- Beauty & Personal Care

- Marker Pens Market

Marker Pens Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Marker Pens Market Analysis By Product Type (Permanent Markers, Whiteboard Markers, Highlighters, Paint Markers, Textile Markers, Water‑Based Markers, Specialty Markers), Ink Type (Alcohol‑Based Ink, Water‑Based Ink, Oil‑Based Ink, Pigment‑Based Ink, Dye‑Based Ink, Non‑Toxic Ink), End-use and Regional Analysis 2025 - 2032

Marker Pens Market Share and Trends Analysis

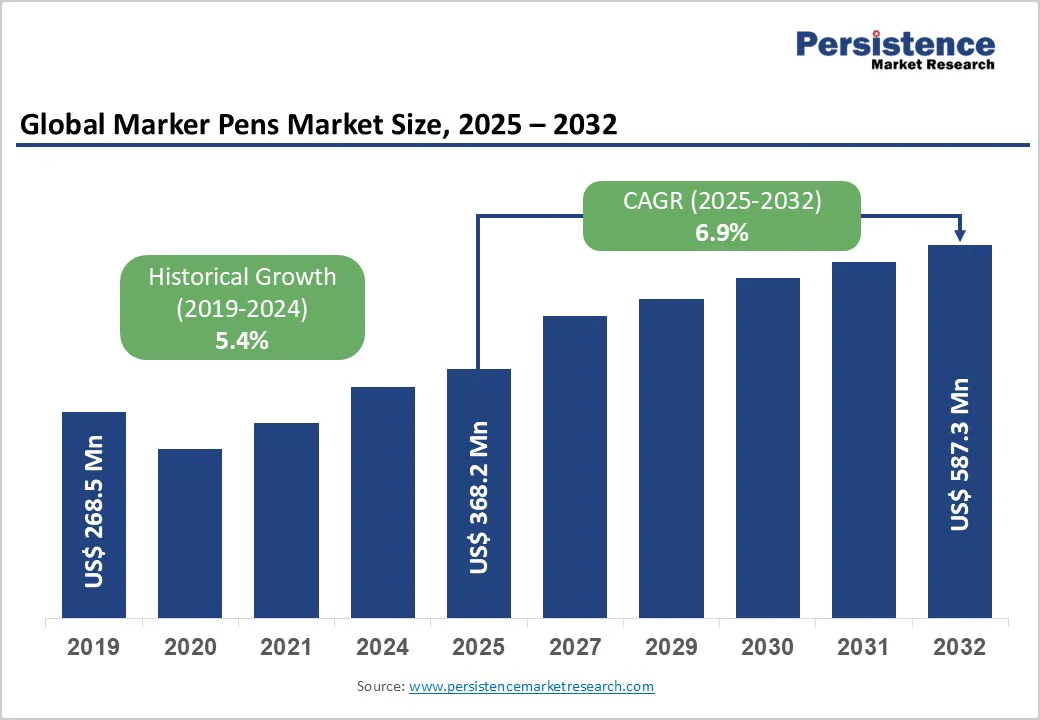

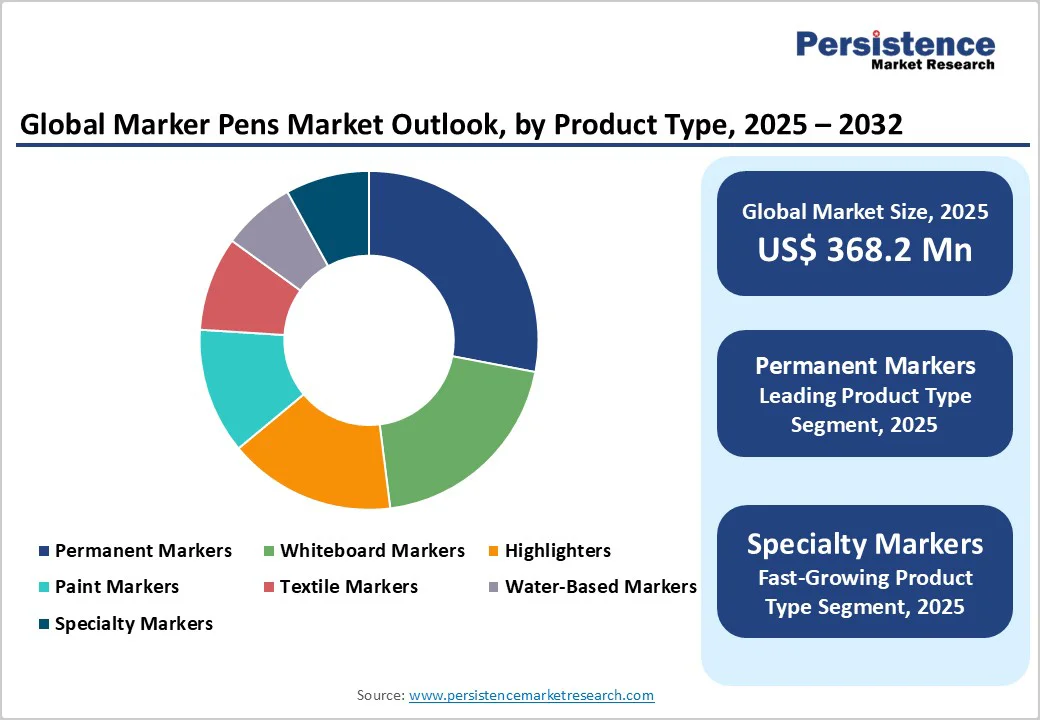

The global marker pens market size is likely to reach US$368.2 million in 2025 and is projected to reach US$587.3 million by 2032, growing at a CAGR of 6.9% between 2025 and 2032. The market is supported by sustained classroom and office adoption of whiteboards and highlighters, steady hobbyist and professional art demand, and product innovation in non-toxic, refillable, and low-odor inks that align with tightening safety and sustainability expectations in education and workplaces.

Key Market Highlights:

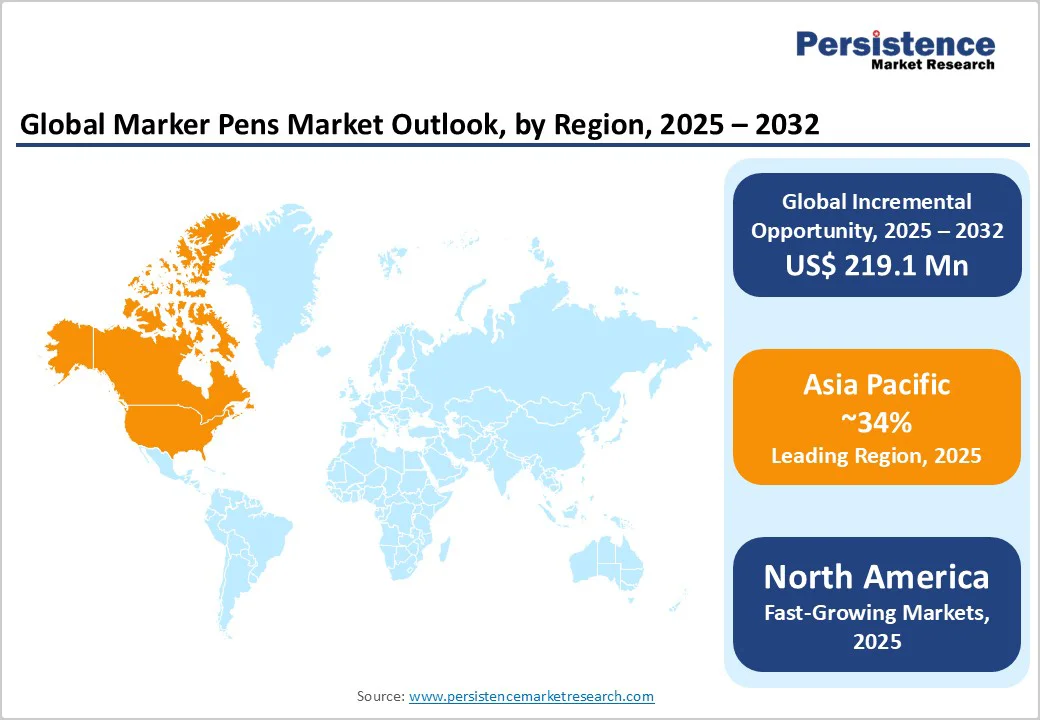

- Leading Region: Asia Pacific leads the marker pens market on volume share, supported by extensive education systems, manufacturing setups, and flourishing creative communities across China, India, Japan, Vietnam, and ASEAN.

- Fastest Growing Region: Asia Pacific grows fastest by value and volume, leveraging school expansions, rising discretionary spend, and e-commerce access to specialty and premium markets, alongside robust supply-side advantages.

- Dominant Segment: Permanent Markers dominate the product type with a 28% share, reflecting cross-surface labeling in homes, logistics, and maintenance, plus widespread packaging and back-room usage that ensure continual replenishment.

- Fastest Growing Segment: Specialty Markers (paint, textile, metallic) are among the fastest-growing by value, propelled by customization, creator economy trends, and industrial niche jobs demanding durable, high-impact inks.

- Key Market Opportunity: Sustainable, non-toxic, refillable marker systems aligned with school and corporate ESG procurement—supported by documented compliance and low-odor chemistry—offer multi-year contract potential and margin uplift.

| Key Insights | Details |

|---|---|

|

Global Marker Pens Market Size (2025E) |

US$368.2 million |

|

Market Value Forecast (2032F) |

US$587.3 million |

|

Projected Growth CAGR (2025–2032) |

6.9% |

|

Historical Market Growth (2019–2024) |

5.4% |

Market Dynamics

Driver - Digital-ready Classrooms and Collaborative Offices Sustain Whiteboard Ecosystems

Education and corporate collaboration remain pivotal for market usage. The academic teaching practices continue to rely on whiteboards and erasable markers for interactive instruction and brainstorming, despite the proliferation of digital tools. Adoption of interactive and hybrid classrooms boosted the use of dry-erase formats, with analyses showing that interactive boards and collaborative methods increase marker use in both schools and home-office settings.

In Europe, regulatory emphasis on low-odor and safer inks has pushed innovation in water-based and low-VOC products, which schools prefer, and corporations focus on indoor air quality and safety compliance. The rise of remote and hybrid work retained a baseline of in-home whiteboard use for planning, tutoring, and meetings, further buttressing demand. Together, these usage patterns underpin durable replacement cycles for whiteboard markers and highlighters across B2B and B2C channels, directly supporting the marker pens market.

Creativity Boom and Specialty Applications Expand the Addressable Base

Beyond classrooms, marker pens are deeply embedded in hobbyist art, graphic design, bullet journaling, labeling, and industrial identification. Industry coverage cites strong growth from arts and crafts communities and DIY culture, which favor vibrant colors, dual-tip formats, and alcohol-based precision markers for blending and illustration.

Specialty markers-such as paint, metallic, textile, and industrial-grade permanent options-address surfaces from plastic and metal to fabric and glass, opening incremental use cases in packaging, warehousing, and maintenance tasks. Major brands are responding with non-toxic and refillable lines, aligning with institutional procurement criteria and consumer ESG preferences. These trends broaden the Marker Pens Market beyond traditional stationery, stabilizing revenues with diversified end-use profiles across B2C and B2B.

Restraint - Digital Whiteboards and Content-sharing Reduce Analog Usage Intensity

The steady rollout of digital whiteboards and interactive flat panels offers feature sets-cloud saving, multi-user collaboration, integrated media-that analog boards cannot match, shifting certain presentation and teaching workflows away from traditional markers. While many classrooms operate in hybrid mode that retains whiteboard markers, the superior storage, annotation, and remote collaboration of digital displays can compress consumption per room over time, especially in well-funded districts and corporates. This substitution effect is most visible in mature markets with higher technology penetration and budgets.

Raw Material Volatility and Compliance Costs Pressure Margins

Ink solvents, pigments, and plastic casings expose manufacturers to commodity swings. At the same time, compliance with standards such as REACH, ASTM D-4236, low-odor/VOC limits, and eco-claims verification increases testing and formulation costs, particularly in the EU and North America. Environmental focus pushes suppliers toward recycled or bio-based plastics and water-based or low-odor inks, which can carry higher input costs during transition. Together, volatility and compliance raise working capital needs and pricing complexity, especially for value-tier SKUs serving school tenders and mass retail.

Opportunity - Sustainable and Refillable Marker Systems for Institutional Procurement

There is clear headroom for refillable bodies, replaceable nibs, recycled casings, and non-toxic or water-based inks that meet school and office sustainability mandates. Product pages and analyses emphasize growing lines of eco-friendly markers, low-odor formulations, and designs that reduce plastic waste while extending lifespan attributes increasingly required in tenders and ESG-screened purchasing.

Brands that document compliance and obtain recognized safety marks stand to win multi-year supply contracts in Europe and North America, and increasingly in urban school districts in Asia. Positioning refillable and recyclable ranges with total-cost-of-ownership (TCO) storytelling can capture higher-margin institutional business and strengthen the Marker Pens Market presence.

Premiumization in Art and Specialty Segments, Supported By Brand Collaborations

Growth in lettering, journaling, design visualization, and creative education favors high-chroma, blendable, dual-tip, and archival-quality pigment markers. Collaborations and lifestyle marketing, such as Zebra Pen’s 2025 multi-year partnership to embed writing instruments in milestone moments, amplify brand reach and create buzz among creators and students.

Heritage brands like Faber-Castell highlight craftsmanship and professional-grade attributes that appeal to both artists and gift buyers, strengthening premium price points. Targeted launches of paint markers, textile markers, and UV-visible or high-temperature variants for industrial and maker communities can capture fast-growing niches by differentiating.

Category-wise Insights

Product Type Analysis

Permanent Markers lead with an estimated share of about 28% of total marker consumption, driven by durable labeling across homes, logistics, warehousing, and maintenance, as well as adoption in packaging and retail back-room workflows. Their ability to write on plastic, metal, glass, and corrugated surfaces underpins broad utility compared with surface-restricted formats.

Whiteboard markers follow closely, sustained by classroom and office collaboration use cases that remain widespread despite digital tool adoption. Specialty formats—paint, textile, metallic—are among the faster-growing sub-groups by value as crafts, customization, and maker culture spread via social media tutorials and marketplace communities. This hierarchy reflects the Marker Pens Market’s dual consumer- and professional-oriented nature.

Ink Type Analysis

Alcohol-based Ink is the leading ink category with an estimated share of 35%, reflecting its fast-drying behavior, vivid pigmentation, and multi-surface adhesion prized by artists, designers, and industrial users for smudge-resistant results. Water-based and non-toxic inks are growing faster in education and office environments due to odor sensitivity and safety standards, supported by ongoing innovation in erasability and brightness.

Oil-based and pigment-based inks have resilient niches in paint markers, outdoor marking, and archival needs where water resistance and UV stability are critical. As institutions prioritize indoor air quality and sustainability, the shift toward low-odor, low-VOC formulations further reinforces water-based growth. At the same time, alcohol-based retains leadership in creative and industrial applications.

End-user Analysis

Educational Institutions hold the leading end-user share at approximately 32%, considering their continuous consumption of whiteboard markers, highlighters, and replacement cycles across primary, secondary, and tertiary institutions, as well as tutoring centers. Classroom activities, hybrid learning, and continual visual instruction keep per-pupil marker usage structurally high, especially in regions with expanding enrollment and modernized facilities.

Commercial/Corporate Buyers (B2B) contribute a substantial portion via meeting rooms, training labs, warehouses, and labeling tasks in offices and operations. Artists & Designers and Industrial Buyers represent smaller shares overall but command higher value per unit due to specialty inks, dual tips, and performance attributes that lift average selling prices.

Regional Insights

Asia Pacific Marker Pens Market Trends

Asia Pacific leads global volumes through expansive education systems, competitive manufacturing clusters, and fast-growing creative user bases. The regional writing instruments market is on a steady growth path, reflecting strong fundamentals for stationery and markers across Vietnam, China, Japan, and India. Local champions and global brands compete on value and innovation, with rising demand for alcohol-based art markers and specialty paint and textile markers among students and creators. Classroom expansions and vocational training further increase the consumption of whiteboard markers and highlighters in both public and private institutions.

Supply-side advantages-plastic molding, ink chemistry capabilities, and integrated packaging-enable rapid product refresh and competitive pricing. As urban consumers embrace journaling, calligraphy, and personalization, premium dual-tip and archival-pigment markers are seeing accelerating uptake across e-commerce and specialty retail channels. In sum, manufacturing advantages and broad education investment keep Asia Pacific at the forefront of the Marker Pens Market’s growth trajectory.

North America Marker Pens Market Trends

North America shows durable demand anchored in institutional procurement and strong brand equities. Whiteboard markers and highlighters remain in high demand in K-12 and higher education, even as districts deploy interactive displays, because hybrid classrooms still use physical whiteboards for engagement and flexibility. Corporate collaboration spaces and training programs similarly sustain B2B usage for dry-erase markers and flip-chart pads.

Brand-led marketing keeps marketers culturally visible: in April 2025, Zebra Pen Corp. announced a multi-year collaboration with OpenFortune to integrate pens into milestone moments, expanding consumer touchpoints through unique media channels.

A notable trend is the coexistence of digital whiteboards and analog markers. While interactive boards enable content saving and remote collaboration, many teams still value quick sketching and physical brainstorming with erasable markers for ideation sprints. In parallel, premium and non-toxic ranges witness procurement traction due to indoor air and safety standards in schools and offices. Together, these dynamics keep North America a high-value market emphasizing performance, low odor, and responsible materials.

Europe Marker Pens Market Trends

Europe emphasizes regulatory compliance, eco-design, and brand heritage. Market coverage underlines a strong pipeline of eco-friendly, low-odor, and refillable markers adopted by schools and enterprises aiming to reduce VOCs and plastic waste. This aligns with consumer preferences and tender requirements in the EU, favoring water-based and non-toxic formulations for education and office environments. Heritage brands such as Faber-Castell leverage craftsmanship messaging and innovation-e.g., lightfast inks and ergonomic designs showcased in broader pen categories to sustain premium price tiers that spill into the marker portfolio.

Regional performance is also supported by steady office demand and creative communities’ uptake of specialty markers. Manufacturers highlight compliance and quality credentials as differentiators in retail and B2B channels. The net effect is a value-oriented European Marker Pens Market, where sustainability narratives and product certifications are core to brand selection in Germany, the U.K., France, and Spain.

Competitive Landscape

The global marker pens market competition is moderately fragmented, with global leaders-BIC Group, Pilot Corporation, Pentel, Mitsubishi Pencil, Faber-Castell, Zebra Pen, Shachihata, and Edding competing alongside regional specialists. Leaders differentiate via breadth of portfolio (permanent, dry-erase, highlighter, paint), safe and non-toxic formulations, and sustainability features such as refillable designs and recycled casings. R&D focuses on low-odor chemistry, vivid pigments, quick-dry inks, dual-tip ergonomics, and nib durability for industrial surfaces. Emerging business models include collaboration-driven branding and creator-community marketing to accelerate adoption in art and journaling segments.

Key Market Developments:

- In 2025: Zebra Pen Corp. launches a multi-year partnership with OpenFortune to expand brand engagement across unique consumer touchpoints through integrated campaigns.

- In 2025: Faber-Castell amplify craftsmanship and ink performance narratives across writing portfolios, supporting premium price points applicable to specialty markers.

Companies Covered in Marker Pens Market

- Arro‑Mark Company L.L.C.

- Ballograf AB

- BIC Group

- DOMS

- Drimark

- Edding Group

- Faber‑Castell AG

- Kokuyo

- Mitsubishi Pencil Co., Ltd.

- Pentel Co., Ltd.

- Pilot Corporation

- Shachihata Inc.

- Sharpie

- Tombow Pencil Co., Ltd.

- Zebra Pen Corp.

Frequently Asked Questions

The marker pens market is likely to value at US$ 368.2 million in 2025 and is projected to reach US$ 587.3 million by 2032, at a 6.9% CAGR during 2025–2032.

Sustained use in education and offices for interactive learning and collaboration, plus growth in arts, journaling, and specialty labeling, supported by low‑odor, non‑toxic innovations and refillable designs in line with institutional procurement standards.

Permanent Markers lead with about 28% share due to cross‑surface utility in labeling, logistics, and maintenance, with broad household and industrial adoption supporting continual replenishment.

Asia Pacific leads on volume, supported by extensive education systems, retail expansion, and competitive manufacturing ecosystems across China, India, Japan, Vietnam, and ASEAN.

Eco‑friendly, non‑toxic, refillable markers and recycled casings tailored to school and corporate ESG criteria-documented compliance can secure multi‑year tenders and premium pricing.

Key companies include BIC Group, Pilot Corporation, Pentel Co., Ltd., Mitsubishi Pencil Co., Ltd., Faber‑Castell AG, Zebra Pen Corp., Shachihata Inc., Edding Group, Sharpie, among others.