- Biotechnology

- Viral Vector Manufacturing Market

Viral Vector Manufacturing Market Size, Share, and Growth Forecast, 2025 - 2032

Viral Vector Manufacturing Market By Virus Type (Adeno-Associated Virus (AAV) Vectors, Lentiviral Vectors, Others), Application (Gene Therapy, Others), End-user (Biotechnology & Pharmaceutical Companies, Others), and Regional Analysis for 2025 - 2032

Viral Vector Manufacturing Market Share and Trends Analysis

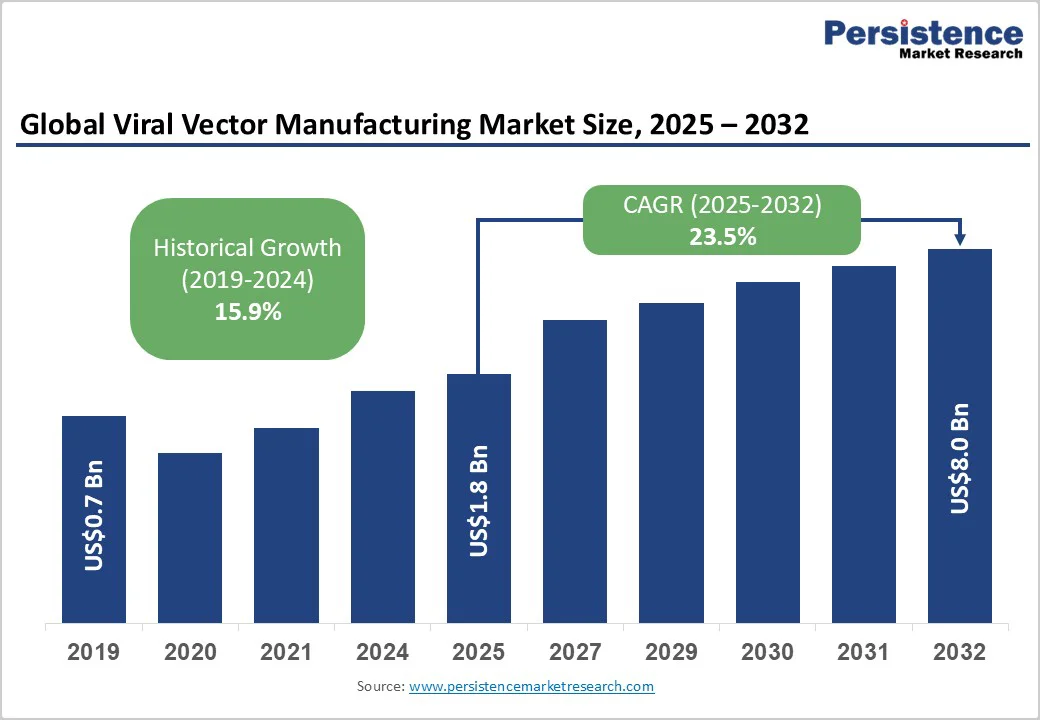

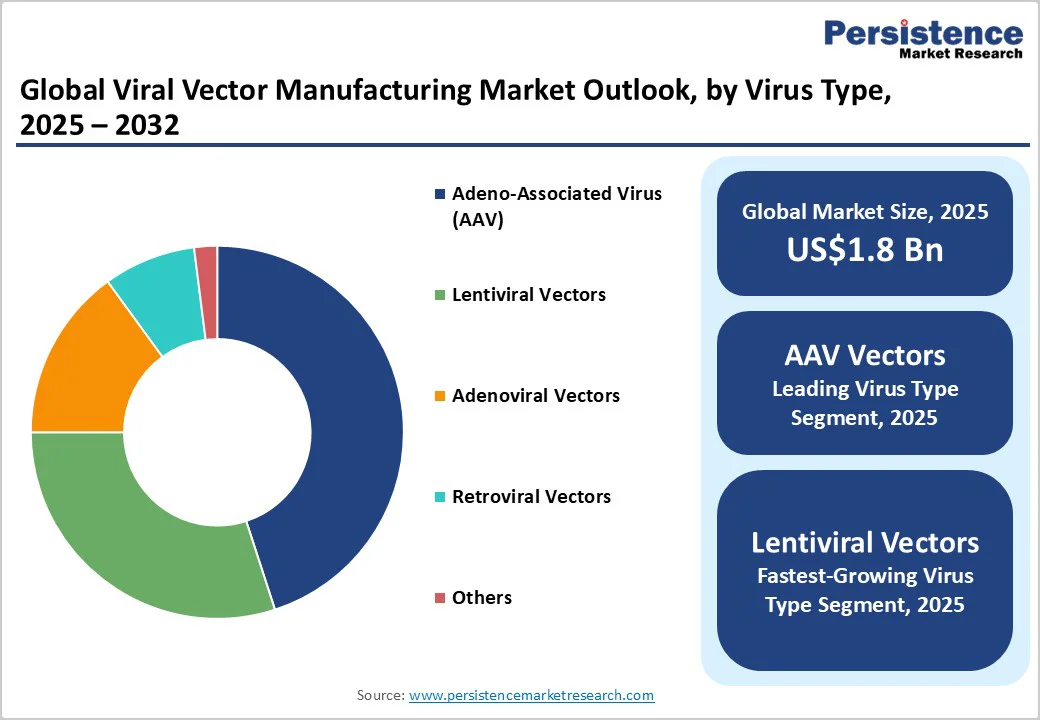

The global viral vector manufacturing market size is likely to be valued at US$1.8 Billion in 2025, and is estimated to reach US$8.0 Billion by 2032, growing at a CAGR of 23.5% during the forecast period 2025 - 2032, driven by accelerated expansion as gene therapy commercialization intensifies across genetic disorders, oncology, and rare diseases.

Regulatory milestones, bioprocessing innovations, and rising viral vector clinical trials, supported by CDMO capacity expansion, pharma-manufacturer partnerships, and scalable AAV and lentiviral platforms enabling commercial therapy production will drive market growth.

Key Industry Highlights

- Leading Virus Type: AAV vectors dominate with an estimated 45% share in 2025 due to AAV's superior safety profile and broad tissue tropism.

- Fastest-growing Virus Type: Lentiviral vectors represent the fastest-growing segment during 2025 - 2032, propelled by expanding CAR-T cell therapy.

- Dominant Application: Gene therapy dominates with about 47% market share in 2025, supported by an increasing number of approvals and a robust clinical pipeline.

- Fastest-growing Application: Vaccine development is likely to grow the fastest through 2032, driven by viral vector-based vaccine platform validation during COVID-19.

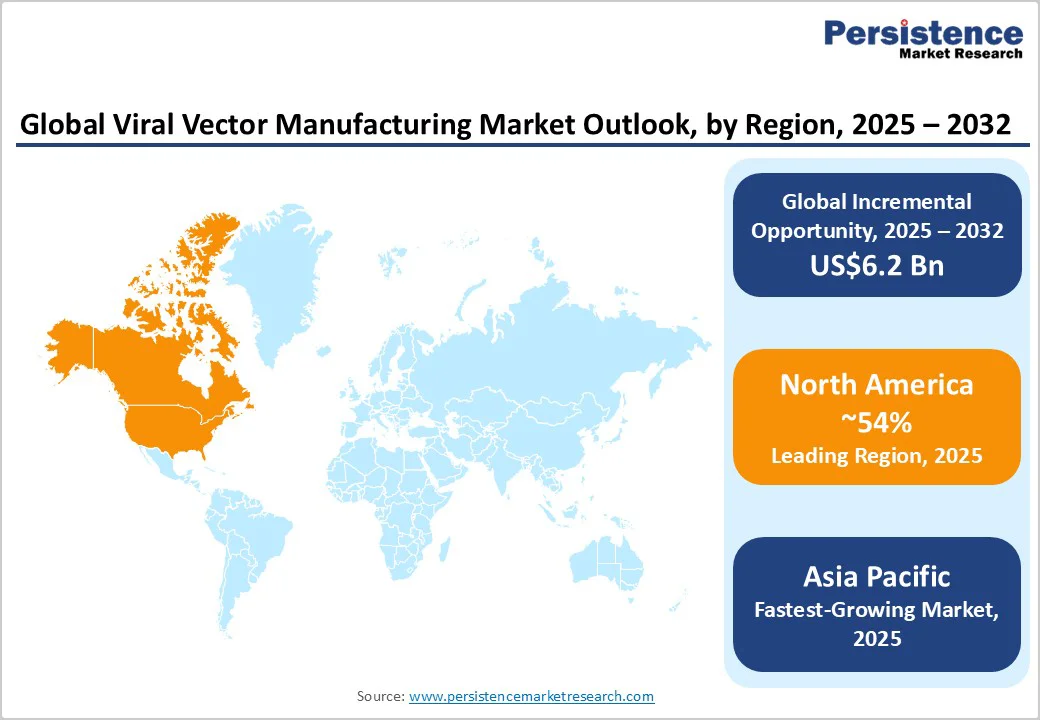

- Dominant Region: North America leads with 54% market share in 2025, underpinned by the concentration gene therapy clinical trials and manufacturing facility investments in the U.S.

- Fastest-growing Regional Market: Asia Pacific is set to post the highest CAGR of 22% during 2025 - 2032, driven by massive funding for cell and gene therapy (CGT) infrastructure by the Chinese government.

- Fastest-growing End-user: CDMOs constitute the fastest-growing end-user segment through 2032, powered by their integrated service offerings and flexible contract structures.

- June 2025: ProBio opened its flagship plasmid and viral vector manufacturing facility in Hopewell, New Jersey, to support advanced CGT development and manufacturing.

| Key Insights | Details |

|---|---|

| Viral Vector Manufacturing Market Size (2025E) | US$1.8 Bn |

| Market Value Forecast (2032F) | US$8.0 Bn |

| Projected Growth (CAGR 2025 to 2032) | 23.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 15.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Accelerated Rare Disease Gene Therapy Approvals and Reimbursement Framework Evolution

Viral vector manufacturing is accelerating due to a surge in regulatory approvals for rare disease gene therapies and evolving reimbursement frameworks that validate the commercial potential of high-cost, one-time curative treatments. Growth is particularly notable in rare genetic disorders with small patient populations where conventional therapies have been ineffective.

Expedited pathways, such as the U.S. FDA’s Orphan Drug Act and the EMA’s PRIME designation, reduce time-to-market by months, enabling faster clinical development, early regulatory engagement, and streamlined process validation for manufacturing.

Reimbursement models are adapting to the unique economic profiles of gene therapies. Health technology assessment bodies such as ICER in the U.S. and their European counterparts are implementing value-based pricing frameworks to quantify therapeutic benefits.

Countries including the U.K., Germany, and France have introduced installment payment and outcomes-based agreements, spreading costs over multiple years and aligning payments with real-world efficacy. These approaches address payer concerns, reduce financial risk, and create predictable revenue streams for manufacturers.

Collectively, regulatory acceleration and innovative reimbursement strategies are catalyzing large-scale investment in viral vector production, supporting the expansion of commercial manufacturing capacity, enabling broader patient access, and enhancing the sustainability of the gene therapy market globally.

Manufacturing Complexity and Regulatory Compliance Cost Escalation

The viral vector manufacturing market growth is getting stalled due to the inherent biological complexity of vector production processes and the increasingly stringent regulatory compliance requirements imposed by global health authorities. Manufacturing viral vectors, particularly AAV and lentiviral vectors, requires sophisticated bioprocessing capabilities, which need to adhere to Good Manufacturing Practice (cGMP) conditions.

Industry analyses indicate that achieving cGMP compliance for viral vector manufacturing increases production costs significantly compared to research-grade production, erecting substantial financial barriers for emerging biotech companies and academic institutions.

The regulatory landscape, dominated by the FDA and EMA, involves divergent requirements for viral vector characterization and release testing, particularly regarding potency assays and replication-competent virus (RCV) testing protocols. For example, the FDA strongly recommends validated functional potency assays for CGTs, whereas the EMA accepts infectivity and transgene expression assays.

These regulatory inconsistencies necessitate dual manufacturing processes and analytical testing strategies for companies pursuing global market access, effectively doubling development costs and extending timelines. Quality control and batch consistency represent additional restraint factors, since viral vector production exhibits inherent variability due to the biological nature of production systems.

AI-Enabled Bioprocess Optimization and Platform Technology Standardization

A transformative opportunity for the market seems to be emerging from the convergence of AI-driven bioprocess optimization and standardized platform technology adoption.

As viral vector production remains highly customized, labor-intensive, and characterized by significant batch-to-batch variability that increases manufacturing costs, AI-powered predictive analytics and machine learning (ML) algorithms are demonstrating remarkable capability to address these inefficiencies.

In upstream manufacturing, ML models analyze real-time bioreactor data to dynamically optimize transfection efficiency and predict viral yields with unprecedented accuracy. Downstream purification operations benefit equally, with AI-driven chromatography modeling enabling precise prediction of optimal elution conditions, reducing trial-and-error experimental runs, and accelerating process development timelines for commercial-scale manufacturing transfers.

Complementing AI implementation, standardized platform technologies are emerging as vehicles for scaling manufacturing efficiency across multiple therapeutic programs. Companies including Thermo Fisher, Merck, and technology specialists are developing pre-validated, modular manufacturing platforms encompassing optimized cell lines, chemically defined culture media, transfection reagents, and purification protocols.

These platforms reduce client-specific process development considerably by providing proven, regulatory-acceptable manufacturing systems requiring only product-specific customization rather than complete process development.

The standardization opportunity extends to CDMOs, which can leverage platform technologies to serve multiple clients simultaneously using shared manufacturing infrastructure, improving asset utilization while reducing per-batch manufacturing costs.

Category-wise Analysis

Virus Type Insights

AAV vectors dominate the viral vector manufacturing market, capturing an estimated 45% revenue share in 2025 due to their favorable safety profile, low immunogenicity, non-integrating genome delivery, and broad tissue tropism.

These features make AAV the preferred choice for in vivo gene therapies, as evidenced by the commercial success of Zolgensma (spinal muscular atrophy), Luxturna (inherited retinal dystrophy), and Hemgenix (hemophilia B). Significant manufacturing investments are focused on AAV production, with leading companies operating large-scale global facilities to meet clinical and commercial demand.

Lentiviral vectors are the fastest-growing segment from 2025 to 2032, driven by their ability to transduce dividing and non-dividing cells and achieve stable genomic integration, critical for ex vivo cell therapies such as CAR-T and CAR-NK immunotherapies. Clinical successes such as Kymriah and Yescarta are fueling manufacturing demand.

Advances in lentiviral production, including third-generation self-inactivating designs and scalable transient transfection systems, are enhancing biosafety and efficiency, overcoming historical production limitations, and positioning lentiviral vectors for sustained expansion across oncology and cell therapy applications throughout the forecast period.

Application Insights

Gene therapy applications dominate the viral vector market, capturing an estimated 47% share in 2025, driven by the transition of gene therapy from experimental research to validated clinical treatments. This growth is supported by an increasing number of FDA- and EMA-approved therapies and a robust clinical pipeline addressing genetic disorders, oncology, and rare diseases.

These applications primarily rely on AAV and lentiviral vectors, necessitating specialized manufacturing capabilities, advanced purification systems, and stringent quality control to meet regulatory standards. As therapies scale from clinical trials to commercial production, manufacturing complexity rises, requiring validated cGMP-compliant processes.

Vaccine development is the fastest-growing application segment from 2025 to 2032, propelled by the success of viral vector-based COVID-19 vaccines and expanding use in infectious disease prevention and cancer immunotherapy. Adenoviral and modified vaccinia virus vectors have shown high efficacy, exemplified by the Oxford-AstraZeneca ChAdOx1 and Johnson & Johnson Ad26.COV2.S vaccines, which delivered over 2 billion doses globally.

The infrastructure established for COVID-19 vaccine production is being adapted for next-generation vaccines targeting influenza, RSV, malaria, and therapeutic cancer vaccines, further accelerating adoption of viral vector manufacturing capabilities across public health and commercial applications.

End-user Insights

Biotechnology and pharmaceutical companies dominate the viral vector market, capturing an estimated 52% share in 2025, driven by concentrated gene therapy development and commercialization activities.

This segment includes vertically integrated pharma firms, such as Novartis and Pfizer, with in-house viral vector manufacturing, and biotech companies outsourcing to specialized CDMOs. Dual-sourcing strategies are common to mitigate supply chain risks, often engaging primary CDMO partners for commercial supply.

CDMOs are projected to grow fastest from 2025 to 2032, fueled by increasing outsourcing across the viral vector manufacturing value chain. Leading CDMOs, including Lonza, Catalent, WuXi Biologics, and Thermo Fisher Scientific, are expanding capabilities by providing end-to-end services spanning process development, analytical validation, regulatory support, and commercial-scale production under flexible contracts.

Growth is accelerated by biotech firms favoring variable cost structures, shorter development timelines, and specialized expertise to navigate complex regulatory landscapes, positioning CDMOs as key enablers in the viral vector ecosystem.

Regional Insights

North America Viral Vector Manufacturing Market Trends

North America maintains leadership with an estimated 54% of the viral vector manufacturing market share in 2025. The region's dominance is anchored in the unparalleled biopharmaceutical innovation ecosystem of the U.S., comprising world-class academic research institutions, robust venture capital funding mechanisms, and the highest concentration of gene therapy clinical trials globally.

The FDA's progressive regulatory framework, including expedited pathways such as Regenerative Medicine Advanced Therapy (RMAT) designation and Priority Review vouchers, has created favorable conditions for rapid therapy advancement from clinical development to commercialization.

Canada, too, is making notable contributions, with government-supported initiatives including the Strategic Innovation Fund allocated to biomanufacturing infrastructure in 2024 - 2025. Canadian companies such as AbCellera and Canadiens are establishing viral vector capabilities specifically targeting vaccine applications and rare disease therapies, benefiting from cost advantages relative to U.S. facilities.

These companies are also maintaining regulatory alignment through Health Canada's collaboration with the FDA on biologics oversight. Extensive reimbursement coverage through government insurance schemes and commercial insurance plans is also stoking the adoption of outcomes-based payment models for gene therapies in the region.

Europe Viral Vector Manufacturing Market Trends

Europe is expected to command an estimated 27% of the global market share in 2025, boosted by sophisticated biopharmaceutical capabilities concentrated in Germany, the U.K., France, and Switzerland, and supported by harmonized regulatory frameworks under the EMA that facilitate multi-country clinical development and marketing authorization.

Germany emerges as Europe's manufacturing hub, hosting high-capacity viral vector facilities operated by BioNTech, Merck, and specialized CDMOs, including Sartorius and Rentschler Biopharma, having particular expertise in lentiviral vector production for cell therapy applications.

Regulatory harmonization under EMA oversight provides Europe with distinctive advantages, enabling companies to conduct clinical trials across multiple countries under unified protocols while achieving centralized marketing authorization valid across all 27 EU member states.

This regulatory efficiency has accelerated market access timelines and bolstered manufacturing investment decisions. Europe faces pricing and reimbursement challenges, with health technology assessment bodies including NICE in the U.K., IQWiG in Germany, and HAS in France applying stringent cost-effectiveness thresholds that have resulted in restricted access or delayed reimbursement for high-cost gene therapies.

Asia Pacific Viral Vector Manufacturing Market Trends

Asia Pacific is the fastest-growing regional market for viral vector manufacturing, projected to grow at a CAGR of approximately 22% from 2025 to 2032. Growth is driven by supportive government policies, rising healthcare expenditure, and cost advantages in manufacturing. Increasing demand for advanced therapies is fueled by aging populations and higher prevalence of genetic disorders and cancer.

China leads the region, benefiting from government investments under the Made in China 2025 initiative and regulatory reforms by the National Medical Products Administration (NMPA) that expedite gene therapy approvals and shorten clinical development timelines.

India is emerging as a key growth market, marked by Bharat Biotech inaugurating the country’s first dedicated viral vector manufacturing facility in 2024. India’s strengths include a highly skilled scientific workforce, established expertise in biologics and pharmaceutical manufacturing, and government incentives such as tax holidays and accelerated regulatory pathways for advanced therapy facilities.

With healthcare expenditure projected to reach US$638 billion in 2025 and a rapidly growing patient population, India presents substantial opportunities for both domestic commercialization and export of viral vector-based therapies, positioning the Asia Pacific region as a critical hub for scalable and cost-efficient viral vector production.

Competitive Landscape

The global viral vector manufacturing market is moderately consolidated, with the top 10-12 players controlling roughly 55-60% of revenue. Leadership is shared between vertically integrated pharma companies managing proprietary gene therapy production and specialized CDMOs serving multiple clients.

Thermo Fisher Scientific leads with an estimated 12% share, strengthened by its Brammer Bio acquisition and expanded AAV and lentiviral capacity. Market dynamics show rising vertical integration and consolidation, exemplified by Merck KGaA’s US$600 Million Mirus Bio acquisition in 2024, enhancing end-to-end capabilities from plasmid production to downstream purification, process development, analytical support, and multi-scale manufacturing.

Key Industry Developments

- In October 2025, Australia opened its first clinical and commercial-scale viral vector manufacturing facility (VVMF) in Sydney. The facility provides GMP-grade lentiviral and AAV vector manufacturing, supporting CGT development with up to 500L manufacturing capacity. VVMF aims to boost Australia’s advanced biomanufacturing capabilities, attract international investment, and accelerate patient access to advanced therapies in areas such as oncology and rare diseases.

- In September 2025, DINAMIQS inaugurated its new state-of-the-art cGMP viral vector manufacturing facility in Zurich, Switzerland, featuring integrated R&D, clinical, and commercial production capabilities with up to 1,000L capacity. The modular facility uses advanced single-use technologies to ensure GMP compliance, containment, and fast turnaround, addressing key scalability challenges in gene therapy manufacturing.

- In July 2025, ViroCell Biologics partnered with AvenCell Therapeutics to produce a retroviral vector for AVC-203, an allogeneic CAR-T therapy targeting B-cell malignancies and autoimmune diseases. Leveraging ViroCell’s high-yield vector expertise, the collaboration aims to accelerate clinical entry in H2 2025, offering an “off-the-shelf” solution, reducing graft-versus-host risks.

Companies Covered in Viral Vector Manufacturing Market

- Thermo Fisher Scientific Inc.

- Lonza Group AG

- Merck KGaA

- Catalent, Inc.

- Sartorius AG

- Oxford Biomedica plc

- FUJIFILM Diosynth Biotechnologies

- Charles River Laboratories International, Inc.

- WuXi Biologics (Cayman) Inc.

- AGC Biologics

- Novartis AG

- Takara Bio Inc.

- Aldevron, LLC

- Batavia Biosciences B.V.

- Resilience

Frequently Asked Questions

The global viral vector manufacturing market is projected to reach US$1.8 Billion in 2025.

Gene therapy commercialization across genetic disorders, oncology, and rare diseases, regulatory milestone achievements, technological breakthroughs in scalable bioprocessing, and surging clinical trial activity for viral vector-based therapeutics are driving the viral vector manufacturing market.

The viral vector manufacturing market is poised to witness a CAGR of 23.5% from 2025 to 2032.

Capacity investments from CDMOs, strategic partnerships between pharmaceutical companies and specialized manufacturers, and the maturation of AAV and lentiviral vector production platforms are key market opportunities.

Thermo Fisher Scientific Inc., Lonza Group AG, and Merck KGaA are some of the key players in the viral vector manufacturing market.