- Advanced Materials

- Concrete Pipes and Blocks Market

Concrete Pipes and Blocks Market Size, Share, and Growth Forecast, 2026 - 2033

Concrete Pipes and Blocks Market by Product Type (Concrete Pipes, Concrete Blocks, Reinforced Concrete Pipes, Precast Concrete Blocks), Application (Sewage Systems, Stormwater Drainage, Water Supply, Construction), End-User (Construction, Municipal, Agriculture), and Regional Analysis for 2026 - 2033

Concrete Pipes and Blocks Market Share and Trends Analysis

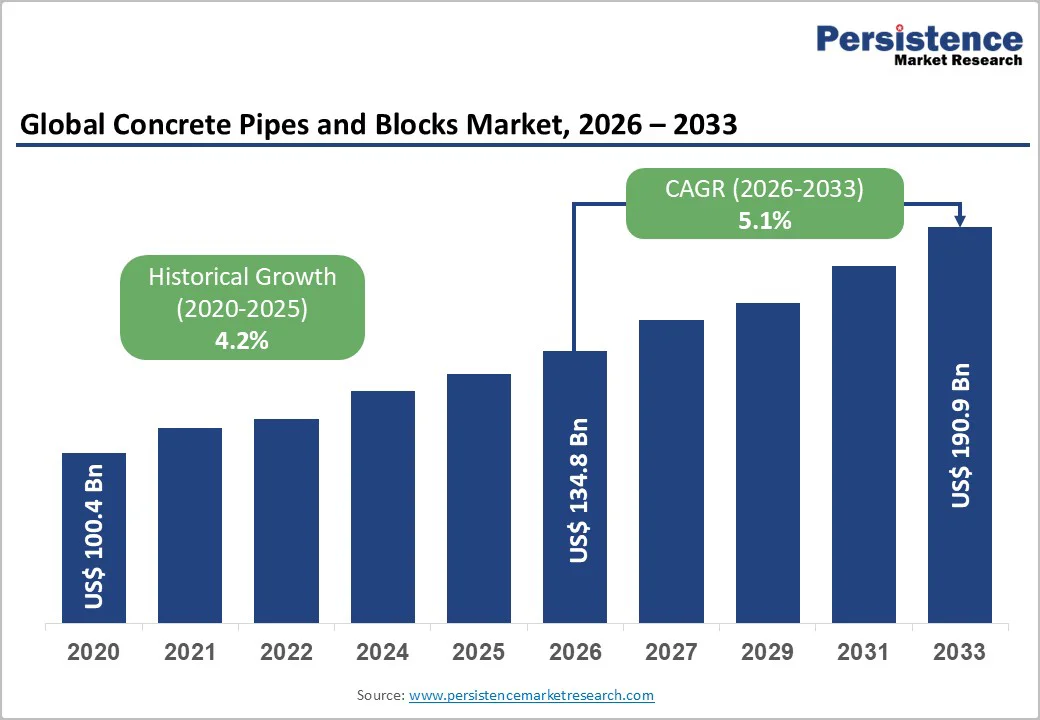

The global concrete pipes and blocks market is estimated to be valued at US$134.8 billion in 2026 and is projected to reach US$190.9 billion by 2033, growing at a CAGR of 5.1% during the forecast period 2026−2033. The market's robust expansion is fundamentally driven by accelerating urbanization across emerging economies, substantial government investments in water management infrastructure, and the construction sector's transition toward sustainable building materials.

Rising population density in urban centers necessitates advanced drainage systems, sewage networks, and water supply infrastructure, directly amplifying demand for durable concrete products.

Key Industry Highlights

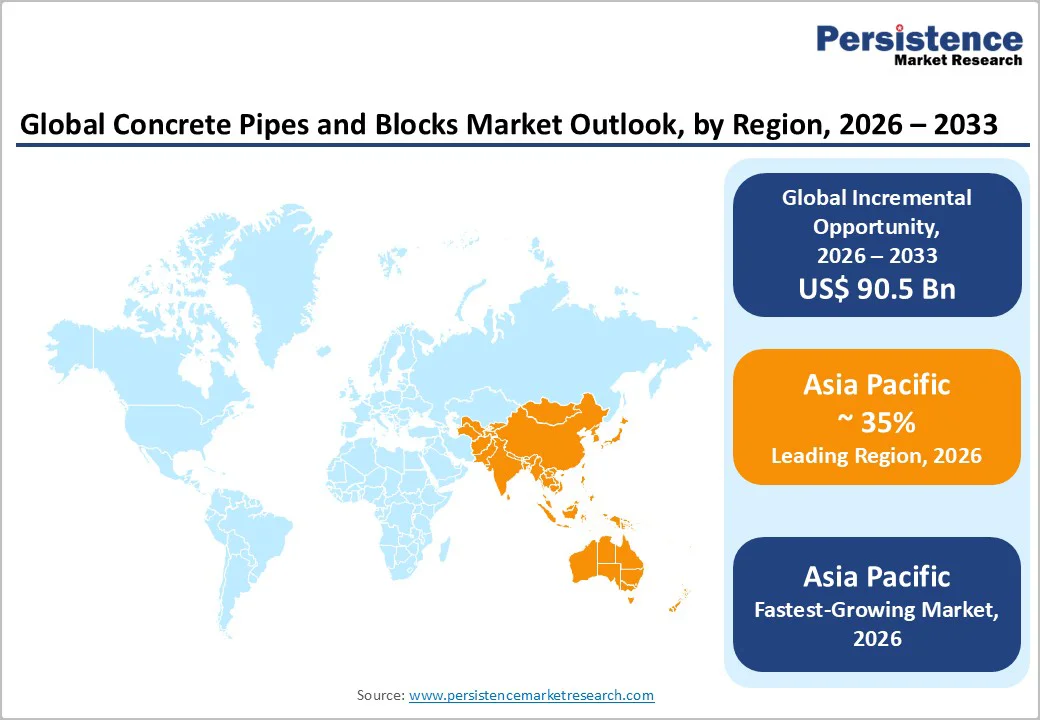

- Dominant Region: Asia Pacific is likely to dominate with about 35% of market share in 2026, and is also poised to be the fastest-growing regional market through 2033, driven by a very large and still-expanding urban population.

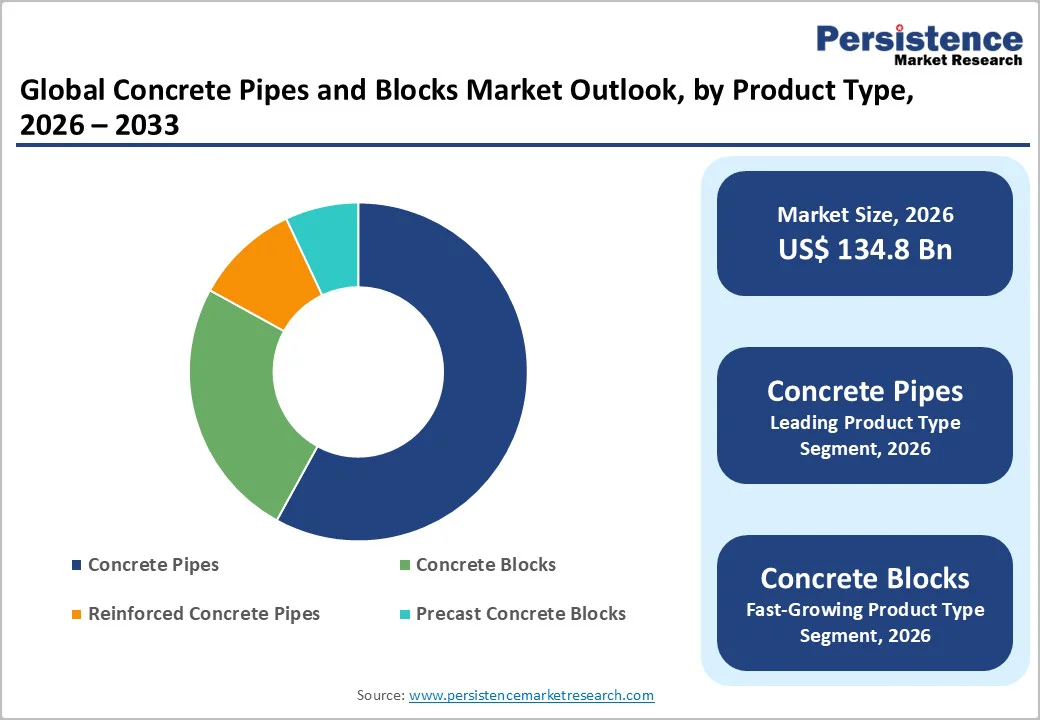

- Leading & Fastest-growing Product Types: Concrete pipes are set to lead with approximately 58% revenue share in 2026, while concrete blocks are likely to grow the fastest owing to residential construction expansion and their thermal insulation properties.

- Leading & Fastest-growing Applications: Sewage systems are anticipated to lead with an estimated 38% market share, whereas water supply is slated to be the fastest-growing due to its foundational role in ensuring the distribution and availability of potable water to communities.

| Key Insights | Details |

|---|---|

|

Market Size (2026E) |

US$134.8 Bn |

|

Market Value Forecast (2033F) |

US$190.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.1% |

|

Historical Market Growth (CAGR 2020 to 2024) |

4.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Infrastructure Modernization and Urbanization Initiatives

Rapid urbanization across the globe, particularly in Asia Pacific and other emerging economies, is creating an unprecedented demand for comprehensive infrastructure modernization and expansion. As metropolitan populations surge and cities expand both horizontally and vertically, existing water supply, wastewater treatment, stormwater management, and transportation networks are becoming critically strained, threatening public health, safety, and operational efficiency. Governments throughout the developing world recognize this infrastructure deficit and are responding with strategically planned capital investments in water systems, sanitation infrastructure, drainage networks, and road connectivity as core components of national development agendas and urban renewal initiatives. This policy emphasis reflects understanding that modern cities require integrated, resilient infrastructure systems, creating substantial and sustained demand for durable construction materials and systems that can scale efficiently to meet exponential urban growth.

Concrete has emerged as the material of choice for critical public infrastructure projects, distinguished by exceptional durability and long-term cost efficiency that align with municipal budget constraints and long-term asset management objectives. Properly engineered and constructed concrete components demonstrate service lives extending across multiple decades, maintaining structural integrity while resisting soil pressures, dynamic traffic loads, environmental weathering, and chemical exposure that would compromise alternative materials. This extended operational lifespan enables municipalities to distribute capital costs across decades of service, dramatically improving cost-benefit economics compared to materials requiring periodic replacement or intensive maintenance interventions. By minimizing lifecycle maintenance demands and avoiding disruptive replacement cycles that strain public budgets and degrade city operations, concrete infrastructure can support sustainable urban development while optimizing scarce public resources.

Capital Intensity and Market Consolidation in Concrete Manufacturing

The concrete pipe and block manufacturing sector exhibits formidable barriers to entry rooted in substantial fixed-cost requirements and specialized technical infrastructure. Establishing even a mid-sized production facility demands significant capital investment in heavy industrial equipment alongside dedicated land, utility infrastructure, quality assurance laboratories, and sophisticated material handling systems. This capital-intensive operational model ensures that only established manufacturers with integrated cement or aggregate supply chains can afford the enormous upfront investment, while smaller competitors and new market entrants struggle to secure adequate financing and technical expertise necessary for competitive production. The result is a market structure dominated by large, vertically integrated players who can amortize high fixed costs across substantial production volumes, effectively preventing fragmentation and limiting competitive dynamics in regional markets.

The geographic and economic constraints inherent in concrete logistics further entrench market consolidation while simultaneously amplifying cyclical vulnerability. Concrete products are inherently heavy and bulky commodities with minimal value density, making long-distance transportation economically prohibitive once accounting for fuel costs, tolls, infrastructure wear, and poor road conditions in developing regions. This geographic fragmentation is compounded by the construction industry's sensitivity to macroeconomic cycles, where the demand for concrete products contracts sharply during economic downturns, creating highly unpredictable revenue volatility that pressures smaller manufacturers with limited financial resilience. Evolving environmental regulations and stringent construction standards also impose continuous compliance burdens and drive innovation costs, requiring manufacturers to maintain substantial R&D and regulatory expertise, further concentrating market power.

Increasing Demand for Sustainable Construction Materials

The construction industry's accelerating transition toward environmentally conscious material selection and sustainable building practices is resulting in compelling growth opportunities for concrete pipe and block manufacturers willing to invest in ecological innovation. Regulatory frameworks, institutional investors, and end-users across developed and emerging markets are increasingly prioritizing materials that demonstrably reduce lifecycle carbon emissions, minimize waste generation, and support circular economy principles, incentivizing concrete products engineered for sustainability. Rather than competing solely on cost and availability, concrete manufacturers can now differentiate through environmental performance metrics, encouraging specification of sustainable concrete solutions in increasingly stringent green building standards and ESG-aligned procurement frameworks.

Emerging advanced concrete technologies represent a frontier of innovation opportunity that substantially enhances both environmental performance and product durability characteristics. Low-clinker cement formulations, carbon-cured concrete blocks, and biologically active self-healing concretes offer transformative possibilities in the form of extended operational service life, dramatically reduced maintenance intervention frequency, and actively sequestered atmospheric carbon during curing and throughout structural lifetime. By demonstrating that enhanced sustainability does not compromise structural performance, these innovative formulations can create compelling value propositions for discerning purchasers seeking to optimize lifecycle economics alongside environmental impact reduction.

Category-wise Analysis

Product Insights

Concrete pipes are expected to dominate, commanding approximately 58% of market share in 2026, based on their indispensable role across critical municipal infrastructure systems. Concrete pipes deliver unmatched performance in sewage collection systems, stormwater drainage networks, and potable water supply infrastructure, which require exceptional compressive strength, long-term durability, and resistance to chemical corrosion. The established institutional reliance on concrete pipe systems, coupled with their proven track record across decades of municipal deployment, creates substantial switching costs and institutional preference inertia that perpetuates market dominance. This entrenched leadership position benefits from consistent, predictable demand driven by ongoing infrastructure maintenance cycles and capacity expansion programs across large and small cities worldwide.

Concrete blocks, conversely, are predicted to grow the fastest through 2033, propelled by expanding residential construction activity and emerging applications that leverage their superior thermal insulation characteristics. Interlocking concrete block systems are gaining considerable market traction, particularly across Southeast Asian markets where construction efficiency and installation speed directly influence project dynamics and developer profitability. This segment's accelerating growth is substantively supported by technological innovations in lightweight concrete formulations that drastically reduce transportation costs and logistics complexity without compromising structural performance or durability.

Application Insights

Sewage infrastructure is poised to emerge as the leading application segment for concrete pipes and blocks, commanding approximately 38% of market revenue share in 2026. The United Nations estimates that approximately 3.4 billion people worldwide currently lack access to safely managed sanitation services, which is driving massive municipal investment in sewage network expansion, particularly across emerging economies experiencing rapid urbanization. Concrete pipes address this critical infrastructure need through exceptional chemical resistance to corrosive sewage compounds and proven ability to maintain structural integrity across multi-decade service periods without degradation or maintenance intervention. This combination of durability, reliability, and cost-effectiveness establishes concrete pipes as the overwhelmingly preferred solution for municipal wastewater conveyance systems, ensuring consistent, substantial demand as governments prioritize sanitation infrastructure as foundational to public health and urban development.

Water supply represents the fastest-growing application segment through 2033, owing to the foundational importance of water distribution to community health, economic development, and public policy frameworks. This segment benefits from increasingly stringent regulatory frameworks governing drinking water quality and safety, coupled with recognition that reliable potable water infrastructure directly influences public health outcomes and supports broader economic development. Urban planners and policymakers recognize that continuous, safe water supply represents a non-negotiable foundation for sustainable city development, elevating water infrastructure investment to a top priority within municipal capital budgets and national development programs. The convergence of regulatory mandates, public health imperatives, and policy prioritization creates a high-growth market environment where municipalities systematically expand and upgrade water distribution networks, establishing concrete pipes as the preferred material solution for infrastructure modernization programs across both developed and emerging economies.

End-User Insights

Municipal authorities are likely to be the dominant end-users for concrete pipes and blocks, securing around 52% market share in 2026. Municipalities face compounding infrastructure pressures from accelerating urbanization, escalating climate-related risks, and systematically aging infrastructure systems. These dynamics have necessitated the aggressive expansion and modernization of water supply networks, sewage collection systems, and stormwater management infrastructure. Unlike private sector construction projects, municipal infrastructure programs operate with long-term planning horizons and sustained capital budgets dedicated to essential services, generating reliable, predictable demand for concrete products across multi-year cycles. This institutional commitment to infrastructure renewal, combined with municipalities' preference for proven, durable materials with established track records, establishes concrete pipes and blocks as foundational components of government procurement strategies and ensures stable demand across markets and economic cycles.

The commercial and residential construction sector represents the fastest-growing end-user segment, propelled by accelerating building expansion across emerging markets where residential demand and commercial development are intensifying simultaneously. Concrete blocks have gained substantial traction in residential construction applications, where their superior fire resistance, effective soundproofing capabilities, and compelling cost advantage relative to traditional brick alternatives make them increasingly preferred for both exterior envelope and interior partition systems. This momentum is strongly amplified by the industry-wide transition toward sustainable and green building practices, where concrete products engineered for environmental performance, thermal efficiency, and circular-economy alignment are increasingly specified in green-certified projects. As construction practices worldwide incorporate sustainability imperatives, the demand for innovative concrete materials will establish residential and commercial construction as the primary engine for market growth.

Regional Insights

Asia Pacific Concrete Pipes and Blocks Market Trends

Asia Pacific is projected to be the leading as well as the fastest-growing regional market, accounting for roughly 35% of the concrete pipes and blocks market share in 2026. This position is underpinned by rapid, policy-backed urbanization in China, India, and Southeast Asia, where governments are rolling out large-scale programs for water supply, sewage, stormwater management, roads, metros, and industrial parks, which depend heavily on concrete infrastructure. As cities expand and megaproject pipelines lengthen, the region’s baseline requirement for concrete-based utilities and transport corridors continues to rise, creating high, sustained demand rather than short, cyclical spikes.

The competitive edge of the region is bolstered by a strong local manufacturing base, abundant raw materials, and relatively lower production and labor costs, which together enable attractive pricing and high-volume output. These structural advantages allow regional producers to efficiently serve both domestic megaprojects and export markets, while economies of scale support ongoing investment in technology and capacity. The combination of very high underlying demand, continuous project flow, and cost-efficient production gives the region a durable growth pathway and cements its role as the global growth engine for concrete pipes and blocks.

Europe Concrete Pipes and Blocks Market Trends

Europe represents a mature yet steadily expanding market for concrete pipes and blocks, driven primarily by the need for infrastructure renewal, upgrading, and decarbonization rather than new construction projects. Stringent sustainability and energy-efficiency policies, including the European Union (EU) Green Deal, National Climate Laws, and updated building codes, shape the region's construction sector, encouraging the adoption of durable, low-carbon materials and high-performance building solutions. Key countries such as Germany, France, and the U.K. lead the market, supported by large construction sectors, strong regulatory enforcement, and active infrastructure renewal programs. Germany’s emphasis on high engineering standards and energy-efficient refurbishment sustains demand for advanced precast and pipe products, while France's investments in urban transport and water management and the U.K.’s focus on flood resilience and wastewater regulation ensure a consistent demand for concrete products.

This regulatory and market environment fosters ongoing innovation and adoption of eco-friendly concrete technologies and solutions, aligning with Europe's broader climate goals and infrastructure modernization efforts. The focus on upgrading existing systems rather than greenfield projects results in steady, long-term demand from infrastructure renewal pipelines, balanced by ambitious decarbonization objectives.

North America Concrete Pipes and Blocks Market Trends

The North America concrete pipes and blocks market is shaped by a combination of ageing assets, large public funding packages, and a tightening sustainability and regulatory environment, all of which support steady growth of concrete pipes and blocks. The United States is in the centre of a major infrastructure reinvestment phase under the Infrastructure Investment and Jobs Act (IIJA), which allocates substantial funds to roads, bridges, transit, water, and wastewater systems and is widely described as the largest federal investment in water infrastructure.

The U.S. and Canada are the principal demand centers in North America, with large volumes of concrete pipes and blocks consumed across water infrastructure, transport networks, and commercial building projects. Their extensive portfolios of water supply and wastewater systems, highways, transit corridors, and urban development’s consistently require durable underground and structural components, which sustains a broad, recurring market for concrete products.

Competitive Landscape

The global concrete pipes and blocks market structure is moderately fragmented, with the top players collectively holding approximately 35-40% of the market share. Leading companies such as Brickwell, Amiantit, Oka Corporation, and Sanyou Concrete compete intensely on product quality, pricing strategies, and technological innovation to secure and expand their market presence. These firms continuously focus on broadening their product portfolios, enhancing production capacities, and adopting advanced manufacturing technologies to gain a competitive advantage within the evolving market landscape.

Market demand for sustainable construction materials is increasingly influencing corporate strategies, prompting key players to invest significantly in research and development aimed at introducing eco-friendly and high-performance concrete products. This shift not only aligns with global environmental regulations but also caters to rising consumer and governmental preferences for materials that support sustainability and reduce lifecycle environmental impacts.

Key Industry Developments

- In June 2025, Yorkshire Purchasing Organization (YPO) launched a £120 million framework agreement for construction materials, aimed at simplifying procurement and supporting public sector projects across the U.K. The framework will offer streamlined access to a wide range of essential construction products, including concrete blocks and pipes, helping local authorities and public organizations deliver infrastructure projects efficiently and cost-effectively.

- In May 2025, Birla Nuvo Limited (BirlaNU) commenced the production of autoclaved aerated concrete (AAC) at its Chennai facility, expanding its product offering in lightweight, energy-efficient construction materials. The launch supports growing demand for sustainable building solutions in India's construction sector, as AAC provides enhanced thermal insulation, fire resistance, and faster installation compared to traditional concrete blocks.

- In April 2025, GE Hitachi Nuclear, in collaboration with the U.S. Department of Energy, successfully tested new diaphragm plate steel composite (DPSC) building blocks designed to reduce nuclear construction costs by up to 10%. These steel-concrete composite modules, which can be prefabricated, shipped, and assembled on-site before being filled with concrete, offer faster construction timelines, lower labor costs, and enhanced design flexibility compared to traditional steel-concrete composites.

Companies Covered in Concrete Pipes and Blocks Market

- Amiantit

- Hanson/HeidelbergCement

- Oka Corporation

- Mexichem/Orbia

- Reinforced Concrete Pipe Association Members

- Supreme Concrete

- Brickwell

- SK Exim

- Guotong Pipes

- Julong Pipes

- Concrete Udyog

- PowerLine Concrete

- IHP

- Sanyou Concrete

- OT Concrete

Frequently Asked Questions

The global concrete pipes and blocks market is projected to reach US$ 134.8 billion in 2026.

Growing concern over environmental degradation and the negative impact of construction activities on the environment is driving the demand for sustainable and eco-friendly construction materials.

The market is poised to witness a CAGR of 5.1% from 2026 to 2033.

Some of the major opportunities in the market include the heightening need for long-lasting urban infrastructure in the form of storm drains and sewage systems, especially in municipalities in emerging economies.

Brickwell, Amiantit Oka Corporation, Sanyou Concrete are some of the key players in the market.