- Specialty & Fine Chemicals

- Metal Cleaners Market

Metal Cleaners Market Size, Share, and Growth Forecast 2025 - 2032

Metal Cleaners Market by Product Type (Aqueous Cleaners, and Solvent-based Cleaners), by Metal Substrate (Ferrous Metals, and Non-Ferrous Metals), Cleaning Chemistry (Surfactant-based Cleaners, Chelating-agent Cleaners, Corrosion Inhibitor Cleaners, Emulsion Cleaners, and Biodegradable / Enzyme-based Cleaners), Cleaning Method, Industry, and by Regional Analysis, 2025 - 2032

Metal Cleaners Market Size and Trend Analysis

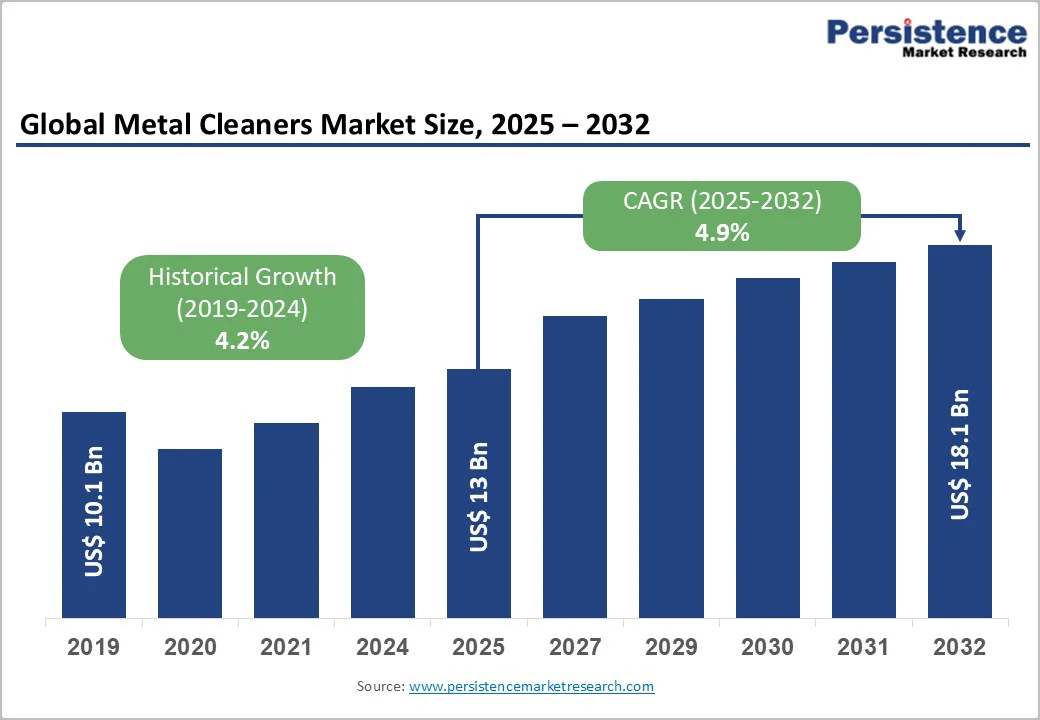

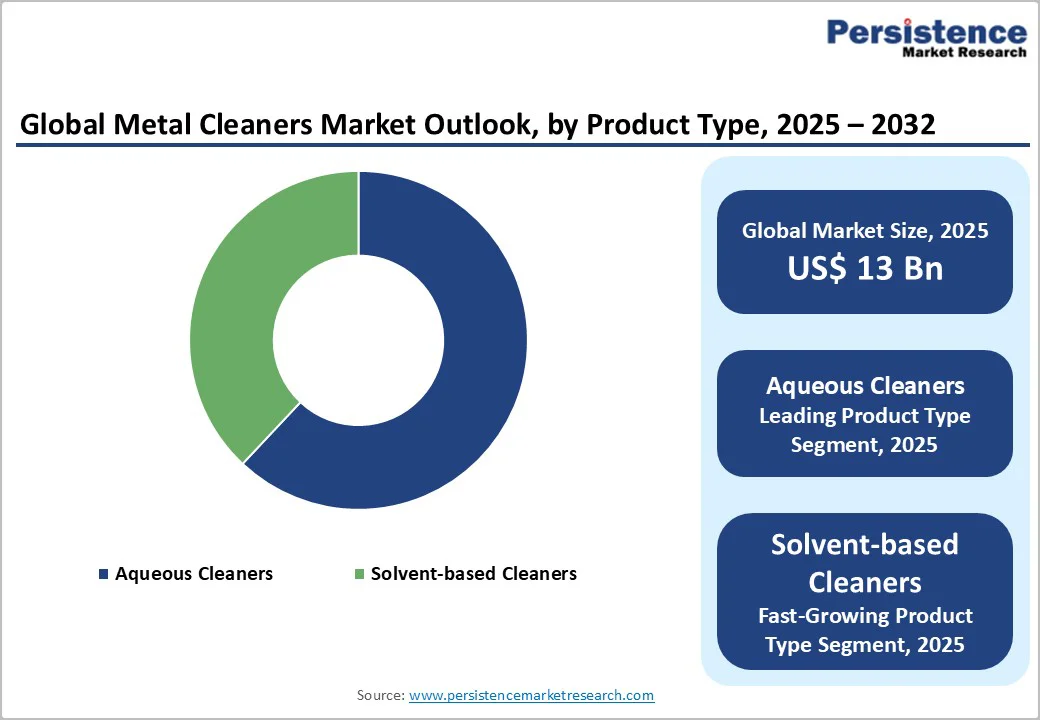

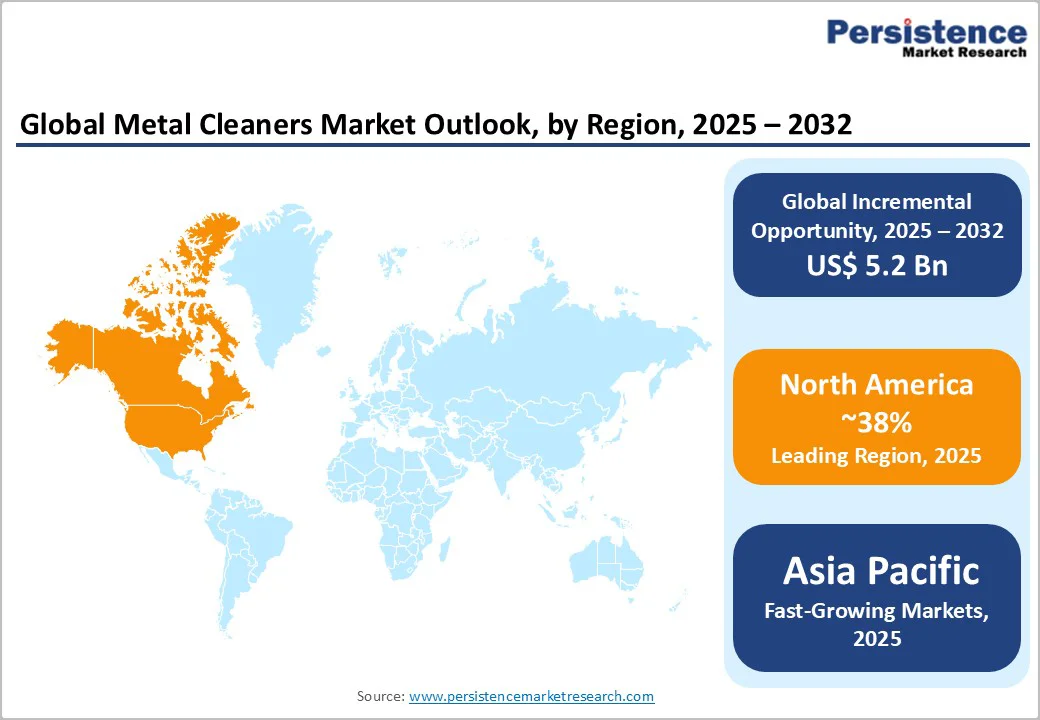

The global metal cleaners market size is valued at US$ 13.0 billion in 2025 and is projected to reach US$ 18.2 billion, growing at a CAGR of 4.9% between 2025 and 2032. Industrial activities and stringent cleanliness standards in manufacturing sectors fuel the need for the metal cleaners market. Key drivers include the growth in the automotive and aerospace industries, which demand high-precision cleaning to ensure component durability and performance.

Key Market Highlights:

- Leading Region: North America dominates the global metal cleaners market with 38% share, driven by stringent U.S. regulations and advanced manufacturing in automotive and aerospace sectors.

- Fastest-Growing Region: Asia Pacific emerges as the fastest-growing region with a rising CAGR of 5.1%, fueled by industrialization in China and India, boosting demand for efficient cleaning solutions.

- Leading Segment: Aqueous cleaners lead product types with a significant share of 62%, offering eco-friendly removal of contaminants with broad compatibility across metals and industries.

- Fastest-Growing Segment: Solvents represent the fastest-growing segment with a rising CAGR of 6.3%, propelled by sustainability mandates reducing reliance on traditional hydrocarbons.

- Key Opportunity: Bio-based cleaners offer key opportunities, enabling compliance with environmental policies while enhancing performance in emerging markets.

| Key Insights | Details |

|---|---|

|

Global Metal Cleaners Market Size (2025E) |

US$ 13.0 Billion |

|

Market Value Forecast (2032F) |

US$ 18.2 Billion |

|

Projected Growth CAGR (2025-2032) |

4.9% |

|

Historical Market Growth (2019-2024) |

4.2% |

Market Dynamics

Drivers - Growing Production in Automotive and Aerospace Industries is Boosting the Need for High-Performance Metal Cleaning Solutions

The automotive and aerospace industries continue to significantly drive the growth of the metal cleaners market, mainly due to their strict surface preparation requirements for high-quality production. Automakers rely on metal cleaners to remove oils, greases, and machining residues from components such as engines, brake systems, and chassis parts to meet global quality standards like ISO guidelines.

The aerospace sector requires highly precise cleaning solutions to protect sensitive alloys used in aircraft manufacturing. With air cargo and passenger traffic increasing in recent years, production activity has intensified, further boosting the demand for metal cleaners. Manufacturers are also shifting toward lightweight composite materials, which demand specialized, non-corrosive cleaning formulations. This growing need for efficiency, safety, and durability during production processes is steadily increasing the consumption of advanced metal cleaners across both industries.

Eco-Friendly and Low-VOC Cleaning Technologies are Accelerating Market Growth through Safer and Greener Industrial Operations

Rapid innovation in eco-friendly, bio-based, and water-based cleaning solutions is transforming the metal cleaners market, making sustainability a major growth driver. Industries are increasingly adopting formulations with low VOC emissions, in line with global environmental regulations that encourage greener manufacturing practices. These advanced cleaners help reduce pollution, improve workplace safety, and support compliance with environmental bodies without compromising performance.

Manufacturers benefit from lower operational costs because sustainable cleaners generate less hazardous waste, reducing disposal fees and long-term liabilities. These modern formulations offer better corrosion resistance and lower residue buildup, helping extend the life of machinery and components. As more industries shift toward sustainable operations and corporate ESG commitments rise, demand for environment-friendly metal cleaners continues to grow, encouraging companies to invest in innovative green technologies.

Restraints - Tough Global Environmental Regulations on Solvent-Based Cleaners are Restricting Market Growth and Increasing Compliance Costs

Environmental regulations imposed on solvent-based metal cleaners present a major challenge for market expansion. Governments in regions like the U.S. and Europe have enforced strict VOC limits and hazardous chemical restrictions, making it difficult for manufacturers to continue using traditional solvent formulations. Many commonly used chlorinated solvents are now classified as high-risk substances, leading to reduced availability and mandatory reformulations.

Compliance requires facilities to upgrade equipment, adopt safer chemicals, and invest in monitoring systems, increasing operational costs, especially for small and mid-sized manufacturers. These restrictions also slow down product approvals and create supply chain disruptions, limiting the options for end users. In developing markets, the transition is slower due to cost barriers, creating a gap between regulatory expectations and industrial readiness, which further impacts market growth.

Complex and Costly Waste Management Requirements for used Cleaning Chemicals are Limiting Widespread Adoption

Waste management remains a significant restraint for the metal cleaners market because used cleaning solutions often contain hazardous chemicals and heavy metals. These wastes require specialized treatment and disposal protocols under strict environmental regulations, increasing compliance costs for industries. Many companies spend a substantial portion of their operational budgets on safe waste handling, storage, and transport.

Improper disposal can lead to soil and water contamination, resulting in legal penalties and costly remediation activities. Emulsion-based cleaners pose additional challenges because they are difficult to separate and recycle, adding to the complexity of waste management. These factors discourage companies from expanding high-volume cleaning operations and create barriers for industries with limited resources. As a result, waste management difficulties contribute to higher operational burdens and slow adoption of certain cleaning technologies.

Opportunities - Rising Demand for Biodegradable and Enzyme-Driven Cleaners is Creating Strong Opportunities for Sustainable Product Innovation

The global move toward biodegradable, low-toxicity metal cleaners presents a strong growth opportunity for manufacturers. Bio-based and enzyme-driven formulations are gaining traction as industries prioritize sustainability and compliance with international environmental guidelines. These cleaners offer effective removal of contaminants without damaging sensitive surfaces, making them suitable for high-precision industries such as electronics, pharmaceuticals, and medical devices.

Their natural decomposition reduces ecological impact and supports green manufacturing certifications. As governments and organizations worldwide promote cleaner technologies, demand for such solutions is expected to increase steadily. Companies investing in R&D to create specialized enzyme-based cleaners are positioned to capture significant market share, especially in sectors that require both safety and high performance. This shift aligns with global sustainable development trends and creates long-term revenue potential for innovative manufacturers.

Rapid Industrialization in Emerging Economies is Opening New Growth Avenues for Versatile and Cost-Effective Metal Cleaners

Rapid industrialization in emerging regions, particularly the Asia Pacific and Latin America, offers significant growth opportunities for the metal cleaners market. These regions are experiencing strong growth in automotive, machinery, construction, and electronics manufacturing, creating a rising demand for cleaning solutions that ensure production quality and equipment reliability. Government initiatives supporting industrial development, such as subsidies and incentives for manufacturing, further fuel the need for efficient cleaning systems.

Companies operating in these markets benefit from forming strategic partnerships with local industries, offering customized products suited to regional conditions and cost expectations. Additionally, industries in developing regions are gradually shifting toward eco-friendly and technologically advanced cleaners, driven by rising environmental awareness and regulatory updates. This creates room for innovative suppliers to introduce modern technologies such as ultrasonic and high-pressure cleaning systems, enhancing their market presence.

Category-wise Analysis

By Product Type Insights

Aqueous cleaners lead the product type segment with around 68% market share because they are versatile, safe, and environmentally compliant. These water-based solutions, including alkaline formulations, effectively remove oils, grease, and dirt without the health and safety risks associated with solvent-based products. Industrial users prefer them for heavy-duty applications like degreasing steel parts, as they offer good rinseability and leave minimal residue. With regulations phasing out chlorinated solvents, many automotive and manufacturing plants are shifting to aqueous cleaners to ensure efficiency, worker safety, and regulatory compliance.

By Metal Substrate Analysis

Ferrous metals hold nearly 62% of the substrate segment due to their widespread use in construction, machinery, and industrial equipment. Steel and iron surfaces require strong cleaning solutions to remove rust, scale, and heavy contaminants. Acidic aqueous cleaners work exceptionally well for these metals, helping prevent corrosion and extending component life. The dominance of ferrous metals results from their high production volumes and frequent maintenance needs. Industries often prefer cost-effective, high-performance cleaners for these metals, making them the largest users compared to specialized non-ferrous segments.

By Cleaning Chemistry Insights

Surfactant-based cleaners account for about 55% of the market because they efficiently break down oils and enhance wetting on metal surfaces. By lowering surface tension, surfactants enable deeper penetration and effective removal of contaminants. They are widely used in electronics, automotive, aerospace, and food processing due to their ability to support cleaner surfaces and reduce defects. Many formulations also use biodegradable ingredients, aligning with sustainability goals and environmental regulations. Their flexibility and strong cleaning performance make surfactant-based products a preferred choice across diverse industries.

By Cleaning Method Insights

Immersion cleaning accounts for nearly 40% of the cleaning method segment thanks to its effectiveness in handling complex shapes and batch processing. This method involves submerging components in cleaning baths, ensuring that all areas, including hard-to-reach sections—receive uniform cleaning. It reduces manual labor, improves consistency, and supports automation, making it ideal for high-volume operations such as automotive manufacturing. Industries prefer immersion cleaning for its cost-effectiveness, reliability, and suitability for removing stubborn contaminants more efficiently than spray or manual cleaning techniques.

By Industry Analysis

The automotive sector leads the end-use segment with about 35% market share because of its high production volumes and strict quality standards. Metal cleaners are essential for preparing surfaces before painting, welding, and assembly to prevent defects and ensure strong adhesion. With the rise of electric vehicles, demand for safe and non-corrosive cleaners for battery components is growing. The industry uses large quantities of cleaning solutions for stamping, fabrication, and finishing processes, making it the top consumer among end-use industries.

Regional Insights

North America Metal Cleaners Analysis

North America remains a leading market for metal cleaners, supported by advanced manufacturing industries and strong regulatory frameworks. The U.S. promotes the adoption of sustainable cleaning solutions through strict guidelines that encourage reduced waste generation and safer chemical usage. Innovation continues to thrive in the region due to substantial government funding for green manufacturing technologies.

Industries such as aerospace, automotive, and defense rely on high-performance cleaners to maintain precision and enhance component durability. Research organizations play a key role in developing new formulations that improve corrosion resistance and reduce environmental impact. With growing investment in electric vehicle production and advanced manufacturing, North America continues to adopt modern cleaning technologies, driving steady market growth and supporting ongoing innovation in metal cleaning solutions.

Europe Metal Cleaners Trends Analysis

Europe’s metal cleaners market is shaped by stringent environmental policies and strong emphasis on sustainable manufacturing practices. Countries such as Germany, France, and the U.K. are leading adopters of eco-friendly cleaning technologies due to strict chemical regulations and industry-wide sustainability goals. European industries increasingly prefer enzyme-based and biodegradable cleaners that comply with environmental safety standards.

The region’s automotive, aerospace, and shipbuilding sectors rely on advanced cleaning systems to maintain high-quality production and meet emission targets. Ongoing research and innovation support the development of high-performance formulations, while regulatory alignment under the EU Green Deal accelerates the transition to low-impact cleaning solutions. These factors position Europe as a mature, innovation-driven market with strong demand for environmentally compliant metal cleaners.

Asia Pacific Metal Cleaners Trends

Asia Pacific is experiencing rapid demand growth in the metal cleaners market due to expanding industrialization, manufacturing output, and infrastructure development. Countries like China, India, Japan, and South Korea are major contributors, driven by rising automotive production, electronics manufacturing, and heavy industries. Strong government support for industrial growth and stricter environmental policies encourage the adoption of modern cleaning technologies, including bio-based and ultrasonic systems.

Japan’s focus on precision engineering boosts the use of high-efficiency cleaners, while India’s automotive boom drives strong demand for specialized cleaning solutions for metals like aluminum and brass. Oil and gas operations in Southeast Asia further increase the need for durable and effective cleaners. Overall, the region’s growing industrial base and shift toward sustainable practices continue to strengthen market expansion.

Competitive Landscape

The global metal cleaners market exhibits a consolidated structure, with top players controlling over significant share through vertical integration and R&D investments. Leaders pursue expansion via mergers and sustainable product launches, focusing on bio-based innovations to differentiate. Key strategies include partnerships for regional penetration, like joint ventures in Asia, and R&D trends emphasizing low-VOC formulations compliant with EPA and REACH. Emerging models involve subscription-based supply for industrial users, enhancing loyalty, while differentiators like enzyme tech provide edge in high-precision sectors. Overall, competition drives efficiency, with fragmentation in niche bio-segments offering entry for innovators.

Key Market Developments

- April 2025: BASF SE introduced Trilon G, a GLDA-based chelating agent designed to improve sustainable metal cleaning by reducing chemical load and wastewater impact. It supports eco-efficient industrial applications and strengthens BASF’s green portfolio.

- March 2025: Evonik Industries AG partnered with Sea-Land Chemical in an exclusive U.S. distribution agreement, expanding nationwide access to its advanced surface treatment solutions for automotive, aerospace, and industrial cleaning needs. This move enhances customer reach and service efficiency.

- January 2024: The Dow Chemical Company launched a bio-solvent product line aimed at corrosion inhibition for marine equipment, offering improved environmental compatibility and compliance with global green standards. It supports safer, low-impact cleaning solutions for harsh marine conditions.

Companies Covered in Metal Cleaners Market

- BASF SE

- 3M Company

- E. I. du Pont de Nemours and Company

- ICL Performance Materials

- Henkel

- Eastman Chemical Company

- The Dow Chemical Company

- The Chemours Company

- Evonik Industries AG

- Quaker Chemical Corporation

- Stepan Company

- Houghton International

- Air Products and Chemicals

- Rochester Midland Corporation

- Clariant AG

Frequently Asked Questions

The global metal cleaners market is expected to reach US$ 18.2 Billion by 2032, growing from US$ 13.0 Billion in 2025 at a CAGR of 4.9%.

Key drivers include surging industrial manufacturing, particularly in automotive and aerospace, alongside the push for sustainable, low-VOC formulations to meet environmental regulations.

Aqueous cleaners dominate with about 68% share, valued for their eco-friendliness and effectiveness in removing contaminants from various metal surfaces.

North America leads, supported by U.S. regulatory frameworks like EPA guidelines and strong demand from advanced manufacturing sectors.