- Technology

- Location-Based Services (LBS) Market

Location-Based Services (LBS) Market Size, Share, and Growth Forecast, 2026 - 2033

Location-Based Services (LBS) Market by Technology (GPS, Assisted GPS (A-GPS), Enhanced GPS (E-GPS), Enhanced Observed Time Difference (E-OTD), Wi-Fi, Cellular ID, Others), Application (GIS & Mapping, Navigation & Tracking, Geo Marketing & Advertising, Social Networking & Entertainment, Fleet Management, Others), End-User (Transportation & Logistics, Manufacturing, Retail & Consumer Goods, Automotive, Healthcare, Government & Public, Aerospace & Defense, Others), and Regional Analysis for 2026 - 2033

Location-Based Services (LBS) Market Share and Trends Analysis

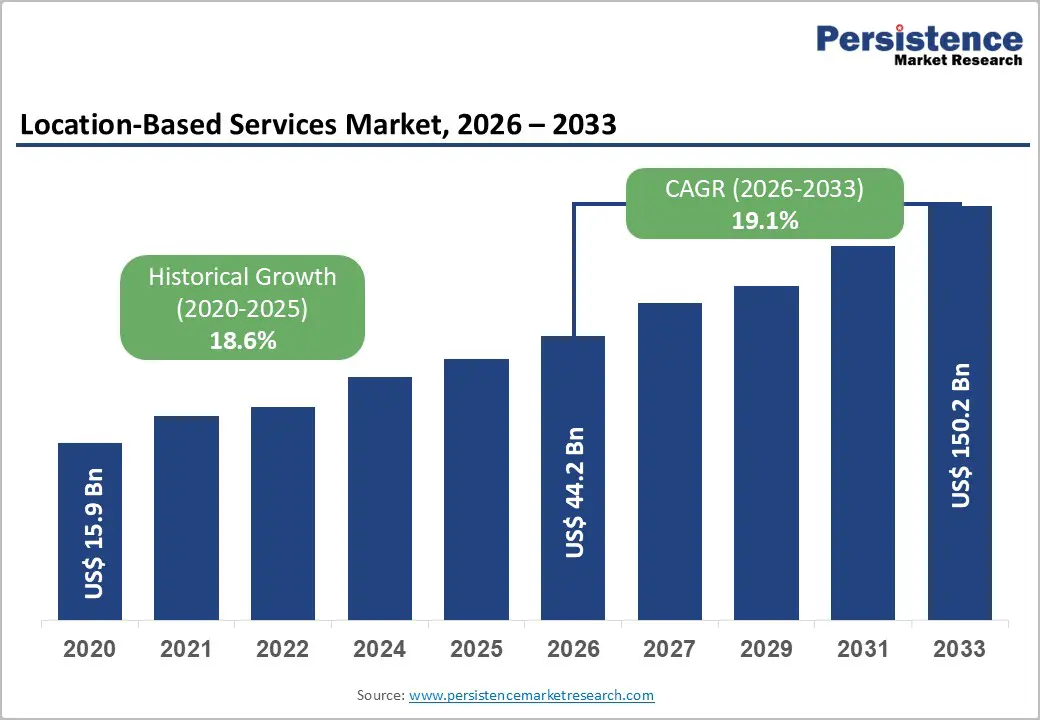

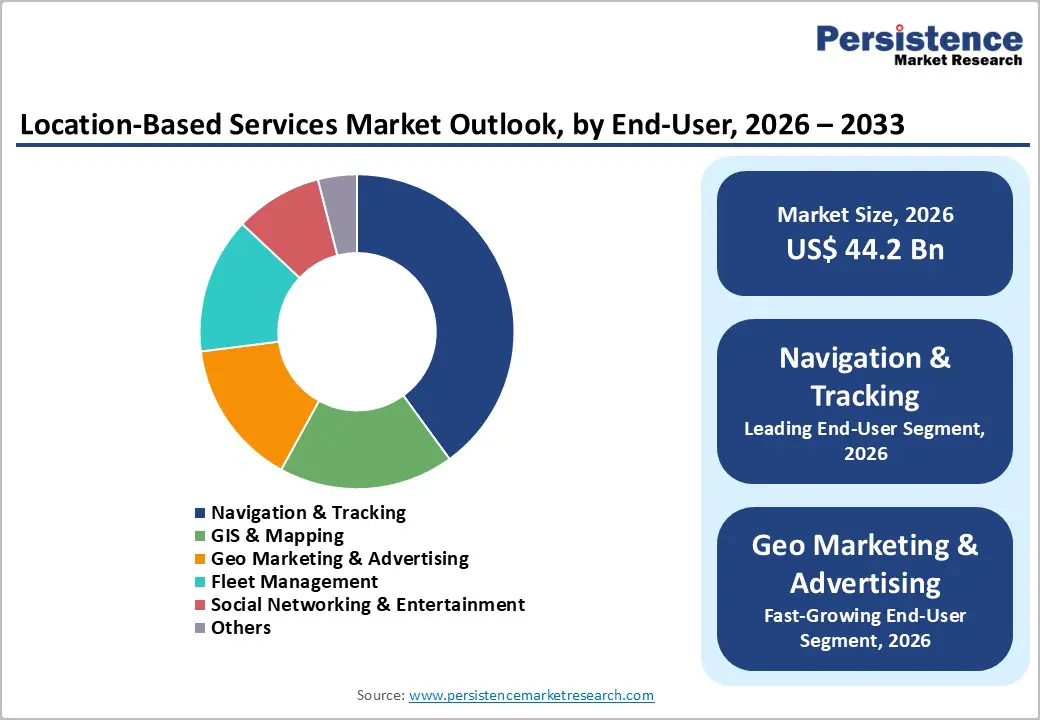

The global location-based services (LBS) market size is likely to be valued at US$ 44.2 billion in 2026, and is projected to reach US$ 150.2 billion by 2033, growing at a CAGR of 19.1% during the forecast period 2026−2033.

Advancements in Global Positioning System (GPS), fifth-generation (5G) connectivity, and the increasing use of mobile devices across sectors such as transportation, healthcare, retail, and logistics are mainly propelling market growth. The integration of LBS into smart devices and the rising demand for real-time data analytics and location-based marketing are reshaping consumer engagement. While growth opportunities abound, challenges such as high infrastructure costs and data privacy concerns may limit the pace of expansion.

Key Industry Highlights

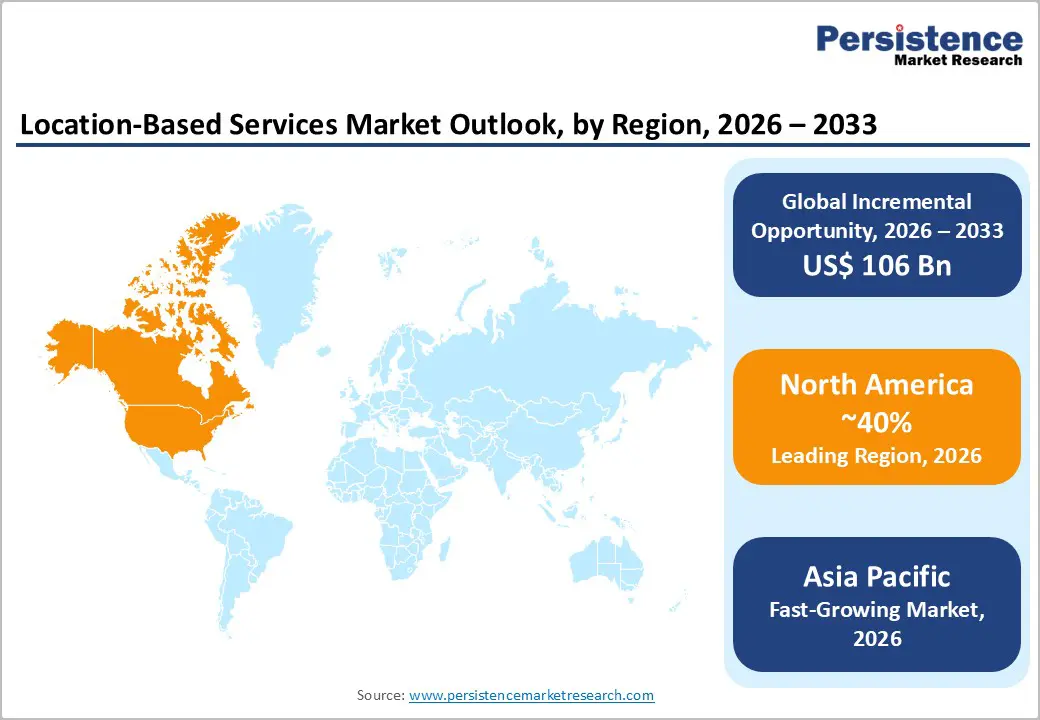

- Dominant Region: North America is set to hold 40% of the LBS market in 2026, driven by advanced tech, high smartphone use, and widespread adoption across key industries.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing LBS market from 2026 to 2033, propelled by rising smartphone adoption and massive growth in e-commerce and logistics.

- Leading Application: Navigation and tracking services are likely to lead with about 40% market share in 2026 due to growing demand for efficient route planning, fleet management, and real-time location tracking.

- Fastest-growing Application: Geo marketing and advertising is slated to grow the fastest through 2033, fueled by the increased use of location data for targeted advertising, personalized promotions, and data analytics.

- July 2025: Stellantis partnered with 4screen to integrate real-time LBS into FIAT, Jeep, and Ram vehicles' Uconnect systems, enabling drivers to discover nearby restaurants, charging stations, and dealerships directly via infotainment.

| Key Insights | Details |

|---|---|

|

Location-Based Services (LBS) Market Size (2026E) |

US$ 44.2 Bn |

|

Market Value Forecast (2033F) |

US$ 150.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

19.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

18.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Proliferation of Smartphones and Connected Devices

The widespread use of smartphones and connected devices has been propelling the growth of location-based services by embedding advanced features such as GPS, Bluetooth, and various sensors for precise, real-time user tracking. Businesses have been harnessing this data to deliver hyper-personalized offerings, including tailored marketing campaigns and dynamic promotions tied to immediate surroundings, which sharpen customer engagement and streamline operations like delivery routing. Enterprises are being encouraged to treat these capabilities as foundational assets that not only boost immediate response times but also cultivate long-term loyalty through context-aware interactions.

Billions of interconnected devices have been broadening LBS applications across sectors by flooding systems with actionable location intelligence, enabling refined tactics from immersive retail navigation to efficient fleet coordination. The fusion of Internet of Things (IoT) sensors, GPS accuracy, and high-speed networks such as 5G has been elevating data reliability and responsiveness, which unlocks predictive analytics for demand forecasting and hazard avoidance. Organizations are increasingly auditing their device ecosystems to prioritize scalable integrations, ensuring they capture emerging value while navigating privacy mandates for sustained competitive advantage.

Privacy and Data Security Concerns

Privacy and data security concerns have been posing a major obstacle to the location-based services market growth, as they can expose sensitive details such as current positions, movement habits, and individual tastes to potential breaches or exploitation. Users have been growing wary of how providers handle this information, especially when firms repurpose it for unsolicited ads or profiling without clear permission, which erodes confidence and slows market penetration. Organizations are being advised to embed privacy-by-design principles early, conducting regular audits to align with user expectations and preempt backlash from mishandled data.

Businesses operating in LBS have been compelled to fortify defenses through advanced encryption, anonymization techniques, and explicit consent mechanisms amid tightening rules from bodies such as the General Data Protection Regulation (GDPR). This regulatory push has been intensifying the tension between crafting bespoke experiences and upholding ironclad protections, where lapses risk fines, eroded brand equity, and client exodus. Forward-thinking leaders are prioritizing transparent policies and ethical frameworks, which will have not only neutralized threats but also differentiated them as trustworthy partners in a data-saturated landscape.

Expansion in Indoor Positioning Technologies

The expansion of indoor positioning technologies presents a key opportunity due to the increasing demand for precise location tracking in indoor environments. Traditional GPS systems face limitations in indoor spaces, where signal obstruction and interference can reduce accuracy. Indoor positioning systems (IPS) leverage technologies such as Wi-Fi, Bluetooth, and RFID (Radio Frequency Identification) to enable accurate tracking within buildings, malls, airports, and other indoor environments. This opens up new avenues for businesses across sectors to offer tailored services, such as navigation, asset tracking, and personalized customer experiences, without the constraints of outdoor positioning. For example, in September 2025, OpenSpace launched AI Autolocation, a spatial AI technology that delivers real-time indoor positioning on standard smartphones without beacons, by matching sensor data to 360° site maps for construction field productivity.

As industries such as retail, healthcare, and logistics seek to improve operational efficiency and customer engagement, the demand for indoor positioning systems is growing. The ability to track assets in real-time, provide location-based promotions, or enhance emergency response services provides a clear competitive advantage. With the rising adoption of smart building technologies and the increasing investment in infrastructure, IPS allows businesses to capitalize on untapped market segments. Companies that integrate these advanced indoor technologies will be positioned to enhance customer experiences and optimize business operations in ways previously unattainable with outdoor-only tracking systems.

Category-wise Analysis

Technology Insights

GPS is likely to be the leading segment with a projected 45% of LBS market revenue share in 2026 due to widespread adoption and established infrastructure across both consumer and enterprise applications. The ability of this technology to provide accurate, real-time location data is crucial for navigation, fleet management, and geo-marketing. For example, in August 2025, TRAC Intermodal launched GeoFleet, an on-demand chassis solution using geofencing and GPS for usage-based billing, guaranteed availability, and real-time tracking to enhance flexibility amid volatile shipping demands. Seamless integration into smartphones, vehicles, and wearables strengthens market leadership, ensuring continued dominance as a key enabler of location-based services across various industries.

5G-enabled LBS is anticipated to be the fastest-growing segment from 2026 to 2033, fueled by the rollout of 5G networks and the significant improvements in connectivity they bring. Ultra-low latency, faster download speeds, and more reliable connections offered by 5G will enable enhanced real-time tracking, smarter location-based advertising, and more accurate location services. In September 2025, for instance, Airtel Business partnered with Swift Navigation to launch Airtel-Skylark, an AI/ML-powered cloud-based location service delivering centimeter-level accuracy for enhancing emergency responses, industrial operations, autonomous mobility, and satellite tolling, starting in India's National Capital Region (NCR). As industries such as automotive, transportation, and smart cities increasingly adopt 5G, demand for advanced location-based services is expected to grow rapidly.

Application Insights

Navigation and tracking services are anticipated to secure around 40% of the market share in 2026, reflecting their dominance in both personal and business applications. This segment’s leadership is driven by the increasing demand for efficient route planning, fleet management, and real-time location tracking. GPS navigation systems, logistics, and ride-hailing services such as Uber and Lyft rely heavily on accurate location data. The ability to streamline operations and improve user experiences makes navigation and tracking a crucial component across various industries.

The geo-marketing & advertising segment is expected to be the fastest-growing during the 2026–2033 forecast period, propelled by the increasing reliance on location-based data for targeted advertising and personalized promotions. The rise of data analytics platforms has enabled businesses to craft highly effective marketing strategies, boosting consumer engagement and conversion rates. In November 2025, for instance, Prime Video introduced location-based interactive video ads in the U.S., enabling national advertisers to customize TV commercials with local details such as pricing, dealerships, or agents via Amazon DSP templates, creating thousands of ZIP code-specific variants without extra assets. As the demand for more precise and tailored marketing solutions continues to grow, this segment is projected to expand rapidly, driven by companies seeking to leverage location data for competitive advantage.

End-User Insights

The transportation & logistics sector is poised to dominate with a forecasted of 30% of the location-based services market revenue share in 2026, powered by the growing demand for real-time tracking, route optimization, and fleet management. Location-based services have become integral in improving operational efficiency, ensuring accurate deliveries, and reducing fuel consumption. By enabling better resource management, optimizing routes, and tracking shipments in real time, LBS help companies in the transportation and logistics industry streamline operations and enhance customer satisfaction, solidifying this sector as the largest consumer of location-based services.

The healthcare sector is estimated to be the fastest-growing segment from 2026 to 2033, fueled by the increasing adoption of location-based services for patient tracking, managing emergency services, and improving medication safety. The rise of telemedicine, health monitoring technologies, and the need for real-time tracking of medical assets and personnel are accelerating the integration of LBS into healthcare systems. With the demand for efficient, real-time health services skyrocketing, location-based services are expected to play a pivotal role in transforming healthcare delivery on a global scale.

Regional Insights

North America Location-Based Services (LBS) Market Trends

North America has been forecasted to command a 40% of the location-based services market share in 2026, fueled by its sophisticated technological foundation and broad integration across sectors such as transportation, retail, logistics, and healthcare. Organizations have been capitalizing on robust mobile and internet penetration to embed LBS seamlessly, while high rates of GPS-equipped smartphones have been amplifying demand for precise, real-time applications. Enterprises are being urged to assess their LBS readiness by mapping current device ecosystems against emerging use cases, ensuring they harness this regional strength for competitive differentiation.

Sustained funding in smart city initiatives and IoT networks has been reinforcing North America's lead, with urban centers such as New York, San Francisco, and Toronto deploying location-based services for optimized traffic flow, enhanced safety measures, and strategic planning. Supportive regulations have been balancing innovation with data safeguards, fostering trust that accelerates adoption among businesses and consumers alike. Consultants advise leaders to prioritize partnerships with local tech hubs, aligning investments with privacy-compliant architectures to sustain momentum and unlock scalable value in this dynamic landscape.

Europe Location-Based Services (LBS) Market Trends

Europe is positioned to maintain a substantial foothold in the location-based services LBS market through 2033, bolstered by technological progress, robust infrastructure, and extensive digital uptake across sectors such as transportation, retail, healthcare, and logistics. Enterprises have been utilizing real-time positioning data to refine fleet operations, streamline routing, and execute precise advertising campaigns, yielding measurable gains in productivity and consumer engagement. Leaders are encouraged to evaluate their LBS maturity by pinpointing high-impact applications within their operations, transforming location intelligence into a core competitive asset.

High smartphone usage, pervasive IoT deployments across diverse sectors, and committed funding for smart urban developments have been propelling this growth, particularly in nations such as the United Kingdom, Germany, and France. Municipalities have been incorporating LBS to enhance traffic coordination, bolster community security, and accelerate parcel distribution, fostering resilient city frameworks. The GDPR has also been shaping the development of trustworthy solutions that prioritize consent and encryption, which guides organizations toward compliant innovations that build enduring confidence among users.

Asia Pacific Location-Based Services (LBS) Market Trends

Asia Pacific is forecasted to be the fastest-growing regional market for location-based services between 2026 and 2033, stimulated by rapid urbanization, increasing smartphone adoption, and substantial investments in digital infrastructure. The large, tech-savvy consumer base in countries such as China and India is driving demand for location-based data. The expanding middle class and growth in sectors like e-commerce, ride-hailing, and logistics further fuel this trend, as businesses seek to optimize operations and enhance customer experiences through real-time location tracking and analytics.

Growth of the Asia Pacific LBS market is further driven by significant government support for smart city development and the integration of IoT technologies into urban planning. Countries are increasingly deploying location-based services to improve traffic flow, manage public safety, and streamline logistics operations. The rise of location-based advertising also plays a crucial role, as businesses leverage real-time consumer data to create targeted campaigns. Technological advancements and improved connectivity, combined with the rapidly evolving digital landscape, are enabling businesses to adopt LBS solutions at an accelerated pace, driving continued market expansion.

Competitive Landscape

The global location-based services market landscape is moderately consolidated, with the top players accounting for a significant portion of global market share. Tech giants such as Google and Apple dominate through their integrated platforms, offering LBS solutions across mobile apps, navigation, and advertising. These companies leverage their extensive technological resources, data analytics capabilities, and global reach to maintain market leadership. Their continuous investment in R&D, expansion of service offerings, and strategic partnerships help them strengthen their position in both mature and emerging markets.

Specialized companies such as HERE Technologies and TomTom complement the market by focusing on niche areas like mapping, fleet management, and real-time navigation. These companies prioritize innovation in mapping technology, route optimization, and customized solutions for specific industries. Smaller players focus on regional market penetration, targeting underserved areas by offering cost-effective and localized services. Through partnerships with local businesses and government initiatives, these companies contribute to the market's growth and drive further adoption of location-based services in diverse sectors.

Key Industry Developments

- In December 2025, LinkGraph rolled out a groundbreaking geographic search engine optimization (GEO) methodology to boost local SEO performance by optimizing content, entities, and signals for enhanced visibility in search results.

- In December 2025, Google activated its Emergency Location Service for Android phones in India, enhancing emergency response times by providing real-time location data to responders.

- In June 2025, GPS Air expanded its smartIAQ technology, transforming clean air solutions into a capital-saving strategy for businesses by integrating advanced air quality monitoring with cost-efficiency tools.

Companies Covered in Location-Based Services (LBS) Market

- Apple

- HERE Technologies

- TomTom

- Qualcomm

- Foursquare

- Uber Technologies

- Garmin

- Sygic

- Telenav

Frequently Asked Questions

The global location-based services market is projected to reach US$ 44.2 billion in 2026.

The market is driven by technological advancements in GPS, mobile connectivity, and the increasing demand for real-time location-based applications across various industries.

The market is poised to witness a CAGR of 19.1% from 2026 to 2033.

Key market opportunities include integration of LBS technologies with smart city development projects and autonomous vehicles and the growth of geo-marketing and location-based advertising.

Key players in the market include Google, Apple, HERE Technologies, TomTom, Qualcomm, and Foursquare.