- Biotechnology

- Biologics Contract Manufacturing Market

Biologics Contract Manufacturing Market Size, Share, and Growth Forecast 2026 - 2033

Biologics Contract Manufacturing Market by Product (Monoclonal Antibodies, Recombinant Proteins, Vaccines, Insulin, Interferons, Growth Factors, Others), by Therapeutic Area (Oncology, Autoimmune Disease, Metabolic Disease, Ophthalmology, Cardiovascular Disease, Infectious Disease, Neurology, Respiratory Disorder, Others), by Application (Hybrid Electric Vehicles, Consumer Electronics, Medical Devices, Industrial Equipment, Power Tools, Emergency Lighting & Backup Power), by End User (Pharmaceutical Companies, Biotechnology Companies, Academic & Research Institutes/CROs, Others), by Regional Analysis, 2026-2033

Biologics Contract Manufacturing Market Size and Trend Analysis

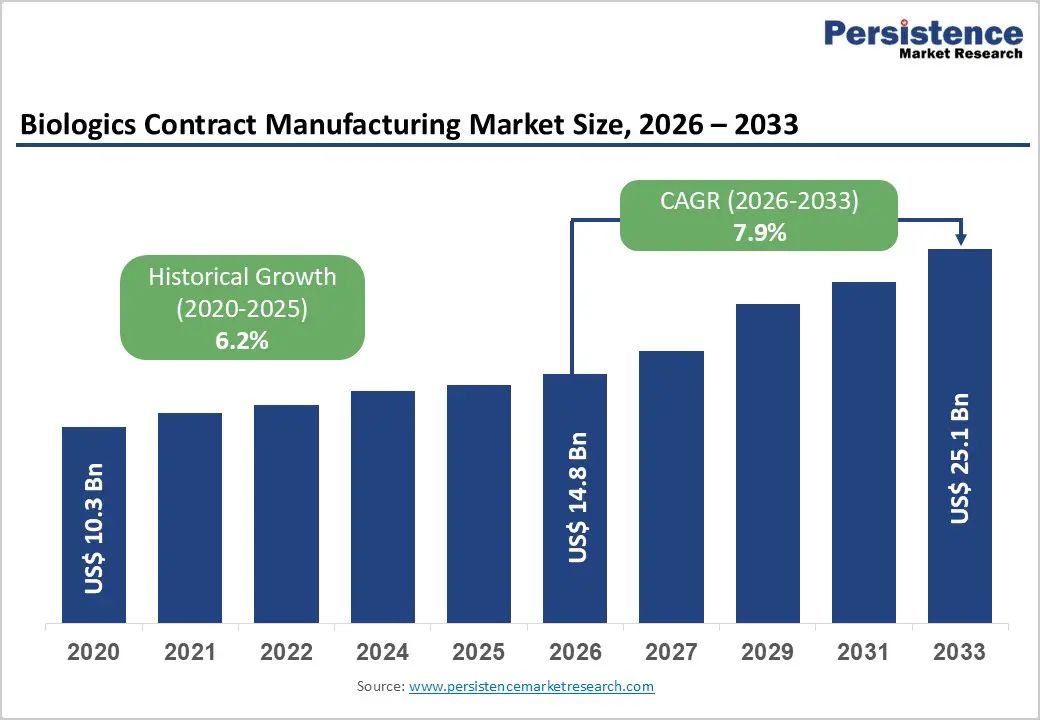

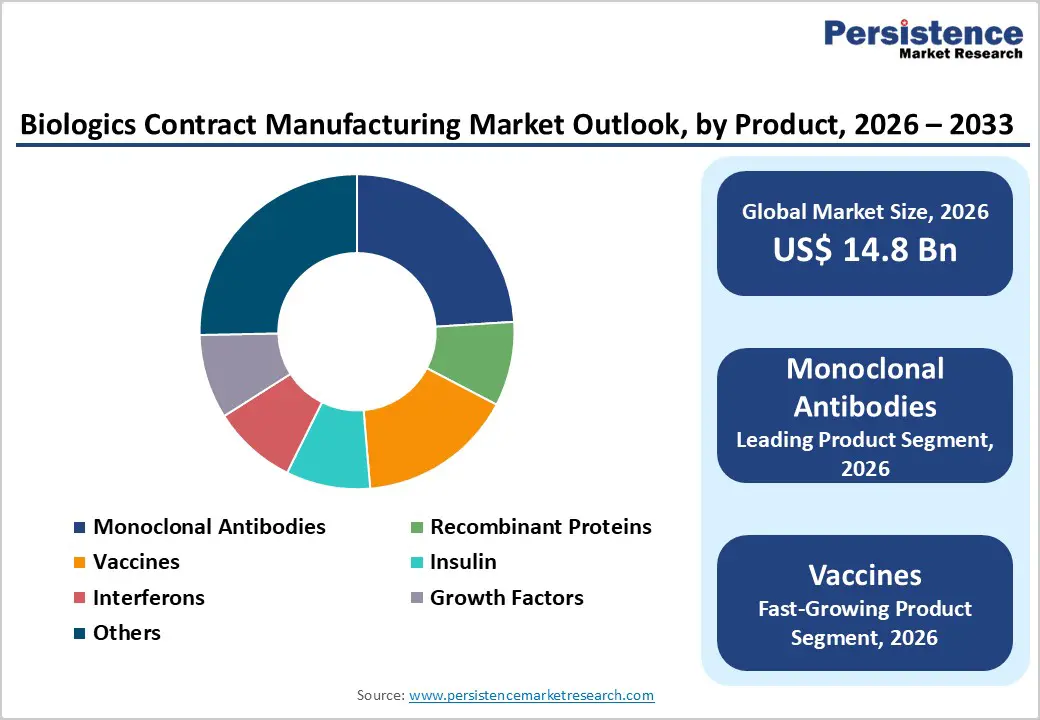

The global biologics contract manufacturing market size is expected to be valued at US$ 14.8 billion in 2026 and projected to reach US$ 25.1 billion by 2033, growing at a CAGR of 7.9% between 2026 and 2033.

The biologics contract manufacturing market is experiencing robust expansion driven by three critical factors: the exponential growth in demand for complex biologic therapeutics including monoclonal antibodies (mAbs), recombinant proteins, and cell and gene therapies, coupled with the strategic shift by biopharmaceutical companies toward outsourcing manufacturing operations to specialized Contract Development and Manufacturing Organizations (CDMOs) for cost efficiency and technical expertise. The FDA approved a record 50 novel drugs in 2024, with 16 being biologics, including the highest number of monoclonal antibodies since 2015, demonstrating the accelerating pipeline of biologic therapeutics that require external manufacturing capacity. Additionally, the implementation of advanced manufacturing technologies including single-use systems, continuous bioprocessing, and automation platforms has enhanced production efficiency and reduced contamination risks, making outsourcing increasingly attractive to pharmaceutical companies seeking to manage capital expenditure while maintaining regulatory compliance.

Key Market Highlights

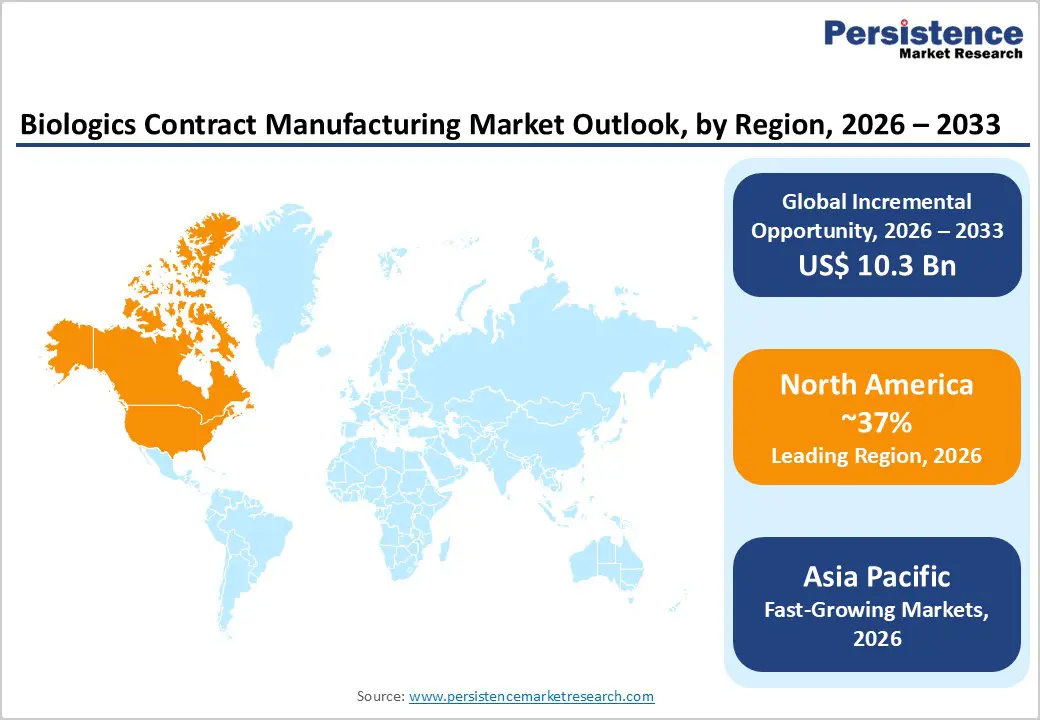

- North America maintains leadership with 37% market share in 2025, driven by regulatory expertise, biopharmaceutical innovation ecosystem, and proximity to major pharmaceutical company headquarters, establishing the region as the preferred manufacturing destination for innovative biologic therapies requiring FDA approval and commercialization support.

- Asia-Pacific emerges as fastest-growing region with projected CAGR exceeding 13% through 2030, fueled by government-supported biopharmaceutical initiatives including China's Healthy China 2030 program, India's cost-competitive manufacturing hub development, and South Korea's advanced manufacturing infrastructure investments.

- Monoclonal Antibodies dominate product segment with 24% market share in 2025, driven by FDA approval of 13 mAbs in 2024 (highest since 2015), expanding therapeutic applications across oncology, autoimmune diseases, and infectious diseases, with global mAb market projected to exceed US$ 823 billion by 2034.

- Oncology represents fastest-growing therapeutic area, with pharmaceutical companies prioritizing development and manufacturing of bispecific antibodies, checkpoint inhibitors, and antibody-drug conjugates, supported by aging global population, increasing cancer incidence exceeding 20 million new cases annually, and efficacy of targeted cancer immunotherapies.

| Global Market Attributes | Key Insights |

|---|---|

| Market Size (2026E) | US$ 14.8 billion |

| Market Value Forecast (2033F) | US$ 25.1 billion |

| Projected Growth CAGR (2026-2033) | 7.9% |

| Historical Market Growth (2020-2025) | 6.2% |

Market Dynamics

Market Growth Drivers

Escalating Pipeline of Biologic Drug Approvals and Complex Therapeutics Manufacturing Requirements

The biopharmaceutical industry has witnessed a fundamental paradigm shift from small-molecule drugs toward complex biologic therapeutics, creating unprecedented demand for specialized manufacturing capabilities. The FDA's approval of 16 biologics in 2024 and the projected continued expansion of biologic pipelines across multiple therapeutic modalities including monoclonal antibodies, bispecific antibodies, cell and gene therapies, and biosimilars have created significant capacity constraints for traditional manufacturing infrastructure. According to industry data, more than 305 contract manufacturing organizations (CMOs) are now engaged in biologics production, with over 90% providing finished dosage form (FDF) manufacturing services. The manufacturing of therapeutics at metric ton scale has become necessary to address global healthcare demands, particularly evident during the COVID-19 pandemic when the global monoclonal antibody manufacturing capacity proved insufficient to meet pandemic response requirements. This supply-demand imbalance has incentivized pharmaceutical and biotechnology companies to engage external manufacturing partners, establishing long-term strategic collaborations with specialized CDMOs to ensure consistent and scalable production without significant capital investment in dedicated facilities.

Strategic Cost Management and Operational Efficiency Through Outsourcing Models

Biopharmaceutical companies are increasingly recognizing outsourcing to CDMOs as a strategic imperative for cost containment and operational flexibility, driving robust market growth. Biologics manufacturing requires substantial capital investment in specialized infrastructure, including GMP (Good Manufacturing Practice) certified facilities, sophisticated bioreactor systems, and skilled technical personnel investments that often exceed the financial capacity of emerging biotechnology companies. The outsourcing model enables pharmaceutical companies to achieve 11% average growth in outsourcing budgets in 2025, up from 8.5% in 2024, reflecting renewed confidence in CDMO partnerships. By leveraging external manufacturing expertise, companies can reduce infrastructure costs by up to 40-50%, eliminate long facility construction timelines ranging from 3-5 years, and allocate capital toward research and development activities. This cost-efficiency advantage is particularly compelling for small and mid-sized biotechnology firms that lack internal manufacturing capacity, allowing them to accelerate product commercialization timelines and bring novel therapeutics to market faster than competitors with internal manufacturing constraints.

Market Restraints

Stringent Regulatory Frameworks and Compliance Complexities Across Jurisdictions

The biologics manufacturing sector operates under increasingly stringent regulatory requirements imposed by global health authorities including the FDA, European Medicines Agency (EMA), ICH (International Council for Harmonisation), and regional regulatory bodies, creating substantial barriers to market growth. Biologic drugs require adherence to complex current Good Manufacturing Practice (cGMP) standards, comprehensive analytical testing protocols, and rigorous quality control procedures that demand specialized expertise and infrastructure investments. The regulatory harmonization process remains incomplete across different geographic regions, forcing CDMOs to maintain multiple compliance frameworks simultaneously, increasing operational complexity and costs. Manufacturing facilities must undergo extensive regulatory inspections, validation studies, and documentation requirements that extend facility commissioning timelines by 6-12 months and increase capital expenditure by approximately 15-20%. Additionally, changes in regulatory guidelines, such as the FDA's evolving requirements for Advanced Therapy Medicinal Products (ATMPs), necessitate continuous investment in facility upgrades and staff training, creating ongoing operational burdens that particularly disadvantage smaller CDMOs with limited resources.

Intellectual Property Protection Concerns and Technology Transfer Risks

The outsourcing of biologics manufacturing introduces significant intellectual property (IP) and proprietary knowledge transfer risks that act as a major market restraint, particularly for biopharmaceutical companies headquartered in regions with geopolitical tensions or uncertain IP enforcement mechanisms. Pharmaceutical companies must disclose proprietary manufacturing processes, cell line technologies, and formulation secrets to contract manufacturers, creating vulnerability to technology misappropriation and competitive intelligence leakage. In certain geographic regions, concerns regarding IP protection adequacy and enforceability remain elevated, deterring multinational pharmaceutical companies from establishing manufacturing partnerships with local CDMOs. The complex negotiations surrounding confidentiality agreements, technology transfer agreements, and exclusive manufacturing rights increase partnership development timelines by 4-8 months, delaying time-to-market and reducing the attractiveness of outsourcing partnerships. Furthermore, the risk of contract manufacturers utilizing proprietary information to serve competing clients or establish competing product lines creates disincentives for technology sharing, particularly for blockbuster biologic products with significant commercial value.

Market Opportunities

Geographic Expansion and Capacity Development in the Asia-Pacific Region as High-Growth Opportunity

The Asia-Pacific biologics contract manufacturing market, currently valued at approximately US$ 4.5 billion in 2023 with projected CAGR of 13.3% through 2030, presents substantial growth opportunities driven by government initiatives, cost advantages, and expanding manufacturing infrastructure. China's government-supported "Healthy China 2030" initiative has incentivized investment in biopharmaceutical manufacturing infrastructure, with the country now hosting more than 400 biologics manufacturing sites and leading monoclonal antibody technologies. India has emerged as a major hub for cost-effective biologics manufacturing, leveraging lower production costs (approximately 40-50% lower than Western manufacturing), skilled technical workforce, and advanced capabilities in biosimilar production and recombinant protein manufacturing.

Category-wise Insights

Product Analysis

Therapeutic Area Analysis

Oncology: Leading Therapeutic Application Driving CDMO Capacity Expansion

Oncology represents the leading therapeutic area for biologics contract manufacturing, driven by the escalating prevalence of cancer globally and the pharmaceutical industry's commitment to developing novel targeted cancer therapies including monoclonal antibodies, bispecific antibodies, cell therapies, and antibody-drug conjugates. The FDA's 2024 biologic approvals included 6 monoclonal antibodies specifically indicated for oncology applications, continuing a multi-year trend of accelerating cancer drug approvals and expanding the biologic pipeline. The therapeutic efficacy of checkpoint inhibitor antibodies, HER2-targeting antibodies, and bispecific T-cell engager antibodies has revolutionized cancer treatment paradigms, creating sustained demand for manufacturing capacity. CDMOs specializing in oncology biologic manufacturing command premium pricing for their services due to the specialized expertise required for handling potent and potentially immunogenic therapeutic proteins, regulatory expertise in oncology product development, and the ability to scale manufacturing for blockbuster cancer medications that generate peak annual sales exceeding US$ 1 billion. The aging global population, combined with increasing cancer incidence projected to exceed 20 million new cases annually by 2030, ensures continued robust demand for oncology biologics and associated manufacturing services through the forecast period.

End User Analysis

Pharmaceutical Companies: Market Leadership and Strategic CDMO Partnerships

Large pharmaceutical companies represent the largest end-user category within biologics contract manufacturing, commanding the majority of manufacturing capacity and contract value, as these organizations increasingly adopt outsourcing strategies for non-core manufacturing operations. Pharmaceutical companies are leveraging CDMO partnerships to maintain competitive advantage in an environment characterized by patent expirations on blockbuster small-molecule drugs and the need to establish pipelines of innovative biologic therapeutics. Data indicates that more than 215 major pharmaceutical company initiatives are underway for partnerships and manufacturing expansions, with these collaborations representing more than 80% of all strategic initiatives undertaken by large pharma organizations. Samsung Biologics has established partnerships with 17 of the world's top 20 pharmaceutical companies, demonstrating the strategic importance of CDMO relationships in global pharmaceutical supply chains. The strategic preference for outsourcing manufacturing enables large pharmaceutical companies to avoid infrastructure bottlenecks during peak commercial production periods, manage supply chain diversification across multiple geographic locations, and allocate capital toward research and development activities with higher return on investment.

Regional Insights

North America Biologics Contract Manufacturing Market Trends and Insights

North America maintains the largest market share with 37% market share in 2025, driven by the region's dominance in biopharmaceutical research, development, and commercial manufacturing infrastructure. The United States hosts the highest concentration of biopharmaceutical companies globally, with over 1,400 biotechnology firms and established contract manufacturing infrastructure supporting drug development across all phases of clinical trials. The FDA approval process remains the global gold standard for biologic drug authorization, incentivizing pharmaceutical companies worldwide to establish manufacturing partnerships with CDMOs located in the United States to ensure regulatory compliance and facilitate market access. North America has maintained leadership in the number of biologic drug approvals, with the FDA approving 16 biologics in 2024 and maintaining an average approval rate of 5.6 biologic therapies annually, establishing sustained demand for clinical and commercial manufacturing capacity.

Asia Pacific Biologics Contract Manufacturing Market Trends and Insights

Asia-Pacific represents the fastest-growing geographic region for biologics contract manufacturing, with projected CAGR exceeding 13% through 2030, driven by government-supported biopharmaceutical initiatives, substantially lower manufacturing costs, and rapidly expanding manufacturing capacity. China's biopharmaceutical market is projected to grow at a CAGR of 9.5% through 2033, with the country now hosting more than 400 biologics manufacturing sites and establishing itself as a global manufacturing hub for monoclonal antibodies, biosimilars, and recombinant proteins. Domestic companies including WuXi Biologics, have expanded beyond China to establish international manufacturing networks, with over 281 First-in-Class projects in development, demonstrating China's growing innovation capacity and manufacturing excellence.

India has emerged as the fastest-growing biologics manufacturing destination within Asia-Pacific, leveraging cost advantages of 40-50% relative to Western manufacturing, skilled scientific workforce, and established regulatory compliance infrastructure aligned with ICH guidelines. Indian CDMOs including Aragen are establishing new GMP-certified biologics manufacturing facilities equipped with single-use bioreactor systems (2,000-liter capacity) and integrated downstream processing capabilities, positioning the country as a competitive hub for global biologics manufacturing. South Korea, through companies including Samsung Biologics, has become a major player in the biopharmaceutical contract manufacturing landscape, securing record-breaking contracts worth US$ 3.3 billion in 2024 and maintaining the world's largest CDMO production capacity of 784,000 liters. The region's strategic focus on cell and gene therapy manufacturing, combined with government investment in biopharmaceutical infrastructure parks, positions Asia-Pacific to capture an increasing proportion of global biologics manufacturing activity through 2033.

Competitive Landscape

Market Structure Analysis

The biologics contract manufacturing market is highly competitive and characterized by the presence of large, mid-sized, and specialized service providers offering end-to-end solutions. Competition is driven by manufacturing scale, regulatory compliance, technical expertise in complex biologics, and the ability to support both clinical and commercial production. Players compete on capacity expansion, adoption of single-use and continuous bioprocessing technologies, and strong quality and compliance track records.

Key Market Developments

- In January 2026, Rakuten Medical and Lotte Biologics signed a biopharmaceutical contract manufacturing agreement at the J.P. Morgan Healthcare Conference to enhance manufacturing capacity for Rakuten’s oncology photoimmunotherapy program. Under the deal, Lotte Biologics will supply advanced manufacturing services for monoclonal antibody intermediates and their conjugates to support global clinical development and future commercialization.

Companies Covered in Biologics Contract Manufacturing Market

- Samsung Biologics

- BioXcellence (Boehringer Ingelheim)

- Lonza Group AG

- Fujifilm Diosynth Biotechnologies

- AbbVie CM (AbbVie Inc.)

- WuXi Biologics (Cayman) Inc.

- AGC Biologics

- Patheon N.V. (Thermo Fisher Scientific Inc.)

- Emergent BioSolutions Inc.

- Ajinomoto Bio-Pharma

- Avid Bioservices, Inc.

- KBI Biopharma

- Rentschler Biotechnologie GmbH

- Merck KGaA

Frequently Asked Questions

The global biologics contract manufacturing market is expected to reach US$ 14.8 billion in 2026 and is projected to grow to US$ 25.1 billion by 2033.

The primary demand drivers include the escalating pipeline of FDA-approved biologics (with 16 biologic approvals in 2024 including 13 monoclonal antibodies), strategic outsourcing by pharmaceutical companies to reduce capital investment and manufacturing cost.

North America maintains the largest market share with 37% in 2025, driven by regulatory expertise, the presence of major pharmaceutical company headquarters, robust FDA approval infrastructure, and established biopharmaceutical manufacturing excellence.

Key market opportunities include the rapidly expanding demand for personalized medicine and Advanced Therapy Medicinal Products (ATMPs) including cell and gene therapies (growing at 13-15% CAGR), the geographic expansion of manufacturing capacity in Asia-Pacific.

Samsung Biologics, BioXcellence (Boehringer Ingelheim), Lonza Group AG, Fujifilm Diosynth Biotechnologies, etc.