- Hardware & Software IT Services

- Manufacturing Operations Management Software Market

Manufacturing Operations Management Software Market Size, Share, and Growth Forecast, 2025 - 2032

Manufacturing Operations Management Software Market by Component (Software, Services), Enterprise (Large Enterprises, Small and Medium Enterprises), Application (Advanced Planning & Scheduling, Manufacturing Execution Systems (MES), Labor Management, Inventory Management, Quality Management, Laboratory Management, Others), End-use, and Regional Analysis for 2025 - 2032

Manufacturing Operations Management Software Market Size and Trend Analysis

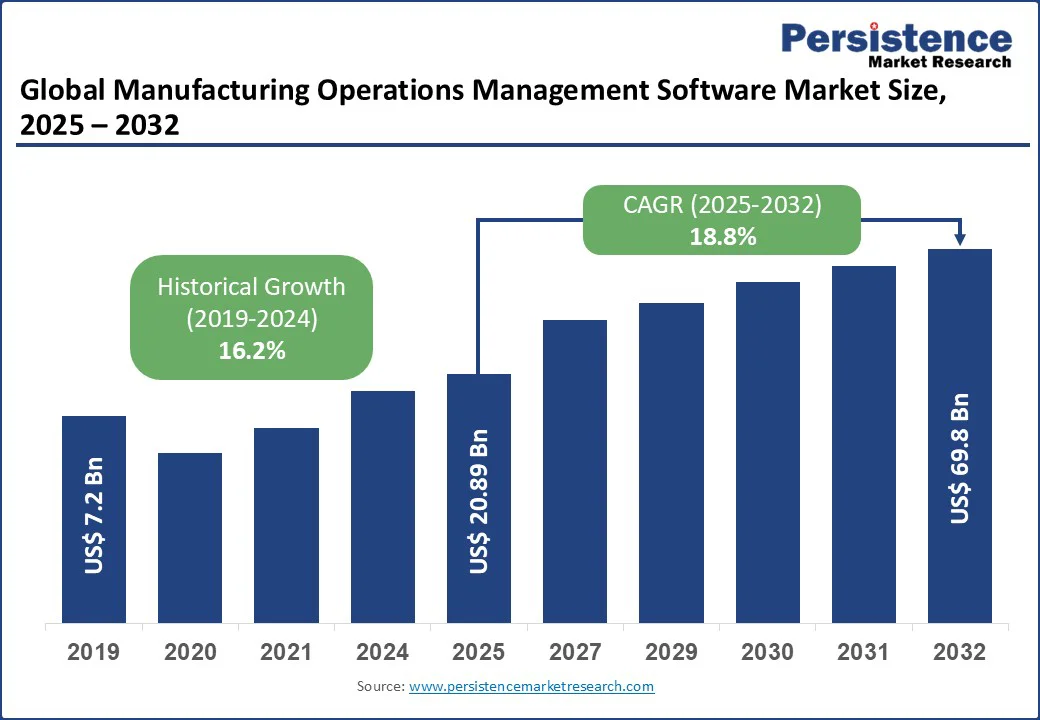

The global manufacturing operations management software market size is likely to value at US$20.89 Bn in 2025 and reach US$69.8 Bn by 2032, growing at a CAGR of 18.8% during the forecast period from 2025 to 2032.

The manufacturing operations management software market is witnessing robust growth, driven by increasing demand from industries such as automotive, pharmaceuticals, and aerospace, where efficient production planning, real-time monitoring, and quality control are critical.

Manufacturing operations management software, known for its integration capabilities, scalability, and data analytics features, is essential for optimizing workflows, reducing downtime, and enhancing supply chain visibility. The rise in global digital transformation initiatives, coupled with advancements in AI and IoT technologies, supports market expansion.

Key Industry Highlights:

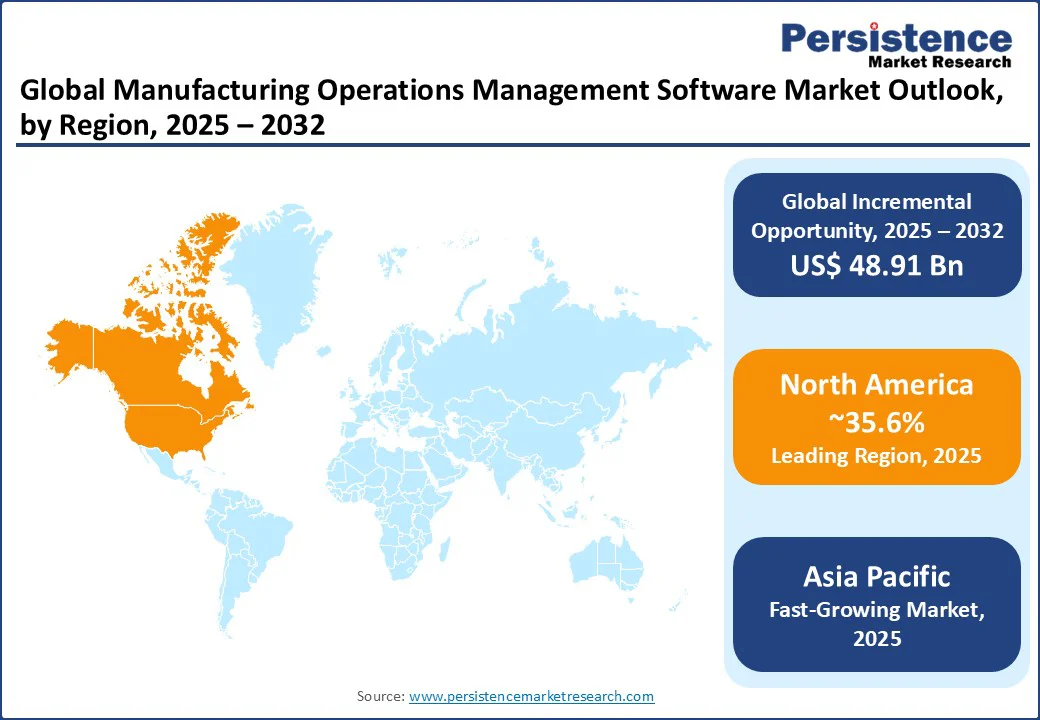

- Leading Region: North America holds 35.6% market share in 2025, driven by advanced technology infrastructure and strong manufacturing sectors in the U.S. and Canada, supported by investments in smart factories.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, propelled by rapid industrialization, manufacturing hubs, and high adoption of digital tools in countries such as China and India.

- Investment Plans: In May 2023, L&T Technology Services (LTTS) partnered with Critical Manufacturing to support Danfoss in implementing a next-generation Manufacturing Execution System (MES) as part of its Smart Manufacturing initiative. This collaboration aims to build a digital framework enhancing visibility, transparency, quality, IT/OT security, and time-to-market efficiencies.

- Dominant Component Type: Software, accounting for nearly 70.2% of the market share, due to its core functionality in process optimization and cost-efficiency for large-scale operations.

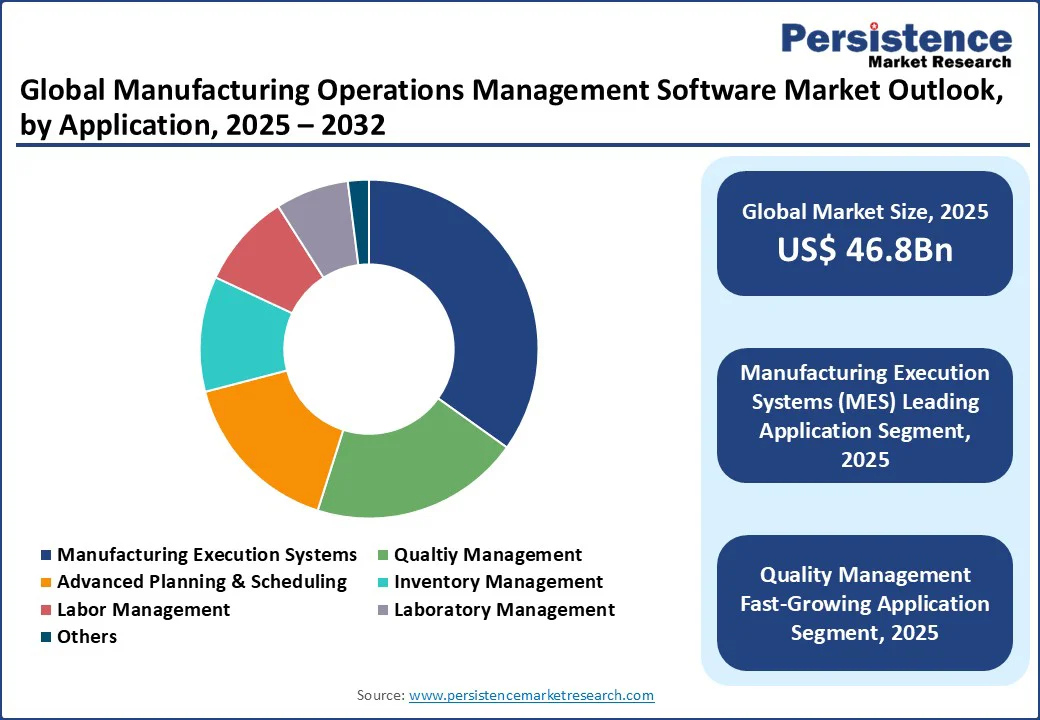

- Leading Application: Manufacturing Execution Systems (MES), contributing over 34.8% of market revenue, driven by the global push for real-time production tracking and efficiency improvements.

|

Global Market Attribute |

Key Insights |

|

Manufacturing Operations Management Software Market Size (2025E) |

US$ 20.89Bn |

|

Market Value Forecast (2032F) |

US$ 69.8Bn |

|

Projected Growth (CAGR 2025 to 2032) |

18.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

16.2% |

Market Dynamics

Driver: Increasing Adoption of Industry 4.0 and Digital Transformation in Manufacturing Fuels Market Expansion

The global manufacturing operations management software market is experiencing significant growth due to the surge in Industry 4.0 adoption and digital transformation initiatives worldwide. Manufacturing operations management software is critical for enabling smart factories through real-time data analytics, predictive maintenance, and seamless integration with IoT devices.

Programs such as Made in China 2025 and Digital India programs drive demand for software in automating production lines. According to NAM's Q2 2025 Manufacturers’ Outlook Survey, over 53% of manufacturers are focusing on digital transformation initiatives, further increasing the need for scalable operations management solutions.

Companies such as Siemens reported a revenue increase in MES software in 2024. Government-led policies and rising automation trends ensure sustained demand, positioning digital transformation as a key driver for market growth through 2032.

Restraint: High Implementation Costs and Integration Challenges with Legacy Systems

The manufacturing operations management software market faces challenges due to high initial implementation costs and difficulties in integrating with existing legacy systems. Software deployment requires substantial investments in hardware, training, and customization, impacting adoption rates. Additionally, compatibility issues with outdated infrastructure lead to prolonged downtime and data silos.

The manufacturing sector, particularly in emerging markets, faces a shortage of skilled professionals with expertise in digital technologies, data analytics, and MOM platforms. Recruiting and retaining such talent is challenging, especially when competing against tech-focused industries. Digitizing manufacturing processes exposes critical operational data and control systems to cyber threats. Legacy systems often lack modern security protocols, making integration with MOM software a potential vector for cyberattacks.

Opportunity: Rising Integration of AI and IoT in Manufacturing Processes

The increasing focus on AI and IoT technologies presents significant opportunities for the manufacturing operations management software market. These technologies enhance predictive analytics, machine learning for quality control, and real-time monitoring in smart manufacturing environments.

IDC's global AI spending forecast suggests that AI spending will grow at three times the rate of overall digital technology spending in the next three years, generating a global economic impact of over $6.4 trillion by the end of 2027, driving demand for integrated software platforms. In the automotive sector, AI-enabled software optimizes assembly lines and reduces defects.

Companies such as Rockwell Automation are innovating with AI-infused MES for efficient operations, aligning with sustainability goals. Government incentives, such as the U.S. CHIPS Act, further encourage investments in tech-driven manufacturing, creating opportunities for vendors to develop advanced, AI-powered manufacturing operations management software to meet evolving industry needs through 2032.

Category-wise Analysis

By Component

- Software holds the largest market share, approximately 70.2% in 2025, due to its essential role in core functionalities such as process automation, data analytics, and real-time monitoring. Widely adopted in large enterprises for enhancing operational efficiency and reducing production costs, software solutions are favored for their scalability and integration with emerging technologies such as AI and cloud computing. Companies such as SAP SE and Oracle lead with comprehensive portfolios, catering to demand in the automotive and pharmaceutical sectors across North America and the Asia Pacific.

- The emphasis on digital twins and predictive maintenance further bolsters software adoption, as manufacturers seek to minimize downtime and optimize resource utilization in competitive environments.

- Services is the fastest-growing component segment, driven by the need for customization, training, and ongoing support in complex implementations. Services include consulting, integration, and maintenance, making them ideal for SMEs transitioning to digital operations. Their adoption is rising in dynamic industries such as food and beverages, with providers such as Schneider Electric expanding offerings in Europe and the Asia Pacific, supported by growing demand for tailored solutions that address specific operational challenges. As manufacturing becomes more interconnected, services ensure seamless software deployment and long-term value, helping businesses navigate regulatory compliance and technological upgrades effectively.

By Enterprise

- Large Enterprises hold the largest market share, approximately 65.4% in 2025, due to their extensive resources for investing in advanced software to manage complex, global operations. These entities benefit from comprehensive solutions that integrate across multiple facilities, enabling centralized control and data-driven decision-making. Companies such as Siemens and Honeywell International Inc. dominate with enterprise-grade platforms, addressing needs in the aerospace and chemicals sectors in North America and Europe. The focus on scalability and compliance with international standards drives adoption, as large firms leverage software to enhance supply chain resilience and achieve cost efficiencies in high-volume production environments.

- Small and Medium Enterprises (SMEs) are the fastest-growing enterprise segment, propelled by affordable cloud-based solutions and government incentives for digital adoption. SMEs are increasingly utilizing user-friendly software to compete with larger players, focusing on inventory and quality management. Providers such as Epicor Software Corporation are tailoring offerings for agile operations in consumer goods and medical equipment industries, particularly in the Asia Pacific and Latin America. This growth is supported by the rise of subscription models, reducing upfront costs and enabling SMEs to improve productivity and respond quickly to market changes.

By Application

- Manufacturing Execution Systems (MES) holds the largest market share, approximately 34.8% in 2025, due to its critical function in real-time production tracking, workflow orchestration, and performance optimization. Widely used in automotive and pharmaceuticals for ensuring compliance and reducing errors, MES solutions are favored for their ability to bridge planning and execution. Leading vendors such as Rockwell Automation and AVEVA Solutions Limited offer robust systems, serving infrastructure-heavy sectors in the Asia Pacific and North America. The integration with ERP systems further enhances MES appeal, as manufacturers prioritize visibility and efficiency in increasingly automated facilities.

- Quality Management is the fastest-growing application segment, driven by stringent regulatory requirements and the push for zero-defect manufacturing. It enables defect detection, compliance tracking, and continuous improvement, ideal for pharmaceuticals and food, and beverages. Companies such as Aspen Technology Inc. are advancing AI-driven quality tools for precise analytics in Europe and the Middle East. Growth is fueled by global standards such as ISO 9001, encouraging adoption to minimize recalls and boost customer satisfaction in competitive markets.

By End-use

- Automotive holds the largest market share, approximately 25.6% in 2025, driven by the need for precision in assembly lines, supply chain management, and just-in-time production. Manufacturing operations management software is critical for optimizing production schedules and supporting robotic systems in vehicle manufacturing. Major players such as Dassault Systèmes supply specialized software for projects in the U.S. and Germany, where investments in electric vehicle production fuel demand.

- Pharmaceuticals are the fastest-growing end-use segment, propelled by rising regulatory compliance and demand for traceability in drug manufacturing. Software aids in batch management and quality assurance, with companies such as Oracle innovating for high-precision applications. Growth in the Asia Pacific and Europe, driven by biotech expansions, supports this segment’s rapid expansion.

Regional Insights

North America Manufacturing Operations Management Software Market Trends

North America dominates the manufacturing operations management software market, accounting for 35.6%, driven by advanced technology infrastructure and strong demand from automotive and aerospace sectors in the U.S. and Canada, supported by investments in smart factories. The U.S. manufacturing industry relies heavily on software for automation and analytics.

Canada’s tech sector drives demand for scalable solutions, per Innovation, Science and Economic Development Canada. Major players such as GE Vernova and Honeywell International Inc. dominate with extensive networks, catering to projects such as EV manufacturing and high-tech assembly. Consumer preference for AI-integrated software further strengthens North America’s market position.

Asia Pacific Manufacturing Operations Management Software Market Trends

The Asia Pacific is the fastest-growing region, fueled by rapid industrialization, manufacturing hubs, and high adoption of digital tools in countries such as China and India. China, the world’s largest manufacturing economy, contributes significantly to global output, according to the United Nations Industrial Development Organization, driving the availability of affordable software solutions.

India’s Make in India initiative boosts demand for operations management in automotive and consumer goods. The region’s pharmaceuticals and chemicals industries also contribute, with companies such as ABB and Siemens expanding their presence. Rising e-commerce and government-led digital projects ensures Asia Pacific’s rapid market growth through 2032.

Europe Manufacturing Operations Management Software Market Trends

Europe is the second fastest-growing region for the manufacturing operations management software market, driven by stringent regulations, rising demand in automotive and pharmaceuticals, and digital initiatives in countries such as Germany and France. The European manufacturing industry supports demand for software in process optimization and sustainability applications.

Germany’s Industry 4.0 initiative, a key driver for advanced systems, benefits from players such as SAP SE and Schneider Electric. The EU’s Digital Decade promotes tech adoption in the chemicals and food sectors, increasing demand for compliant software. Europe’s focus on innovation and green manufacturing drives market growth, with companies adapting to meet regulatory and consumer demands.

Competitive Landscape

The global manufacturing operations management software market is highly competitive, characterized by extensive product portfolios and global distribution networks. The Manufacturing Operations Management Software market is fragmented due to the presence of numerous domestic and international players, ranging from large, established companies to smaller, regional vendors.

Regional players such as Aegis Industrial Software Corporation focus on localized offerings in the Asia Pacific. Companies are investing in AI-driven features and cloud-based platforms to enhance market share, driven by demand for efficient solutions in the automotive and pharmaceutical sectors.

Key Industry Developments:

- April 2025: Aegis Software announced that HEITEC's Elektronik division, based in Eckental, Germany, is expanding its use of the FactoryLogix Manufacturing Execution System (MES) platform. Building upon the success of its initial implementation in 2021, HEITEC is scaling its FactoryLogix deployment to additional products, aiming to enhance production efficiency, automation, and data-driven decision-making.

- April 2025: iBase-t, a global leader in cloud software for the aerospace and defense industry, announced a strategic partnership with Articul8, a pioneer in enterprise Generative AI (GenAI) platforms. This collaboration aims to integrate Articul8's advanced GenAI capabilities into iBase-t's Solumina Manufacturing Operations Platform, enhancing operational efficiency in aerospace and defense manufacturing.

Companies Covered in Manufacturing Operations Management Software Market

- ABB

- Aegis Industrial Software Corporation

- Aspen Technology Inc.

- AVEVA Solutions Limited

- Dassault Systemes

- DURR Group

- Epicor Software Corporation

- GE Vernova

- Honeywell International Inc.

- iBase-t

- Oracle

- Rockwell Automation

- SAP SE

- Schneider Electric

- Siemens

- Amway

- Others

Frequently Asked Questions

The Manufacturing Operations Management Software market is projected to reach US$20.89 Bn in 2025.

Increasing adoption of Industry 4.0 and digital transformation, and expanding applications in AI-integrated processes are the key market drivers.

The Manufacturing Operations Management Software market is poised to witness a CAGR of 18.8% from 2025 to 2032.

The rising integration of AI and IoT in manufacturing processes is the key market opportunity.

ABB, Siemens, SAP SE, and Rockwell Automation are key market players of the Manufacturing Operations Management Software Market.