading market share position of approximately 35% in 2025. ILI remains the gold standard for assessing the internal condition of pressurized pipelines, with API Standard 1163 and ASME B31.8S mandating its use for high-consequence area integrity evaluations. The widespread regulatory requirement for ILI runs across the U.S. interstate pipeline network, which spans over 300,000 miles of hazardous liquid and natural gas lines, according to PHMSA data, making this segment structurally dominant. Advances in multi-channel MFL tools and high-resolution ultrasonic transducers have expanded the defect detection capabilities of inspection solutions, further reinforcing operator preference.

Pipeline Type Insights

Natural Gas Pipelines accounted for the leading market share of approximately 34% in 2025, reflecting the sheer scale and regulatory intensity of gas transmission infrastructure globally. According to the International Energy Agency (IEA), natural gas remains the largest single source of energy in many OECD countries and continues to serve as a critical transition fuel in decarbonization roadmaps. The U.S. alone operates one of the world’s largest natural gas pipeline networks, with PHMSA-regulated transmission mileage exceeding 300,000 miles. Regulatory frameworks such as PHMSA’s integrity management rule for gas transmission pipelines (49 CFR Part 192) mandate rigorous inspection, assessment, and remediation protocols, generating recurring demand for integrity management solutions.

Location Insights

The onshore segment held a commanding market share of approximately 65% in 2025, underpinned by the vast majority of the world’s operating pipeline infrastructure being land-based. According to PHMSA and the Interstate Natural Gas Association of America (INGAA), onshore pipelines form the backbone of energy distribution systems in North America, Europe, Russia, and increasingly in Asia Pacific and the Middle East. The concentration of regulatory oversight on onshore high-consequence area pipelines, those traversing populated areas, water bodies, and environmentally sensitive zones, generates intensive and recurring demand for integrity management services and software. While the offshore segment is growing faster due to deepwater expansion, onshore pipelines’ aggregate mileage, regulatory compliance requirements, and sheer density of infrastructure ensure continued dominance through the forecast period.

Industry Insights

The oil & gas sector represented the dominant end-use segment with an estimated market share of approximately 55% in 2025, a position reinforced by the sector’s extensive global pipeline infrastructure, high-consequence regulatory environment, and historically strong investment in integrity management practices. The American Petroleum Institute (API) and PHMSA jointly estimate that over 190,000 miles of hazardous liquid pipelines in the U.S. alone require regular integrity assessments. Major integrated oil companies including BP, Shell, ExxonMobil, and Saudi Aramco have long-established pipeline integrity departments that deploy sophisticated inspection platforms, corrosion management systems, and predictive analytics tools.

Regional Insights

North America Pipeline Integrity Management Market Trends and Insights

North America led the global Pipeline Integrity Management market with an estimated regional share of approximately 37% in 2025, driven by the world’s most extensive regulated pipeline network and a mature, enforcement-driven compliance culture. The United States is the undisputed market leader, home to over 2.7 million miles of pipelines regulated by PHMSA under statutes including the Pipeline Safety, Regulatory Certainty, and Job Creation Act and the PIPES Act of 2020. Significant investments have been allocated under the Bipartisan Infrastructure Law for pipeline safety upgrades and leak detection improvements. Canada, led by operators such as Enbridge and TC Energy, also maintains rigorous integrity standards enforced by the Canada Energy Regulator (CER).

The region’s innovation ecosystem is highly dynamic, with leading technology developers such as Baker Hughes, Emerson, and GE continuously advancing ILI platforms, fiber-optic monitoring systems, and AI-driven predictive analytics. The U.S. Department of Energy (DOE) continues to fund advanced pipeline monitoring research, while API standards set global benchmarks for integrity management practices. The convergence of regulatory tightening and technological innovation positions North America as both a demand leader and a center of excellence for pipeline integrity management globally.

Europe Pipeline Integrity Management Market Trends and Insights

Europe is a mature but dynamically evolving pipeline integrity management market, characterized by rigorous regulatory harmonization and accelerating energy security imperatives. The European Union’s Gas Regulation (EU) 2024/1789 and the broader European Green Deal infrastructure agenda have prompted significant investment in natural gas pipeline safety and leak reduction, particularly in Germany, France, Italy, and Spain. Following the disruption of Russian gas supply via Nord Stream pipelines and subsequent geopolitical uncertainties, European governments have prioritized the integrity and resilience of domestic transmission assets and new LNG import infrastructure.

The United Kingdom maintains its own rigorous standards through the Health and Safety Executive (HSE) and Ofgem. DNV GL, headquartered in Norway, remains a globally respected certification and integrity management advisory body with deep roots in the European market. The region is seeing growing adoption of digital twin platforms and remote fiber-optic monitoring, particularly among major transmission system operators (TSOs), reflecting European operators’ preference for sustainable, long-term technology investments over reactive inspection approaches.

Asia Pacific Pipeline Integrity Management Market Trends and Insights

Asia Pacific is the fastest-growing region in the Pipeline Integrity Management market and is expected to register the highest CAGR during 2026-2033, propelled by rapid energy infrastructure build-out across China, India, Japan, South Korea, and Southeast Asian nations. China has been investing aggressively in its gas distribution network; the National Development and Reform Commission (NDRC) has outlined plans to expand the domestic natural gas pipeline network to over 300,000 km by 2030, creating massive demand for integrity management solutions. India, through the Petroleum and Natural Gas Regulatory Board (PNGRB), is expanding its city gas distribution (CGD) and national transmission pipeline networks under the National Gas Grid initiative.

Japan and South Korea, as major LNG import economies, are investing in terminal infrastructure and associated pipeline networks that require specialized cryogenic integrity management solutions. The ASEAN bloc presents emerging opportunities as Vietnam, Indonesia, and Thailand expand their gas transmission infrastructure to support power sector growth. Regional players and global majors alike are establishing partnerships and joint ventures to address the unique regulatory, geological, and climatic challenges of Asia Pacific pipeline systems, making this region a strategic growth priority for market participants through 2033.

Competitive Landscape

The global pipeline integrity management market is moderately consolidated, characterized by the presence of large technology providers, engineering service firms, and specialized inspection solution companies operating across different segments of the value chain. Major participants leverage integrated portfolios combining inspection tools, monitoring technologies, analytics software, and lifecycle management services to strengthen their competitive positioning and capture long-term contracts with pipeline operators.

Market competition is largely driven by technological innovation, particularly in AI-enabled analytics, digital integrity platforms, and advanced inline inspection technologies. Companies are increasingly focusing on platform integration, predictive maintenance capabilities, and remote monitoring solutions to improve operational efficiency for pipeline operators. Strategic collaborations, acquisitions, and long-term service agreements with energy and utility companies remain key growth strategies.

Key Developments

- November, 2025: Irth Solutions announced a strategic partnership with Jee Ltd. to deliver integrated pipeline integrity management solutions across the EMEA region, combining Irth’s cloud-native Asset Integrity for Pipelines (AIP) analytics platform with Jee’s engineering expertise to enhance pipeline safety and operational efficiency.

- October, 2025: PROtect, LLC announced the acquisition of Trident Pipeline Integrity, expanding its pipeline integrity division with advanced non-destructive testing capabilities, strengthening ultrasonic inspection expertise, and enhancing regional presence in Oklahoma to support energy and industrial infrastructure clients.

Companies Covered in Pipeline Integrity Management Market

- Baker Hughes

- Enbridge

- GE (GE Vernova)

- Schneider Electric

- TC Energy

- AVEVA

- Applus+

- NDT Global

- ROSEN Group

- Infosys

- Emerson Electric

- DNV GL

- Larsen & Toubro

- TechnipFMC

- Pure Technologies (Xylem)

- T.D. Williamson (TDW)

- Oceaneering International

- Tetra Tech

Frequently Asked Questions

The global Pipeline Integrity Management market is estimated to reach US$ 10.3 billion in 2026, driven by increasing pipeline infrastructure and regulatory compliance requirements.

Demand is driven by stringent regulatory requirements, aging pipeline infrastructure, and increasing adoption of digital monitoring, predictive maintenance, and advanced inspection technologies.

North America leads the market due to its extensive pipeline network, strict regulatory framework, and strong investments in pipeline monitoring and inspection technologies.

Major opportunities include expansion of LNG infrastructure and growing adoption of AI- and analytics-based predictive maintenance solutions.

Key companies include Baker Hughes, GE Vernova, Schneider Electric, Emerson Electric, ROSEN Group, NDT Global, DNV, Applus+, TechnipFMC, and T.D. Williamson.