- Food Ingredients & Additives

- Digestion Resistant Maltodextrin Market

Digestion Resistant Maltodextrin Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Digestion Resistant Maltodextrin Market by Source (Corn-based, Wheat-based, Potato-based, Others), by Form (Powder, Liquid, Granular), by End Use (Food and Beverages, Pharmaceuticals, Dietary Supplements, Animal Feeds, Others), by Regional Analysis, 2026-2033

Digestion Resistant Maltodextrin Market Size and Share Analysis

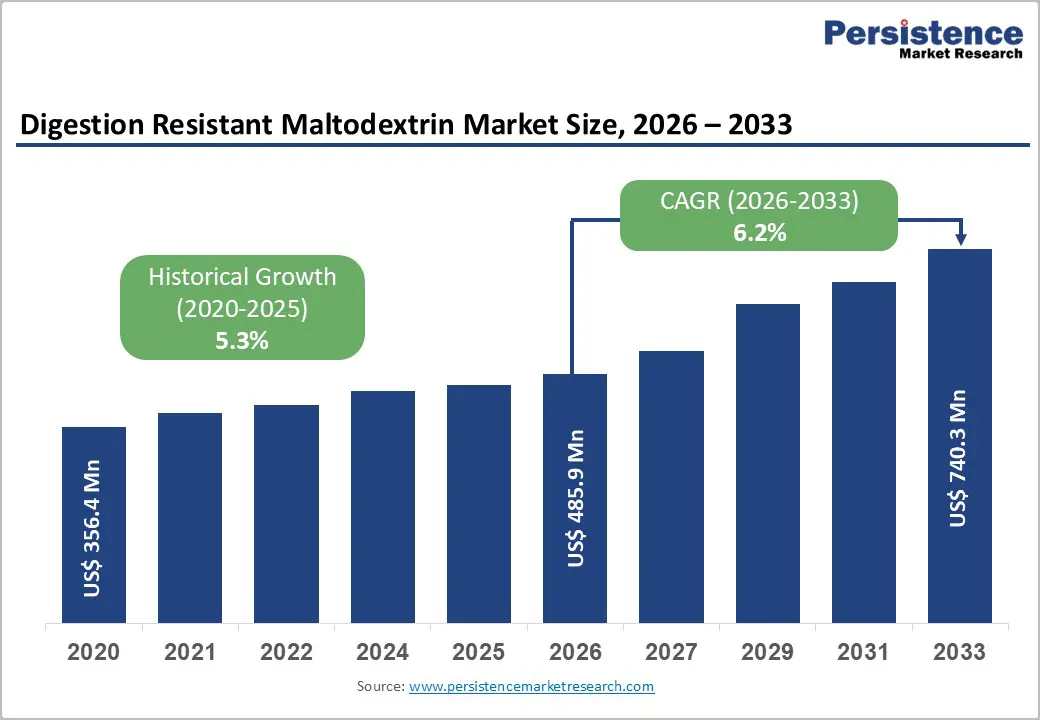

The global Digestion Resistant Maltodextrin market size is expected to be valued at US$ 485.9 million in 2026 and projected to reach US$ 740.3 million by 2033, growing at a CAGR of 6.2% between 2026 and 2033

The market is currently witnessing a transformative surge as health-conscious consumers pivot from simple carbohydrates to high-functionality dietary fibers. This growth is primarily underpinned by the ingredient's exceptional stability and neutral sensory profile, making it a preferred choice for food formulators aiming to bridge the fiber gap in modern diets. As regulatory bodies like the FDA and EFSA continue to validate its physiological benefits, the integration of digestion resistant maltodextrin into mainstream better-for-you products has moved from a niche health trend to a fundamental pillar of the functional food industry.

Key Industry Highlights

- Leading Region: Europe dominates with a 36% share, centered on the high-value white Digestion Resistant Maltodextrin markets in Germany and France.

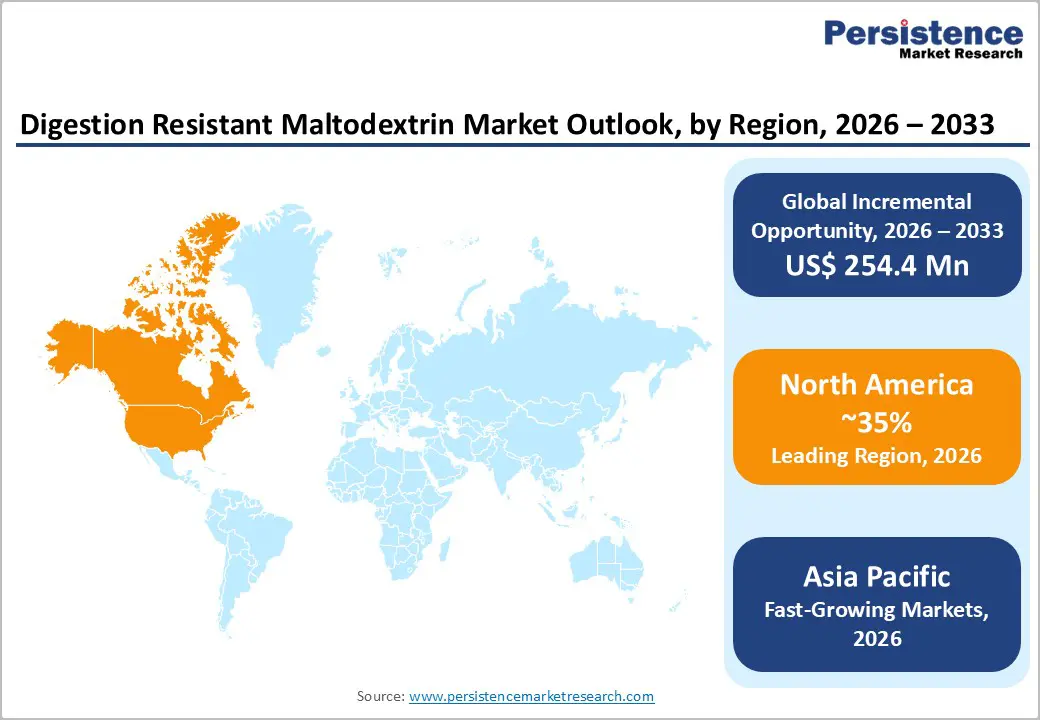

- Leading Region: North America leads with a 35% share, driven by a mature functional food market and favorable FDA regulatory definitions.

- Fastest Growing Region: Asia Pacific is the primary growth engine, fueled by the rapid expansion of the middle class and metabolic health concerns in China and India.

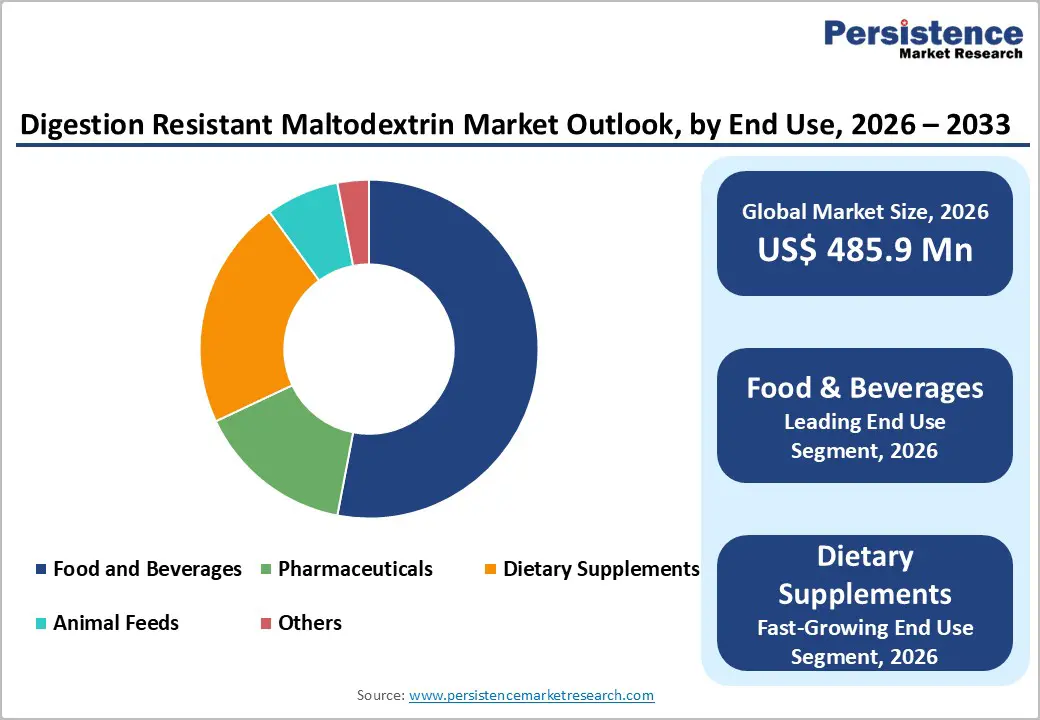

- Dominant Segment: The Food and Beverages segment is the largest user of resistant maltodextrin, essential for texture in low-sugar food formulations.

- Fastest Growing Segment: Dietary Supplements is the most dynamic category, reflecting the global trend toward preventative healthcare and prebiotic wellness.

- Key Market Opportunity: The development of fiber-fortified gummies and functional snacks offers a high-margin revenue pocket for new entrants and startups.

| Key Insights | Details |

|---|---|

| Digestion Resistant Maltodextrin Market Size (2026E) | US$ 485.9 Mn |

| Market Value Forecast (2033F) | US$ 740.3 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.3% |

Market Dynamics

Driver – Rising Demand for Functional Fibers in the Global Food Sector

The primary engine driving this market is the aggressive push by global food conglomerates to enhance the nutritional profile of processed goods without sacrificing taste. According to the World Health Organization (WHO), increasing dietary fiber intake is critical to combating the rising tide of non-communicable diseases. Digestion resistant maltodextrin (DRM) serves as a versatile solution, offering high solubility and a low glycemic response that appeals to the expanding diabetic and pre-diabetic populations. Manufacturers are increasingly utilizing DRM in products like meal replacements and sugar-reduced snacks to maintain texture while claiming high fiber status. This trend is particularly strong as consumers scrutinize labels for metabolic health benefits, prompting brands to reformulate their core offerings with digestion-friendly carbohydrates that support satiety.

Restraints – High Processing Complexity and Raw Material Sensitivity

Producing high-quality digestion resistant maltodextrin requires a sophisticated two-step process involving pyrodextrinization followed by precise enzymatic hydrolysis. This complexity leads to higher production costs compared to conventional maltodextrins or simple starches. Furthermore, the market is highly sensitive to price fluctuations in core raw materials like non-GMO corn and wheat. For instance, data from the USDA regarding agricultural yield volatility can directly impact the profit margins of ingredient suppliers. These high overheads often result in premium pricing at the retail level, which can deter cost-sensitive manufacturers in emerging economies from making the switch to resistant variants.

Opportunity – Explosive Potential in the Personalized Nutrition and Gummy Segment

The pill fatigue epidemic has created a massive opportunity for digestion resistant maltodextrin in the functional gummy and chewable supplement market. As consumers move away from traditional tablets, DRM is becoming a vital structural component in sugar-free gummies, providing the necessary body and chewiness while acting as a fiber fortifier. Since DRM has a high melting point and remains stable under diverse pH conditions, it is perfectly suited for the manufacturing of fortified treats that cater to Gen Z and Millennial health enthusiasts. Startups that focus on active lifestyle supplements can leverage DRM's satiety-promoting properties to create weight-management gummies that align with the proactive wellness trends dominating the current retail landscape.

Category-wise Analysis

Source Analysis

The Corn-based segment remains the dominant source for digestion resistant maltodextrin, holding an estimated 56% market share in 2025. This leadership is primarily due to the vast global availability of corn starch and the well-established supply chains in the United States and China. Corn-derived DRM is highly favored by manufacturers for its consistent molecular weight and high fiber yield, making it the most cost-effective option for large-scale food fortification. While Wheat-based and Potato-based variants are gaining ground, particularly in the European gluten-free and clean-label niches, corn's logistical advantages and proven performance in beverage applications ensure its continued dominance as the primary feedstock for the global market.

End Use Analysis

The Food and Beverages segment holds the largest portion of the market, accounting for 53% market share as of 2025. This leadership is driven by the massive consumer base for fiber-enriched cereals, dairy products, and non-alcoholic drinks. On the other hand, the Dietary Supplements segment is the fastest-growing area through 2032. As preventative healthcare becomes a global priority, the demand for dedicated fiber supplements that offer low-discomfort prebiotics is soaring. Unlike inulin, which can cause bloating, DRM is highly tolerated, making it the go-to choice for premium supplement brands focusing on chronic digestive issues and metabolic syndrome management.

Region-wise Insights

North America Market Trends and Insights

North America is the leading regional market, holding a 35% market share in 2025. The region's dominance is underpinned by a highly sophisticated functional food ecosystem and the strong presence of industry titans like ADM and Ingredion. The U.S. FDA's clear stance on the physiological benefits of resistant maltodextrin has paved the way for widespread commercial adoption.

The North American market is currently being reshaped by the sugar reduction mandate, with major soda and snack brands using DRM to maintain mouthfeel in zero-sugar formulations. Additionally, the region has a well-developed cold-chain and e-commerce infrastructure, allowing for the rapid distribution of innovative better-for-you products. The innovation ecosystem in the United States is particularly focused on high-performance sports nutrition, where DRM is used to provide sustained energy release without the glycemic spikes of traditional sugars.

Asia Pacific Market Trends and Insights

The Asia Pacific region is the fastest-growing market globally, projected to see a high CAGR through 2032. This growth is primarily fueled by the rapid urbanization in China, Japan, and India, alongside an escalating awareness of metabolic health. Japan is a pioneer in the FOSHU (Foods for Specified Health Uses) segment, where resistant maltodextrin has been a staple for decades.

In China and India, the rising middle class is moving away from traditional diets toward processed foods, creating a massive opportunity for fiber-fortified instant noodles, beverages, and infant nutrition. The manufacturing advantage in Asia Pacific is also significant; the region is a global leader in corn and wheat production, providing a localized and cost-efficient raw material base. As regional players like Luzhou and Baolingbao expand their capacity, the Asia Pacific region is set to become a global export hub for high-purity digestion resistant maltodextrin.

Market Competitive Landscape

The global digestion resistant maltodextrin market is consolidated, with the top five players Matsutani (ADM), Tate & Lyle, Roquette, Ingredion, and Cargill controlling a significant portion of the global production capacity. These leaders maintain their dominance through multi-year supply contracts and extensive R&D investments aimed at improving the clean-label status of their ingredients. Emerging business models are increasingly focused on vertical integration, with companies acquiring starch processing facilities to secure their supply chains. Key differentiators include the ability to provide clinical-grade data to back up fiber claims and the development of specialized instantized powders that offer superior solubility for premium consumer brands.

Companies Covered in Digestion Resistant Maltodextrin Market

- Tate & Lyle

- Roquette Freres S.A.

- Luzhou

- Ingredion Incorporated

- ADM

- Matsutani Chemical Industry Co., Ltd.

- Cargill Incorporated

- WGC Co., Ltd.

- Gulshan Polyols Ltd

- Baolingbao Biology Co. Ltd

- Tereos Syral S.A.S.

- Others

Frequently Asked Questions

The global Digestion Resistant Maltodextrin market is projected to be valued at US$ 485.9 Mn in 2026.

Rising Demand for Functional Fibers in the Global Food Sector is driving demand for Digestion Resistant Maltodextrin market.

The Global Digestion Resistant Maltodextrin market is poised to witness a CAGR of 6.2% between 2026 and 2033

Explosive Potential in the Personalized Nutrition and Gummy Segment is the key opportunity in the market.

The market is dominated by global ingredient giants such as Matsutani (ADM), Tate & Lyle, Roquette, Ingredion, and Cargill.