ID: PMRREP32359| 289 Pages | 5 Jan 2026 | Format: PDF, Excel, PPT* | Semiconductor Electronics

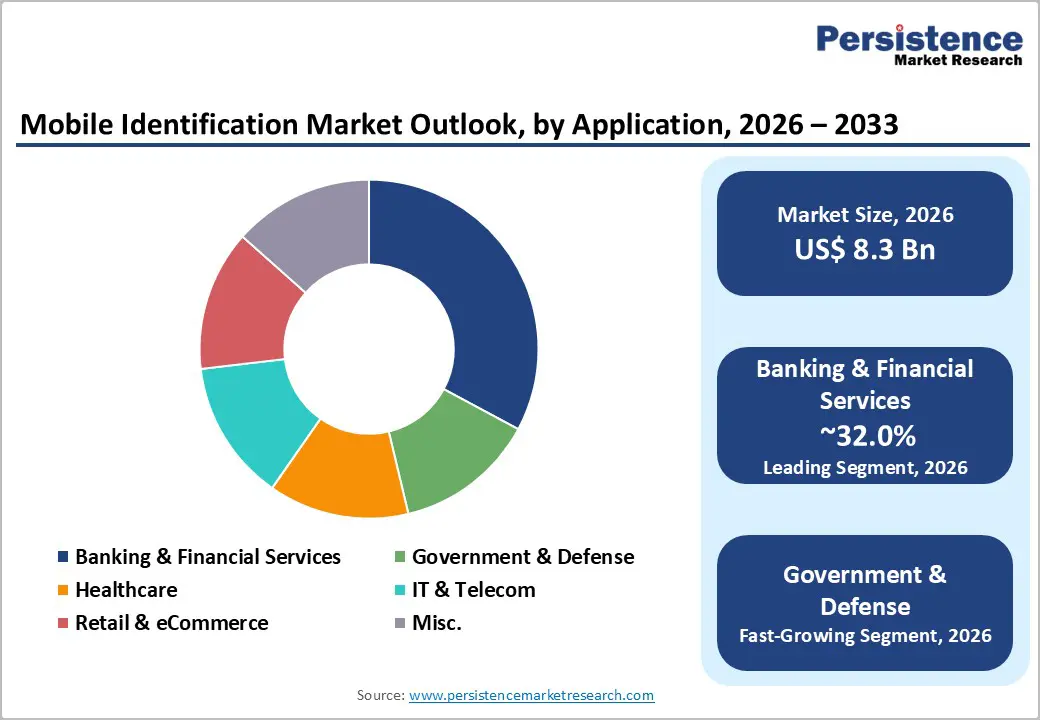

The Global Mobile Identification Market size was valued at US$8.3 billion in 2026 and is projected to reach US$ 22.5 Billion by 2033, growing at a CAGR of 15.3% between 2026 and 2033. This accelerating growth trajectory reflects fundamental shifts in digital authentication paradigms driven by escalating cybersecurity threats, regulatory mandates, and government initiatives aimed at achieving digital identity for all citizens.

The market's expansion demonstrates how mobile identification has transitioned from a convenience feature to a critical infrastructure component supporting financial inclusion, public security, and digital service delivery across government, banking, healthcare, and enterprise sectors globally.

| Key Insights | Details |

|---|---|

|

Mobile Identification Market Size (2026E) |

US$ 8.3 Bn |

|

Market Value Forecast (2033F) |

US$ 22.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

15.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

12.5% |

Growth Drivers

International standardization bodies and national governments are establishing binding regulatory frameworks that mandate digital identification capabilities across public and private sectors, thereby structuring demand within the Mobile Identification Market.

The National Institute of Standards and Technology (NIST) released its updated SP 800-63-4 guidelines in July 2025, establishing the first comprehensive risk-based Digital Risk Management (DIRM) framework that specifically incorporates mobile driver's licenses and phishing-resistant multi-factor authentication as foundational methods for identity proofing. This regulatory evolution removes technical ambiguity and accelerates organisational investment decisions. Internationally, the ISO/IEC 18013-5 standard for mobile driver's licenses, published in September 2021, has achieved global adoption as the interoperable technical baseline for secure mobile identification across jurisdictions. The Mobile Identification Market benefits from this standardisation because it enables verifier systems to accept credentials across borders without proprietary integration.

UN Sustainable Development Goal Target 16.9 mandates legal identity for all by 2030, with an estimated 850 million persons globally lacking any official identity documentation. This supranational commitment has catalysed government-led initiatives, India's Aadhaar biometric identification system, Singapore's SingPass digital identity framework, and Australia's myGovID platform, which demonstrate how regulatory imperative drives Mobile Identification Market deployment at population scale. The convergence of NIST standards, ISO interoperability requirements, and SDG 16 commitments creates a policy environment where mobile identification adoption becomes institutionally mandatory rather than discretionary.

The Technical Foundation for Mobile Identification Market expansion rests on unprecedented global connectivity and device proliferation that enables service delivery at scale. Global internet usage reached approximately 6 billion users by 2025, representing 74% of the world's population, with mobile internet overwhelmingly dominant in China. 1.105 billion mobile internet users account for 99.7% of netizens, demonstrating the central role of mobile access to digital services. This infrastructure foundation enables the Mobile Identification Market to function as a genuine mass-market capability rather than a niche government program. India's telecom sector exemplifies this opportunity scale: the country recorded 1.21 billion subscribers and 86.09% tele-density as of June 2025, with 979 million internet subscribers highlighting the addressable population for mobile identification services.

Mobile banking adoption validates consumer readiness to conduct secure transactions through mobile devices. Globally, 61% of people use mobile phones for banking activities, with 48% employing dedicated banking applications. In developed markets, 76% of American adults use mobile banking.

The Digital Identification Market's expansion leverages this existing behavioral infrastructure, positioning mobile identification as a natural evolution of consumer authentication preferences. This driver's impact extends beyond individual nations; digital identity verification checks reached 86 billion in 2025, up from 75 billion in 2024, indicating 15% year-on-year growth in the actual usage volume of digital identity systems globally.

Market Restraining Factors

Deployment of the Mobile Identification Market infrastructure requires substantial capital investment in backend authentication systems, biometric enrollment processes, and device compatibility management, creating barriers particularly for small organisations and developing economies. Initial installation costs for enterprise-grade mobile identification systems involve significant expenses for hardware procurement (biometric sensors, secure elements), software licensing, integration with legacy systems, and staff training. Small and medium enterprises frequently lack dedicated cybersecurity budgets to justify these expenditures, limiting market penetration in segments below enterprise scale.

Network connectivity gaps in rural areas of developing markets further constrain Mobile Identification Market adoption, while urban internet penetration approaches universal levels, rural connectivity remains inconsistent, preventing seamless credential verification in geographically dispersed populations. Device compatibility presents a technical challenge despite iOS and Android dominance; older device models lack the necessary biometric hardware or sufficient processing capability for secure credential storage, fragmenting the addressable user base. These cost barriers and technical constraints encourage organizations to defer Mobile Identification Market adoption or pursue alternative, lower-cost verification methods, hampering revenue growth and creating geographic disparities in service availability.

Key Market Opportunities

The Mobile Identification Market addresses critical barriers to financial and social inclusion by enabling individuals lacking traditional identity documentation to participate in digital banking, government services, and commerce through mobile-first verification. Approximately 1.3 billion people came online between 2020 and 2025, but 2.2 billion remain offline, representing an addressable population where the Mobile Identification Market could unlock access to essential services. In developing economies, physical identity documents are frequently unavailable, expensive, or vulnerable to loss. Mobile identification eliminates these barriers by storing secure credentials in devices already in use for daily communication.

The Mobile Identification Market's impact on financial inclusion has been documented across multiple contexts. Kenya's mobile money services, underpinned by digital identity verification tied to mobile SIM registration, have enabled over 50% of the previously unbanked adult population to access financial services. In Nigeria, the implementation of digital ID systems for civil servants enabled the identification and removal of approximately 60,000 ghost workers, recovering government resources for legitimate service delivery. Peru achieved near-universal identity through coordinated digital programs and generated US$45 million in annual government revenue through improved tax collection and reduced benefit fraud.

The Market's technical capability to conduct remote verification over internet connections expands access beyond urban centres where government enrollment facilities concentrate, directly supporting UN SDG 16.9 commitments. Projects in Kenya and Nigeria conducted by the UK Foreign Commonwealth and Development Office demonstrated Mobile Identification Market applications in healthcare access, enabling secure medical record management and small business financing, allowing individuals to establish business credentials, illustrating how mobile identification serves as foundational infrastructure for broader socioeconomic participation.

The Mobile Identification Market presents substantial operational and revenue opportunities within banking, healthcare, and government sectors where regulatory frameworks mandate Know-Your-Customer (KYC), Anti-Money Laundering (AML), and identity verification processes. Banking and Financial Services held 32.0% of the Mobile Identification Market in 2026, but this segment remains underexploited relative to regulatory compliance requirements. Digital identity verification checks are forecast to reach 86 billion in 2025, indicating continuous demand for verification services driven by regulatory mandates rather than discretionary adoption.

The Market's capacity to automate compliance workflows reduces operational costs while improving audit trails and regulatory transparency. Implementation evidence from financial institutions demonstrates this value: organisations deploying advanced identity and access management frameworks report 79.8% lower fraud losses, 84.5% reduced authentication-related customer complaints, and 72.3% fewer abandonment rates compared to legacy verification approaches.

Healthcare organizations face similar compliance imperatives. 63% of healthcare organizations identify identity and access management (IAM) as a critical security priority, driven by regulatory requirements like HIPAA that mandate verification of workforce credentials and patient identity before access to sensitive health information.

The Market enables healthcare providers to implement federated identity frameworks that grant patients access to electronic health records across institutional boundaries through single sign-on authentication, directly improving care coordination while reducing duplicate testing and prescribing errors. Retail and e-commerce sectors, though currently smaller market segments, face escalating regulatory requirements for identity verification tied to anti-fraud and consumer protection mandates. The Mobile Identification Market's fraud prevention capabilities directly address this requirement gap. These regulatory compliance drivers create durable market demand across sectors, supporting sustained growth independent of discretionary spending decisions.

Authentication Type Insights

Multi-Factor Authentication dominates the Mobile Identification Market with 72.0% market share in 2026, representing the established, institutionally-preferred authentication approach. MFA combines multiple verification factors (passwords/PINs), possession (devices), and inherence (biometrics) to establish identity with high assurance.

The leading position reflects regulatory requirements that increasingly mandate MFA across financial services, government, and healthcare sectors. NIST SP 800-63-4 guidelines explicitly require phishing-resistant MFA for high-assurance authentication, and financial services regulations like PSD2 Revised Payment Services Directive in Europe, mandate strong customer authentication using MFA for digital payment transactions. This regulatory mandate translates to institutional adoption, 73% of security leaders globally prioritise scalable and intelligent mobile identification solutions, with MFA representing the institutional default. Biometric authentication serves as the primary MFA modality within the Mobile Identification Market as 671 million people were conducting biometric-enabled payments in 2020, with projections reaching 1.4 billion by 2025, validating consumer acceptance and commercial deployment on a scale.

The dominance of MFA within the Market reflects institutional preference for layered security over single-factor approaches, as MFA demonstrably reduces fraud rates while maintaining acceptable user experience friction.

Single-Factor Authentication represents the fastest-growing segment within the Mobile Identification Market, despite holding the smaller market share, reflecting specific use cases where biometric or device-based verification provides sufficient assurance without knowledge-based factors.

Application Insights

Banking and Financial Services held 32.0% of the Mobile Identification Market in 2026, establishing clear institutional dominance driven by regulatory compliance requirements and fraud prevention imperatives. The financial services sector's leading position reflects both mandatory authentication regulations and competitive pressure to provide seamless digital customer experiences. PSD2 (Revised Payment Services Directive) in Europe and similar regulations globally mandate strong customer authentication (SCA) using MFA for electronic payment transactions, creating institutional demand for mobile identification infrastructure.

The BFSI sector's particular vulnerability to identity fraud justifies this leading market position: over 80% of organizations experienced payment fraud attacks, with estimated merchant losses reaching US$362 billion cumulatively between 2023 and 2027. This fraud environment creates economic justification for comprehensive mobile identification deployment. Organisations implementing advanced identity and access management frameworks realize 79.8% reduction in fraud losses.

Consumer banking behaviour validates the sector's technological readiness, with around 61% of people globally using mobile banking, with 4.2 billion mobile banking users by 2026 and projections of 2 billion additional users by 2030. This established consumer base, combined with regulatory requirements and fraud risk, positions Banking and Financial Services as the Mobile Identification Market's anchor segment.

Government and Defense represents the fastest-growing segment of the Mobile Identification Market, reflecting government investment in citizen service modernisation and security infrastructure. This segment's rapid expansion is driven by policy-level commitments: 19 U.S. states implemented mDL programs by October 2025, with all remaining states expected to follow based on AAMVA adoption curves.

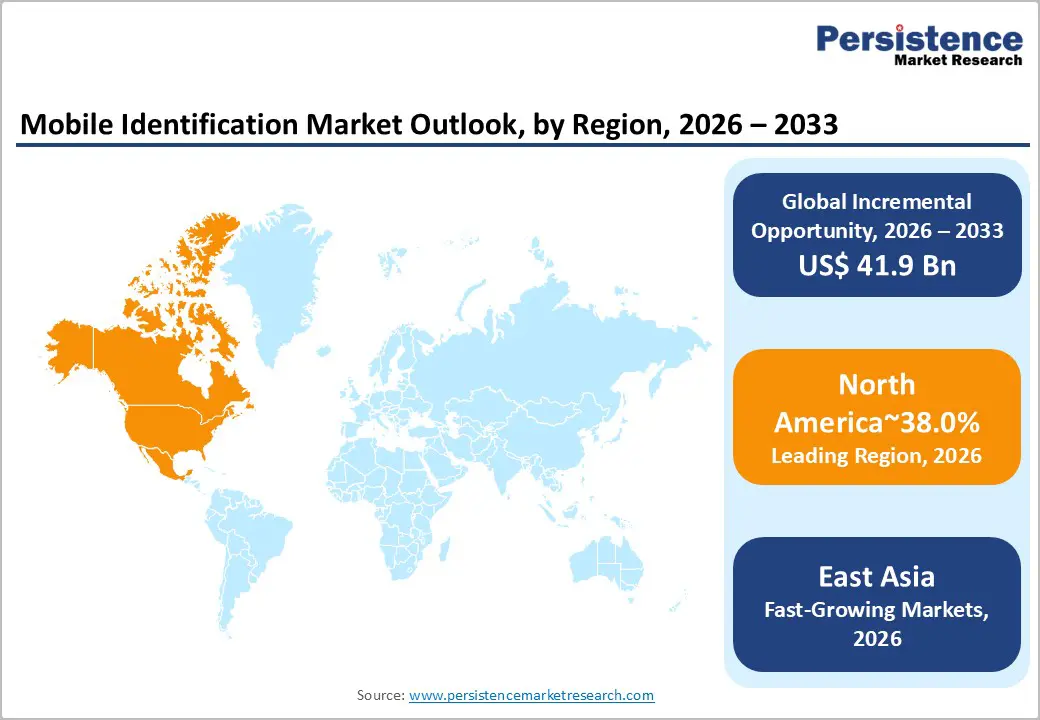

North America Market Trend

North America commands 38% of the Global Mobile Identification Market, positioning the region as the leading market by absolute revenue. The United States and Canada together generate the greatest aggregate demand for mobile identification solutions through a combination of regulatory mandates, advanced technology adoption, and institutional investment capacity.

The American Association of Motor Vehicle Administrators (AAMVA) has orchestrated coordinated mDL deployment across 19 U.S. states as of October 2025, with additional states implementing programs through 2026-2027. This institutional coordination creates multi-year revenue visibility for platform providers supporting mDL issuance, verification, and back-office infrastructure. NIST SP 800-63-4 guidelines, finalised in July 2025, establish the technical baseline for federal and private sector identity systems across North America, creating standardisation that accelerates adoption and reduces fragmentation. The North American regulatory environment includes HIPAA (healthcare), GLBA (financial services), and state-specific privacy laws like CCPA (California) that mandate strong authentication and identity verification, creating institutional compliance-driven demand.

East Asia Market Trend

East Asia represents the region with the fastest growth trajectory despite holding 18% market share, driven by exponential mobile device penetration, government digital transformation initiatives, and expansion of digital financial services. China's digital ecosystem exemplifies East Asia's opportunity: 1.108 billion internet users with 99.7% mobile internet access as of December 2024, with mobile internet penetration reaching 78.6%. This infrastructure foundation enables mass-scale mobile identification deployment. Chinese national identity programs increasingly incorporate mobile authentication capabilities, while private sector platforms like Alipay and WeChat Pay have embedded biometric identification into payment ecosystems serving hundreds of millions of users. The Market's application within China's e-government services, where citizens access government licensing, registration, and administrative functions through mobile channels, creates sustained institutional demand.

Southeast Asian nations like Singapore and Thailand implement government-led digital identity programs (SingPass, Thailand Digital ID) that create regional standards and demonstrate government commitment to mobile identification infrastructure investment. Japan's advanced mobile ecosystem and regulatory frameworks supporting digital authentication, particularly in payment and healthcare domains, support significant Mobile Identification Market deployment.

The fastest-growth trajectory in East Asia reflects convergence of massive addressable populations, government digital transformation investment, and private sector competition in digital financial services that collectively drive Mobile Identification Market adoption rates exceeding North American and European growth rates.

Europe Market Trend

Europe holds 22% of the Global Mobile Identification Market and is characterised by stringent privacy regulations, coordinated digital identity frameworks, and government-led modernisation initiatives. The European Union's eIDAS Regulation such as electronic Identification, Authentication and Trust Services) and proposed eIDAS 2.0 create binding requirements for digital authentication and identity verification standards across EU member states. This regulatory framework drives institutional Mobile Identification Market adoption by establishing interoperability requirements that platform providers must meet.

The European banking sector's regulatory environment strongly drives Mobile Identification Market adoption. PSD2 (Revised Payment Services Directive) mandates strong customer authentication (SCA) using MFA for digital payment transactions across EU member states, creating an explicit regulatory requirement for mobile identification solutions supporting payment authentication. The European financial services sector, with total assets of €43.6 trillion in 2023 and 26.8 trillion in outstanding loans, demonstrates substantial institutional capital availability and investment capacity supporting Mobile Identification Market deployment. The region's GDPR-driven data protection requirements create premium demand for privacy-respecting mobile identification solutions that minimise data collection and implement selective data-sharing mechanisms.

The Global Mobile Identification Market is moderately consolidated, dominated by key players such as Thales Group, IDEMIA, HID Global, Samsung SDS, Entrust, and NEC Corporation. These companies lead through advanced biometric authentication, secure mobile ID solutions, and large-scale government and enterprise deployments. Mid-tier players like Okta, ForgeRock, and Veridos are gaining traction with cloud-based and AI-driven identity solutions. Technology giants such as Apple, Google, and Microsoft influence the market through platform integrations and APIs. Competition is driven by strategic partnerships, acquisitions, and continuous innovation to meet security, privacy, and regulatory demands, while smaller innovators push new use cases, keeping the market dynamic.

Key Industry Developments

The global Mobile Identification Market is projected to be valued at US$ 8.3 Bn in 2026.

The Banking & Financial Services Segment is expected to account for approximately 32% of the global Mobile Identification Market by Application in 2026.

The market is expected to witness a CAGR of 22.5% from 2026 to 2033.

The Mobile Identification Market is driven by regulatory harmonisation and government digital ID mandates, global standardisation (ISO/IEC 18013-5, NIST DIRM), and rapid growth in internet connectivity and mobile device adoption, enabling secure, large-scale digital identity verification.

The Mobile Identification Market offers key opportunities in enabling financial inclusion, expanding digital service access for underserved populations, and supporting regulatory compliance and fraud prevention across banking, healthcare, and government sectors.

The key players in the Mobile Identification Market include OneLogin (One Identity LLC), Thales Group, SecureAuth Corporation, IBM Corporation, and Micro Focus.

| Report Attribute | Details |

|---|---|

|

Forecast Period |

2026 to 2033 |

|

Historical Data Available for |

2020 to 2025 |

|

Market Analysis |

USD Million for Value |

|

Region Covered |

|

|

Key Companies Covered |

|

|

Report Coverage |

|

By Authentication Type

By Component / Solution

By Deployment Mode

By Application

By Region

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author