- Healthcare Services

- Radiology Microcatheters Market

Radiology Microcatheters Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Radiology Microcatheters Market by Catheter Type (Diagnostic Microcatheters, Delivery Microcatheters, Steerable Microcatheters, Aspiration Microcatheters), Application (Hospitals, Ambulatory Surgical Centers, Clinics, Diagnostic Centers), and Regional Analysis for 2025 - 2032

Radiology Microcatheters Market Size and Trends Analysis

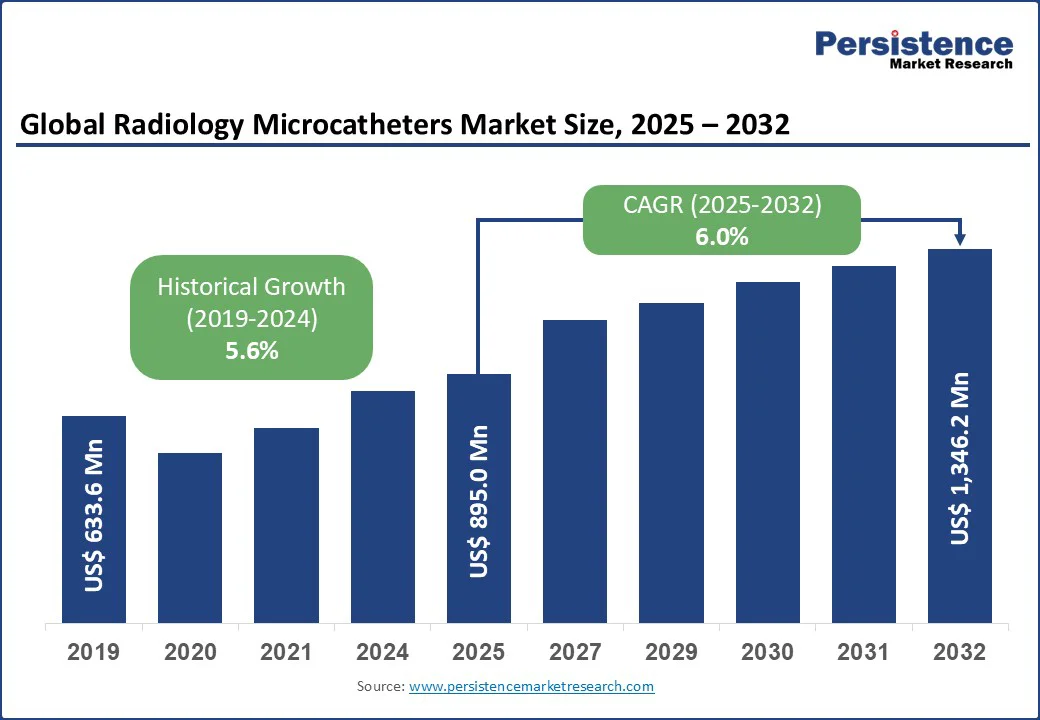

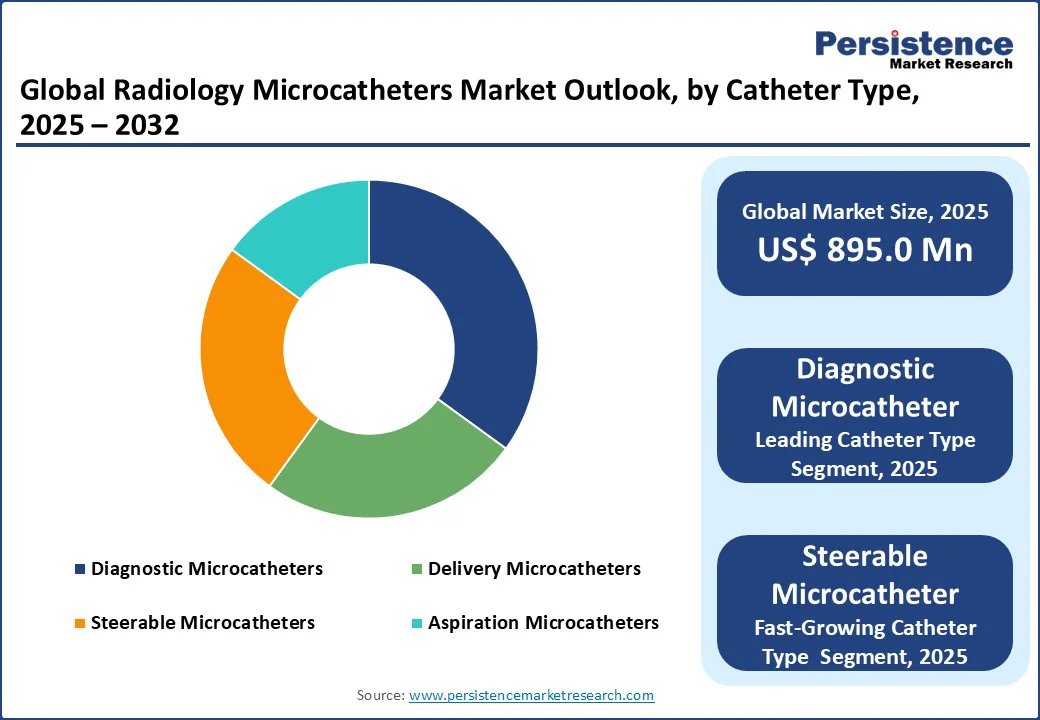

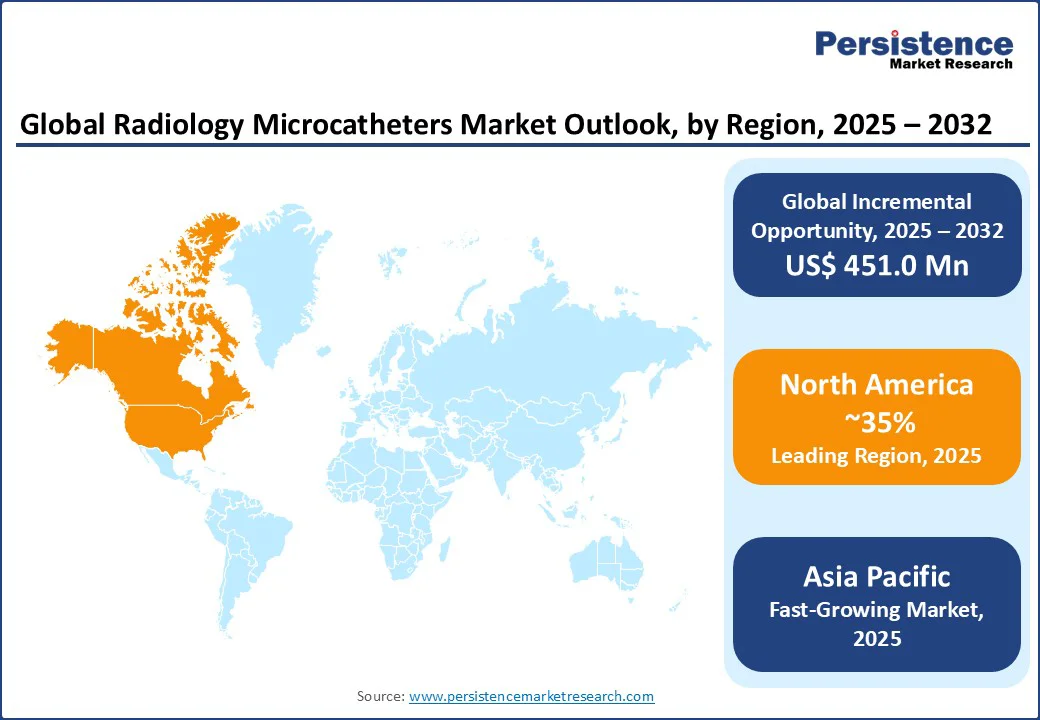

The global radiology microcatheters market size is expected to be valued at US$895.0 Mn in 2025, with a forecast to reach US$1,346.2 Mn by 2032, growing at a CAGR of 6.0% during the forecast period of 2025 - 2032.

The radiology microcatheters industry is witnessing robust growth, driven by the rising prevalence of chronic diseases, increasing demand for minimally invasive procedures, and advancements in interventional radiology techniques. These devices play a critical role in diagnostic and therapeutic imaging, including angiography, embolization, and neurovascular interventions. Microcatheters are increasingly paired with advanced imaging modalities for precise positioning during complex interventions.

Key Industry Highlights

- Leading Microcatheter Type: Diagnostic Microcatheters Are Expected to hold a 32% market share in 2025, driven primarily by diagnostic catheters.

- Fast-growing Microcatheter Type: Steerable Microcatheters are fueled by advanced interventional radiology tools.

- Leading Application: Hospitals account for 45% market share, supported by catheter-based interventions.

- Fastest-Growth: Ambulatory Surgical Centers grow at a CAGR of 6.3%, driven by minimally invasive radiology tools.

- Dominant Region: North America holds a 35% market share, with the U.S. leading in interventional radiology.

- Fast-growing Region: Asia Pacific commands the share of 20%, driven by neurovascular treatment devices.

- Chronic Disease Impact: 15% growth in radiology microcatheters for tumor embolization.

| Global Market Attribute | Key Insights |

| Radiology Microcatheters Market Size (2025E) | US$895.0 Mn |

| Market Value Forecast (2032F) | US$ 1,346.2 Mn |

| Projected Growth (CAGR 2025 to 2032) | 6.0% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.6% |

Market Dynamics

Drivers: Rising Prevalence of Chronic Diseases and Advancements in Minimally Invasive Procedures

The rising prevalence of chronic diseases, including cardiovascular disorders, cancer, and neurological conditions, is a significant driving factor for the radiology microcatheters market. These conditions often require precise diagnostic and interventional procedures, where microcatheters play a critical role in navigating complex vascular pathways.

Additionally, the growing demand for minimally invasive procedures has further accelerated market growth, as these techniques offer benefits such as reduced patient trauma, shorter hospital stays, and faster recovery times compared to traditional surgeries. Technological advancements in microcatheter design, such as improved flexibility, smaller diameters, and enhanced navigation capabilities, have expanded their applications in complex interventions. This combination of increasing disease burden and the shift toward minimally invasive solutions continues to drive the global adoption of microcatheters.

Restraint: High Manufacturing Costs and Stringent Regulatory Approvals

The production of microcatheters requires advanced materials, precision engineering, and sophisticated quality control processes to ensure safety and performance in critical medical procedures. These factors significantly increase manufacturing expenses, making the products costlier for both healthcare providers and patients.

The stringent regulatory requirements imposed by authorities such as the FDA and EMA necessitate rigorous clinical testing, thorough documentation, and adherence to international safety standards. This not only prolongs the product development cycle but also adds substantial costs to the approval process. As a result, new entrants face high barriers to entry, and even established players encounter challenges in bringing innovative products to market quickly, thereby limiting overall market growth.

Opportunity: Growing Adoption of Advanced Imaging Technologies

Innovations such as 3D imaging, real-time fluoroscopy, and MRI-guided interventions enable enhanced visualization of complex and small vessels, which is critical for accurate navigation during minimally invasive procedures. This advancement drives the demand for reilogy microcatheters, as they are essential for precision in neurovascular, cardiovascular, and oncology treatments. The integration of microcatheters with next-generation image-guided systems allows for improved procedural outcomes, making them the preferred choice among healthcare professionals.

As medical imaging continues to evolve, manufacturers can develop advanced, compatible microcatheters, further fueling market growth and expanding applications in targeted drug delivery and embolization procedures. Optical Coherence Tomography (OCT) imaging, with 20% higher resolution than traditional angiography, drives 15% growth in diagnostic catheters. The integration of AI in catheter navigation enhances neurovascular treatment devices by 18%, supporting catheter-based interventions.

Category-wise Analysis

Catheter Type Insights

Diagnostic microcatheters are projected to hold a 32% market share in 2025, driven by the demand for diagnostic catheters and dual-lumen microcatheters for diagnostic imaging purposes. With 35% adoption in angiographic procedures, they support catheter-based interventions. Their small diameter and superior trackability make them ideal for navigating tortuous vessels, which is vital in neurovascular and peripheral vascular imaging. The growing demand for early disease detection, combined with the increasing use of image-guided interventions, continues to fuel the expansion of this segment.

Advanced interventional radiology tools fuel steerable microcatheters. With 12% growth, they enhance neurointerventional catheters and vascular access devices. Steerable designs also support complex embolization, tumor targeting, and chronic total occlusion (CTO) treatments, where high manoeuvrability improves success rates and reduces procedural complications. Furthermore, these devices are increasingly integrated with advanced imaging systems, boosting their application in minimally invasive therapies.

Application Insights

Hospitals are expected to command a 45% market share in 2025, driven by catheter-based interventions. With 50% adoption, they rely on radiology microcatheters and embolization microcatheters. The availability of specialized radiologists, neurosurgeons, and interventional cardiologists ensures higher utilization of these devices. The growing trend toward image-guided therapies and the integration of hybrid operating rooms also strengthens the hospital segment dominance.

Ambulatory Surgical Centers fueled by minimally invasive radiology tools. With 10% growth, they adopt oncology embolization devices and guide catheters. These centers are particularly adopting oncology embolization devices and guide catheters for cancer-related treatments such as transarterial chemoembolization (TACE) and radioembolization, as well as vascular access interventions. The preference for ASCs is growing due to their shorter recovery periods, reduced hospital stays, and improved patient convenience, making them an ideal setting for outpatient interventional radiology.

Regional Insights

North America Radiology Microcatheters Market Trends

North America is expected to hold a 35% global market share in 2025, with the U.S. leading due to its advanced healthcare infrastructure and high adoption of interventional radiology, generating US$358 million in sales in 2025. The U.S. market is poised to achieve a leading CAGR driven by diagnostic catheters, with 70% of hospitals adopting microcatheters for tumor embolization in 2025.

Key drivers include a 20% increase in cardiovascular procedures, which are expected to reach one million annually by 2026, thereby boosting the demand for endovascular microcatheters and vascular access devices. The rise of outpatient procedures increased the use of minimally invasive radiology tools by 25%, supporting the adoption of angiographic microcatheters.

Boston Scientific Corporation holds a 15% regional share, leveraging embolization microcatheters, with 40% of neurovascular procedures using their products. The oncology sector, with 81,400 bladder cancer cases, drives demand for neurointerventional catheters.

Europe Radiology Microcatheters Market Trends

Europe accounts for a 30% global share, led by Germany, the UK, and France, driven by robust healthcare systems and regulatory support for interventional radiology. Germany’s market is growing at a CAGR of 5.9%, driven by advanced microcatheters for angiographic procedures, with 50% of hospitals adopting catheter-based interventions.

The cardiology sector, contributing €1 Tn to the economy, drives 15% growth in embolization microcatheters. The UK market is driven by neurointerventional catheters, with 40% of clinics adopting dual-lumen microcatheters for diagnostic imaging.

Government initiatives, with €300 Mn in medical technology funding, boost minimally invasive radiology tools. France experiences 8% growth in the oncology sector, with a 12% adoption rate of oncology embolization devices for TACE procedures, supported by Medtronic plc’s guide catheters.

Asia Pacific Radiology Microcatheters Market Trends

The Asia Pacific is the fastest-growing region, with a 20% lead driven by China, Japan, and India, primarily due to rapid growth in healthcare infrastructure and the prevalence of chronic diseases. China holds a 40% regional share, fueled by US$10 Bn in healthcare investments, boosting radiology microcatheters and vascular access devices. The cardiology sector, with 14.6 Mn cancer cases projected in 2025, drives 20% growth in oncology embolization devices.

India’s market is driven by a 15% growth in hospitals, with a 30% adoption rate of diagnostic catheters. Government initiatives such as Ayushman Bharat, with US$ 3 Bn in funding, enhance catheter-based intervention. Japan’s market is experiencing 10% growth in neurovascular treatment devices, driven by a 12% increase in the adoption of angiographic microcatheters in clinics. Terumo Corporation expands with embolization microcatheters, capturing 10% of the regional market.

Competitive Landscape

The global radiology microcatheters market is highly competitive, with Terumo Corporation, Medtronic plc, Cook Medical, Boston Scientific Corporation, Merit Medical Systems, Asahi Intecc, Argon Medical Devices, and Kaneka Corporation focusing on interventional radiology, diagnostic catheters, and advanced interventional radiology tools.

Companies leverage radiology microcatheters for tumor embolization and neurointerventional catheters to gain market share. Strategic R&D investments in minimally invasive radiology tools and partnerships drive catheter-based interventions, addressing embolic agents and oncology embolization devices needs.

Key Developments

- In June 2024, MicroVention, Inc., a global neurovascular company, and wholly owned subsidiary of Terumo Corporation, today announced that the LVIS™ EVO™ Intraluminal Support Device is now commercially available in the United States for the treatment of wide neck intracranial aneurysms. LVIS EVO has been available in Europe since 2019, and over 12,000 units have been sold. LVIS EVO is the first fully visible coil-assist-intracranial stent available in the US Market.

- In April 2022, Boston Scientific Corporation (NYSE: BSX) has received U.S. Food and Drug Administration (FDA) 510(k) clearance for the EMBOLD™ Fibered Detachable Coil, which is indicated to obstruct or reduce the rate of blood flow in the peripheral vasculature. The first procedure using the device was performed this week at the University of Alabama at Birmingham.

Companies Covered in Radiology Microcatheters Market

- Terumo Corporation

- Medtronic plc

- Cook Medical

- Boston Scientific Corporation

- Merit Medical Systems

- Asahi Intecc

- Argon Medical Devices

- Kaneka Corporation

- Others

Frequently Asked Questions

The radiology microcatheters market is projected to reach US$ 895.0 Mn in 2025, driven by microcatheters and catheter-based interventions.

Rising chronic disease prevalence and 20% adoption of minimally invasive radiology tools in 2025 fuel demand for diagnostic catheters and embolization microcatheters.

The radiology microcatheters market grows at a CAGR of 6.0% from 2025 to 2032, reaching US$ 1,346.2 Mn by 2032.

Advanced imaging technologies, with 15% growth in diagnostic catheters, offer opportunities for neurointerventional catheters and oncology embolization devices.

Key players include Terumo Corporation, Medtronic plc, Cook Medical, Boston Scientific Corporation, and Merit Medical Systems.