- Food Ingredients & Additives

- Maltitol Market

Maltitol Market Size, Share, and Growth Forecast, 2026 - 2033

Maltitol Market by Form (Liquid, Powdered), Application (Food and Beverage, Pharmaceutical, Personal Care, Other Industrial Uses), Distribution Channel (Offline Stores, Online Stores), and Regional Analysis 2026 - 2033

Maltitol Market Size and Trends Analysis

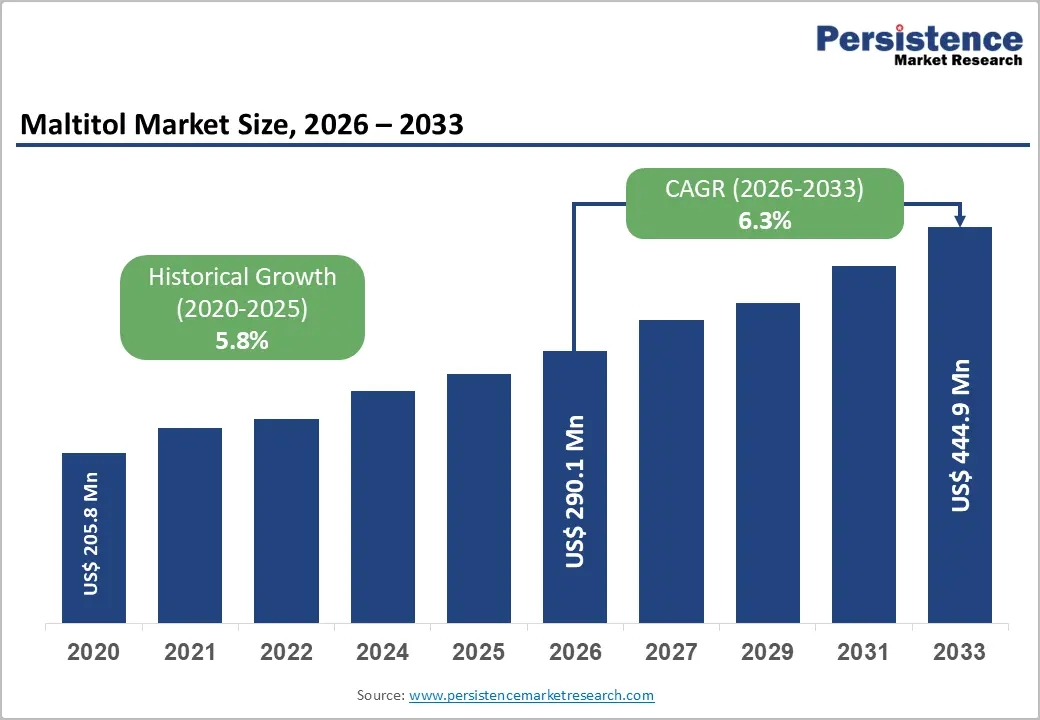

The global maltitol market size is likely to be valued at US$290.1 million in 2026 and is expected to reach US$444.9 million by 2033, growing at a CAGR of 6.3% during the forecast period from 2026 to 2033, driven by the increasing prevalence of metabolic disorders, which is accelerating the adoption of low-glycemic sweeteners across industrial food processing. Rising consumer preference for sugar-free and low-calorie alternatives is further supporting market expansion, particularly in food and pharmaceutical applications.

At the same time, global health initiatives aimed at reducing sugar intake are prompting manufacturers to reformulate high-calorie products using functional polyols. This ongoing shift is expected to sustain strong demand in the confectionery and pharmaceutical sectors over the coming years.

Key Industry Highlights:

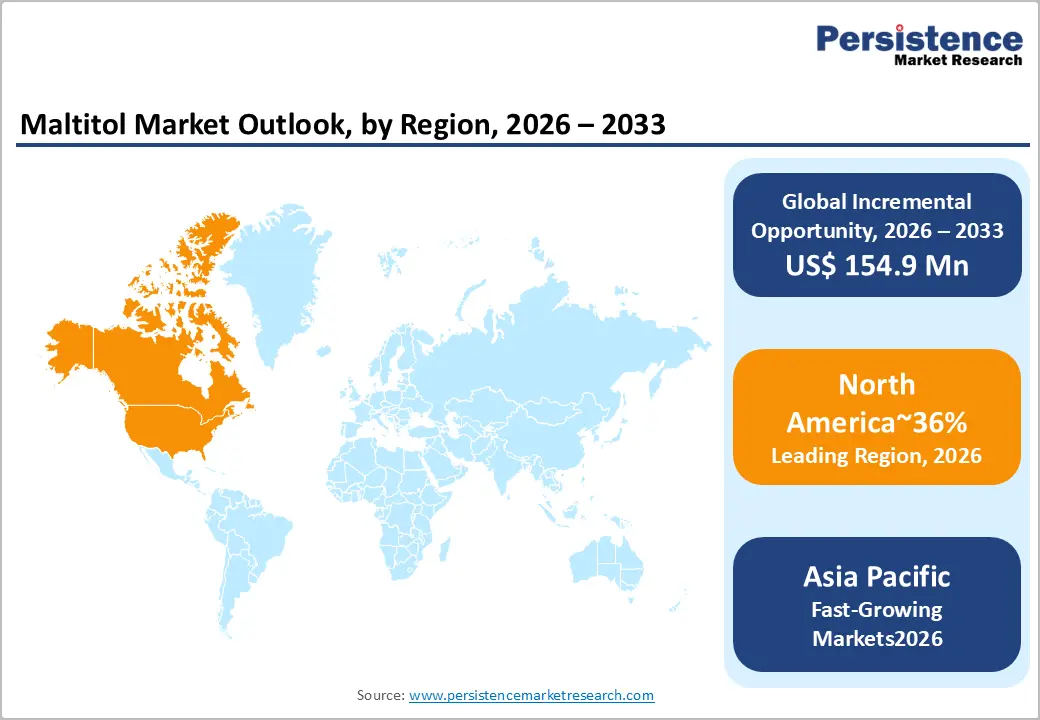

- Leading Region: North America is projected to lead, accounting for approximately 36% share in 2026, supported by high consumer awareness regarding caloric intake and a robust presence of specialized ingredient manufacturers.

- Fastest-growing Region: Asia Pacific is anticipated to grow fastest, driven by rapid urbanization and expanding healthcare infrastructure in emerging economies.

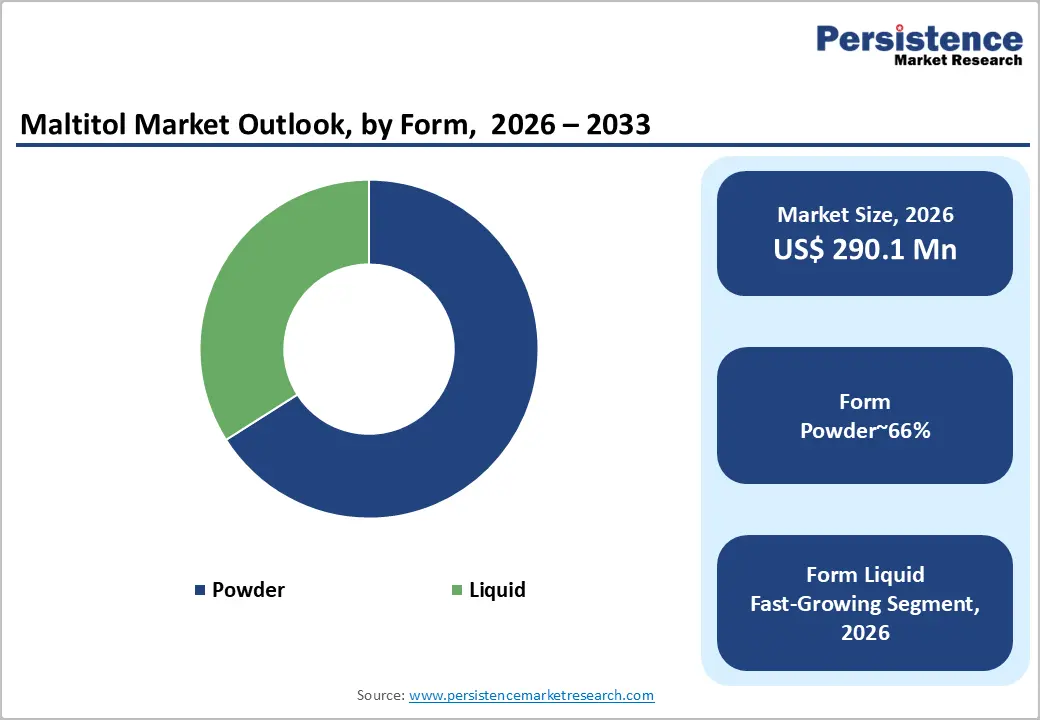

- Leading Form: The powdered segment is expected to lead, accounting for approximately 66% share in 2026, anchored by its high stability and seamless integration into dry-mix formulations.

- Leading Application: The food & beverage segment is anticipated to dominate, accounting for approximately 56% share in 2026, anchored by the massive demand for sugar-free confectionery and bakery products.

| Key Insights | Details |

|---|---|

| Maltitol Market Size (2026E) | US$290.1 Mn |

| Market Value Forecast (2033F) | US$444.9 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

Market Factors - Driver, Restraint, and Opportunity Analysis

Driver Analysis - Metabolic Health and Glycemic Management

The rising global incidence of diabetes is compelling food processors to utilize sweeteners with minimal insulinemic impact. Public health agencies are intensifying campaigns to reduce sucrose consumption in Western diets. This regulatory pressure is shifting the ingredient focus toward polyols that provide bulk without elevating blood glucose levels. Consumers are increasingly seeking out "no added sugar" labels on snacks and beverages. These health-centric purchasing patterns are projected to underpin long-term demand for stable crystalline sweeteners.

Strategic ingredient placement remains essential for maintaining the sensory profiles of sugar-free consumer goods. Roquette with SweetPearl enables manufacturers to replicate the crunch and mouthfeel of traditional sucrose in confectionery. This functional capability ensures that health-conscious products meet the taste expectations of mainstream buyers. Successful formulation strategies are positioned to capture expanding market share within the premium health-food segment. Ongoing clinical validation of low-glycemic benefits reinforces the credibility of these specialized bulk sweeteners.

Clean Label and Natural Sourcing

Food manufacturers are pivoting toward non-GMO and plant-derived ingredients to satisfy transparency requirements in modern labeling. Traditional synthetic sweeteners are losing favor as buyers prioritize recognizable sources in their dietary choices. The derivation of maltitol from maize or wheat starch aligns with these naturally occurring trends. Supply chains are adapting to provide traceable and sustainable raw materials for high-volume production lines. This transition is set to increase the utilization of maltitol in high-end artisanal and organic product ranges.

Reliability in the sourcing of raw starch remains a critical factor for industrial scalability. Cargill, with C*Maltidex addresses these transparency needs by providing documented supply chains for its polyol portfolio. Such transparency is set to strengthen partnerships between ingredient suppliers and global consumer brands. Enhanced labeling accuracy sustains trust among skeptical consumer groups in mature economic regions. These factors are poised to accelerate the transition from artificial additives to grain-based polyol solutions.

Restraint Analysis - Competition from High-Intensity Sweeteners

Emergence of high-intensity sweeteners such as stevia and monk fruit introduces competitive pressure on bulk polyol demand. These alternatives offer zero-calorie profiles while avoiding gastrointestinal concerns associated with sugar alcohol consumption. Clean-label positioning and minimal usage levels enhance their appeal within health-conscious consumer segments globally. Although maltitol provides bulk functionality, high-intensity sweeteners dominate applications requiring low dosage and high sweetness potency. This substitution dynamic reduces reliance on polyols within specific liquid and reduced-calorie product formulations.

Foodchem with Maltitol Solution faces competition as manufacturers adopt hybrid sweetening systems combining multiple ingredient classes. These systems optimize sensory performance while reducing overall polyol inclusion within finished product formulations. Reduced usage volumes directly impact procurement demand from large-scale food and beverage processors. Pricing advantages and functional efficiency of high-potency sweeteners further intensify competitive displacement effects. Consequently, innovation in alternative sweetening technologies continues to constrain growth prospects within traditional polyol segments.

Volatility in Agricultural Feedstock Prices

Maltitol production relies heavily on corn and wheat starch, exposing manufacturers to agricultural price fluctuations globally. Climate variability disrupts crop yields, introducing uncertainty in feedstock availability and procurement cost structures. Trade policies and export restrictions further destabilize supply chains, amplifying pricing volatility across international markets. Elevated input costs compress margins for ingredient processors, particularly within specialized polyol manufacturing operations. This economic instability limits competitiveness against conventional sucrose, especially in price-sensitive consumption regions.

Tereos with Maltilite leverages integrated agricultural networks to manage procurement risks and stabilize supply inputs. However, smaller producers lack such infrastructure, increasing vulnerability to sudden cost escalations. Financial pressure from raw material volatility can delay capital investments in capacity expansion and process optimization technologies. Long-term pricing contracts become difficult to sustain under fluctuating input cost conditions. As a result, market stability remains closely linked to global grain production performance and commodity pricing dynamics.

Opportunity Analysis - Oral Care Formulation Shifts

Rising preference for sugar-free oral care products is increasing demand for non-cariogenic sweetening agents across formulations. Maltitol supports anti-caries positioning by reducing plaque formation risk while maintaining acceptable taste profiles. Expansion into chewing gums and dental hygiene products strengthens its role within daily-use preventive care solutions. Consumer awareness initiatives and dental endorsements reinforce trust in sugar-free oral care product claims. These dynamics enhance integration of polyols within regulated personal care and hygiene product categories.

Roquette with Lycasint and Merck with Maltitol DC enable uniform dispersion within gel-based and semi-solid oral care formulations. Clinical collaborations with dental professionals support validation of efficacy and safety within product development frameworks. These partnerships enhance credibility and facilitate regulatory acceptance across healthcare-oriented consumer segments. Consistent product performance strengthens adoption within toothpaste, mouthwash, and medicated oral formulations. As preventive care gains prominence, demand for non-cariogenic ingredients continues to expand across personal care markets.

E-Commerce Bulk Packaging

Expansion of e-commerce channels is increasing demand for adaptable packaging formats suited for direct-to-consumer distribution models. Granular maltitol formats align with resealable packaging, supporting convenience in home baking and small-scale food preparation. Efficient logistics frameworks reduce handling costs while improving delivery reliability across dispersed consumer bases. Digital marketing strategies enhance product visibility, enabling targeted outreach within niche consumer segments. These developments support increased penetration of ingredient products within household consumption channels.

Subscription-based purchasing models encourage repeat consumption and stable demand patterns among end users. Packaging innovation ensures product stability while maintaining usability across extended storage durations. Integration with digital commerce platforms strengthens supply chain responsiveness and inventory management efficiency. Consequently, e-commerce expansion reinforces growth opportunities for maltitol within consumer-facing ingredient markets.

Category-wise Analysis

Form Insights

The powdered segment is expected to lead, accounting for approximately 66% share in 2026, underpinned by its exceptional physical stability and versatility in dry-mix industrial applications. This form is particularly valued for its ability to mimic the crystalline structure of sucrose, which is critical for the texture of chocolate and baked goods. High-purity crystalline versions facilitate easy handling and storage within large-scale manufacturing environments. Roquette with SweetPearl and Ingredion with Maltisweet exemplify the technical standard required for high-performance dry ingredients. Manufacturers prioritize this form to ensure consistent dispersion and mouthfeel in solid confectionery products. Ongoing investments in granulation technology further reinforce the segment's operational dominance. This structural alignment between ingredient functionality and industrial processing requirements sustains the leadership of powdered formats.

The liquid segment is anticipated to be the fastest-growing segment, driven by the increasing demand for convenient sweetening solutions in the beverage and dairy sectors. Fluid formats offer superior solubility, which eliminates the need for high-temperature dissolving processes during production. Manufacturers are increasingly integrating these syrups into sugar-free cough medicines and liquid nutritional supplements. Foodchem with Maltitol Solution addresses the need for high-clarity sweeteners in clear liquid applications. The shift toward automated liquid dosing systems in modern factories further accelerates the uptake of this format. As industrial efficiency becomes a primary competitive factor, the demand for pre-dissolved sweetening agents is expanding. This evolution in manufacturing workflow is positioning liquid variants for rapid commercial expansion.

Application Insights

The food & beverage segment is anticipated to lead, accounting for approximately 56% share in 2026, reinforced by the global transition toward sugar-reduced diets and healthy snacking. This segment remains the primary consumer of bulk polyols due to the massive scale of the confectionery and bakery industries. Maltitol provides the necessary volume and structural integrity that high-intensity sweeteners cannot replicate. Cargill with C* Maltidex and Tereos with Maltilite are deeply embedded in the supply chains of global snack manufacturers. The demand is anchored in the necessity to maintain flavor profiles while meeting stringent caloric reduction targets. Continuous innovation in sugar-free chocolate formulations continues to drive high-volume procurement. This convergence of consumer taste preferences and public health objectives sustains the application's market leadership.

Pharmaceuticals are forecast to be the fastest-growing segment, driven by the expanding requirement for non-cariogenic and low-glycemic excipients in medicated products. The sector is increasingly adopting polyols to improve the palatability of pediatric medicines and geriatric health supplements. Maltitol serves as a stable coating agent for tablets, providing a smooth finish and a pleasant taste without the risks associated with sugar. The rise in chronic conditions requiring long-term medication is fueling the demand for sugar-free pharmaceutical vehicles. Enhanced regulatory focus on drug stability and patient compliance is further pushing manufacturers toward specialized polyol solutions. This strategic shift in medicinal formulation is accelerating segment growth across all major markets.

Regional Insights

North America Maltitol Market Trends

North America is expected to remain the leading regional market, accounting for approximately 36% share in 2026, supported by high levels of health consciousness and a mature food processing industry. The region's dominance is anchored in the early adoption of sugar reduction policies and a robust regulatory framework for food additives. Large-scale confectionery manufacturers are continuously reformulating products to cater to the growing diabetic population. Sustained investments in research and development for alternative sweeteners remain a hallmark of the regional market. High disposable income levels also support the demand for premium sugar-free artisanal products across urban centers.

The U.S. is expected to anchor regional momentum through the extensive presence of major ingredient players and strict FDA labeling mandates. American consumers are increasingly scrutinizing ingredient lists for added sugars, which is driving the demand for polyol-based alternatives. Roquette with SweetPearl is frequently utilized by domestic brands to meet the high standards of the North American confectionery market. Government-led health initiatives are further incentivizing the food industry to lower the caloric density of processed goods. This alignment between public policy and corporate strategy is projected to maintain the country's central role in the global market.

Asia Pacific Maltitol Market Trends

Asia Pacific is expected to register the fastest growth trajectory, as rapid urbanization and the expansion of the middle class accelerate the demand for Western-style convenience foods. The region is witnessing a significant shift in dietary habits, leading to a rise in lifestyle-related health concerns. Governments are responding with sugar taxes and health awareness campaigns, which are compelling manufacturers to seek sucrose alternatives. The presence of large-scale manufacturing hubs in emerging economies is facilitating the localized production of bulk sweeteners. This industrial expansion is anticipated to lower production costs and increase the affordability of sugar-free products for the general population.

China is anticipated to anchor regional growth through its massive food and beverage manufacturing base and increasing focus on public health. The Chinese government’s "Healthy China 2030" initiative is promoting the reduction of sugar intake across the nation. Mitsubishi Shoji Foodtech with Lesys is actively expanding its footprint to cater to the rising demand for functional ingredients in East Asia. Rapid growth in the local pharmaceutical sector is also contributing to the uptake of high-purity maltitol for medicinal use. The country's expanding e-commerce infrastructure is making specialized sweeteners more accessible to a broader consumer base. These factors are set to sustain China's role as a primary engine for regional market acceleration.

Europe Maltitol Market Trends

Europe is expected to remain a mature and structurally stable regional market, with demand primarily anchored in stringent food safety regulations and a strong tradition of bakery production. The region exhibits a sophisticated understanding of functional ingredients, with consumers prioritizing non-GMO and plant-based sweeteners. European manufacturers are leaders in the development of high-quality sugar-free chocolates and functional snacks. The market is supported by well-established supply chains for grain-based starches, ensuring a steady supply of raw materials for maltitol production. Persistent focus on dental health and obesity prevention continues to drive the utilization of polyols in public procurement programs.

Germany is expected to drive European demand through its advanced pharmaceutical and food processing sectors that prioritize technical precision. The country’s commitment to "clean label" products is forcing manufacturers to adopt traceable and sustainable sweetening solutions. Tereos with Maltilite is a key player in providing high-grade polyols to the German confectionery industry. Robust investments in bio-based chemicals are supporting the expansion of the local ingredient market. Regulatory pressure from the European Food Safety Authority ensures that all maltitol applications meet the highest safety standards. This focus on quality and compliance reinforces Germany's position as a regional hub for ingredient innovation.

Competitive Landscape

The global maltitol market is consolidated, with leadership concentrated among global ingredient suppliers such as Roquette, Cargill, and Ingredion. These leaders maintain influence through advanced fermentation capabilities and stringent compliance with global food and pharmaceutical standards. Their scale enables consistent production of high-purity maltitol across multiple regions, ensuring supply chain reliability. Deep procurement relationships with multinational manufacturers position them as strategic partners in product reformulation initiatives. Their technical expertise and application support establish benchmarks for functionality, quality, and regulatory adherence.

Competitive positioning is defined by specialization in high-functionality grades and increasing vertical integration across raw material sourcing. Premium players emphasize pharmaceutical-grade purity and non-GMO sourcing, while others focus on cost-efficient solutions for bulk applications. Companies such as Mitsubishi Shoji Foodtech and Tereos advance differentiated offerings targeting niche and premium end-use segments. Innovation is shifting toward hybrid sweetening systems combining polyols with natural high-intensity alternatives. Industry dynamics include strategic collaborations with biotechnology firms to enhance fermentation efficiency and product consistency.

Key Industry Developments:

- In September 2025, Caldic partnered with Ingredion to distribute maltitol and other polyols across Brazil, expanding availability and enabling faster development of lower-sugar products while strengthening regional reach.

- In March 2025, Cargill inaugurated a corn milling plant in Madhya Pradesh, India, to support its sweetener and starch portfolio and strengthen raw material supply for local maltitol production.

Companies Covered in Maltitol Market

- Roquette Frères

- Cargill, Incorporated

- Ingredion Incorporated

- Archer Daniels Midland (ADM)

- Tereos S.A.

- Südzucker AG

- Tate & Lyle PLC

- BENEO GmbH

- Associated British Foods (ABF)

- Mitsubishi Shoji Foodtech

- Merck KGaA

- SPI Pharma

- Batory Foods

- Foodchem International

- NutraFood

- Fructofin (Tereos)

Frequently Asked Questions

The global maltitol market stands at US$290.1 million in 2026. It is projected to reach US$444.9 million by 2033. This growth reflects sustained demand for sugar alternatives.

Sugar reduction mandates in food and pharma propel expansion. Low-calorie properties enable texture replication without health drawbacks. Consumer shifts toward functional products amplify this trend.

The maltitol market is projected to grow at a CAGR of 6.3% during the forecast period. Structural demands in beverages and excipients underpin this rate. Channel diversification supports steady acceleration.

North America leads with approximately 36% share in 2026. Mature infrastructure and regulations anchor this position. Food processing hubs drive consistent procurement.

Key players include Roquette Frères, Cargill, Ingredion, BENEO, and Tate & Lyle. They focus on powdered and syrup forms for food and pharma. Their innovations shape market standards.