- Telecommunications

- Mobile Value-Added Services Market

Mobile Value-Added Services Market Size, Share, and Growth Forecast 2026 - 2033

Mobile Value-Added Services Market by Platform (Short Message Service, Interactive Voice & Video Response, Wireless Application Protocol, Unstructured Supplementary Service Data, Others), by Application (Mobile Browsing, Location Based Services, Entertainment Services, Mobile Texting, Others), by End User (Consumer, Enterprise, Network Provider), by Regional Analysis, 2026 - 2033

Mobile Value-Added Services Market Size and Trend Analysis

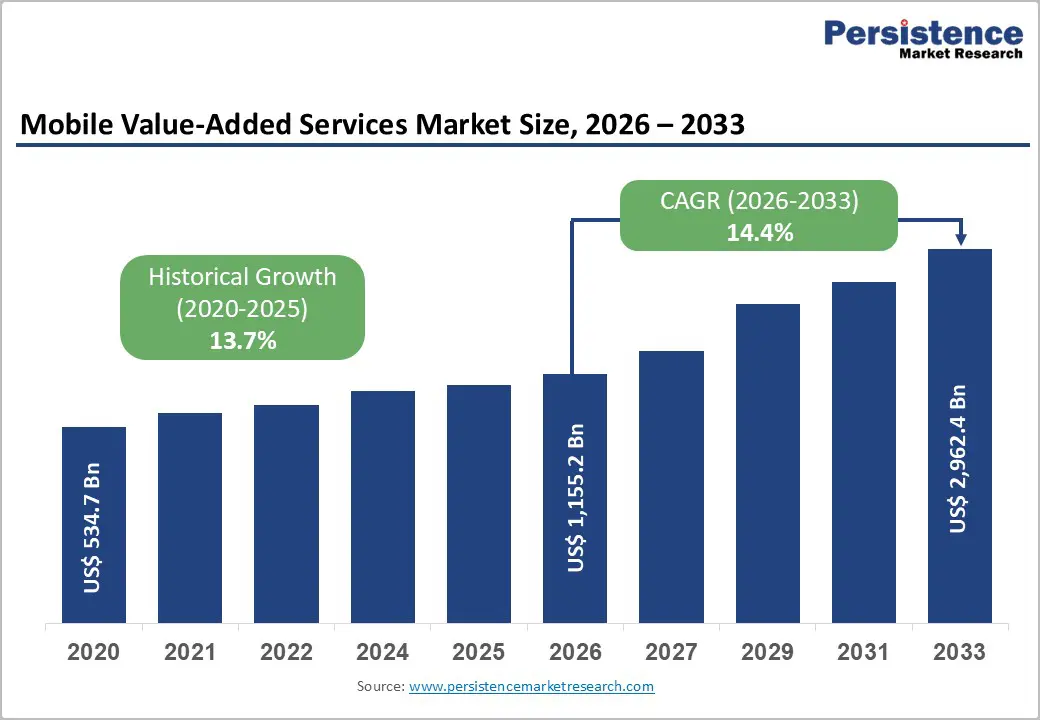

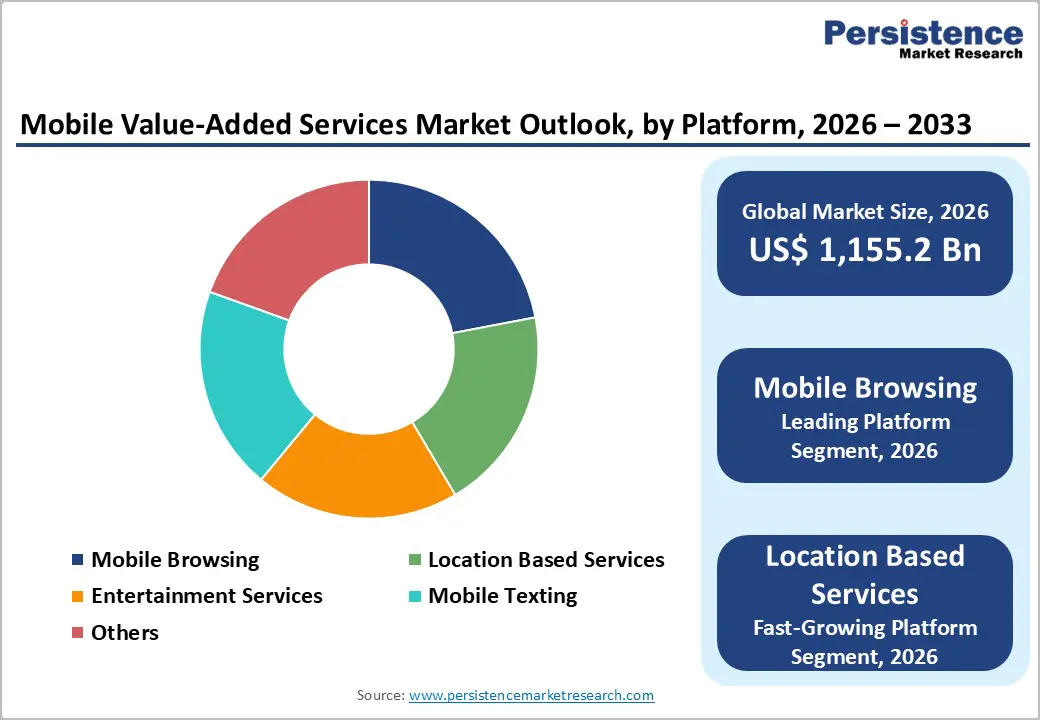

The global Mobile Value-Added Services market size is expected to be valued at US$ 1,155.2 billion in 2026 and projected to reach US$ 2,962.4 billion by 2033, growing at a CAGR of 14.4% between 2026 and 2033.

The market is witnessing strong growth fueled by rising smartphone penetration and growing demand for personalized, context-driven mobile experiences. As both consumers and enterprises increasingly adopt digital-first interactions, telecom operators and technology providers are deploying advanced technologies such as artificial intelligence, machine learning, and 5G to deliver innovative VAS solutions. This expansion is creating new opportunities beyond traditional voice and data services.

Key Market Highlights

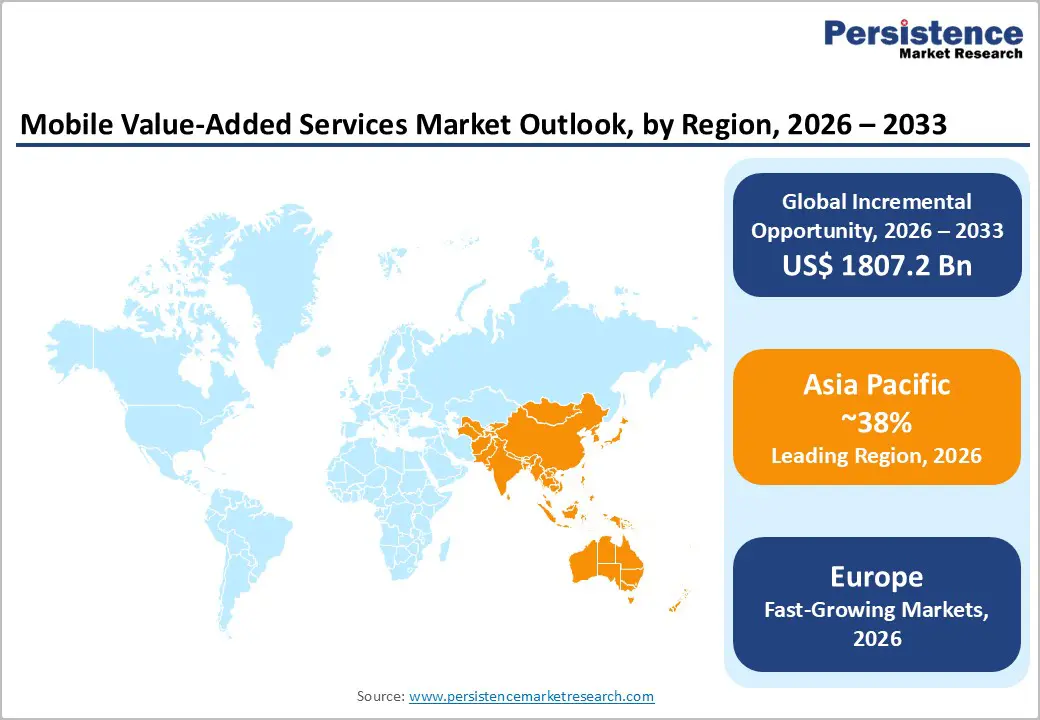

- Dominant Region: Asia Pacific leads the global MVAS market with 38% market share in 2025, driven by large populations, rapid urbanization, smartphone penetration exceeding 83%, and fintech ecosystem growth.

- Fastest Growing Region: Asia Pacific shows the fastest growth globally, with 5G deployment enabling enterprise adoption and data-intensive applications across healthcare, logistics, manufacturing, and digital commerce.

- Dominant Segment: SMS maintains market leadership with 35% market share, supported by universal compatibility, critical role in 2FA and transactional communications, and reliability in banking, healthcare, and retail.

- Fastest Growing Segment: Location-Based Services (LBS) is the fastest-growing application, expanding at a CAGR of 15.84%, driven by enterprise adoption for operational optimization, proximity marketing, asset tracking, and supply chain management.

- Key Market Opportunity: Enterprise digital transformation and workplace modernization create substantial growth opportunities for secure mobile VAS that address hybrid work collaboration and mobile customer relationship management integration.

| Key Insights | Details |

|---|---|

|

Mobile Value-Added Services Size (2026E) |

US$ 1,155.2 billion |

|

Market Value Forecast (2033F) |

US$ 2,962.4 billion |

|

Projected Growth CAGR(2026-2033) |

14.4% |

|

Historical Market Growth (2020-2025) |

13.7% |

Market Dynamics

Market Growth Drivers

Increasing Smartphone Penetration and Mobile Internet Adoption

The global surge in smartphone adoption is a key driver of growth in the Mobile Value-Added Services (MVAS) market. By 2026, smartphone connections are expected to reach approximately 7.5 billion units, with Asia Pacific and Africa leading in adoption. Advanced mobile devices with improved processing power and connectivity are fueling demand for data-intensive services such as mobile gaming, streaming, and location-based applications.

This growing digital ecosystem allows service providers to launch innovative offerings that boost engagement and retention. Research shows that markets like China and India are at the forefront, with smartphone penetration projected to reach 83% by 2025. MVAS solutions are increasingly contributing to higher average revenue per user (ARPU), often achieving up to a 30% increase compared to traditional voice and data services.

5G Technology Deployment and Enhanced Connectivity Infrastructure

The global expansion of 5G networks is transforming the MVAS landscape by providing ultra-low latency, higher bandwidth, and advanced network capabilities. By 2030, 5G connections are projected to exceed 5.6 billion, with 65% operating on standalone networks. These advancements support immersive applications such as virtual reality, augmented reality, high-definition streaming, and industrial IoT solutions, creating new revenue opportunities for providers.

Telecom giants like Vodafone, AT&T, and Verizon have invested roughly US$ 70 billion in 5G spectrum and infrastructure development. Enhanced connectivity enables premium VAS delivery with superior service quality, supporting enterprise applications across healthcare, logistics, manufacturing, and smart city initiatives. This robust infrastructure expansion represents a significant growth catalyst for the MVAS market globally.

Market Restraints

Regulatory Compliance and Data Privacy Constraints

The growing number of data protection regulations, such as GDPR in Europe and CCPA in North America, creates significant compliance obligations for mobile service providers. These laws require explicit user consent, robust security measures, and strict transparency in privacy policies. Non-compliance can result in substantial financial penalties, increasing operational and technological challenges for VAS providers globally.

Mobile developers and VAS operators face added complexity in managing cross-border data flows and obtaining consent across jurisdictions. Regulatory scrutiny, such as from France’s CNIL, has led to formal notices and fines for non-compliant mobile applications. Compliance requirements increase operational costs, extend the time-to-market for new VAS offerings, and limit providers’ ability to innovate quickly or diversify their service portfolios.

Ecosystem Fragmentation and Multi-Platform Complexity

The mobile ecosystem is highly fragmented across platforms, operating systems, and service delivery models, posing technical and commercial challenges for VAS providers. Solutions must be compatible with Android, iOS, and enterprise systems, each with unique specifications, security needs, and user experience standards. Over-the-top (OTT) messaging apps like WhatsApp, Telegram, and Signal further fragment communication channels, increasing competition for traditional SMS-based VAS.

Providers must navigate complex interoperability requirements, adapt to diverse regional deployment standards, manage legacy system technical debt, and innovate to meet evolving customer expectations. This fragmentation drives up development costs, lengthens implementation timelines, and limits scalability and operational efficiency for global VAS platforms, constraining overall market growth potential.

Market Opportunities

Enterprise Digital Transformation and Workplace Modernization

Enterprise adoption of mobile value-added services is accelerating due to global shifts toward hybrid work, remote collaboration, and digital transformation initiatives. Organizations increasingly require secure mobile messaging, CRM solutions, video conferencing, and cloud-based enterprise applications to enable seamless communication and access to data across distributed teams. These solutions support operational efficiency and digital-first workflows.

Telecom operators like Deutsche Telekom, Orange, and Telefónica are partnering with enterprise software providers to deliver industry-specific VAS solutions addressing healthcare compliance, financial security standards, and manufacturing technology integration. Enterprise VAS adoption is growing at the fastest pace across end-user segments, driven by demand for mobile-first security architectures, integrated productivity platforms, and scalable, flexible infrastructure tailored to vertical market needs.

Entertainment Services and Mobile Gaming Market Expansion

The entertainment and mobile gaming segment is one of the fastest-growing areas within the MVAS market, fueled by technological innovations, expanding broadband infrastructure, and evolving consumer preferences for mobile-first experiences. Mobile gaming drives significant data usage and revenue through in-app purchases, premium subscriptions, and advertising, creating substantial monetization potential for service providers.

Asia Pacific is emerging as the most dynamic entertainment market, with China, India, and Southeast Asia showing rapid adoption. Streaming services, interactive apps, and user-generated content are increasing premium data consumption, enabling operators to offer tiered pricing, bundled entertainment packages, and superior quality-of-service options. Companies like Apple, Tencent, and Google are investing heavily in integrated entertainment VAS platforms that combine gaming, streaming, and content discovery.

Category-wise Insights

Platform Analysis

The Short Message Service (SMS) platform continues to dominate the Mobile Value-Added Services market, capturing approximately 35% of total market share in 2025. Its universal compatibility, high reliability, and critical role in enterprise communications ensure sustained demand. SMS powers mission-critical applications such as two-factor authentication (2FA), OTP delivery, transactional banking alerts, healthcare appointment reminders, and e-commerce notifications, with 68% of daily global messages transactional.

While SMS leads in adoption and reliability, Rich Communication Services (RCS) is emerging as the fastest-growing platform segment. RCS offers enriched messaging capabilities, including multimedia, interactive content, and enhanced customer engagement features. Enterprises are increasingly exploring RCS for marketing campaigns, brand communication, and customer support, leveraging its ability to deliver a richer, more interactive user experience than traditional SMS, despite limited early adoption.

Application Analysis

SMS and transactional alerts dominate with approximately 41% market share, particularly in banking, healthcare, and e-commerce. LBS, while rapidly expanding, is emerging as a high-growth application. Enterprises are adopting location analytics for asset management, personnel tracking, and proximity marketing. Mobile wallets and payment platforms increasingly incorporate LBS features for contactless payments and location-based offers, broadening their applications beyond navigation and advertising.

Location-Based Services (LBS) are emerging as the fastest-growing application within the MVAS market, driven by technological advancements, smartphone penetration, and enterprise adoption. LBS leverages GPS, geofencing, and proximity marketing to deliver contextual offers, asset tracking, and real-time navigation across sectors such as retail, logistics, healthcare, and transportation. Its integration with enterprise solutions enhances operational efficiency and customer engagement.

End User Analysis

Network providers represent the largest revenue contributor in the MVAS market, accounting for approximately 46% of total end-user market share in 2025. Leading telecom operators such as Vodafone, China Mobile, Bharti Airtel, and Verizon leverage VAS to diversify revenue, enhance customer retention, and increase ARPU. Providers bundle connectivity, entertainment, cloud, and financial services to differentiate from commoditized offerings and strengthen their market position.

The enterprise segment is the fastest-growing end-user category, driven by the adoption of mobile messaging, CRM integration, video conferencing, and productivity tools. Enterprises are deploying VAS for workforce collaboration, secure communication, and customer engagement across healthcare, finance, government, and logistics sectors. Tailored, industry-specific solutions in this segment create significant revenue potential, positioning enterprise customers as a major growth opportunity for the MVAS market.

Regional Insights

North America Mobile Value-Added Services Market Trends and Insights

North America holds a significant share of approximately 28% of the global MVAS market in 2025, driven by advanced telecommunications infrastructure, high smartphone penetration, and enterprise demand for mobile solutions. The U.S., valued at around US$ 242.37 billion in 2024, leads regional growth, supported by extensive 5G deployment, smart home integration, and enterprise digital transformation initiatives across healthcare, logistics, and financial services.

Telecom operators such as AT&T and Verizon are deploying immersive services including augmented reality, cloud-based enterprise VAS, and mobile financial solutions like Apple Pay and Google Wallet. Integration of IoT capabilities in energy management, home security, and health monitoring within converged service portfolios further strengthens regional growth, providing telecom providers with opportunities to enhance customer engagement and increase average revenue per user.

Europe Mobile Value-Added Services Market Trends and Insights

Europe represents a mature, highly regulated MVAS market, characterized by strong regulatory frameworks, sophisticated consumer demand, and significant infrastructure investment. Leading operators such as Deutsche Telekom, Orange, Telefónica, and Vodafone are monetizing VAS through convergent offerings that combine fiber-optic broadband, 5G, and entertainment services. The European MVAS market is projected to grow at a CAGR of 6.4% between 2026 and 2033, driven by enterprise adoption, data privacy compliance, and digital advertising innovation.

Enterprise VAS adoption is particularly strong due to GDPR and cybersecurity regulations, with operators investing in privacy-compliant digital advertising platforms and fixed-mobile convergence (FMC) portfolios. Deutsche Telekom’s MagentaOne has demonstrated 3.8% growth in FMC customers across Central and Eastern Europe. Compliance-driven innovation enables European operators to differentiate offerings, providing privacy-preserving services that strengthen competitive positioning and consumer trust.

Asia Pacific Mobile Value-Added Services Market Trends and Insights

Asia Pacific dominates the global MVAS market, commanding approximately 38% of total market share in 2025, driven by rapid urbanization, mobile internet adoption, and large-scale smartphone penetration. Key markets such as China, India, and Japan are fueling growth with massive populations, high mobile commerce activity, and advanced technology adoption. China’s mobile payments ecosystem, led by WeChat Pay and Alipay, drives integration of entertainment, social, and financial services.

India’s telecom sector is expanding rapidly, supported by government initiatives such as BharatNet, which enhance rural digital infrastructure and create opportunities in mobile banking, payments, and location-based services. The region’s 5G deployment is accelerating, with 1.9 billion subscriptions expected by 2028, enabling data-intensive VAS like augmented reality, HD streaming, and industrial IoT. Southeast Asian countries, including Indonesia, the Philippines, and Vietnam, also demonstrate strong growth potential.

Competitive Landscape

The Mobile Value-Added Services market is moderately consolidated, dominated by major telecommunications operators and technology platforms, alongside a broad ecosystem of specialized service providers and application developers. Incumbent operators leverage network infrastructure and customer relationships, while technology firms focus on platform capabilities, application development, and content delivery. Market participants implement vertical integration strategies and partnerships to expand service portfolios, enhance engagement, and differentiate offerings across consumer and enterprise segments.

Specialized VAS providers compete through technological innovation, including AI-driven personalization, cloud-native service delivery, and API-based integration. Competitive differentiation increasingly relies on ecosystem collaborations and privacy-by-design architectures, ensuring compliance with global data protection regulations and offering secure, scalable, and customized VAS solutions across industries.

Key Market Developments

- In January 2025, Vodafone Idea Limited announced commencement of 5G service deployment in Mumbai telecom circle, with subsequent expansion planned to Delhi, Bihar, Karnataka, and Punjab, establishing competitive positioning within India's mobile value-added services market through enhanced network capabilities supporting advanced VAS offerings.

- In October 2024, Deutsche Telekom AG, Orange S.A., Telefónica S.A., and Vodafone Group Plc established a joint venture for a privacy-by-design digital advertising platform compliant with European GDPR and ePrivacy directives, representing a strategic collaboration addressing targeted mobile advertising services while maintaining regulatory compliance across European markets.

- In December 2024, Ant Group restructured Alipay into Digital Payment and Alipay Business units, pivoting toward merchant SaaS, credit-technology, and local services marketing to diversify revenue streams beyond payment transaction fees and enhance monetization of ecosystem traffic within China's mobile financial services market.

Companies Covered in Mobile Value-Added Services Market

- Vodafone Group Plc

- AT&T Inc.

- Verizon Communications Inc.

- China Mobile Limited

- Orange S.A.

- Bharti Airtel Limited

- Telefónica S.A.

- Deutsche Telekom AG

- Tencent Holdings Limited

- Google LLC

- Apple Inc.

- Comviva Technologies Limited

- InMobi Pte. Ltd.

- OnMobile Global Limited

- ZTE Corporation

Frequently Asked Questions

The global Mobile Value-Added Services market is projected to reach US$ 1,155.2 billion in 2026, up from US$ 534.7 billion in 2020.

Key drivers include smartphone penetration exceeding 85% by 2025, 5G deployment, enterprise digital transformation, and demand for personalized mobile experiences.

Asia Pacific is expected to dominate, driven by large populations, 83% smartphone penetration, rapid urbanization, and advanced mobile commerce ecosystems.

Opportunities exist in enterprise digital transformation, mobile financial services, entertainment and gaming, LBS, and 5G-enabled immersive applications.

Major market players include telecommunications operators Vodafone Group Plc, AT&T Inc., Verizon Communications Inc., China Mobile Limited, Orange S.A., Bharti Airtel Limited, Deutsche Telekom AG, and Telefónica S.A.