- Automation & Robotics

- Manufacturing Market

Manufacturing Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Manufacturing Market By End-user Industry (Automotive & Auto Components, Electronics & Electricals, Others), Technology (Smart Manufacturing/Industry 4.0, Traditional Manufacturing, Additive Manufacturing, Others), Enterprise Size (Large Enterprises, Others), and Regional Analysis for 2025 - 2032

Manufacturing Market Share and Trends Analysis

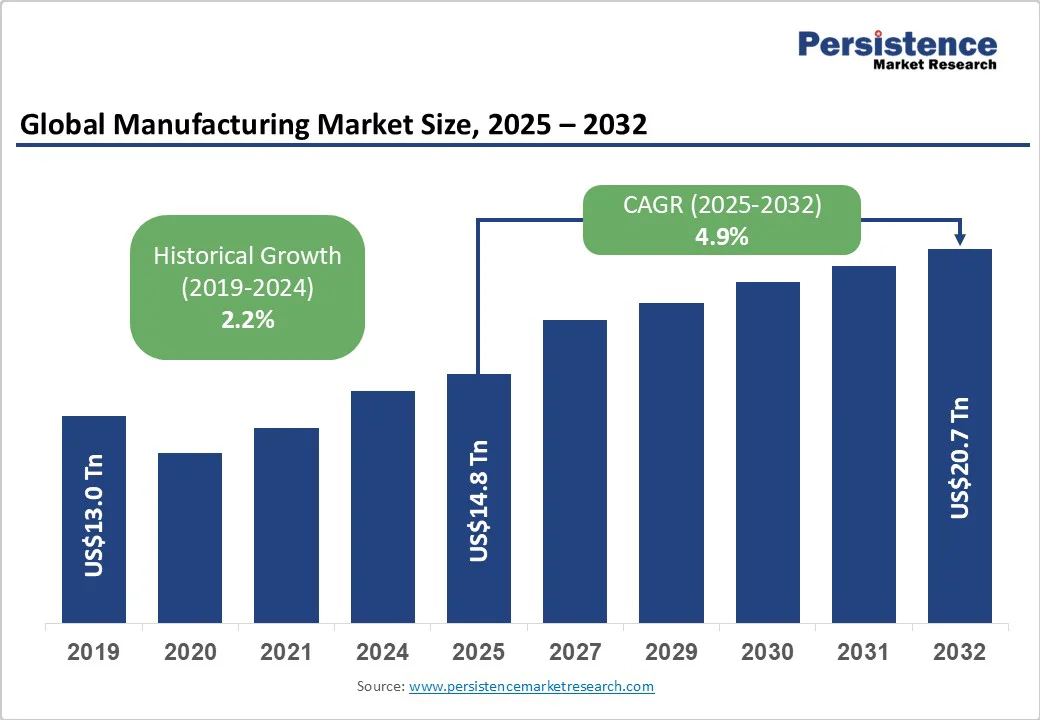

The global manufacturing market size is expected to reach US$14.8 trillion by 2025. It is estimated to reach US$20.7 trillion by 2032, growing at a CAGR of 4.9% during the forecast period 2025−2032, driven by growing adoption of Industry 4.0, advances in smart manufacturing, and policy efforts for reindustrialization and resilient supply chains.

Key Industry Highlights:

- Leading Industries: Automotive leads the end-user segment at about 21.4% share in 2025, with electronics & electricals emerging as the fastest-growing sector through 2032 with a 15.3% CAGR.

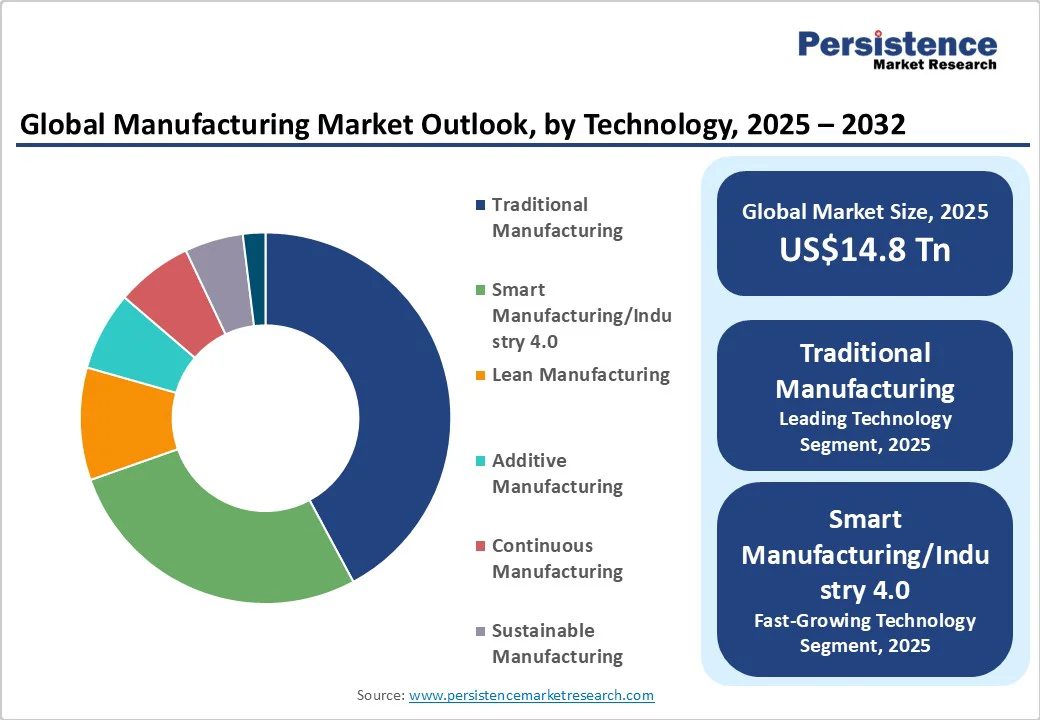

- Leading Technologies: Traditional manufacturing holds approximately 42.3% share in 2025, while smart manufacturing is likely to expand at nearly 14.0% CAGR from 2025 to 2032, driven by AI and automation adoption.

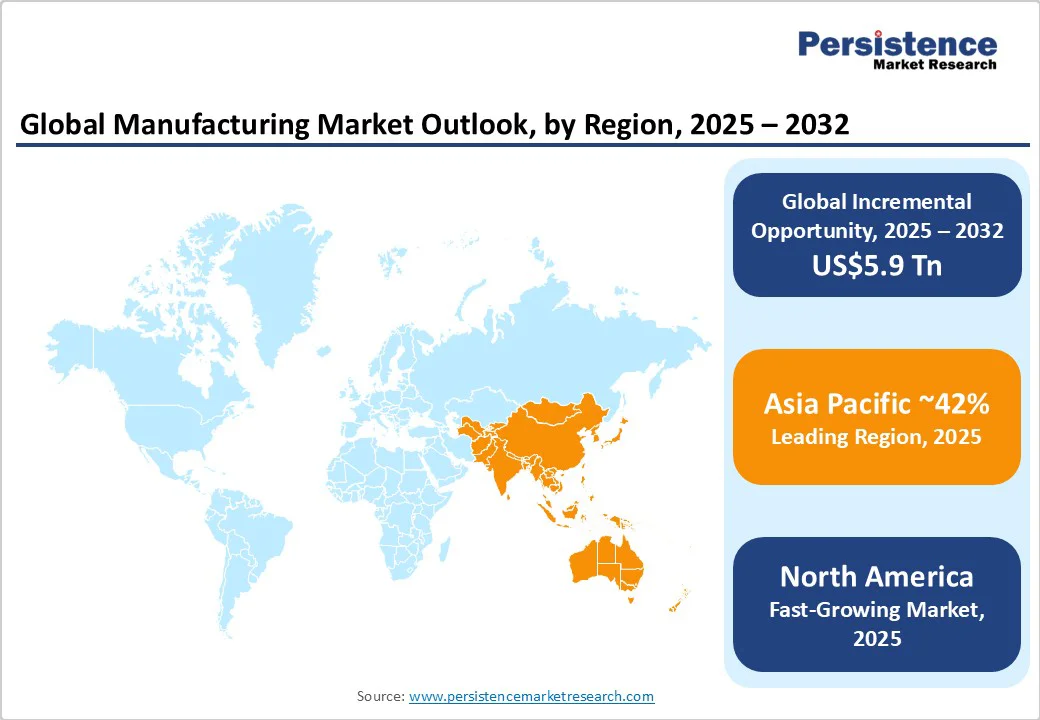

- Dominant Region: Asia Pacific is set to lead with an estimated 42.7% market share, with North America growing the fastest at 5.2% CAGR through 2032 due to reshoring and innovation incentives.

- Leading Enterprise Size: Large enterprises dominate the market with 48.2% of the market share in 2025; SMEs exhibit the highest growth rates, enabled by cloud and modular platforms.

| Key Insights | Details |

|---|---|

|

Manufacturing Market Size (2025E) |

US$14.8 Tn |

|

Market Value Forecast (2032F) |

US$20.7 Tn |

|

Projected Growth (CAGR 2025 to 2032) |

4.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

2.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Structural Digitalization of Production Systems

The ongoing integration of Industry 4.0 technologies, including IoT connectivity, AI-enabled predictive maintenance, and advanced manufacturing execution systems, is revolutionizing the sector. This digital transformation fundamentally improves operational efficiency metrics, such as overall equipment effectiveness, and reduces waste, thereby enhancing productivity. Firms leveraging these technologies are achieving 10.0%-20.0% throughput enhancements and up to 30.0% maintenance cost reductions. As these innovations permeate beyond leading original equipment manufacturers (OEMs) to tiered suppliers, the manufacturing ecosystem becomes more cost-efficient and competitive, encouraging broader adoption and investment.

Furthermore, governmental policy frameworks across leading markets are fostering reindustrialization efforts. This trend is poised to transform supply chains into multi-hub configurations, prioritizing resilience and risk mitigation. Firms are aligning investments to leverage local content requirements and workforce development policies, thus optimizing cost control and enhancing responsiveness to geopolitical uncertainties.

Capital Intensity and Frictions with Legacy Systems

Transitioning brownfield plants to smart manufacturing environments faces challenges, including cyber risk, integration complexities, and significant upfront capital investment. Inadequate cybersecurity measures can lead to substantial operational losses, while skill shortages hinder deployment velocity. Financing these upgrades remains a critical barrier for mid-sized enterprises, necessitating innovative financing and incremental upgrade strategies to mitigate risk and realize cost savings efficiently. Compounding this are the persistent component shortages, logistical delays, and divergent regulatory frameworks across jurisdictions.

Tariff uncertainties and multi-week shipping disruptions can substantially erode operational margins, with some sectors experiencing margin compression of up to 300 basis points. Compliance heterogeneity increases product development timelines and hinders rapid market access, necessitating robust dual-sourcing strategies and proactive regulatory engagement to maintain supply chain integrity and minimize business risk.

Electrification and Power Electronics Manufacturing Expansion

The surge in AI data centers, electric vehicles, and renewable energy infrastructure is amplifying demand for silicon carbide power devices, battery components, and energy conversion systems. Complimentary market scaling, supported by U.S. and EU incentives, is estimated to unlock a multi-hundred-billion-dollar opportunity by 2032. Firms positioned to integrate advanced manufacturing execution systems with high-yield power electronics production will secure a competitive advantage.

The increased focus of OEMs on high-mix, regulated segments, including medtech and aerospace, is stimulating growth in outsourced manufacturing. This trend is catalyzed by demand for compliance with FDA and EU MDR standards and high levels of customization. With the U.S. engaging in reshoring initiatives, regional engine management system (EMS) providers with robust quality systems are projected to access a double-digit billion-dollar incremental addressable market opportunity.

Category-wise Analysis

End-user Industry Insights

The automotive & auto components segment is expected to continue leading with an estimated 21.4% share in 2025, driven by ongoing electrification, autonomous vehicle integration, and heightened demand for lightweight materials and advanced electronics. This segment is rapidly adopting innovations such as giga-pressing, laser welding, and highly automated assembly lines, which are streamlining production and stabilizing yields. Moreover, regional regulatory frameworks mandating local content requirements in North America and Europe are prompting tier-1 suppliers and EMS partners to diversify and adapt assembly capacities, improving supply chain robustness and cost competitiveness.

Conversely, the electronics & electricals segment is poised to grow the fastest, with a leading CAGR by 2032. Growth drivers include the expansion of AI data centers, 5G infrastructure, semiconductor fabrication, and consumer electronics supported by substantial foundry investments and policy incentives in the Asia Pacific and North America. The segment's growth is further fueled by demand for smart industrial controls, telecom equipment, and edge-computing devices. This trend encourages suppliers to invest in substrate production, advanced packaging, and test automation capabilities, optimizing design-for-manufacturing approaches to meet client expectations and evolving regulatory standards.

Technology Insights

Traditional manufacturing processes, including casting, forging, machining, and forming, are forecasted to retain a dominant 42.3% revenue share in 2025, owing to their wide applicability in heavy industries such as metals, construction materials, and industrial machinery. These legacy processes are undergoing gradual modernization through the integration of machine vision, computer numerical control (CNC) connectivity, and robotic tending, which improve operational efficiency without necessitating full process replacement. Operators are prioritizing interoperable data environments that enable condition monitoring and predictive maintenance on legacy equipment, sequencing upgrades on a line-by-line basis to maintain production continuity and delivery reliability.

Smart manufacturing or Industry 4.0 technologies represent the fastest-growing segment, projected to expand at an approximate 14.0% CAGR through 2032. These include AI, industrial Internet of Things (IIoT), robotics, digital twins, and augmented reality applications that enable real-time process control, autonomous material handling, and adaptive quality assurance. Industry adoption is most intense in high-mix, complexity-sensitive sectors such as pharmaceutical, semiconductor, and aerospace manufacturing. Companies deploying smart manufacturing solutions are achieving measurable gains in overall equipment effectiveness (OEE), first-pass yield, and cycle-time compression, making early investment in these technologies increasingly critical for competitive differentiation.

Enterprise Size Insights

Large enterprises are estimated to command approximately 48.2% of the manufacturing market in 2025. Their market dominance is attributable to substantial capital resources, global supply chain control, and in-house engineering capabilities that facilitate early adoption of advanced automation, digital transformation, and sustainability initiatives. These players often lead supplier standardization efforts on cybersecurity, traceability, and quality management, setting the compliance baseline for the wider ecosystem.

Micro, small, & medium enterprises (MSMEs) represent the fastest-growing sub-segment, forecasted to grow at a formidable CAGR of around 14.8% through 2032. Cloud-native manufacturing execution systems (MES), scalable robotics, and subscription-based analytics platforms are lowering access barriers, enabling SME digital footprints to expand rapidly. Policy-backed cluster development and industrial parks are further catalyzing SME growth, especially in the Asia Pacific and North America. SMEs focusing on modular production cells, rapid certification acquisition, and cybersecurity compliance are well-positioned to capture high-value, high-mix manufacturing niches that are increasingly favored by reshoring OEMs.

Regional Insights

North America Manufacturing Market Trends

North America is projected to hold approximately 26.5% of the manufacturing market share in 2025 and is anticipated to post the fastest regional growth over 2025–2032, with a CAGR of approximately 5.2%. The United States is the principal contributor, supported by extensive federal, state, and local government incentives focused on semiconductors, clean energy, defense, and advanced manufacturing technologies. This ecosystem benefits from a vigorous innovation pipeline, including leading EMS providers, greenfield advanced fabs, and robust aerospace and pharmaceutical manufacturing hubs.

The regulatory landscape emphasizes cybersecurity standards, environmental compliance, and domestic content requirements, which collectively shape footprint decisions and supplier qualification processes. Investors and operators in the region benefit from proximity to end markets, advanced logistics infrastructure, and technology clusters that enhance the speed of new product introductions and operational resilience. Growth areas of focus include silicon carbide power electronics, battery pack assembly, aerospace components, and GMP-certified medical technology (medtech) manufacturing, supported by continuous workforce development and IT/OT convergence initiatives.

Europe Manufacturing Market Trends

Europe is estimated to account for approximately 23.7% of the global market in 2025, with Germany, the United Kingdom, France, Spain, and Italy as the leading contributors. Germany continues to champion precision manufacturing, driving high-value production in automotive, machinery, and electrical equipment through its Industrie 4.0 initiative. Regulatory harmonization across the European Union (EU), including carbon border adjustment measures and stricter product safety frameworks, incentivizes investment in low-emission manufacturing technologies, life-cycle assessment, and circular economy practices.

The industrial landscape in Europe is characterized by deeply integrated clusters of suppliers, technology providers, and academic partnerships, fueling a continuous innovation cycle. Investments are particularly robust in hydrogen technology, sustainable materials manufacturing, and next-gen automotive sectors, with technology partnerships playing a critical role in accelerating compliance and industrial scale-up.

Asia Pacific Manufacturing Market Trends

The Asia Pacific region retains its position as the largest regional manufacturing market, estimated to account for 42.7% of the global market in 2025. The region boasts a comprehensive and diversified base spanning China, Japan, South Korea, India, and ASEAN nations, distinguished by their scale, supplier networks, and increasing adoption of advanced manufacturing technologies. China, as the biggest player, continues to emphasize upgrading capabilities through its Made in China 2025 program targeting robotics, aerospace, and EV manufacturing. Japan and South Korea maintain global leadership in precision equipment and semiconductor fabrication, while India’s manufacturing sector is rapidly expanding, supported by Production Linked Incentive (PLI) schemes, improving infrastructure, and rising export orientation.

Asia Pacific regional growth is driven by favorable demographics, industrial policy continuity, and strategic investments in logistics and technology diffusion. Regulatory environments across the region are trending toward greater facilitation of manufacturing and green initiatives, although variance persists. The competitive landscape is distinguished by a mix of domestic champions and multinational corporations expanding localized manufacturing footprints. Investment focus areas include electronics, automotive components, pharmaceutical production, and the manufacture of EV supply chain parts, where integration with R&D hubs enhances time to market and quality compliance.

Competitive Landscape

The global manufacturing market structure remains broadly fragmented, but vertical markets such as automotive, aerospace, and semiconductors exhibit concentrated leadership. Leading corporations control low single-digit shares of total manufacturing value but exert outsized influence within their niches through scale, intellectual property (IP), and certification. Competitive positioning hinges on mastery over end-to-end digital threads, supplier orchestration, and decarbonization. Ongoing consolidation is anticipated in contract manufacturing and EMS domains, driven by customer demands for quality, regional diversification, and capacity scalability.

Dominant strategies emphasize accelerating digital innovation, achieving cost leadership through automation, and expanding geographically with agility and compliance. Market leaders pursue ecosystem integration, combining proprietary technologies with broad supply networks. Emerging business models involve manufacturing-as-a-service and modular microfactories, which facilitate high-mix responsiveness. Sustainability commitments are integral, driving investment in circular processes and verifiable emissions reductions.

Key Industry Developments:

- In September 2025, Machina Labs, in collaboration with Toyota North America, introduced AI-powered RoboForming technology for on-demand, tool-free production of custom automotive body panels. This innovation reduces costs, enhances flexibility, and supports mass-production quality at low volumes, addressing the growing demand for vehicle customization.

- In September 2025, Precision Biologics Manufacturing, a subsidiary of NHMS, broke ground on a new GMP-compliant facility in Southern Nevada. Set to create 200–300 MedTech jobs by late 2026, the site will boost U.S. biologics production, support advanced tech development, and serve as a hub for engineering and compliance training, driving regional economic growth and academic collaboration.

- In September 2025, Hong Kong Polytechnic University (PolyU) launched the AI-driven Centre for Smart Manufacturing to boost Industry 4.0 adoption. The center will develop AI and robotics solutions to enhance efficiency, quality, and customization, positioning Hong Kong as a smart manufacturing hub while promoting talent development and industry collaboration.

Companies Covered in Manufacturing Market

- Apple Inc.

- Toyota Motor Corporation

- Volkswagen AG

- Samsung Electronics Co., Ltd.

- Hon Hai Precision Industry Co., Ltd.

- Mercedes-Benz Group AG

- Ford Motor Company

- General Motors Company

- Bayerische Motoren Werke AG (BMW)

- SAIC Motor Corporation Limited

- Siemens AG

- Robert Bosch GmbH

- Boeing Company

- Airbus SE

- BASF SE

Frequently Asked Questions

The manufacturing market is projected to reach US$14.8 Trillion in 2025.

Strategic policy initiatives aimed at reindustrialization and building supply chain resilience are driving the market.

The manufacturing market is poised to witness a CAGR of 4.9% from 2025 to 2032.

Accelerating Industry 4.0 adoption and technological advancements in smart manufacturing are key market opportunities.

Apple Inc., Toyota Motor Corporation, and Volkswagen AG are some of the key players in the market.