- Food Ingredients & Additives

- Liquid Egg Whites Market

Liquid Egg Whites Market Size, Share, and Growth Forecast 2026 - 2033

Liquid Egg Whites Market by Nature (Pasteurized, Refrigerated, Frozen), by End Use (Food & Beverage, Dietary Supplements, Sports Nutrition, Dairy & Frozen Desserts, Others), by Sales Channel (B2B, B2C), by Regional Analysis, 2026-2033

Liquid Egg Whites Market Share and Trends Analysis

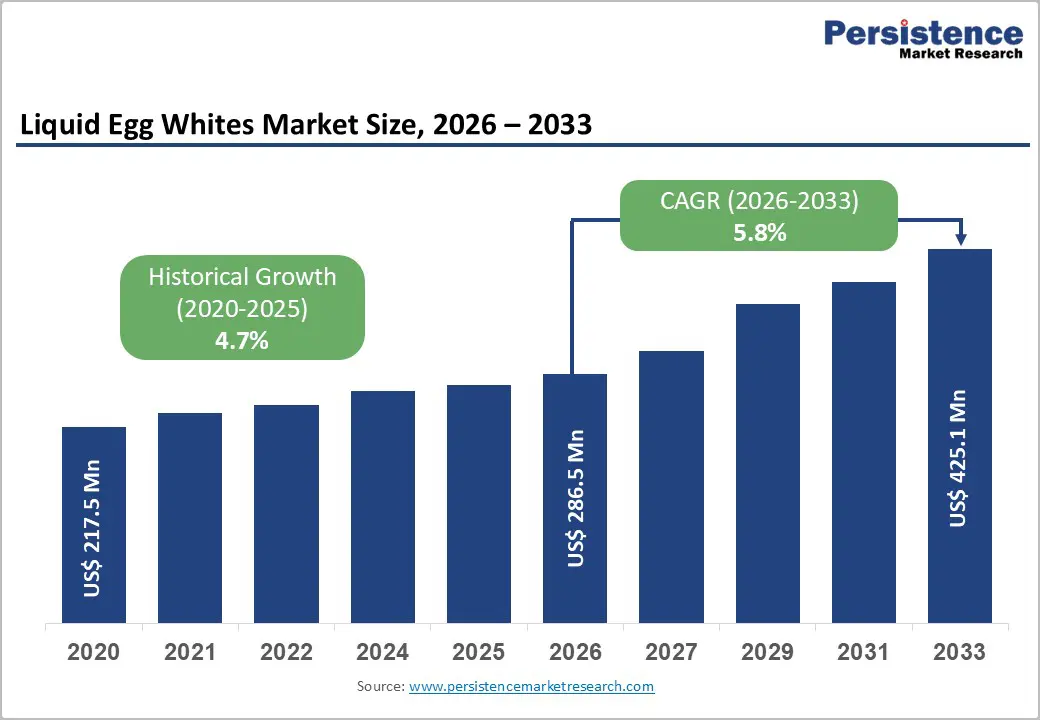

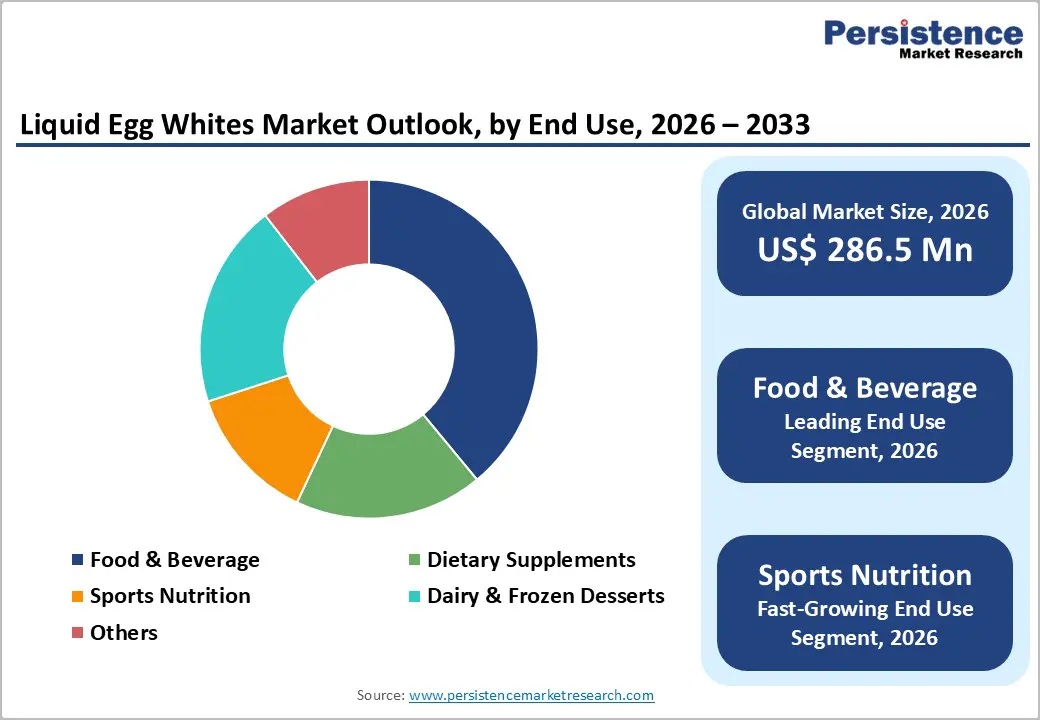

The global Liquid Egg Whites market size is expected to be valued at US$ 286.5 million in 2026 and projected to reach US$ 425.1 million by 2033, growing at a CAGR of 5.8% between 2026 and 2033.

The global liquid egg whites market is evolving from a processing convenience ingredient into a value-driven protein category shaped by food safety, performance nutrition, and ready-to-use applications. Shifts in consumption habits, regulatory focus, and innovation in formats are redefining growth priorities across regions and end uses.

Key Industry Highlights

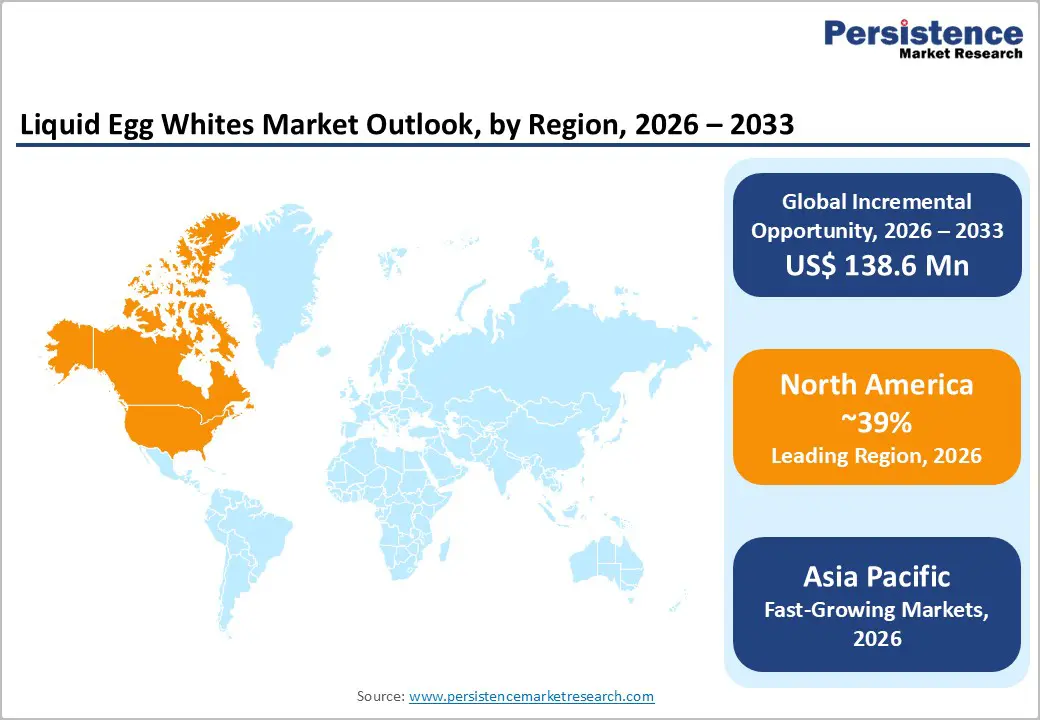

- Leading Region: North America, holding approximately 39% market share, supported by advanced food processing infrastructure, high protein intake, strong foodservice demand, and rapid adoption in sports nutrition and convenience-focused prepared foods.

- Fastest-Growing Region: Asia Pacific, driven by modernization of bakery and foodservice operations in India, rising fitness-oriented protein consumption in China, and specialized nutrition applications in Japan and South Korea.

- Fastest-Growing End Use Segment: Sports Nutrition, fueled by increasing demand for lean, fast-digesting, lactose-free protein sources in ready-to-mix and ready-to-drink formats targeting active and performance-focused consumers.

- Market Drivers: Expanded use of liquid egg whites in bakery, confectionery, and prepared foods due to operational efficiency, consistent functionality, reduced contamination risk, and scalability in high-volume manufacturing.

- Opportunities: Innovation in flavored and fortified liquid egg white beverages enables premium positioning, direct-to-consumer reach, and differentiation for key players and new entrants targeting on-the-go protein consumption.

- Key Developments: In April 2025, Eurovo acquired a majority stake in the Two Chicks egg white brand, strengthening its footprint in value-added egg ingredients and consumer-focused protein products.

| Key Insights | Details |

|---|---|

| Global Liquid Egg Whites Market Size (2026E) | US$ 286.5 Mn |

| Market Value Forecast (2033F) | US$ 425.1 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.7% |

Market Dynamics

Driver – Expanded use of liquid egg whites in bakery, confectionery, and prepared foods

Cracking efficiency is becoming a competitive advantage as food manufacturers streamline operations. Liquid egg whites offer consistency, portion control, and reduced contamination risk, making them increasingly attractive for industrial bakery and confectionery production. Their functional properties support aeration, binding, and structure in cakes, meringues, fillings, and desserts. Prepared food producers value liquid formats for speed, reduced labor, and predictable performance across large batches.

Rising demand for protein-enriched baked goods and ready meals further accelerates adoption. Liquid egg whites integrate seamlessly into high-volume processing lines, supporting scalable production without shell waste. Shelf-stable handling under refrigeration improves inventory planning for foodservice operators. As convenience-driven food categories expand globally, liquid egg whites strengthen their role as a reliable, functional protein ingredient across commercial kitchens and packaged food manufacturing ecosystems.

Restraints – Price Volatility and Animal-Welfare Concerns

Egg pricing remains structurally volatile due to feed cost fluctuations, disease outbreaks, and seasonal production cycles. These variables directly affect liquid egg white pricing, creating margin uncertainty for processors and downstream buyers. Manufacturers face challenges in long-term contract pricing, especially when supply disruptions ripple through poultry supply chains.

Animal-welfare scrutiny adds another layer of complexity. Growing consumer concern around cage systems pressures producers to transition toward cage-free sourcing, increasing production costs. Compliance with evolving welfare standards demands capital investment, certification, and operational adjustments. Smaller processors often struggle to absorb these costs, limiting scalability. As transparency expectations rise, brands reliant on conventional egg sourcing encounter reputational and cost-related risks that can restrain broader market expansion.

Opportunity – Innovation in flavored and fortified egg white beverages targeting on-the-go consumers

Protein consumption is shifting toward convenience, creating fertile ground for drinkable nutrition formats. Liquid egg white beverages offer high protein density, low fat, and fast absorption, aligning well with on-the-go lifestyles. Flavor innovation improves palatability, overcoming traditional taste barriers associated with egg-based products. Fortification with electrolytes, vitamins, or functional ingredients enhances appeal for active consumers.

For key players and startups, this segment enables brand differentiation beyond commodity ingredients. Ready-to-drink formats support premium pricing and direct-to-consumer distribution models. Shelf-life extension technologies further expand retail and fitness channel access. As demand for portable protein rises across urban populations, flavored and fortified egg white beverages represent a scalable opportunity for value-added growth and category expansion.

Category-wise Analysis

Nature Analysis

Pasteurized Liquid Egg Whites holds approx. 84% market share as of 2025, reflecting strong emphasis on food safety and regulatory compliance. Pasteurization reduces microbial risk while preserving functional properties essential for baking, beverages, and prepared foods. This processing step enables widespread adoption across foodservice, industrial manufacturing, and institutional catering.

Manufacturers prefer pasteurized formats due to extended shelf life and simplified handling protocols. Regulatory acceptance across major markets further reinforces dominance, especially in applications involving vulnerable consumer groups. Pasteurization supports consistent quality, reduces liability concerns, and enables broader distribution through chilled supply chains. As food safety standards tighten globally, pasteurized liquid egg whites remain the default choice for large-scale and premium food applications.

End Use Analysis

Sports Nutrition are projected to grow at a CAGR of 10.3% during the forecast period as demand for lean, fast-digesting protein accelerates. Liquid egg whites appeal to athletes seeking high biological value protein without fats or carbohydrates. Their liquid format supports rapid absorption and flexible dosing in shakes and functional beverages.

Fitness brands increasingly incorporate egg whites into clean-label formulations targeting muscle recovery and weight management. Absence of lactose broadens appeal among sensitive consumers. Ready-to-mix and ready-to-drink formats fit training routines and on-the-go consumption patterns. As performance nutrition shifts toward minimal processing and transparent sourcing, liquid egg whites strengthen their position within sports-focused dietary solutions.

Region-wise Insights

North America Liquid Egg Whites Market Trends and Insights

North America holds approximately. 39% market share in the global Liquid Egg Whites Market, supported by mature food processing infrastructure and strong protein consumption trends. In the United States, demand rises from sports nutrition, foodservice chains, and convenience-focused meal solutions. Clean-label positioning and allergen awareness reinforce usage across packaged foods.

Canada contributes through steady egg production and adoption of pasteurized formats in institutional catering. Investments in cage-free transitions influence sourcing strategies across the region. Cross-border supply chains enhance availability while supporting export-oriented growth. As regulatory oversight and wellness-driven consumption intensify, North America remains a key innovation hub for liquid egg white applications.

Asia Pacific Liquid Egg Whites Market Trends and Insights

Asia Pacific Liquid Egg Whites Market is expected to grow at a CAGR of 10.9% as protein consumption modernizes. In India, adoption increases within bakery chains and hospitality kitchens seeking efficiency. China shows rising use in protein beverages and functional foods aligned with fitness trends.

Japan emphasizes precision nutrition and elderly-friendly formulations, supporting controlled protein intake formats. South Korea integrates liquid egg whites into convenience foods and fitness-oriented snacks. Regional growth is supported by expanding cold-chain infrastructure and foodservice modernization. As urban lifestyles intensify, liquid egg whites gain relevance as a practical protein source across diverse culinary applications.

Market Competitive Landscape

The global Liquid Egg Whites Market is moderately consolidated, led by vertically integrated egg processors and ingredient suppliers. Leading companies invest in pasteurization efficiency, quality certifications, and product consistency to secure long-term B2B contracts. Sustainability initiatives focus on cage-free sourcing, waste reduction, and energy-efficient processing.

Product innovation targets extended shelf life and application-specific formats. Strategic partnerships with foodservice operators and nutrition brands strengthen demand stability. Vertical integration enhances cost control and supply security. Compliance with evolving food safety and animal-welfare regulations shapes competitive positioning. As buyers prioritize reliability and transparency, operational scale and regulatory alignment increasingly define market leadership.

Key Developments:

- In April 2025, Eurovo acquired a majority stake in the Two Chicks egg white brand, strengthening its presence in the value-added egg ingredients and consumer protein products segment.

Companies Covered in Liquid Egg Whites Market

- ТМ Ovostar

- Bob Evans Farms

- Abbotsford Farms

- Egg Whites International

- Muscle Egg

- Organic Valley

- Eazy Egg

- TwoChicks

- Uncle Jack's

- Kings Farm Foods Limited

- Others

Frequently Asked Questions

The global Liquid Egg Whites market is expected to reach around US$ 286.5 million in 2026.

Expanded use of liquid egg whites in bakery, confectionery, and prepared foods is key demand driver in the Liquid Egg Whites market.

North America leads the Liquid Egg Whites market with about 39% share in 2025.

Innovation in flavored and fortified egg white beverages targeting on-the-go consumers is the key opportunity for key players in the market.

Key players include ТМ Ovostar, Bob Evans Farms, Abbotsford Farms, Egg Whites International, Organic Valley, Kings Farm Foods Limited, and others