- Healthcare Services

- Renal Biomarker Market

Renal Biomarker Market Size, Share and Growth Forecast, 2026 - 2033

Renal Biomarker Market by Testing Kit (Functional Biomarkers, Others), Diagnostic Techniques (Enzyme-Linked Immunosorbent Assay (ELISA), Others), and End-use (Hospitals, Diagnostic Laboratories, Others), and Regional Analysis for 2026 - 2033

Renal Biomarker Market Size and Trends Analysis

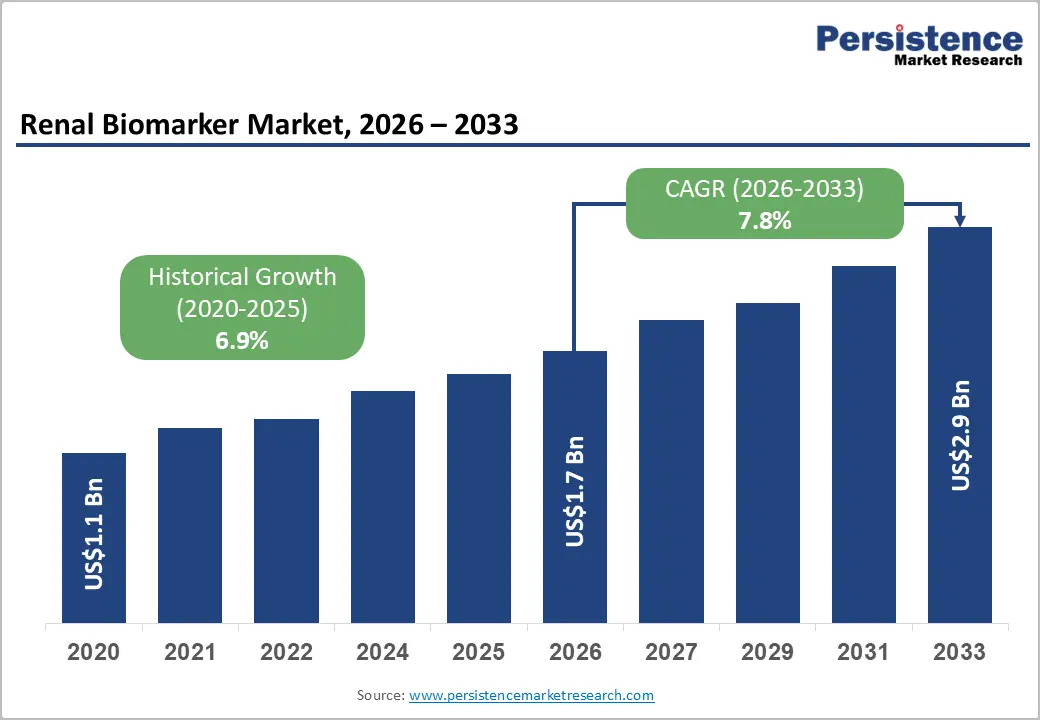

The global renal biomarker market size is likely to be valued at US$1.7 billion in 2026 and is projected to reach US$2.9 billion by 2033, growing at a CAGR of 7.8% during the forecast period from 2026 to 2033, driven by the rising prevalence of chronic kidney disease (CKD) and acute kidney injury (AKI), increasing demand for early and accurate diagnosis, and wider adoption of renal biomarker testing.

Healthcare providers are increasingly utilizing advanced kidney biomarkers to detect renal dysfunction earlier than conventional creatinine-based methods. Ongoing advancements in diagnostic biomarkers, expanding screening initiatives, and growing support for precision medicine are further driving market expansion across hospitals, diagnostic laboratories, and research institutions.

Key Industry Highlights:

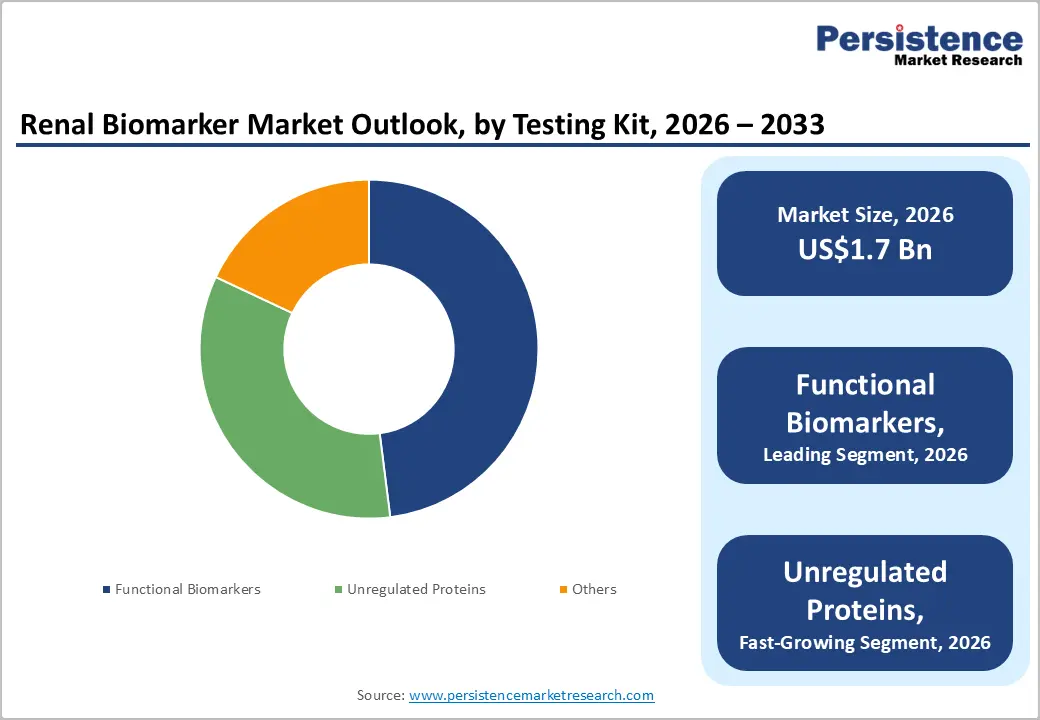

- Dominant Testing Kit Type: Functional biomarkers are expected to lead with an estimated 48% market share in 2026, while unregulated proteins are projected to be the fastest-growing segment through 2033, supported by expanding biomarker discovery and precision medicine applications.

- Leading Diagnostic Technique: ELISA is anticipated to dominate with approximately a 52% share in 2026, whereas PETIA is likely to be the fastest-growing diagnostic technique during 2026 - 2033, driven by increasing laboratory automation and demand for rapid testing.

- Dominant End-user: Hospitals are projected to account for around 46% of market revenue in 2026, while diagnostic laboratories are expected to register the fastest growth through 2033 due to rising outsourced testing volumes and screening programs.

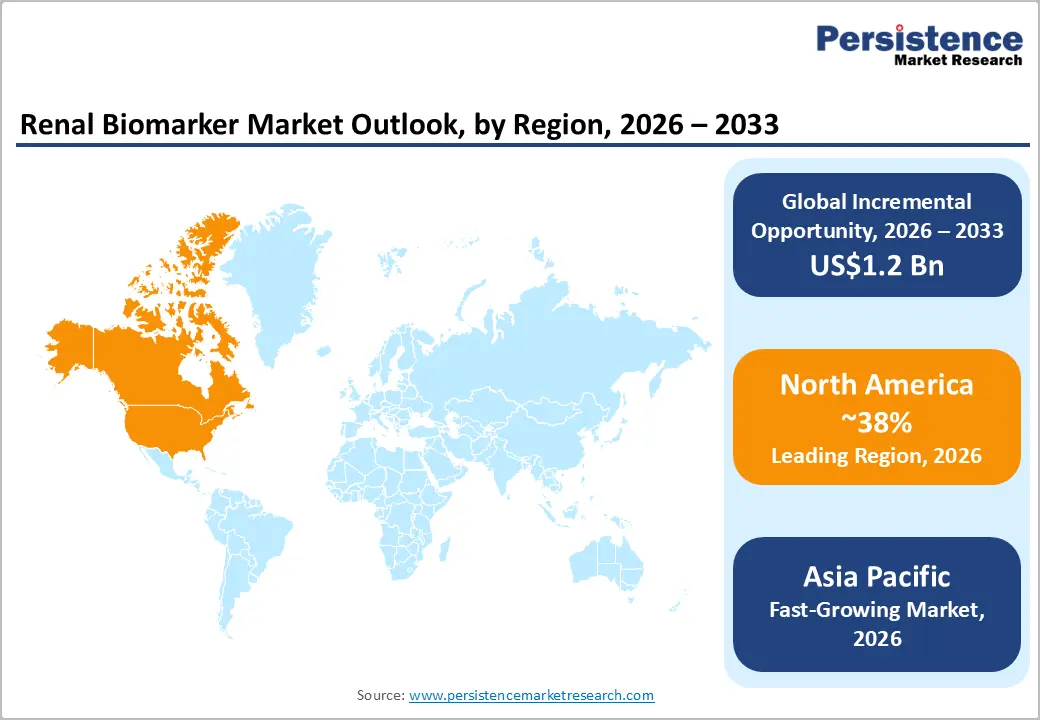

- Regional Leadership: North America is poised to lead with an estimated 38% market share in 2026, while Asia Pacific is expected to record the highest CAGR through 2033, supported by expanding healthcare access and growing kidney disease prevalence.

- Competitive Environment: Market participants are focusing on biomarker innovation, regulatory approvals, strategic partnerships, and geographic expansion, with recent developments centered on advanced kidney function diagnostics and AKI detection solutions.

DRO Analysis

Driver - Rising Global Burden of Chronic Kidney Disease and Acute Kidney Injury

The growing prevalence of chronic kidney disease remains the most influential factor driving demand for renal biomarkers. According to the International Society of Nephrology and the National Kidney Foundation, more than 850 million people worldwide are affected by kidney diseases, while CKD is among the fastest-growing causes of mortality globally. The WHO estimates that kidney disease-related deaths continue to increase due to aging populations, diabetes, hypertension, and obesity.

Traditional diagnostic methods often detect kidney damage only after significant functional decline. Consequently, healthcare providers are increasingly adopting kidney biomarkers such as NGAL, KIM-1, cystatin C, and L-FABP for earlier diagnosis and intervention. Early-stage detection can significantly reduce progression to end-stage renal disease, lowering dialysis and transplant costs. This clinical and economic value proposition is accelerating biomarker adoption across hospitals, nephrology centers, and diagnostic laboratories worldwide.

Restraint - High Validation Requirements and Limited Standardization across Biomarker Platforms

Despite significant clinical promise, the market faces challenges associated with biomarker validation, reimbursement variability, and lack of universal standardization. Regulatory agencies require extensive clinical evidence demonstrating diagnostic accuracy, reproducibility, and clinical utility before widespread adoption. Many emerging renal biomarkers remain under evaluation, creating barriers to commercialization and reimbursement approvals.

In addition, healthcare providers often rely on established kidney function indicators such as serum creatinine and estimated glomerular filtration rate (eGFR), slowing the transition toward newer biomarker technologies. Differences in assay methodologies, laboratory workflows, and reference ranges can further affect result consistency. These challenges increase development costs and prolong commercialization timelines for manufacturers. As a result, smaller diagnostic companies may face difficulties achieving broad market penetration, particularly in cost-sensitive healthcare systems and developing economies.

Opportunity - Expansion of Precision Medicine and Early Disease Screening Programs

The growing emphasis on preventive healthcare creates substantial opportunities for advanced renal biomarker testing. Governments and healthcare systems are increasingly implementing CKD screening initiatives to reduce long-term treatment expenditures associated with dialysis and kidney transplantation. Biomarker-driven diagnostics support precision medicine by enabling risk stratification, treatment monitoring, and personalized therapeutic interventions.

Emerging economies across Asia Pacific, Latin America, and the Middle East are investing heavily in diagnostic infrastructure, creating new revenue streams for biomarker manufacturers. Furthermore, artificial intelligence-assisted biomarker interpretation and multi-marker diagnostic panels are improving predictive accuracy for kidney disease progression. The integration of biomarkers into population-level screening programs, critical care settings, and pharmaceutical clinical trials is expected to significantly expand addressable market opportunities throughout the forecast period.

Category-wise Analysis

Testing Kit Insights

Functional biomarkers are expected to lead the testing kit segment with an estimated 48% market share in 2026. Their dominance reflects the growing clinical emphasis on early kidney disease detection, particularly as the International Society of Nephrology estimates that over 850 million people worldwide are affected by kidney diseases. Biomarkers such as NGAL and cystatin C can identify renal injury earlier than conventional creatinine-based tests, making them increasingly valuable in routine nephrology practice and acute care settings.

Unregulated proteins are projected to be the fastest-growing segment, recording a CAGR of over 8.5% through 2033. Growth is supported by expanding investments in proteomics and biomarker discovery programs aimed at identifying novel indicators of kidney injury. The increasing number of clinical studies evaluating protein-based biomarkers for risk stratification and disease progression monitoring is accelerating their transition from research environments to commercial diagnostic applications.

Diagnostic Techniques Insights

Enzyme-Linked Immunosorbent Assay (ELISA) is anticipated to account for approximately 52% of market revenue in 2026, making it the leading diagnostic technique. Its strong position stems from its high analytical sensitivity, cost-effectiveness, and widespread availability across clinical laboratories. ELISA remains one of the most commonly used immunoassay platforms globally, supporting large-scale testing of renal biomarkers in hospitals, diagnostic laboratories, and academic research institutions.

Particle-Enhanced Turbidimetric Immunoassay (PETIA) is expected to be the fastest-growing diagnostic technique, expanding at a CAGR of around 8.4% through 2033. The growth reflects increasing demand for automated testing solutions capable of handling rising diagnostic workloads. With healthcare systems facing growing CKD screening requirements, PETIA's compatibility with high-throughput analyzers and rapid result generation is driving adoption among centralized laboratory networks and large healthcare providers.

End-user Insights

Hospitals are projected to hold nearly 46% of the global market in 2026, positioning them as the leading end-user segment. The segment benefits from rising hospitalizations linked to chronic kidney disease, diabetes, and hypertension, which remain the primary risk factors for renal impairment. According to the CDC, more than 35 million adults in the United States have CKD, highlighting the significant diagnostic burden managed within hospital-based healthcare systems.

Diagnostic laboratories are expected to register the fastest growth, advancing at an estimated CAGR of 8.6% during the forecast period. Increasing adoption of outsourced testing models, coupled with growing preventive screening initiatives, is expanding laboratory testing volumes worldwide. Investments in automation, digital pathology integration, and advanced biomarker assay platforms are enabling diagnostic laboratories to deliver faster, more specialized renal testing services while meeting the rising demand for early disease detection.

Regional Analysis

North America Renal Biomarker Market Trends

North America is expected to account for approximately 38% of the global renal biomarker market in 2026, supported by the region's proactive response to the growing economic burden of kidney disease. According to the U.S. Medicare program, spending on CKD and end-stage kidney disease exceeds US$130 billion annually, encouraging healthcare systems to invest in earlier diagnosis and risk prediction tools. This cost-containment focus is accelerating the adoption of advanced renal biomarkers that can identify disease progression before irreversible kidney damage occurs.

U.S. Renal Biomarker Market Trends

The U.S. is projected to contribute around 86% of the North America market in 2026. The country continues to strengthen kidney disease management through initiatives such as the Advancing American Kidney Health program, which promotes earlier detection and improved patient outcomes. Additionally, the FDA approval of MediBeacon's Transdermal GFR System in 2025 reflects growing regulatory support for innovative technologies capable of enhancing kidney function assessment.

Canada Renal Biomarker Market Trends

Canada is estimated to hold nearly 14% of the regional market share in 2026. The country's response is being driven by increasing healthcare investments and a growing focus on chronic disease prevention. According to the Kidney Foundation of Canada, approximately 4 million Canadians are affected by kidney disease, creating demand for earlier diagnostic interventions. Expanding laboratory digitization and provincial healthcare modernization programs are further supporting biomarker adoption.

Europe Renal Biomarker Market Trends

Europe is anticipated to represent approximately 29% of the global market share in 2026, reflecting the region's strong emphasis on preventive healthcare and disease management. Kidney disease affects more than 100 million people across Europe, creating substantial pressure on healthcare systems to improve early diagnosis rates. As a result, healthcare providers are increasingly incorporating biomarker-based diagnostics into clinical pathways to reduce long-term treatment costs and improve patient outcomes.

Germany Renal Biomarker Market Trends

Germany is expected to account for roughly 31% of the Europe market share in 2026. The country benefits from one of Europe's highest healthcare expenditures, exceeding 12% of GDP, which supports widespread access to advanced diagnostic technologies. Strong investment in clinical research and laboratory automation has accelerated the integration of renal biomarkers into nephrology care, particularly for monitoring high-risk patient populations.

U.K. Renal Biomarker Market Trends

The U.K. is projected to capture around 18% of the regional market share in 2026. The NHS has increasingly prioritized early-stage disease detection as part of broader efforts to reduce avoidable hospitalizations associated with chronic conditions. The growing deployment of precision medicine programs and advanced diagnostic pathways is creating favorable conditions for renal biomarker adoption, particularly within community-based and outpatient care settings.

Asia Pacific Renal Biomarker Market Trends

Asia Pacific is expected to account for approximately 24% of global market revenue share in 2026 and remains the fastest-growing regional market through 2033. The region is responding to a rapidly expanding chronic disease burden, with diabetes prevalence projected to exceed 260 million cases by 2045, according to the International Diabetes Federation. Since diabetes remains a leading cause of kidney disease, governments are increasingly investing in screening and early diagnostic infrastructure to reduce future healthcare costs.

China Renal Biomarker Market Trends

China is estimated to contribute nearly 35% of the Asia Pacific market share in 2026. Healthcare reforms and increased public health expenditure have significantly expanded access to advanced diagnostic services across the country. The government's Healthy China 2030 strategy continues to emphasize early disease detection and chronic disease management, creating a favorable environment for the adoption of renal biomarker technologies.

India Renal Biomarker Market Trends

India is expected to account for approximately 16% of the regional market share in 2026. The country faces a growing kidney disease challenge, with studies indicating that CKD affects an estimated 10-15% of the adult population. In response, healthcare authorities and research organizations have expanded screening and awareness initiatives, including the 2025 ICMR-supported biomarker testing program in Andhra Pradesh, aimed at improving early identification of kidney disease in high-risk communities.

Competitive Landscape

The global renal biomarker market is moderately consolidated, with leading players such as Abbott Laboratories, Roche Diagnostics, Siemens Healthineers, and Danaher Corporation holding a significant share of market revenue. These companies benefit from strong diagnostic portfolios, established laboratory networks, and continuous investments in biomarker research, assay development, and automated testing platforms to strengthen their competitive positions.

Specialized companies such as BioPorto A/S, SphingoTec GmbH, and Randox Laboratories are expanding through innovative kidney injury biomarkers and precision diagnostic solutions. While stringent regulatory requirements and clinical validation standards remain key entry barriers, advances in proteomics and personalized medicine are creating opportunities for emerging players. Strategic partnerships, licensing agreements, and portfolio expansion initiatives are expected to drive gradual market consolidation over the forecast period.

Key Industry Developments:

- In May 2025, SphingoTec and Boditech Med launched the AFIAS penKid assay through a strategic commercialization partnership. The launch expanded global access to penKid-based kidney function diagnostics, enabling earlier detection of renal impairment in critical care settings and strengthening the adoption of novel renal biomarkers across hospital laboratories.

- In February 2025, Quest Diagnostics announced the acquisition of select Spectra Laboratories assets from Fresenius Medical Care. The transaction strengthened Quest's renal-specific diagnostic testing portfolio, expanded its nephrology laboratory capabilities, and enhanced support for kidney disease monitoring and dialysis-related testing services across the U.S. healthcare market.

Companies Covered in Renal Biomarker Market

- Abbott Laboratories

- Roche Diagnostics

- Siemens Healthineers

- Danaher Corporation

- Thermo Fisher Scientific

- BioPorto A/S

- Randox Laboratories

- Sysmex Corporation

- Bio-Rad Laboratories

- PerkinElmer/Revvity

- EKF Diagnostics

- SphingoTec GmbH

- Tosoh Corporation

- Becton Dickinson (BD)

- QuidelOrtho Corporation

Frequently Asked Questions

The global renal biomarker market is projected to reach US$1.7 billion in 2026.

Rising chronic kidney disease prevalence, growing demand for early diagnosis, and increasing adoption of precision diagnostics drive market growth.

The renal biomarker market is expected to grow at a CAGR of 7.8% from 2026 to 2033.

Opportunities lie in biomarker-based early disease detection, precision medicine adoption, and expanding diagnostic infrastructure in emerging markets.

Major players include Abbott Laboratories, Roche Diagnostics, Siemens Healthineers, and Danaher Corporation.