- Processed Food

- Malt Beverage Market

Malt Beverage Market Size, Share, and Growth Forecast 2026 - 2033

Malt Beverage Market by Malt Type (Regular Malt, Flavored Malt, Non-Alcoholic Malt, Low/Reduced Alcohol Malt), Packaging (Bottles, Cans, Cartons/Pouches), Distribution Channel (On-Trade, Off-Trade), and Regional Analysis, 2026 - 2033

Malt Beverage Market Share and Trends Analysis

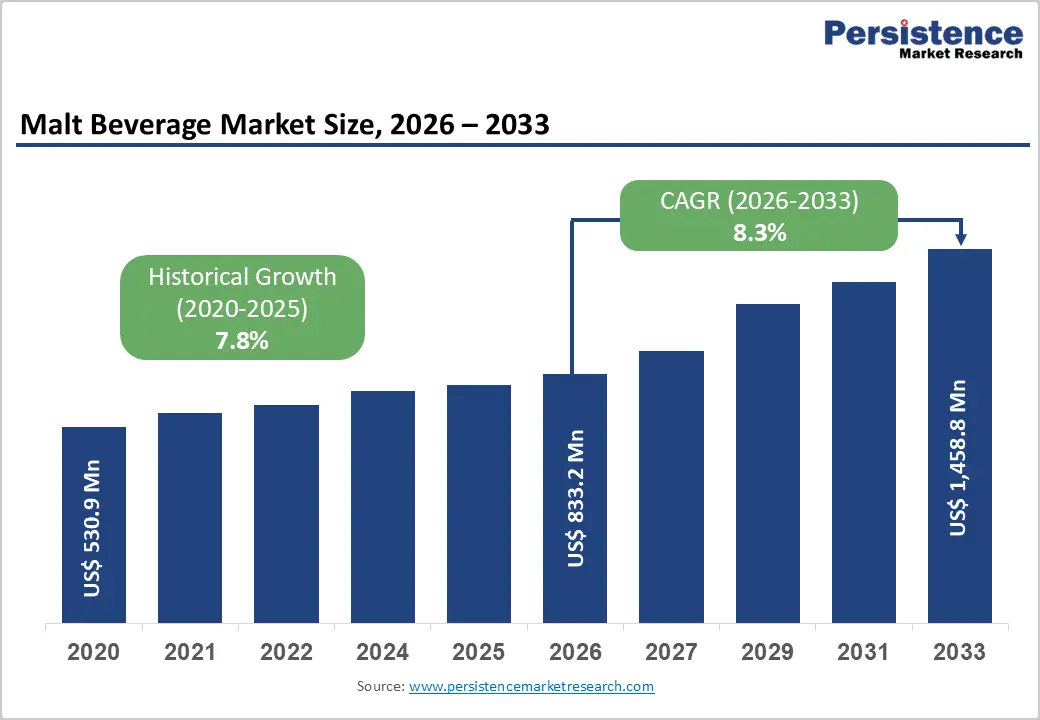

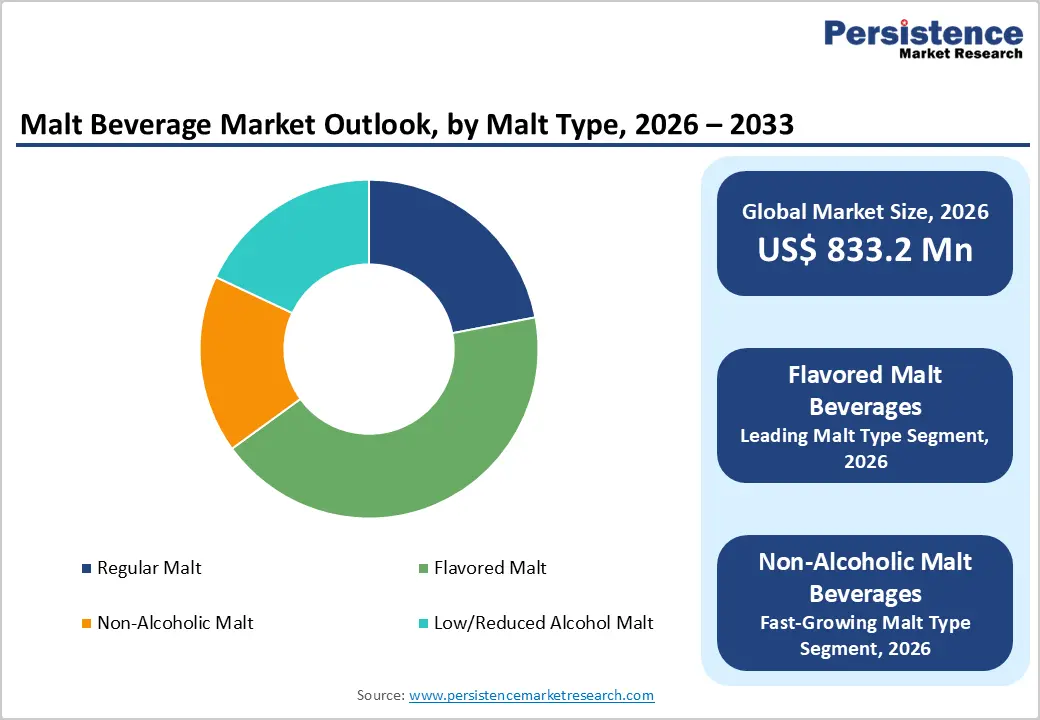

The global malt beverage market size is expected to be valued at US$ 833.2 million in 2026 and projected to reach US$ 1,458.8 million by 2033, growing at a CAGR of 8.3% between 2026 and 2033.

The market's robust growth trajectory is fueled by shifting consumer preferences toward diverse flavor experiences and health-conscious beverage alternatives. The rising popularity of non-alcoholic and low-alcohol malt beverages, combined with increasing premiumization trends and craft beverage innovation, has created significant momentum across both developed and emerging markets. Consumers are gravitating toward malt beverages that offer sophisticated taste profiles while aligning with wellness priorities, including reduced sugar content, natural ingredients, and functional nutritional benefits.

Key Industry Highlights:

- North America leads the global malt beverage market with about 41% share in 2025, underpinned by strong beer culture, advanced retail networks, and robust growth in flavored and non-alcoholic malt beverages supported by major brand owners’ innovation and marketing investments.

- Asia Pacific is the fastest-growing region, with the broader malt beverages market projected to rise to USD 468.99 billion roughly at 7.8% CAGR, driven by urbanization, income growth, Westernization of tastes, and rapid development in China, India, and ASEAN.

- Flavored malt beverages are the dominant malt type, holding roughly 43% share in 2025, reflecting strong consumer demand for sweeter, fruit-forward, and innovative taste profiles that provide an approachable alternative to traditional beer, particularly among younger adults.

- Non-alcoholic malt beverages constitute the fastest-growing malt type segment, with their market expected to expand from around USD 36.78 billion in 2025 to nearly USD 64.73 billion by 2035 at about 5.8% CAGR, supported by health and wellness trends, moderation, and demand in markets with cultural or religious limitations on alcohol.

- Functional and clean-label innovation represents a key opportunity, as malt beverages fortified with probiotics, fiber, vitamins, minerals, and adaptogens respond to rising consumer interest in products that combine enjoyable taste with tangible wellness benefits and sustainable, natural ingredient profiles.

| Key Insights | Details |

|---|---|

| Malt Beverage Market Size (2026E) | US$ 833.2 million |

| Market Value Forecast (2033F) | US$ 1,458.8 million |

| Projected Growth CAGR (2026 - 2033) | 8.3% |

| Historical Market Growth (2020 - 2025) | 7.8% |

Market Dynamics

Drivers - Accelerating Health and Wellness Movement Driving Non-Alcoholic Segment Expansion

The global health and wellness movement represents a transformative force reshaping malt beverage consumption patterns worldwide. The non-alcoholic malt beverages segment is projected to grow from USD 36.78 billion in 2025 to USD 64.73 billion by 2035, exhibiting a CAGR of 5.8%. This surge is driven by consumers actively seeking beverages that deliver authentic taste experiences without intoxicating effects, particularly among Millennials and Gen Z consumers who are driving the “sober curious” trend. Non-alcoholic malt beverages offer nutritional benefits, including B-vitamins, antioxidants, and essential minerals, while supporting hydration and energy levels, enhancing their appeal as everyday wellness beverages. Religious and cultural factors also contribute significantly, with markets under alcohol consumption restrictions showing particularly strong adoption of non-alcoholic malt drinks. The COVID-19 pandemic further amplified health consciousness, accelerating demand for immunity-supporting and better-for-you beverages that fit into preventive wellness strategies.

Premiumization and Craft Beverage Innovation Elevating Market Value

Premiumization trends are fundamentally transforming the malt beverage landscape as consumers demonstrate willingness to pay more for superior quality and distinctive products. The craft brewing movement has catalyzed innovation in specialty malt beverages, with artisanal producers introducing sophisticated flavor profiles based on roasted, caramel, and specialty malts. Industry associations in Europe report that over 70% of urban millennials now prioritize unique and handcrafted beverages, underscoring strong interest in differentiated offerings. Premium malt beverages often command price premiums of around 15-20% versus mainstream options in mature markets such as Germany and the United Kingdom, especially in flavored and craft styles. This premiumization extends into non-alcoholic malt beverages as well, where brands experiment with exotic flavors, organic certifications, and functional additions such as adaptogens, probiotics, and plant-based proteins to justify higher price points. As a result, manufacturers can drive margin expansion while catering to consumers seeking authenticity, provenance, and experience-led drinking occasions.

Market Restraints

Volatile Raw Material Costs Impacting Production Economics

The malt beverage industry faces persistent headwinds from volatile prices of key agricultural inputs such as barley, wheat, and hops, which are highly sensitive to weather and climate-related disruptions. Droughts, heatwaves, and erratic rainfall patterns have impaired cereal yields in major producing regions, causing pronounced fluctuations in malting barley availability and prices. At the same time, rising energy costs associated with kilning, brewing, refrigeration, and logistics add further pressure to production economics, particularly for small and mid-sized producers that lack scale-based cost advantages. Producers are forced either to absorb cost increases, squeezing margins, or pass them on through higher retail prices, which can dampen demand among price-sensitive consumers and constrain category penetration in emerging markets.

Regulatory Complexity and Marketing Restrictions

Evolving regulatory frameworks around alcohol content thresholds, marketing standards, labeling, and taxation create a complex operating environment for malt beverage manufacturers. Rules on advertising, sponsorship, and on-pack health messaging differ widely between countries and regions, particularly for products positioned close to the borderline between alcoholic and non-alcoholic categories. Flavored malt beverages face intensified scrutiny due to concerns that sweet profiles and vibrant branding may unintentionally appeal to underage consumers, prompting stricter marketing codes and monitoring. Tax regimes based on alcohol by volume may disadvantage higher-strength malt beverages or certain ready-to-drink formats, affecting pricing and portfolio strategy. In addition, tightening requirements around nutritional information, ingredient disclosure, and sustainability reporting demand administrative resources and compliance investments, raising barriers to entry for smaller companies and complicating cross-border expansion by global brands.

Opportunities - Functional Beverage Innovation and Natural Ingredient Formulations

The convergence of malt beverages with broader functional beverage trends opens attractive avenues for innovation. Consumers increasingly seek drinks that deliver specific health benefits such as gut health, stress reduction, beauty support, or immune enhancement, not just hydration and taste. Malt beverages provide a versatile base for adding probiotics, fiber, vitamins, minerals, and emerging ingredients such as adaptogens or collagen. Clean-label expectations and demand for natural or organic products encourage the use of minimally processed ingredients, reduced use of artificial sweeteners or colors, and transparent sourcing. Surveys show that about 40-43% of global consumers intend to buy more high-fiber or probiotic-rich products, aligning well with functional malt drink concepts. Plant-based, vegan, and low-sugar formulations further broaden the consumer base. Brands that combine credible health claims, regulatory-compliant labeling, and appealing sensory profiles can differentiate themselves, command premium pricing, and secure loyalty among health-conscious and lifestyle-focused segments.

Category-wise Analysis

Malt Type Insights

Flavored Malt Beverages are the leading malt type, accounting for roughly 43% of the market in 2025, as specified in the scope, supported by strong consumer interest in novel and indulgent taste experiences. Category momentum is visible in North America and Europe, where flavored malt beverages and hard seltzer-adjacent products continue to expand shelf space and on-premise presence. These products appeal especially to younger adults who may find traditional beer too bitter or heavy, favoring fruit-led, citrus, tropical, and dessert-inspired flavor profiles with moderate alcohol content. Seasonal and limited-edition flavors help maintain buzz and trial, while crossover innovation with cocktail and RTD trends further reinforces growth. The segment also benefits from convenient ready-to-drink formats and strong support from large brand owners who invest heavily in marketing, influencer partnerships, and festival/event sponsorships to reinforce lifestyle positioning.

Packaging Insights

Aluminum cans have emerged as the dominant packaging format in malt beverages, and are a logical leading segment within packaging. In the U.S. beer and malt-based drinks category, the Beer Institute reported that in 2023, about 64.1% of beer volume was shipped in aluminum cans, compared with 26.9% in glass bottles and 8.9% in draft, highlighting the strength of cans. Key advantages include light weight, shatter resistance, portability, rapid chilling, and excellent protection against light and oxygen, all of which help preserve flavor. From a sustainability perspective, aluminum cans are highly recyclable, and recycling rates in many markets exceed those of glass or plastic, aligning with corporate ESG commitments and consumer expectations on environmental responsibility. Innovations such as sleek can formats, resealable or specialty closures, and eye-catching graphics further enhance brand differentiation on shelves. These factors collectively position cans as the leading and most dynamic packaging solution for malt beverages globally.

Distribution Channel Insights

Off-trade distribution (including supermarkets, hypermarkets, convenience stores, liquor specialists, and e-commerce) forms the leading distribution channel for malt beverages, with a substantial share of retail sales in most major markets. Growth of at-home consumption, heightened during and after the pandemic, has permanently shifted part of the demand from on-trade outlets to home-based occasions, benefiting off-trade retailers. Modern grocery retail consolidates large assortments at competitive prices, while promotional mechanics and multipack offerings encourage volume purchases. Parallelly, online channels and direct-to-consumer models are gaining traction; in some regions, online alcohol sales recorded double-digit growth as regulations relaxed and logistics improved. Off-trade channels also facilitate the discovery of new flavors and smaller brands through curated shelves, end-caps, and digital recommendation engines on e-commerce platforms, reinforcing their central role in category expansion.

Regional Insights

North America Malt Beverage Market Trends and Insights

North America is the leading regional market, holding around 41% global share in 2025 per the given scope, supported by a long-established beer culture and sophisticated retail and logistics infrastructure. In the United States, growth is increasingly driven by non-alcoholic, low-alcohol, and flavored malt beverages, reflecting shifting attitudes toward moderation, wellness, and variety. Non-alcoholic beer and malt drinks have been among the fastest-growing beverage segments, with several large brewers investing aggressively in alcohol-free lines and marketing campaigns that normalize moderate lifestyles.

The region is also a hub of premiumization and craft innovation, with thousands of craft breweries experimenting with specialty malts, barrel aging, and hybrid styles. Ready-to-drink (RTD) cocktails and hard seltzers, often based on flavored malt bases, have carved out a substantial share; U.S. RTD cocktail sales surpassed USD 1.0 billion mid-decade and continue to grow

Asia Pacific Malt Beverage Market Trends and Insights

The Asia Pacific malt beverage market is emerging as a high-growth region driven by rapid urbanization, rising disposable incomes, and evolving consumer lifestyles. Countries such as China, India, Japan, and South Korea are witnessing increasing demand for both alcoholic and non-alcoholic malt beverages. A young demographic profile and growing acceptance of western drinking culture are accelerating beer and flavored malt beverage consumption across urban centers. At the same time, non-alcoholic malt drinks are gaining traction, particularly in markets with cultural or religious restrictions on alcohol, as well as among health-conscious consumers seeking functional and energy-boosting alternatives.

Product innovation, including fruit-flavored variants and low-alcohol options, is further expanding the consumer base. Expansion of modern retail formats, e-commerce penetration, and strong distribution networks are improving product accessibility in tier-2 and tier-3 cities. Additionally, regional and international beverage manufacturers are increasing investments in local production facilities to reduce costs and strengthen market presence. With shifting preferences toward premium and craft offerings, Asia Pacific is expected to remain one of the fastest-growing and most dynamic regions in the global malt beverage market.

Competitive Landscape

The malt beverage market is highly competitive and moderately consolidated, characterized by strong global brewers and a growing presence of regional producers. Competition is driven by product innovation, flavor diversification, and expansion into low- and non-alcoholic variants to capture health-conscious consumers. Companies compete on pricing, brand positioning, packaging formats, and distribution strength across on-trade and off-trade channels. Premiumization and craft-style offerings are intensifying rivalry, particularly in urban markets. Strategic partnerships, acquisitions, and capacity expansions are common to strengthen geographic presence. Additionally, marketing campaigns and digital engagement play a crucial role in attracting younger consumers and building long-term brand loyalty in this evolving market.

Key Developments:

- In January 2026, Mahou San Miguel entered the Middle East market by launching a new non-alcoholic malt beverage, Vamos by Mahou, in Egypt, marking a strategic expansion of its international footprint with products tailored to regional consumer tastes.

Companies Covered in Malt Beverage Market

- Anheuser-Busch InBev

- Heineken N.V.

- Carlsberg Group, Molson Coors Beverage Company

- Diageo plc

- Asahi Group Holdings, Ltd.

- Kirin Holdings Company, Ltd.

- Boston Beer Company, Inc.

- Constellation Brands, Inc.

- Anadolu Efes Beverage Group

- Van Pur S.A.

- Royal Unibrew A/S

- Suntory Holdings Limited

- Nestlé S.A.

- PepsiCo, Inc.

- The Coca-Cola Company

Frequently Asked Questions

The global malt beverage market is expected to be valued at US$ 833.2 million in 2026 and is projected to reach US$ 1,458.8 million by 2033, reflecting a CAGR of 8.3% over the forecast period.

Key demand drivers include the health and wellness movement boosting non-alcoholic malt beverage consumption, premiumization and craft innovation, rising demand for diverse flavors, and growing interest in functional and clean-label formulations that deliver added health benefits.

North America is the leading regional market, accounting for about 41% of global share in 2025, driven by mature beer culture, strong retail and e-commerce infrastructure, and rapid growth in flavored and non-alcoholic malt beverage segments, especially in the United States.

The most significant opportunity lies in the Asia Pacific, where the malt beverages market is projected to grow from roughly USD 276.90 billion in 2023 to about USD 468.99 billion by 2030 at around 7.8% CAGR, along with functional malt beverages that integrate probiotics, fiber, vitamins, minerals, and natural ingredients to meet evolving wellness and lifestyle needs.

Major players include Anheuser-Busch InBev, Heineken N.V., Carlsberg Group, Molson Coors Beverage Company, Diageo plc, Asahi Group Holdings, Ltd., Kirin Holdings Company, Ltd., Boston Beer Company, Inc., Constellation Brands, Inc., Anadolu Efes Beverage Group, Van Pur S.A., and Royal Unibrew A/S, among others active in regional and niche segments.