- Medical Devices

- Medical Image Analysis Software Market

Medical Image Analysis Software Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Medical Image Analysis Software Market by Product (Integrated Software, Standalone Software), Modality (Tomography, Ultrasound Imaging, Radiographic Imaging, Combined Modalities, Mammography), Imaging Type, Application, End-user, and Regional Analysis from 2026 - 2033

Medical Image Analysis Software Market Share and Trends Analysis

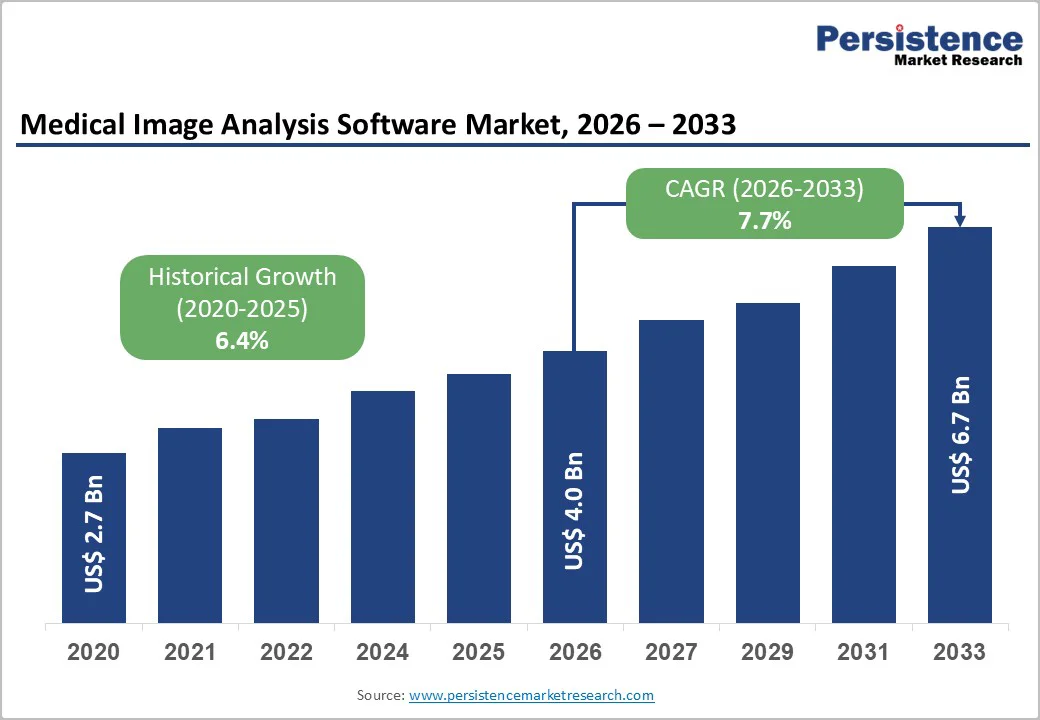

The global medical image analysis software market size is estimated to reach US$ 4.0 billion in 2026 and is projected to reach US$ 6.7 billion by 2033, growing at a CAGR of 7.7% between 2026 and 2033. Medical image analysis refers to the use of specialized software to interpret, quantify, and derive clinically meaningful insights from imaging modalities such as computed tomography (CT), magnetic resonance imaging (MRI), X-ray, ultrasound, positron emission tomography (PET), and digital pathology.

These tools enhance diagnostic accuracy by automating measurements, detecting subtle abnormalities, and highlighting patterns that may be invisible to the human eye. Advanced algorithms further support early prediction of disease progression, risk stratification, and assessment of treatment responses. By integrating imaging data with clinical parameters, medical image analysis software enables more precise decision-making and facilitates clinicians personalize care pathways for improved patient outcomes.

Key Industry Highlights:

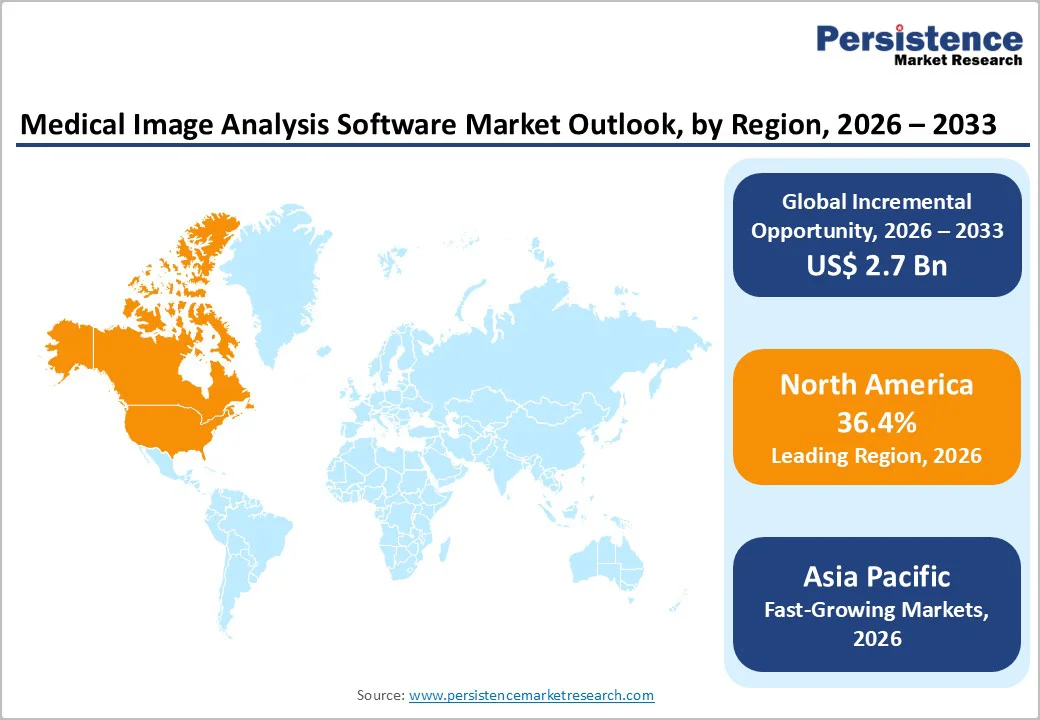

- Leading Region: North America dominates the global market with 36.4%, driven by advanced healthcare infrastructure, high AI adoption, and significant investment in imaging technologies.

- Fastest-Growing Region: Asia Pacific market is expected to grow rapidly with a CAGR of 9.6% in the forecast period, fueled by increasing cancer incidence, expanding diagnostic facilities, and rising adoption of AI-enabled imaging platforms.

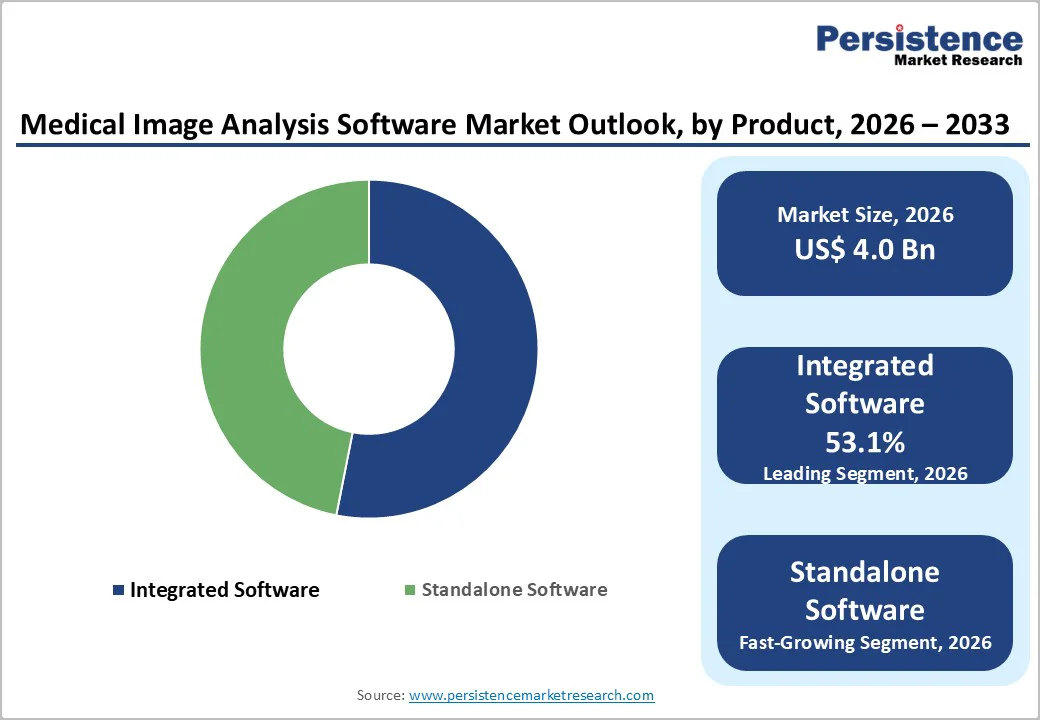

- Leading Product: Integrated Software leads with 53.1% share, supported by its ability to unify workflows, improve efficiency, and enable seamless integration across multiple clinical departments.

- Leading Modality: Tomography is anticipated to lead with 39.5% share, owing to its high-resolution volumetric imaging, versatility across clinical applications, and growing use in cancer and cardiovascular diagnostics.

- Leading Imaging Type: 4D imaging is estimated to dominate with 48.1% share, as it provides real-time functional insights for cardiac, respiratory, tumor, and fetal motion assessments.

- Leading Application: Cardiology remains dominant with 22.4%, driven by rising cardiovascular disease prevalence, advanced 4D imaging adoption, and AI-enabled automated quantification tools for precise diagnosis.

- Leading End-user: Hospitals lead with 36.2% share due to high imaging volumes, centralized infrastructure, multi-specialty coordination, and demand for integrated software solutions enhancing workflow efficiency.

| Key Insights | Details |

|---|---|

|

Global Medical Image Analysis Software Market Size (2026E) |

US$ 4.0 Billion |

|

Market Value Forecast (2033F) |

US$ 6.7 Billion |

|

Projected Growth (CAGR 2026 to 2033) |

7.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.4% |

Market Dynamics

Driver - Rising Disease Burden and Imaging Digitization Accelerate Software Adoption

The global medical image analysis software market is expanding rapidly as healthcare systems face rising diagnostic complexity, higher patient volumes, and an increasing burden of chronic diseases. A major driver of this growth is the acceleration of cancer cases worldwide.

For example, the International Agency for Research on Cancer (IARC) under the World Health Organization (WHO) reported in 2024 that 2022 saw 20 million new cancer cases, 9.7 million deaths, and 53.5 million people living within five years of a diagnosis, reinforcing the need for faster, more accurate, and scalable image-analysis tools.

Supporting this trend, hospitals globally are integrating electronic health records (EHR), multimodal imaging systems, and computer-aided diagnostic technologies to manage growing imaging datasets more efficiently. These solutions enhance image quality, reduce diagnostic turnaround times, and enable seamless sharing of imaging data across clinical teams—making them essential to modern care delivery. Research institutions also benefit from automated pattern recognition and cross-patient comparisons, which accelerate biomarker discovery and strengthen public-health insights.

The need for advanced software is further amplified by rising clinician burnout. A 2023 American Medical Association (AMA) survey found that 63% of physicians and 49% of nurses experienced burnout, driven by workload and staffing pressures. In response, vendors are introducing AI-powered tools that reduce clinical burden.

A key example is GE HealthCare, which in December 2024 introduced Sonic DL for 3D, an advanced deep-learning MRI acceleration technology. Building on the success of its AIR Recon DL platform—used in over 34 million scans—Sonic DL expands 12× acceleration from cardiac MRI to 3D brain, spine, orthopedic, and body imaging, cutting scan times by up to 86% and enabling faster, more confident diagnoses. Together, these factors continue to drive robust global adoption of medical image analysis software.

Restraints - Bias, Security Risks, and Limited Trust Hinder Clinical Integration

The global medical image analysis software market faces several restraints that slow clinical adoption despite strong technological momentum. A major challenge is dataset bias, as many training datasets underrepresent certain demographics or rare conditions, leading to misinterpretation and reduced model reliability in real-world settings. This becomes more critical as hospitals increasingly rely on automated tools for disease detection and risk assessment across diverse patient populations.

Security and compliance concerns add further complexity. Medical image analysis platforms process large volumes of sensitive data, and any vulnerabilities raise the risk of breaches and unauthorized access. This is compounded by pushback from healthcare professionals, who may hesitate to adopt complex systems that require strict data-quality maintenance and additional patient-consent workflows. Trust is also limited by the lack of interpretability in deep-learning models, as clinicians often struggle to understand how an algorithm arrives at its decision, hindering confidence in its predictions.

Real-world deployment introduces additional risks. Every imaging algorithm can produce artifacts: over-smoothing may obscure subtle pathology, while hallucinated structures can mimic lesions. Performance also varies depending on scanner hardware, patient characteristics, and acquisition protocols.

Although regulatory frameworks such as U.S. FDA 510(k) clearances provide oversight, departments installing new reconstruction or analysis tools must conduct phantom and human testing, ensure transparent labeling of AI-processed images, and continuously monitor models for performance drift. These technical, regulatory, and trust-related barriers collectively restrain the growth of the global market.

Opportunity - Rapid AI Regulatory Approvals and Ecosystem Innovation Expand Market Potential

The global medical image analysis software market is witnessing expanding opportunities such as regulatory acceptance, AI maturity, and imaging digitization, accelerating worldwide. A major catalyst is the sharp rise in U.S. regulatory approvals for AI-enabled devices. In October 2024, the U.S. Food and Drug Administration (FDA) reported authorizing nearly 950 AI-driven medical devices between 1995 and 2024, with approvals surging from just six in 2015 to 221 in 2023. This trend signals strong confidence in AI as a medical device and encourages broader commercialization of imaging software globally.

These approvals also include clinically transformative tools. For instance, Siemens Healthineers’ AI-Rad Companion enhances quantitative and qualitative interpretation of clinical images, while Digital Diagnostics’ LumineticsCore autonomously detects diabetic retinopathy without specialist involvement—demonstrating how AI can expand diagnostic capacity where experts are limited. At the same time, major medtech companies, along with new startups, continue to develop advanced imaging AI solutions, pushing the boundaries of AI-enabled imaging innovation.

Further opportunity emerges from large-scale platform modernization efforts across global health systems. In November 2025, Neusoft launched next-generation intelligent imaging solutions that integrate data-driven engines across clinical, administrative, and educational workflows. With a focus on medical collaboration, precision diagnostics, departmental optimization, and research enablement, such innovations strengthen the ecosystem for AI-embedded imaging software. Together, these developments create a robust landscape of opportunity for the global medical image analysis software market.

Category-wise Analysis

By Product Insights: Integrated Software Dominates Due to Unified Workflow Efficiency

Integrated software solutions are expected to capture 53.1% of the global medical image analysis software market by 2026 due to their ability to streamline workflows across radiology, cardiology, oncology, and neurology departments. These platforms consolidate image viewing, reporting, 3D reconstruction, and quantitative analysis into a single interface, reducing operational complexity. Their seamless compatibility with Picture Archiving and Communication Systems (PACS) and EHRs helps eliminate data silos. Thus, supporting faster decision-making, enabling multidisciplinary coordination, and minimizing the cost and effort of maintaining multiple standalone tools.

By Modality Insights: Tomography Lead Owing to High Diagnostic Precision and Versatile Use

Tomography is anticipated to lead with 39.5% of the global medical image analysis software market share in 2026 due to its central role in high-resolution disease assessment. CT, MRI, and PET remain indispensable for early detection, treatment planning, and longitudinal monitoring across cancer, cardiovascular disorders, and neurological diseases. Their ability to generate volumetric datasets requires advanced software for segmentation, fusion, and quantification. As multi-modal tomography adoption expands in hospitals and diagnostic centers, demand for robust analytical platforms capable of handling complex datasets continues to strengthen rapidly.

By Imaging Type Insights: 4D Imaging Capture Market Leadership Through Real-Time Functional Insights

4D imaging is estimated to dominate with a 48.1% share of the global medical image analysis software market in 2026 due to its ability to capture motion-based functional information. It enables dynamic assessment of cardiac movement, respiratory patterns, tumor motion, and fetal development, improving diagnostic reliability. Clinicians increasingly rely on 4D datasets for radiation therapy planning, interventional guidance, and advanced cardiology evaluations. These time-resolved images require sophisticated analytics for tracking, prediction, and automated interpretation. As real-time visualization becomes essential in precision medicine, the need for advanced 4D analysis platforms continues to accelerate.

By Application: Cardiology Leads Driven by Rising Cardiovascular Disease Burden

Cardiology is projected to account for nearly 22.4% of the medical image analysis software market in 2026, driven by the rising global incidence of coronary artery disease, heart failure, and structural abnormalities. Advanced software supports automated ejection-fraction calculation, plaque characterization, perfusion analysis, and valve-function assessment through CT, MRI, and echocardiography. Increasing adoption of cardiac 4D imaging and AI-enabled quantification tools enhances diagnostic accuracy and reduces interpretation time. As cardiology shifts toward earlier detection, personalized treatment planning, and image-guided interventions, demand for sophisticated cardiac analysis platforms continues to intensify across clinical settings.

Regional Insights

North America Medical Image Analysis Software Market Trends

North America is projected to capture 36.4% of the global medical image analysis software market by 2026, driven by a strong push toward AI-enabled clinical decision support and the region’s rapid digitalization of diagnostic workflows. This momentum is reinforced by the growing pressure on clinicians to interpret rising volumes of complex imaging data. To illustrate this, the American Medical Association (AMA) reported in 2024 that an ICU physician today manages nearly 1,300 data points per patient—compared to only seven pieces of information 50 years ago—highlighting why the AMA is investing heavily in research, resource development, and AI-governance programs to ensure technology enhances physician efficiency.

Supporting this shift toward advanced AI capability, October 2024 saw the development of UCLA’s (University of California, Los Angeles) SLIViT (SLice Integration by Vision Transformer) model, which achieved clinical-expert-level accuracy across multiple 3D modalities such as retinal optical coherence tomography (OCT), ultrasound videos, MRI, and CT. This demonstrates how adaptable deep-learning tools in expanding real-world diagnostic automation. Further strengthening market growth, October 2025 marked a major expansion milestone for Subtle Medical, whose FDA-cleared AI enhancement tools surpassed 600 U.S. installations, showing accelerating enterprise adoption. Together, these advancements underscore why North America remains the most influential hub for medical image analysis software innovation and revenue expansion.

Europe Medical Image Analysis Software Market Trends

Europe is projected to account for 28.1% of the global medical image analysis software market by 2026, supported by its strong academic ecosystem, emphasis on research-driven innovation, and active collaboration across clinical and engineering disciplines. This foundation continues to accelerate the development of advanced algorithms, imaging biomarkers, and AI-based diagnostic tools, strengthening the region’s role in shaping global imaging standards.

One key example of this momentum is the 29th UK Conference on Medical Image Understanding and Analysis (MIUA), held in July 2025 at the University of Leeds. Such platforms bring together experts from mathematics, computer science, bioinformatics, engineering, biosciences, and clinical practice, fostering cross-disciplinary exchange and enabling rapid translation of research into practical medical imaging solutions.

Further illustrating Europe’s strong innovation pipeline, November 2025 saw Median Technologies (France) present its AI-powered Software as a Medical Device (SaMD) suite, Eyonis®, including its Lung Cancer Screening (LCS) module, at the Radiological Society of North America (RSNA) meeting. Designed to enhance diagnostic accuracy and screening efficiency, Eyonis® LCS has already completed pivotal studies and is under U.S. FDA 510(k) and European CE-mark review—highlighting Europe’s growing influence in developing regulatory-ready, AI-driven imaging solutions.

Asia Pacific Medical Image Analysis Software Market Trends

The medical image analysis software market in the Asia Pacific is rapidly expanding and projected to grow at a CAGR of 9.6%, supported by rising diagnostic demand, accelerated digital health adoption, and increasing investment in AI-driven imaging tools. The region faces a steadily growing clinical workload, particularly in oncology, cardiology, and chronic disease management, which is pushing hospitals toward software that can automate image interpretation, standardize reporting, and support early detection. A key indicator of this rising clinical burden comes from the Global Cancer Observatory (GLOBOCAN) 2022, which reports that Asia accounted for 49.2% of global cancer cases and 56.1% of cancer deaths. India alone ranks third in cancer incidence and second in mortality within the South-East Asia region, underscoring the need for advanced imaging software capable of identifying disease earlier and improving triage efficiency.

Building on this need for precision diagnostics, countries across the Asia Pacific particularly India, China, Japan, and South Korea—are accelerating AI integration in radiology. Large-scale government digital-health programs, expanding cloud-based PACS deployments, and partnerships between hospitals and AI startups are strengthening access to high-quality imaging analytics. As cancer incidence resurges in the region, the adoption of software for cancer screening, automated nodule detection, and risk stratification is growing rapidly. Together, these factors position Asia Pacific as one of the strongest future growth hubs for medical image analysis software.

Competitive Landscape

The medical image analysis software market is highly competitive, driven by continuous innovation in AI-powered diagnostics, faster processing workflows, multimodal integration, and cloud-based imaging platforms. Vendors compete on algorithm accuracy, interoperability, regulatory approvals, and enterprise scalability, while partnerships with hospitals, imaging centers, and device manufacturers strengthen market presence and accelerate adoption across clinical specialties.

Key Industry Developments:

- In December 2024, GE HealthCare introduced Sonic DL for 3Dii, expanding its deep learning MRI acceleration technology beyond cardiac to brain, spine, orthopedic, body, and cardiac exams, offering up to 12x faster scans and reducing scan times by nearly 86%.

- In November 2025, Royal Philips launched Image Management 15, the next-generation Vue PACS with a zero-footprint web diagnostic viewer that delivers full workstation-level clinical capability via a browser, enhancing mobility, collaboration, radiologist efficiency, and reducing IT complexity across healthcare enterprises.

Companies Covered in Medical Image Analysis Software Market

- Siemens Healthineers AG

- Koninklijke Philips N.V.

- Hologic, Inc.

- Digital Diagnostics Inc.

- ResolutionMD

- Leica Microsystems

- Aidoc

- Thermo Fisher Scientific Inc.

- iSchemaView, Inc

- 3DHISTECH Ltd.

- Butterfly Network, inc

- GE HealthCare

- Medtronic

- Subtle Medical, Inc.

- Synopsys, Inc.

- Flywheel

- Median Technologies

- Orases

Frequently Asked Questions

The global medical image analysis software market is projected to be valued at US$ 4.0 Billion in 2026.

Rising chronic disease burden, growing imaging volumes, AI integration, and digitization of healthcare workflows drive market growth.

The global market is poised to witness a CAGR of 7.7% between 2026 and 2033.

Expansion of AI-enabled imaging, regulatory approvals, cloud adoption, and real-time multimodal diagnostic solutions present major growth opportunities.

Major players in the global are Siemens Healthineers AG, Koninklijke Philips N.V., Hologic, Inc., Digital Diagnostics Inc., ResolutionMD, and others.