- Pharmaceuticals

- Oral Solid Dosage Pharmaceutical Formulation Market

Oral Solid Dosage Pharmaceutical Formulation Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Oral Solid Dosage Pharmaceutical Formulation Market by Dosage Form (Tablets, Capsules, Powders and Granules, Lozenges and Pastilles, and Gummies), by Drug Release Mechanism (Immediate Release, Delayed Release, Sustained Release, Controlled Release, and Extended Release), by Formulation Technology (Conventional Oral Solid Formulations, Modified-Release Technologies, Taste-Masking Technologies, Fixed-Dose Combinations (FDCs), and Orally Disintegrating Tablets (ODTs)), Therapeutic Area, End-user, and Regional Analysis from 2026 to 2033

Oral Solid Dosage Pharmaceutical Formulation Market Share and Trend Analysis

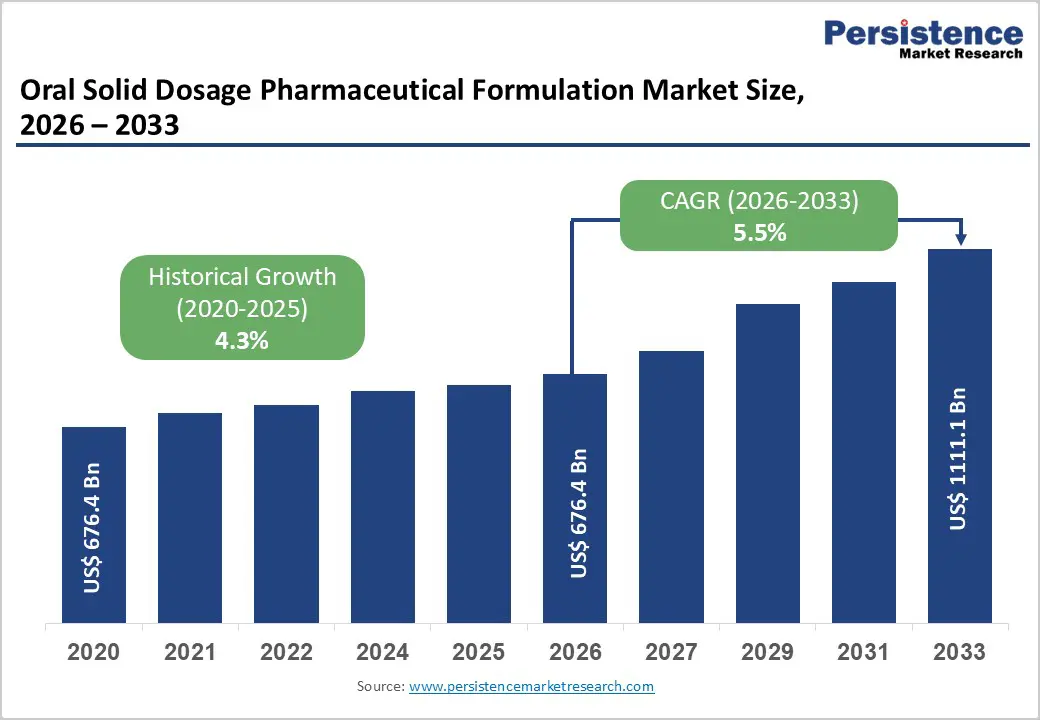

The global oral solid dosage pharmaceutical formulation market size is estimated to grow from US$ 676.4 billion in 2026 to US$ 1111.1 billion by 2033.

The market is projected to grow at a CAGR of 5.5% from 2026 to 2033. Global demand for oral solid-dose pharmaceutical formulations is rising steadily, driven by the increasing prevalence of chronic and lifestyle-related diseases such as cardiovascular disorders, diabetes, CNS conditions, gastrointestinal diseases, and cancer, as well as a strong preference for convenient, cost-effective, and patient-friendly drug-delivery routes. Widespread use of tablets and capsules across hospitals, retail pharmacies, and outpatient care settings continues to support sustained market growth.

Rising prescription volumes, long-term therapy requirements, and expanding access to essential medicines are further accelerating demand. In addition, increasing healthcare expenditure, strong penetration of generic drugs, and improved access to pharmaceutical treatments are enabling broader adoption across both developed and emerging markets. Continuous innovation in formulation science, including enhanced bioavailability, improved stability, and patient-centric dosage designs, is strengthening therapeutic outcomes and manufacturing efficiency. The growing focus on outpatient care, home-based treatment, and simplified dosing regimens is further propelling the global oral solid dosage pharmaceutical formulation market.

Key Industry Highlights:

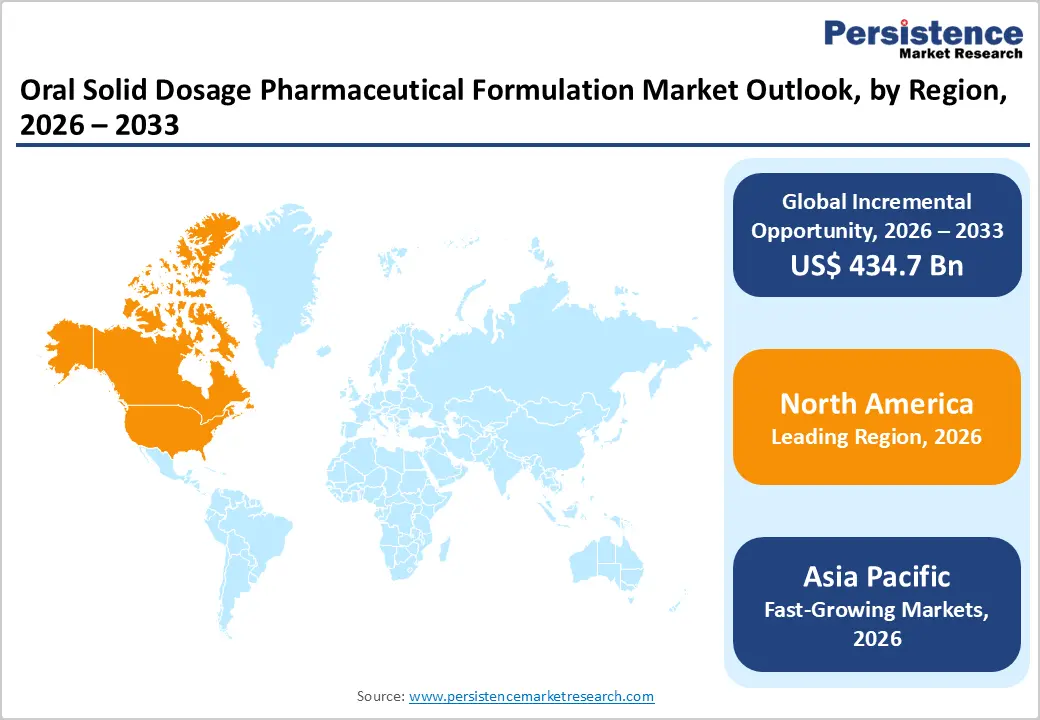

- Leading Region: North America holds the largest share at 46.7%, supported by a mature pharmaceutical manufacturing ecosystem, high prescription volumes for chronic diseases, strong generic drug adoption, advanced formulation capabilities, and the presence of leading global pharmaceutical companies.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to large patient populations, rapid growth in pharmaceutical manufacturing capacity, increasing access to essential medicines, supportive government policies, and rising demand for affordable oral therapies.

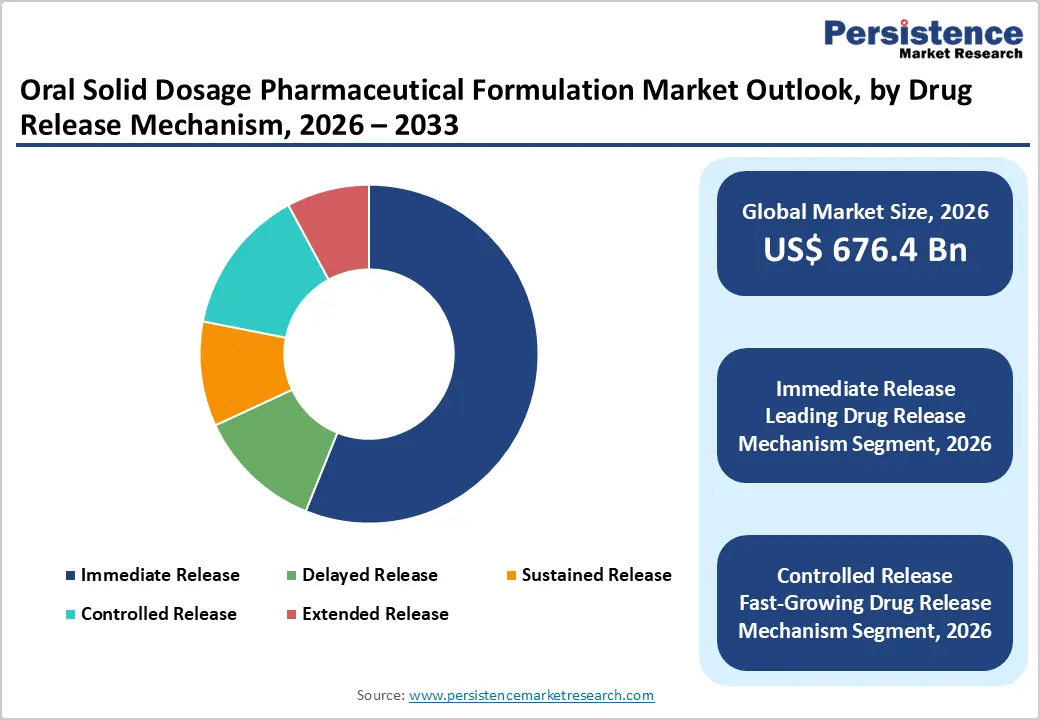

- Leading Drug Release Mechanism Segment: Immediate Release dominates the market due to ease of formulation, cost efficiency, rapid onset of action, and widespread use across acute and chronic therapies.

- Fastest-Growing Drug Release Mechanism Segment: Controlled Release is expanding rapidly as demand increases for reduced dosing frequency, improved patient adherence, and optimized long-term disease management.

- Leading Formulation Technology Segment: Conventional oral solid dosage forms remain the most widely used, owing to high-volume manufacturing, broad therapeutic applicability, and established regulatory pathways.

- Fastest-Growing Formulation Technology Segment: Modified-release technologies are expanding rapidly as pharmaceutical companies focus on product differentiation, lifecycle extension, and improved clinical outcomes through advanced oral delivery systems.

| Key Insights | Details |

|---|---|

| Oral Solid Dosage Pharmaceutical Formulation Market Size (2026E) | US$ 676.4 Bn |

| Market Value Forecast (2033F) | US$ 1111.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Dynamics

Driver - Growing Chronic Disease Burden and Preference for Convenient Oral Therapies

The rising incidence of chronic and lifestyle-related diseases is a primary force accelerating demand for oral solid dosage formulations worldwide. Conditions such as cardiovascular disorders, diabetes, neurological diseases, gastrointestinal ailments, and oncology increasingly require long-term or lifelong pharmacotherapy, making orally administered medicines the most practical option. Tablets and capsules are widely preferred by both clinicians and patients due to ease of administration, dosing accuracy, portability, and suitability for self-management outside clinical settings.

Aging populations across developed and emerging economies further amplify demand, as elderly patients often rely on multiple oral medications for chronic disease control.

Additionally, healthcare systems are shifting toward outpatient care and home-based treatment models, reinforcing reliance on oral solid dosage forms rather than injectable or hospital-administered therapies. Advances in formulation science, such as modified-release profiles, fixed-dose combinations, and taste-masking technologies, are improving therapeutic outcomes and patient adherence. Regulatory support for generic drug substitution and cost-effective oral medicines also contributes to volume growth. Together, these clinical, demographic, and systemic factors continue to strengthen demand for scalable, patient-friendly oral solid dosage formulations across global healthcare markets.

Restraints - Formulation Complexity, Manufacturing Costs, and Regulatory Stringency

Despite strong demand, several challenges constrain the broader expansion of oral solid-dose development and commercialization. Increasing formulation complexity, particularly for poorly soluble or highly potent APIs, raises development timelines and manufacturing costs. Advanced technologies such as controlled-release matrices, multilayer tablets, and abuse-deterrent formulations require specialized equipment, skilled personnel, and rigorous process validation, which may limit adoption among smaller manufacturers.

Supply-side pressures, including fluctuating raw material prices, excipient shortages, and energy costs, further affect production economics. Stringent regulatory requirements across major markets add additional hurdles, as authorities demand robust bioequivalence data, stability testing, and compliance with evolving quality standards.

Delays in regulatory approvals can impact time-to-market, especially for generic manufacturers operating in competitive pricing environments. Operational challenges such as scale-up failures, batch variability, and dissolution inconsistencies also pose risks. In cost-sensitive regions, pricing controls and reimbursement limitations may restrict profitability, discouraging investment in advanced oral formulations. These technical, regulatory, and economic constraints collectively moderate growth momentum, particularly for complex or high-value oral solid dosage products.

Opportunity - Expansion of Advanced Formulations, Generics, and Outsourced Manufacturing

Significant growth opportunities are emerging from innovation in formulation technologies and shifting pharmaceutical business models. Rising adoption of modified-release systems, orally disintegrating tablets, and fixed-dose combinations creates avenues for product differentiation and lifecycle extension. These formats improve patient adherence, reduce dosing frequency, and enhance therapeutic effectiveness, particularly in chronic disease management.

The global push toward affordable healthcare is also accelerating demand for high-quality generic medicines, thereby increasing volume requirements for oral solid-dose manufacturing. Contract development and manufacturing organizations are gaining prominence as pharmaceutical companies outsource formulation development, scale-up, and commercial production to optimize costs and focus on core R&D activities. Emerging markets present additional opportunities due to expanding healthcare access, rising prescription volumes, and government support for local pharmaceutical manufacturing.

Digitalization of manufacturing, including process analytics and continuous production, further enhances efficiency and quality consistency. As personalized medicine evolves, flexible oral dosage platforms capable of dose customization and combination therapy are gaining attention. These trends position advanced, scalable, and outsourced oral solid dosage solutions as a key growth avenue over the medium to long term.

Category-wise Analysis

By Dosage Form Insights

The tablets segment is projected to dominate the global oral solid dosage pharmaceutical formulation market in 2026, accounting for 68.2% of revenue. This leadership is driven by tablets’ unmatched advantages in large-scale manufacturing, cost efficiency, dose accuracy, and long shelf life. Tablets remain the preferred dosage form across hospitals, retail pharmacies, and public health programs due to ease of administration, high patient compliance, and flexibility in formulation design. They are widely used in chronic therapies for cardiovascular diseases, diabetes, CNS disorders, and anti-infective agents, enabling consistent long-term treatment.

Advances in coating technologies, modified-release systems, and fixed-dose combinations further enhance therapeutic performance and lifecycle management. Tablets also support broad geographic distribution due to stability under varied storage conditions. Growing demand for generic medicines, government-led procurement programs, and expansion of outpatient treatment models continue to reinforce the dominance of tablets, making them the most commercially viable and widely adopted oral solid dosage form globally.

By Therapeutic Area Insights

The cardiovascular segment is expected to lead the global oral solid-dose pharmaceutical formulation market in 2026, accounting for 22.5% of revenue. This dominance is attributed to the high and growing prevalence of cardiovascular diseases worldwide, particularly among aging populations and patients with lifestyle-related risk factors. Oral solid dosage forms are extensively used in cardiovascular therapy due to their suitability for long-term administration, dose consistency, and patient adherence.

Tablets and capsules are widely prescribed for hypertension, hyperlipidemia, heart failure, and arrhythmias, driving sustained formulation demand. The widespread use of fixed-dose combinations to simplify treatment regimens further supports segment growth. The increasing focus on preventive care, routine screening, and early disease management drives ongoing use of cardiovascular medications. Additionally, the strong penetration of generic cardiovascular drugs across emerging and developed markets increases volume demand, ensuring that this therapeutic area remains the largest contributor to overall oral solid dosage formulation revenues.

By End-user Insights

The pharmaceutical companies segment is projected to dominate the global oral solid dosage pharmaceutical formulation market in 2026, accounting for 42.0% of revenue. This leadership is driven by the extensive formulation capabilities, broad therapeutic portfolios, and high-volume production capacities of branded pharmaceutical companies. These players invest heavily in formulation R&D, enabling continuous development of modified-release products, fixed-dose combinations, and patient-centric oral dosage forms.

Pharmaceutical companies maintain strong control over product commercialization, regulatory approvals, and global distribution, supporting consistent demand for oral solid formulations. Their dominance is further reinforced by robust pipelines targeting chronic diseases, oncology, and metabolic disorders, which rely heavily on oral therapies. Long product lifecycles, strong brand recognition, and sustained investments in manufacturing infrastructure enable pharmaceutical companies to maintain scale advantages. Strategic collaborations with CDMOs and expansion into emerging markets further strengthen their position as the primary end users in the global market.

Regional Insights

North America Oral Solid Dosage Pharmaceutical Formulation Market Trends

North America is expected to dominate the global oral solid dosage pharmaceutical formulation market in 2026, with a 46.7% value share, primarily driven by the United States. The region benefits from a highly advanced pharmaceutical manufacturing ecosystem, a strong presence of multinational pharmaceutical companies, and widespread adoption of oral therapies across both chronic and acute disease areas. High prevalence of cardiovascular disorders, diabetes, CNS conditions, and oncology drives sustained demand for oral solid formulations. Favorable reimbursement frameworks, strong insurance coverage, and high prescription volumes support consistent market growth.

North America also demonstrates early adoption of advanced formulation technologies, including modified-release systems, fixed-dose combinations, and patient-centric dosage designs. Strict regulatory standards encourage continuous innovation and quality optimization in formulation development. Additionally, strong generic drug penetration, expansion of outpatient care, and increasing emphasis on medication adherence further reinforce market leadership. Ongoing investments in R&D, digital manufacturing, and supply chain resilience ensure the region's sustained dominance.

Europe Oral Solid Dosage Pharmaceutical Formulation Market Trends

Europe’s oral solid-dose pharmaceutical formulation market is expected to grow steadily in 2026, supported by aging populations, the rising prevalence of chronic diseases, and robust public healthcare systems. Countries such as Germany, the U.K., France, Italy, and the Nordic nations exhibit consistent demand for oral solid formulations due to widespread access to prescription medicines and structured treatment protocols. Cardiovascular, CNS, and gastrointestinal therapies account for a significant share of oral dosage consumption. A strong emphasis on generic drug adoption and cost-containment strategies increases demand for tablets and capsules.

Europe also benefits from robust regulatory frameworks that promote formulation quality, bioequivalence standards, and patient safety. Increasing use of fixed-dose combinations and modified-release products supports therapeutic optimization and adherence. Growth in outpatient care, home-based treatment models, and preventive healthcare further increases the utilization of oral dosages. Continuous investments in manufacturing modernization and formulation innovation ensure stable long-term growth across the region.

Asia Pacific Oral Solid Dosage Pharmaceutical Formulation Market Trends

The Asia Pacific oral solid dosage pharmaceutical formulation market is projected to register a higher CAGR of around 8.7% between 2026 and 2033, driven by the rapid expansion of healthcare infrastructure and rising patient populations. Large and growing markets such as China, India, Japan, and South Korea contribute significantly to regional demand due to the increasing prevalence of chronic diseases and expanding access to essential medicines.

Government initiatives to strengthen pharmaceutical manufacturing, improve insurance coverage, and expand public health programs support large-scale adoption of oral solid dosage forms. Cost-effectiveness and ease of distribution make tablets and capsules the preferred choice across urban and rural healthcare settings.

The region is also witnessing rapid growth in generic drug production, contract manufacturing, and localized formulation development. Rising investments by global pharmaceutical companies, combined with technology transfer and workforce training, enhance manufacturing capabilities. Increasing focus on preventive care, chronic disease management, and affordable therapies further accelerates market growth across the Asia Pacific.

Competitive Landscape

The global oral solid dosage pharmaceutical formulation market is highly competitive, with strong participation from AstraZeneca Plc., Bristol-Myers Squibb Company, Eli Lilly and Company, Gilead Sciences, and Merck and Co. Inc. These players leverage global manufacturing footprints, robust distribution networks, strong brand equity, and continuous innovation in formulation science, drug release technologies, excipient optimization, and scalable production processes to address a wide range of therapeutic applications.

Rising prevalence of chronic diseases, increasing preference for patient-friendly oral therapies, and growing demand for cost-effective mass-manufactured medicines are driving innovation across the market. Manufacturers are focusing on modified-release formulations, fixed-dose combinations, taste-masking technologies, and orally disintegrating formats, while prioritizing partnerships with CDMOs, expansion into emerging markets, and sustained R&D to enhance bioavailability, compliance, and lifecycle management.

Key Industry Developments:

- In February 2026, BioNxt Solutions Inc., a bioscience company focused on advanced drug delivery platforms, announced that it has entered into a non-binding letter of intent (LOI) for a proposed transaction under which BioNxt would obtain exclusive rights to an advanced drug chaperone technology designed for oral dissolvable applications from a third-party biotechnology developer specializing in chaperone-enabled delivery systems.

- In September 2024, Thermo Fisher Scientific announced the expansion of its oral solid dose development and manufacturing capabilities across North America, strengthening its integrated CDMO platform. The expansion is aimed at supporting increasing demand for complex oral formulations, accelerating scale-up, and improving supply reliability for pharmaceutical and biotechnology customers.

Companies Covered in Oral Solid Dosage Pharmaceutical Formulation Market

- AstraZeneca Plc.

- Bristol-Myers Squibb Company

- Eli Lilly and Company

- Gilead Sciences

- Merck and Co. Inc.

- Novartis AG

- Pfizer Inc.

- AbbVie Inc.

- Boehringer Ingelheim GmbH

- F. Hoffman-La-Roche Ltd.

- Johnson and Johnson

- Biogen Inc.

- Bayer AG

- Teva Pharmaceuticals

- Amgen Inc.

- Others

Frequently Asked Questions

The global oral solid dosage pharmaceutical formulation market is projected to be valued at US$ 676.4 Bn in 2026.

The market is primarily driven by the rising prevalence of chronic diseases and aging populations increasing long-term oral medication demand, coupled with technological advancements in formulation and patient-centric drug delivery systems.

The global oral solid dosage pharmaceutical formulation market is poised to witness a CAGR of 5.5%between 2026 and 2033.

Key opportunities lie in expansion of fixed-dose combinations and adoption of advanced technologies such as 3D printing and personalized oral formulations.

AstraZeneca Plc., Bristol-Myers Squibb Company, Eli Lilly and Company, Gilead Sciences, and Merck and Co. Inc., are some of the key players in the oral solid dosage pharmaceutical formulation market.