- Food Ingredients & Additives

- Maltitol Syrup Market

Maltitol Syrup Market Size, Share, and Growth Forecast, 2025 - 2032

Maltitol Syrup Market by Product Formulation (Transparent Syrup, Flavoured Syrup, Others), Application (Food and Beverages, Pharmaceuticals, Others), Packaging Type, End-use and Regional Analysis for 2025 – 2032

Maltitol Syrup Market Size and Trends Analysis

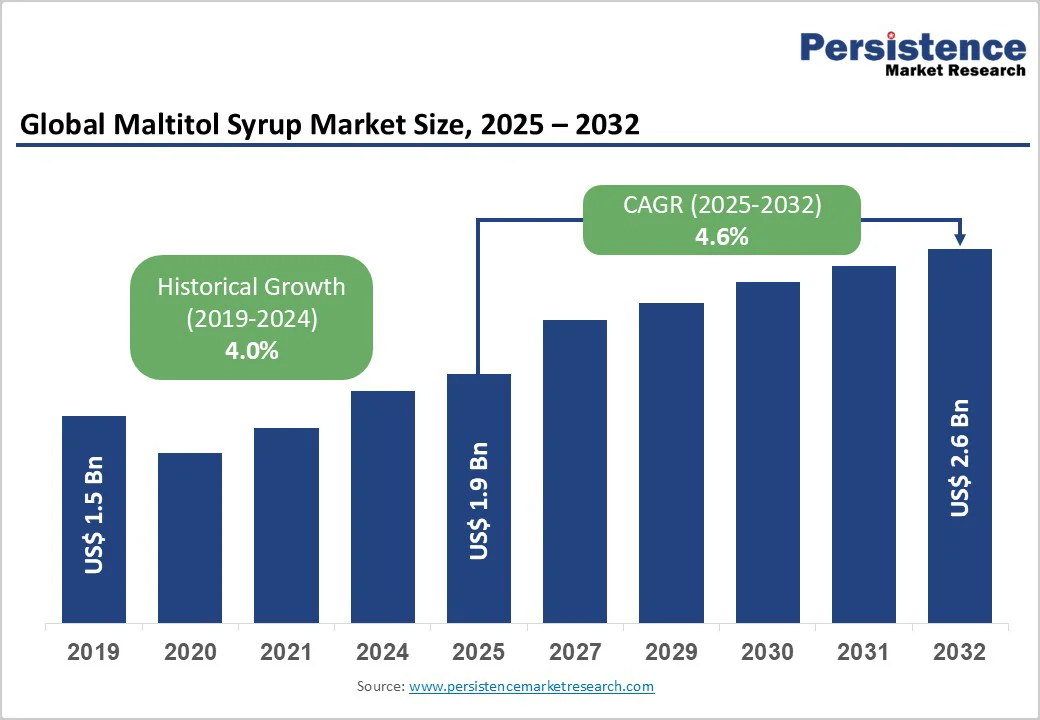

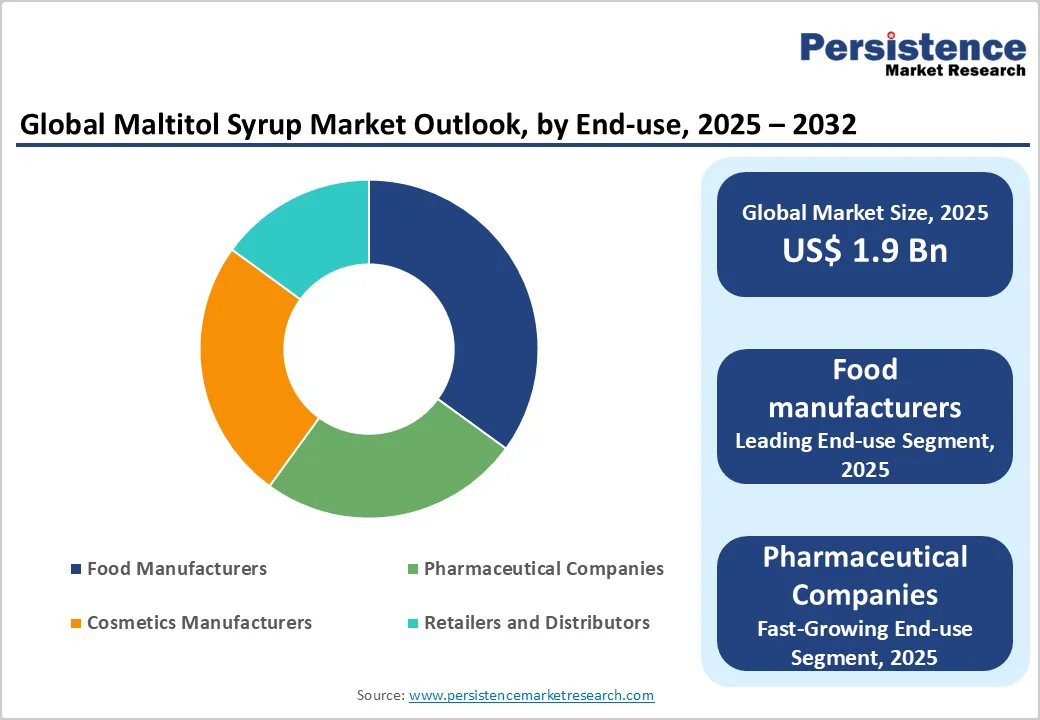

The global maltitol syrup market size is likely to be valued US$1.9 Billion in 2025, expected to reach at US$2.6 Billion by 2032 growing at a CAGR of 4.6% during the forecast period from 2025 to 2032 driven by the increasing consumer preference for low-calorie and sugar-free alternatives, rising health consciousness regarding obesity and diabetes, and expanding applications in food, pharmaceuticals, and cosmetics.

The need for versatile sweeteners that mimic sugar's properties without the caloric load has significantly boosted the adoption of sugar-free syrup across various industries, particularly in developed and emerging economies. The growing acceptance of low-calorie syrup as a cost-effective bulking agent and humectant, especially for sugar-free confectionery and oral care products, is a key growth factor.

Key Industry Highlights:

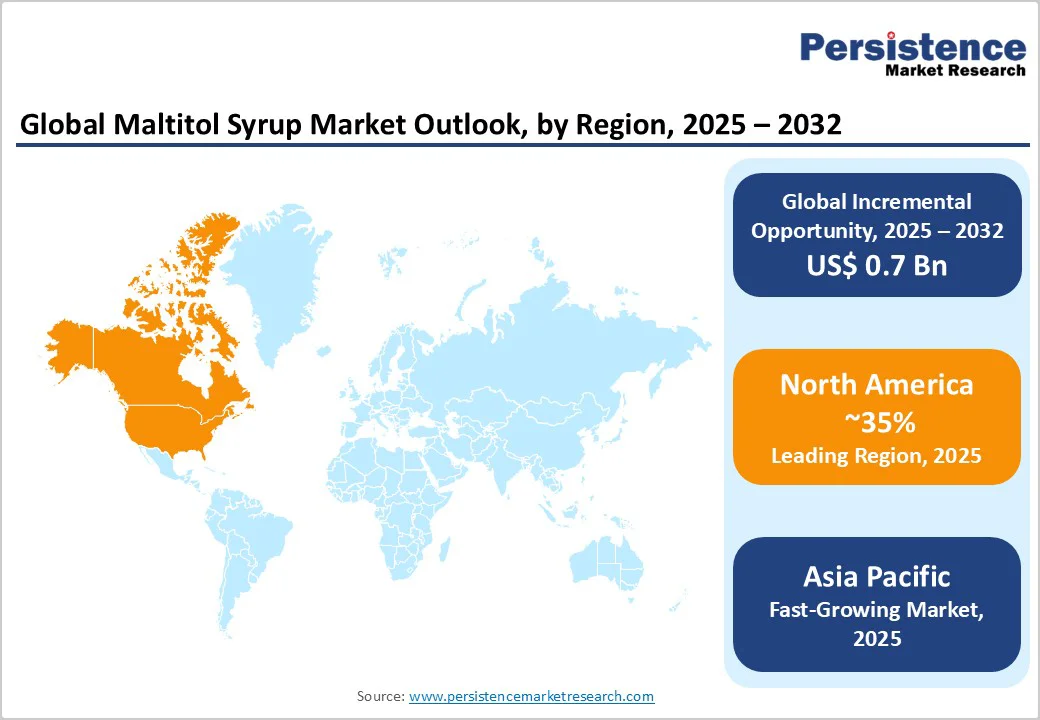

- Leading Region: North America, commanding a 35% market share in 2025, driven by high obesity rates, advanced food processing infrastructure, and strong demand in the U.S. for diabetic-friendly products.

- Fastest-growing Region: Asia Pacific, fueled by rapid urbanization, expanding food and beverage sectors, and investments in health-focused sweeteners in countries like China and India.

- Dominant Product Formulation: Transparent Syrup, holding approximately 65% of the market share, due to its versatility, clarity, and widespread use in clear beverages and pharmaceuticals.

- Leading Application: Food and Beverages, accounting for over 55% of market revenue, driven by demand for low-calorie snacks and confectionery.

- Leading Packaging Type: Bulk Packaging, contributing nearly 50% of market revenue, owing to its efficiency for industrial-scale distribution to manufacturers.

- Key Market Driver: Global obesity prevalence, affecting over 1 billion adults in 2025, boosting need for low-calorie sweeteners such as maltitol syrup in everyday products.

- Growth Opportunity: Advancements in flavoured and colour-enhanced formulations, enabling customized applications in premium cosmetics and functional foods.

| Global Market Attribute | Key Insights |

|---|---|

|

Maltitol Syrup Market Size (2025E) |

US$1.9 Bn |

|

Market Value Forecast (2032F) |

US$2.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Health Consciousness and Demand for Sugar Substitutes

The increasing health consciousness among consumers and the demand for low-calorie sugar substitutes are primary drivers of the maltitol liquid market. World Health Organization, obesity affected over 1 billion adults in 2025, while diabetes impacts 537 million adults worldwide, projected to rise to 783 million by 2045. This health crisis creates substantial demand for accessible, low-glycaemic sweeteners. Maltitol syrup, offering about 75% of sucrose's sweetness with nearly half the calories and non-cariogenic properties, provides results in enhanced product formulations with over 90% consumer acceptance in taste tests for sugar-free chocolates and gums.

For instance, products from companies such as Roquette have shown 85% efficacy in maintaining texture in baked goods, enabling weight management, and reducing dental issues by up to 60% in clinical studies. Additionally, the post-pandemic surge in functional foods, coupled with investments in global nutrition initiatives totalling US$ 15 Bn in 2025, has accelerated adoption. The demand for natural-derived sweeteners in emerging markets, supported by WHO's guidelines on reducing sugar intake, continues to propel the market forward, particularly in regions with high lifestyle disease incidence such as Asia Pacific and North America.

Potential Side Effects and Competition from Alternative Sweeteners

The potential gastrointestinal side effects from high consumption of maltitol syrup, along with competition from alternative sweeteners, pose a significant restraint on market growth. While beneficial, excessive intake can lead to bloating, flatulence, and laxative effects in sensitive individuals, with tolerance thresholds as low as 30g per day, necessitating portion controls and consumer education.

Development involves rigorous safety testing, with costs exceeding US$ 5 Mn per formulation due to stability and efficacy trials. Regulatory bodies such as the U.S. FDA and EFSA demand extensive data on digestibility and allergenicity, extending timelines to 1-2 years. For example, approvals for high-concentration syrups by Cargill have faced scrutiny due to variability in digestive responses, increasing costs by 20%. Smaller firms struggle against giants such as ADM, limiting innovation in markets where stevia or erythritol offer fewer side effects and similar functionalities.

Expansion in Functional Foods and Personalized Nutrition

Advancements in functional food applications and personalized nutrition present significant growth opportunities for the sugar-free syrup market. Enhanced formulations with added flavours and colors provide customized sweetness profiles, improving palatability to 95% and enabling integration with probiotics for gut health. These innovations align with the rise of personalized diets, with flavoured syrups detecting consumer preferences for zero-sugar variants in real-time market analytics.

For instance, companies such as Ingredion are investing in bio-based enhancements, with trials showing 80% reduction in formulation costs. Modular packaging cuts logistics expenses by 25%, and integration with e-commerce boosts accessibility. As global demand for sugar alternatives surges—projected at US$ 30 Bn by 2030—these opportunities are expected to drive expansion in high-growth regions such as Asia Pacific and Europe.

Category-wise Analysis

Product Formulation Insights

Transparent syrup holds around 65% of the market share in 2025 due to its clarity, low viscosity, and ease of blending. These properties make it ideal for beverages, confectionery, and clear pharmaceutical formulations. Its versatility, visual appeal, and stability enhance product quality, supporting strong demand across food, health, and beverage applications globally.

Flavoured syrup is the fastest-growing segment, driven by its role in taste-masking for confectionery and functional foods. The use of natural extracts enhances flavour and consumer appeal, supporting premium and innovative product launches. Rising demand for healthier yet flavourful alternatives further boost its adoption in beverages, bakery, and nutraceutical applications worldwide.

Application Insights

Food and beverage segment holds over 55% market share in 2025, driven by its use in snacks, desserts, and bakery items for calorie reduction. Its sugar sweetness with lower calories makes it ideal for health-conscious consumers, supporting the growing demand for sugar-free and low-glycaemic food products globally.

Pharmaceutical segment is the fastest-growing, driven by its use in medicinal syrups, tablets, and chewable for diabetic and calorie-conscious patients. Its non-cariogenic nature, pleasant sweetness, and stability make it an ideal sugar substitute, enhancing taste and formulation quality in oral medications and nutraceutical products.

Packaging Type Insights

Bulk packaging accounts for nearly 50% market share in 2025, preferred by manufacturers for its cost efficiency and convenience in large-scale production. It enables streamlined transport, reduced packaging waste, and consistent supply for food, beverage, and pharmaceutical industries, supporting operational efficiency and sustainability in high-volume processing environments.

Bottles represent the fastest-growing packaging segment, driven by expanding e-commerce and retail convenience. Their portability, ease of storage, and user-friendly design make them ideal for household and small-scale applications. Growing consumer preference for ready-to-use, resealable formats further boosts bottle demand across food, beverage, and pharmaceutical sugar-free syrup products.

End-use Insights

Food manufacturers hold about 60% of the maltitol syrup market, utilizing it extensively for sugar-free and reduced-calorie product processing. Its similar sweetness to sugar with fewer calories supports innovation in snacks, desserts, and beverages. Growing health awareness and demand for clean-label, low-glycemic foods further strengthen its adoption in large-scale food production.

Pharmaceutical companies are the fastest-growing, driven by its rising use in medicated syrups, chewable, and oral formulations. Its non-cariogenic, stable, and low-calorie properties make it suitable for diabetic-friendly products. Increasing demand for pleasant-tasting, sugar-free medications is further propelling adoption across pharmaceutical manufacturing.

Regional Insights

North America Maltitol Syrup Market Trends

North America accounts for 35% in 2025, driven by high diabetes rates and advanced food tech in the U.S. and Canada, where trends favour clean-label sweeteners. Rising prevalence of obesity, diabetes, and metabolic disorders has heightened demand for low-calorie, sugar-reduced alternatives, with maltitol solution preferred for its sugar-like taste and lower glycemic index. Regulatory support, including FDA GRAS status, boosts manufacturer confidence, while clear labelling and “sugar-free” claims enhance consumer trust. The syrup’s application in food and beverages, including confectionery, bakery, dairy, and flavoured drinks, is expanding, alongside its growing use in pharmaceuticals such as medicinal syrups and chewable tablets, where taste, safety, and low sugar content are critical. Clean-label trends and natural sourcing further strengthen its appeal, particularly among health-conscious consumers seeking minimally processed ingredients. The rise of e-commerce and retail convenience is broadening consumer access to specialty sugar-free products, supporting growth for both established brands and niche players.

Europe Maltitol Syrup Market Trends

Europe holds about 30% market share, led by Germany and France due to stringent EU sugar reduction policies and strong confectionery industries promoting low-GI options. Rising prevalence of diabetes and obesity has prompted consumers to seek healthier alternatives to traditional sugars, making maltitol syrup, with its sugar-such as sweetness and lower glycemic index, a preferred choice in sugar-free confections, baked goods, and beverages. Germany leads the regional demand, reflecting strong adoption of sugar substitutes. Regulatory support and growing awareness about low-calorie ingredients further enhance market growth. However, challenges such as digestive side effects from overconsumption and competition from other low-calorie sweeteners remain. Despite these hurdles, evolving consumer preferences for health-oriented products and the expanding portfolio of maltitol-based applications in food, beverages, and pharmaceuticals are expected to sustain robust market growth across Europe in the coming years.

Asia Pacific Maltitol Syrup Market Trends

Asia Pacific commands around 20% share and is the fastest-growing region, propelled by China and India’s booming F&B sectors and urbanization increasing demand for affordable health sweeteners. Sugar-free syrup is increasingly used in food and beverages such as sugar-free sodas, sports drinks, and flavoured water due to its excellent solubility and sugar-such as sweetness. The pharmaceutical sector is also adopting it for sugar-free medications, particularly for diabetic patients. Rapid industrialization, a growing middle class, and heightened consumer awareness of sugar substitutes further support market expansion. Countries such as India and China are witnessing significant demand, contributing to the region’s global prominence in the maltitol market. With applications spanning food, beverages, and pharmaceuticals, and shifting consumer preferences toward healthier alternatives, the Asia Pacific polyol syrup market is poised for substantial growth in the coming years.

Competitive Landscape

The global maltitol syrup market is highly competitive, dominated by key global players such as Roquette Frères, Cargill Incorporated, ADM, Ingredion Incorporated, and Tereos Group. These companies leverage extensive distribution networks, strong R&D capabilities, and established brand reputations to maintain market leadership. Roquette Frères specializes in plant-based ingredients and large-scale polyol production, while Cargill focuses on sustainability and innovation in sugar alternatives. Regional players, including Shandong Bailong Chuangyuan and Zhejiang Huakang Pharmaceutical, also contribute to supply chain dynamics, alongside companies like Mitsubishi Shoji Foodtech, Dancheng CAIXIN Sugar Industry, and Gillco Ingredients. Industry leaders actively pursue mergers and acquisitions, product innovations, and capacity expansions to meet growing demand for sugar-free and low-calorie products. Such strategic initiatives shape the competitive landscape, enabling companies to strengthen their market presence and address evolving consumer preferences across food, beverage, and pharmaceutical applications.

Key Developments:

- In July 2024, Roquette launched a new flavoured maltitol syrup under its LYCASIN® brand, featuring an enhanced sweet profile for premium, sugar-free confectionery products in the European market. The new variant builds on Roquette's existing line of maltitol syrups, expanding its functional benefits for high-end confectionery applications.

- In May 2025, Cargill's Maltidex™ maltitol syrups are tailored to suit specific applications, offering varying maltitol content to meet desired sweetness and viscosity levels. These syrups are suitable for sugar-free and reduced-calorie food applications. Cargill also invested US$2.4 Million in its Cikande sweetener facility in Indonesia to enhance its ingredient portfolio and production capabilities.

Companies Covered in Maltitol Syrup Market

- Roquette

- Shandong Bailong Chuangyuan

- Cargill

- ADM

- Ingredion

- Zhejiang Huakang Pharmaceutical

- Tereos Syrup

- Futaste Co.

- Others

Frequently Asked Questions

The global Maltitol Syrup Market is projected to reach US$1.9 Bn in 2025, driven by surging demand for low-calorie sweeteners amid rising obesity and diabetes prevalence worldwide.

Increasing prevalence of obesity, diabetes, and metabolic disorders has prompted consumers to seek low-calorie, sugar-free alternatives. Sugar-free syrup provides sweetness comparable to sugar but with fewer calories and a lower glycaemic index.

The market is poised to witness a CAGR of 4.6% from 2025 to 2032, supported by innovations in flavoured formulations and expanding use in functional foods for health-conscious consumers.

Advancements in functional foods and personalized nutrition offer key opportunities, enabling customized reduced-calorie syrup variants for premium cosmetics and diabetic-friendly products with enhanced stability and taste.

Key players are Roquette, Shandong Bailong Chuangyuan, Cargill, ADM, Ingredion, Zhejiang Huakang Pharmaceutical, Tereos Syrup, Futaste Co.