- Hardware & Software IT Services

- Healthcare IT Market

Healthcare IT Market Size, Share, and Growth Forecast, 2026-2033

Healthcare IT Market by Solution Type (Software, Hardware Devices, Services), Technology (Cloud Deployment, AI & ML, Big Data & Analytics, Interoperability & HIE Platforms, Cybersecurity, Telehealth, Smart Hospital, Others), End User (Hospitals & Health Systems, Ambulatory Clinics, Home Healthcare Providers, Insurance Companies, Pharmaceutical Companies, Government & Public Health Agencies), and Regional Analysis for 2026-2033

Healthcare IT Market Share and Trends Analysis

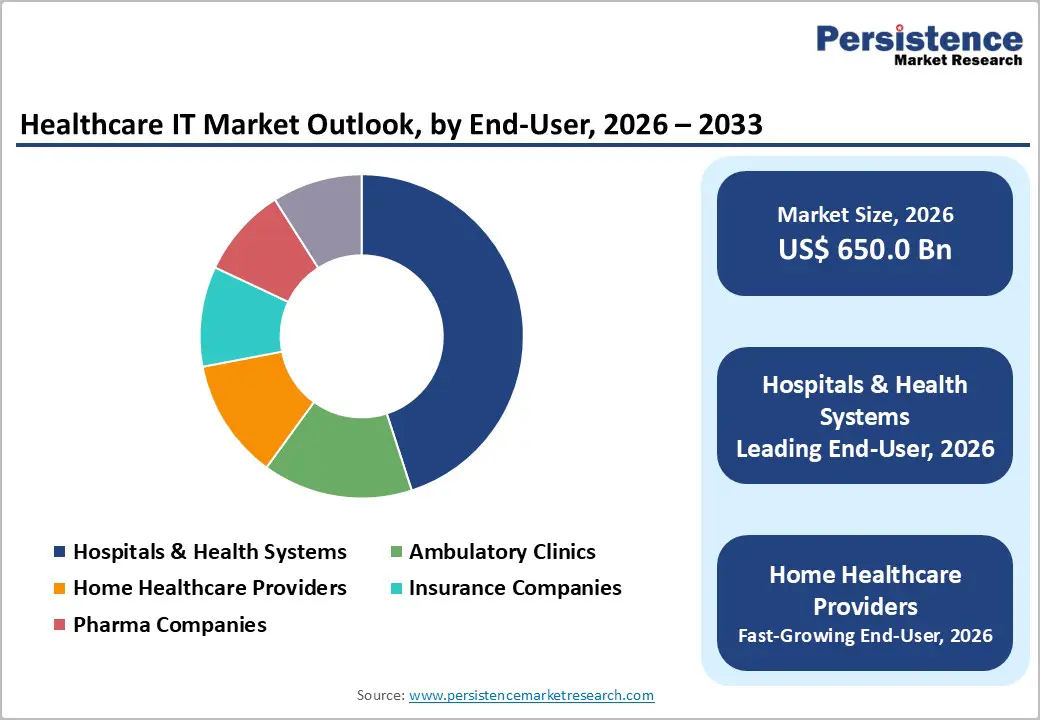

The global healthcare IT market size is likely to be valued at US$ 650.0?billion in 2026, and is projected to reach US$ 1,750.2?billion by 2033, growing at a CAGR of 15.2% during the forecast period 2026?2033.

Healthcare providers are accelerating digital transformation initiatives to streamline clinical workflows, improve care coordination, and enhance patient engagement. Hospitals and integrated delivery networks are expanding the deployment of electronic health record (EHR) and electronic medical record (EMR) systems to centralize patient data and support evidence-based decision making. Telemedicine platforms are increasing access to virtual consultations, particularly in rural and underserved regions.

Artificial intelligence (AI) enabled analytics are assisting clinicians in diagnostics, risk stratification, and resource planning. Cloud-based infrastructure is supporting scalability, cost optimization, and real-time data access across distributed healthcare environments. These technology investments are strengthening operational efficiency and supporting value-based care models. The market is expanding beyond traditional hospital settings as remote patient monitoring and Internet of Medical Things (IoMT) devices are integrating into home-based and ambulatory care pathways. Interoperability standards such as Fast Healthcare Interoperability Resources (FHIR) and Health Level Seven (HL7) are enabling secure data exchange across systems and improving cross-provider collaboration. Public health agencies are supporting digital adoption through funding programs and national health information exchange frameworks. As data volumes are increasing across clinical, imaging, and wearable device platforms, cybersecurity solutions are becoming critical for safeguarding protected health information and maintaining regulatory compliance. Healthcare organizations are investing in encryption technologies, identity management systems, and real-time threat monitoring tools to mitigate cyber risk.

Key Industry Highlights

- Dominant Solution Types: Software solutions are estimated to account for about 42% revenue share in 2026, while services are projected to grow the fastest at around 16% CAGR through 2033, driven by integration and IT support demands.

- Leading Technologies: Cloud deployment is expected to hold roughly 29% revenue share in 2026, whereas AI & machine learning (ML) are likely to post a 2026-2033 CAGR of 17.5%, driven by analytics, clinical decision support, and workflow automation.

- End-User Leadership: Hospitals & health systems are set to hold an estimated revenue share of 45% in 2026, with home healthcare growing the fastest at 15.8% CAGR due to remote and decentralized care adoption

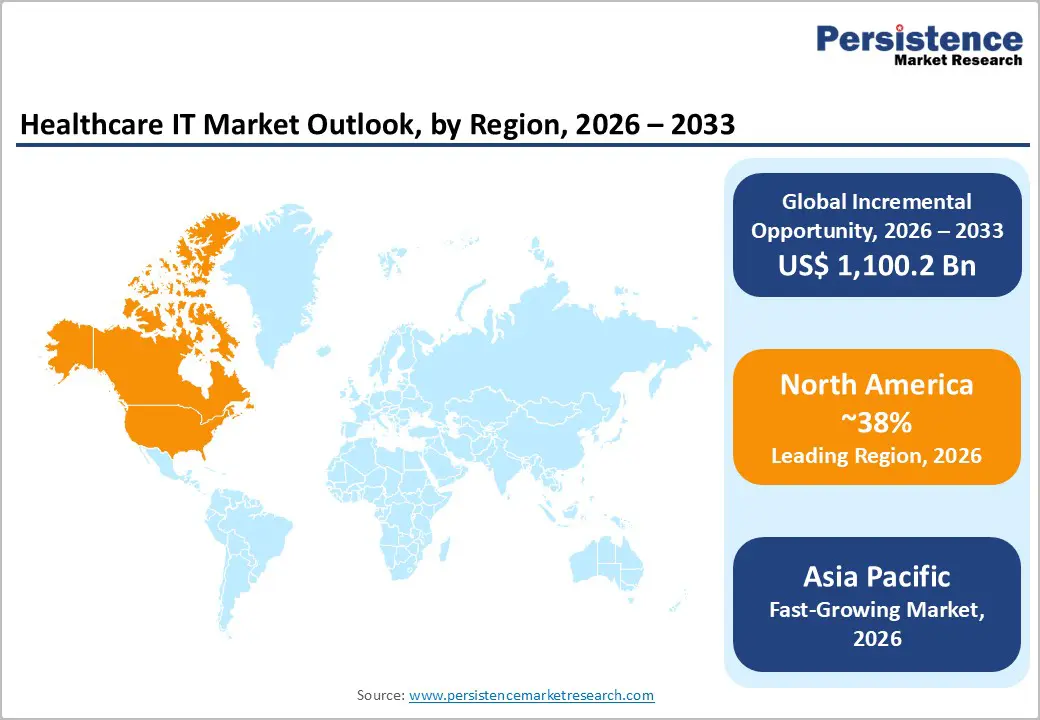

- Regional Leadership: North America is estimated to lead with 38% share in 2026, while the Asia Pacific market is expected to register the highest CAGR of around 18.2%, aided by digital health initiatives.

- Market Growth Driver: The adoption of EHR/EMR software, telehealth platforms, IoMT devices, interoperability frameworks, and cybersecurity solutions is expected to continue driving efficiency, patient engagement, and scalable healthcare operations.

| Key Insights | Details |

|---|---|

| Healthcare IT Market Size (2026E) | US$ 650.0 Bn |

| Market Value Forecast (2033F) | US$ 1,750.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 15.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 14.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Accelerating Adoption of Integrated Digital Health Solutions across the Care Continuum

The adoption of EHR/EMR systems, interoperable platforms, telemedicine, and IoMT devices is reshaping healthcare delivery globally. In 2025, over 90% of hospitals in high-income regions reported EHR adoption, while telehealth usage surged, with more than 90% of providers offering virtual care services. Interoperability standards such as FHIR and HL7 are being implemented in over 30 countries to enable seamless data exchange. Patient demand for mobile health apps and remote monitoring continues to grow, particularly for chronic disease management. Value-based care models are increasing reliance on technologies that improve outcomes and operational efficiency. These factors are driving substantial healthcare IT investments across hospitals, clinics, and home care providers.

Emerging technologies including AI and ML, Big Data Analytics, and cloud/hybrid deployment are further accelerating adoption. Cloud platforms now support approximately 65% of telehealth services globally, enabling scalable infrastructure and real-time analytics. Connected devices and IoMT solutions, now in the hundreds of millions worldwide, support remote monitoring and reduce hospital readmissions. AI-driven predictive analytics enhance diagnostics and workflow efficiency. Strong focus on cybersecurity and privacy compliance is prompting increased IT spending. These integrated digital strategies are expected to sustain robust market growth and improve patient-centric care models across diverse healthcare settings.

High Implementation Costs and Escalating Security Compliance Burden

The initial costs of deploying healthcare IT solutions, including EHR/EMR upgrades, interoperability modules, telemedicine platforms, and cloud migration, continue to limit adoption, especially among small and mid sized providers. For example, a 2024 survey found that over 55% of community hospitals cited upfront IT investment costs as a key barrier to digital adoption, delaying modernization initiatives. Budget constraints often force organizations to defer advanced functionalities in favor of core clinical systems, slowing interoperability and analytics deployment. In emerging markets with limited healthcare funding, these pressures are even more pronounced, leading to uneven digital transformation across geographies. Long deployment cycles and complex integration requirements further elevate total cost of ownership, reducing return on investment in the short term.

Compounding cost barriers are the escalating data security and compliance challenges inherent in digital healthcare ecosystems. Healthcare remains one of the most targeted industries for cyberattacks, with over 85% of surveyed providers reporting at least one cybersecurity incident in the past year, increasing fear of data breaches. Regulations such as Health Insurance Portability and Accountability Act (HIPAA) in the U.S. and the General Data Protection Regulation (GDPR) in Europe mandate rigorous security controls, risk assessments, and breach reporting, requiring continuous investment in advanced cybersecurity solutions and governance frameworks. Providers must balance innovation with accountability, ensuring secure data exchange while maintaining clinical productivity. As cyber threats evolve, the complexity and cost of compliance may slow IT adoption and divert resources from other strategic priorities.

Technology Led Growth across Regions and Care Settings

The healthcare IT landscape is benefiting from strategic government and institutional initiatives that accelerate adoption of digital solutions across technologies and regions. For instance, the World Health Organization (WHO) Regional Office for Europe established a new digital health center in Germany, aimed at strengthening digital health policy, training, and data analytics capabilities, creating a foundation for interoperable platforms and analytics adoption. The U.K. government announced a £ 600?million health data research service to improve patient care and accelerate medical research through expanded data access and security. Similarly, New Zealand awarded a contract for a nationwide Shared Digital Health Record System, leveraging FHIR standards for interoperable clinical data exchange, underscoring growing demand for scalable data infrastructure across national health systems.

Emerging digital health use cases are driving strong investment opportunities in AI, automation, and cloud technologies. In Australia, an AI-powered ambient scribing initiative was launched to reduce clinician documentation burden, highlighting demand for scalable AI solutions integrated into practice management systems. In South Korea, the adoption of digital maturity assessment models is extending digital transformation beyond large hospitals to smaller providers, supporting broader market penetration. Africa is enhancing digital governance through Rwanda’s Health Intelligence Center, consolidating real-time health data for improved decision-making and resource allocation. Meanwhile, new digital health regulations in Kenya are reinforcing opportunities for interoperable platforms and health information management systems in underserved regions, creating a foundation for scalable, technology-driven care delivery.

Category-wise Analysis

Solution Insights

Software solutions are estimated to acquire about 42% of the healthcare IT market revenue share in 2026, and lead demand driven by EHR/EMR systems, telemedicine software, clinical decision support, revenue cycle management, and patient engagement platforms. A notable 2025 industry development saw Innovaccer launch its ‘Gravity’ cloud?agnostic healthcare intelligence platform designed to unify data from EHRs, claims, and other systems to accelerate AI deployment and improve interoperability, reducing implementation timelines significantly. Epic also introduced Launchpad, a structured program to help providers operationalize generative AI workflows into clinical use, strengthening software capabilities. These initiatives underscore software’s central role in improving care coordination and administrative efficiency across provider settings.

IoMT and connected hardware devices are projected to have a 16% CAGR through 2033, and be the fastest growing solution type as providers adopt wearables, sensors, and remote monitoring tools for continuous patient engagement. Virtual hospitals such as Seha Virtual Hospital in Saudi Arabia expanded digital care, collaborating with traditional hospitals to provide specialized remote services, reflecting device?enabled care beyond traditional facilities. Real time device data integrated into clinical workflows enhances chronic disease management and patient monitoring, expanding the role of connected hardware in healthcare IT.

Technology Insights

Cloud and hybrid deployment are anticipated to hold approximately 29% of technology share in 2026, remaining central to healthcare IT by enabling scalable storage, centralized analytics, and real-time insights. The EU’s European Health Data Space (EHDS) regulation, effective March 2025, standardizes cross-border electronic health data use and provides secure access for providers, researchers, and policymakers, reinforcing cloud ecosystems. The CMS Digital Health Technology Ecosystem (eHealth Exchange aligned network) announced in July 2025 also promotes harmonized data exchange across EHRs, further encouraging cloud and analytics adoption. These initiatives improve interoperability, compliance, and insight generation across clinical and administrative workflows. Hospitals, large health systems, and research organizations are increasingly leveraging cloud analytics for population health, predictive care, and operational efficiency.

AI and Machine Learning solutions are projected as the fastest-growing technology segment with approximately 17.5% CAGR from 2026 to 2033, driven by predictive care models, clinical decision support, and workflow automation. Investor confidence grew in AI-enabled platforms, such as Omada Health’s US$ 150 million IPO, highlighting scalable solutions for revenue cycle and care coordination. Programs such as Epic’s Launchpad accelerated responsible AI integration in operational settings. These developments enhance diagnostic accuracy, workflow efficiency, and patient outcomes. Providers are adopting AI for real-time predictive analytics, administrative automation, and virtual care optimization. AI and Machine Learning are increasingly central to healthcare organizations’ digital transformation strategies.

End-User Insights

Hospitals and health systems are estimated to account for approximately 45% of the healthcare IT market share in 2026. These providers have complex clinical workflows, extensive compliance obligations, and large-scale digital transformation initiatives. A notable 2025 development was the MyCare digital access app in Scotland, which allows patients to view appointments and health records via mobile devices, illustrating national efforts to enhance hospital-linked digital services. Large-scale IT adoption supports interoperability, centralized data management, and operational efficiency. Hospitals are investing in EHR integration, analytics platforms, and cloud infrastructure to improve care quality and patient outcomes. These organizations continue to be the primary adopters of advanced healthcare IT solutions.

Home healthcare providers and ambulatory clinics are projected to be the fastest-growing end-user segment at approximately 15.8% CAGR from 2026 to 2033 as care delivery shifts toward decentralized, patient-centered models. AI-enabled general practice initiatives in Australia introduced ambient scribing and documentation automation in primary care, demonstrating technology adoption among outpatient and community providers. Telemedicine platforms, remote monitoring devices, and patient engagement applications support continuous, home-based care. Scalable cloud solutions reduce infrastructure costs and enhance distributed care delivery. The adoption of connected devices and virtual care platforms improves chronic disease management, patient engagement, and continuity of care outside traditional hospital settings.

Regional Insights

North America Healthcare IT Market Trends

North America is expected to remain the dominant market for healthcare IT solutions, capturing approximately 38% of the total revenues in 2026. The growth of the market here is supported by widespread adoption of cloud platforms, telehealth, AI, and remote monitoring solutions. The U.S. government announced the Medicare ACCESS digital care payment trial, incentivizing providers to implement scalable remote monitoring and digital health tools for chronic care management. Extensive EHR penetration, broad telehealth reimbursement policies, and mature digital infrastructure encourage advanced analytics and patient engagement platforms. Provider and payer ecosystems are increasingly integrating clinical and administrative data for predictive insights. High R&D spending and venture capital investments continue to support innovation. These factors reinforce North America’s dominant market position.

Structural challenges are anticipated from cybersecurity threats and privacy concerns as digital networks expand. A White House initiative outlined a voluntary health data tracking system to integrate personal health data across applications, highlighting the need for robust governance and security frameworks. Compliance investments are expected to increase operational costs for providers. Regulatory complexity may slow some digital adoption, but ongoing policy support and the demand for value-based care models are likely to sustain long-term IT investments. Cloud, AI, telehealth, and remote monitoring solutions are projected to remain central to growth.

Europe Healthcare IT Market Trends

Europe is slated to command a considerable portion of the healthcare IT market value in 2026, driven by national programs in Germany, the U.K., France, and Spain that support digital health adoption. The EHDS came into effect, standardizing cross-border health data use and enabling secure access for providers, researchers, and policymakers. This regulation encourages investment in cloud and analytics platforms and strengthens interoperability. Germany’s digital patient record system reached mandatory upload requirements for clinicians, improving structured data flows across hospitals and clinics. Hospitals and large health systems are expanding digital infrastructure for population health management and clinical decision support. Telemedicine, mobile health, and AI-enabled analytics are increasingly integrated into care delivery. Coordinated national programs are enhancing digital transformation across member states.

Structural and operational challenges remain due to regulatory complexity and diverse healthcare funding landscapes. GDPR compliance continues to influence vendor strategy, particularly for cloud platforms and patient engagement solutions. Telemedicine and analytics deployments in the U.K. and France are strengthening chronic disease management and personalized care. Investments in AI diagnostics, remote monitoring, and interoperable health information exchange are accelerating adoption. Regional efforts to harmonize digital health standards support secure data exchange and cross-border care. Public-private collaborations and innovation in digital platforms continue to drive long-term growth. Europe’s market development reflects a balance between regulatory compliance and digital transformation momentum

Asia Pacific Healthcare IT Market Trends

Asia Pacific is projected to be the fastest?growing regional market for healthcare IT, forecasted to exhibit an estimated 18.2% CAGR from 2026 to 2033. Rapid digitization and large patient populations underpin this growth trajectory, supported by national initiatives in key markets such as China, India, and Japan. For example, India’s Ministry of Education launched an AI Centre of Excellence for Healthcare at IISc Bengaluru to develop scalable AI tools for disease detection and frontline decision support, signaling government commitment to digital health innovation. This effort enhances local AI competencies while driving demand for healthcare IT solutions that integrate predictive analytics, machine learning, and point?of?care support.

Across Southeast Asia and Oceania, countries are expanding cloud?based systems, telemedicine, and digital records to bridge urban–rural care gaps. Regional healthcare IT trends include enhanced use of AI for clinical decision support and intelligent workflow automation, with leaders in Australia and Malaysia emphasizing broader AI adoption in hospital operations and predictive health management. Variable regulatory maturity across markets presents both opportunities and challenges, but public?private partnerships and technology collaborations continue to accelerate digital transformation. These developments are expected to drive rapid healthcare IT adoption across hospitals, outpatient care, and community health services in Asia Pacific.

Competitive Landscape

The global healthcare IT market structure is moderately consolidated, with leading vendors such as Cerner, Epic Systems, Allscripts, Philips Healthcare, and GE Healthcare capturing a significant portion of revenue. These established players leverage extensive relationships with hospitals, health systems, and payers, combined with deep regulatory expertise and integrated software-hardware platforms. Heavy investment in R&D allows them to maintain leadership in cloud deployment, AI-enabled analytics, telehealth solutions, and cybersecurity infrastructure.

Regional and niche competitors, including Meditech, NextGen Healthcare, and athenahealth, are focusing on specialized software modules, ambulatory care solutions, and specific geographic markets. Regulatory compliance, complex system integration, and interoperability requirements present barriers to new entrants, though digital transformation and cloud adoption are enabling software-centric companies to participate through scalable IT solutions. Market consolidation is expected to grow gradually as global leaders pursue mergers and acquisitions to expand geographically and technologically, while smaller innovators form partnerships to integrate AI, analytics, and telemedicine capabilities into existing ecosystems.

Key Industry Developments

- In January 2026, Spring Health, a global digital behavioral health platform, announced it has agreed to acquire mental health software provider Alma in a deal expected to close in the second quarter of 2026, combining Spring’s AI?powered clinical tools with Alma’s practice management infrastructure to extend digital care access and continuity across providers and payers.

- In January 2026, Amazon One Medical introduced a new agentic Health AI assistant integrated into its mobile app in early 2026, providing 24/7 personalized healthcare support based on patients’ comprehensive medical records. This AI assistant can explain lab results, answer clinical queries, schedule appointments, manage medications, and connect patients seamlessly with providers.

- In December 2025, Google announced a US$?8?million funding commitment to support four government?backed Artificial Intelligence Centres of Excellence in India, with a specific focus on advancing AI research and innovation that includes healthcare applications such as disease treatment models and medical record digitization.

Companies Covered in Healthcare IT Market

- Epic Systems Corporation

- Cerner

- McKesson Corporation

- Athenahealth, Inc.

- Allscripts

- Philips Healthcare

- IBM

- Oracle Health

- SAP SE

- Optum, Inc.

- Accenture

- Hewlett Packard Enterprise

Frequently Asked Questions

The global healthcare IT market is projected to reach US$ 650.0 billion in 2026.

Rising adoption of EHR/EMR systems, telemedicine platforms, AI and cloud technologies, IoMT devices, and public health initiatives are driving market growth.

The market is poised to witness a CAGR of 15.2% from 2026 to 2033.

High-value opportunities are emerging in AI and telehealth expansion, cloud infrastructure deployment, and value-based care analytics.

Cerner, Epic Systems, Allscripts, Philips Healthcare, and GE Healthcare are among the key market players.